It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

In a blow for green shipping, the e-fuel maker Liquid Wind AB has entered bankruptcy administration and will be sold off, raising questions about the future of its methanol plant project pipeline. The industry already faces a supply shortage, and it is as-yet unclear where adequate quantities of e-fuels will come from in order to power shipping's green transition.

Liquid Wind is a specialist in e-methanol, an energy storage process that takes renewable energy and uses it to create a physical commodity - a liquid fuel, suitable for running an internal combustion engine. It is particularly suitable for hard-to-abate industries like shipping, where high energy density and long endurance between refueling stops are fundamental requirements.

The process requires a source of CO2; if the CO2 is derived from biomass combustion, the resulting product is fossil-free and net carbon-neutral. Liquid Wind has six different combined heat and power projects in its sights, each offering a plentiful stream of biogenic CO2 which could be captured and turned into methanol (using plenty of electricity, clean water and a bit of chemistry). It had hoped to have 10 projects under way by 2030, each producing about 100,000 tonnes of green methanol annually; given the low gravimetric energy density of methanol, the output of each plant would be enough to run one ULCV container ship for roughly 125-250 days of steaming, depending upon speed.

On Monday, Liquid Wind was declared bankrupt, and its management was handed to a court-appointed trustee. The entirety of the business is up for sale, including its Finnish and Swedish subsidiaries. The firm did not provide further details.

The bankruptcy comes despite many notable successes - partnerships with major industrial brands like Alfa Laval and Siemens Energy, a successful $44 million equity raise, project sponsorship from the Swedish Energy Agency, and financing from big names like Samsung Ventures and Uniper.

Just days before the announcement, Liquid Wind had submitted its environmental permit application for a project at a combined heat and power plant at Ornskoldsvik. The new e-methanol facility was designed to take biogenic CO2 from a biomass-fueled powerplant on the waterfront, output e-methanol, and provide district heating to nearby buildings using the waste heat from the process. The fuel for the powerplant comes mostly from forest industry waste products, and the electricity would come from nearby renewable-energy projects.

"With strong local collaboration and integration with Ovik Energi’s CHP plant, we can deliver locally produced volumes of sustainable eMethanol—especially in sectors where alternatives are still limited and reliance on imported fossil fuels remains high," said founder and then-chief executive Claes Fredriksson on May 5.

Hapag-Lloyd Calls Q1 "Unsatisfactory" While Warning of Uncertainty

Hapag-Lloyd points to considerable uncertainty and highly volatile markets based on freight rates and the conflict in the Middle East (HL)

Hapag-Lloyd was the latest carrier to report dramatically lower first quarter financial results. Reporting that the company swung to a financial loss for the quarter, management called the quarter’s performance "unsatisfactory" but maintained its financial outlook for the full year.

The world’s fifth-largest container carrier, which is poised to leap forward with the pending acquisition of Zim, said the near-term outlook remains subject to “considerable uncertainty due to highly volatile development of freight rates and the conflict in the Middle East.” While sounding cautious over the challenging, volatile market environment, management told investors the second quarter of 2026 was seeing some improvements. It said the company was experiencing stronger cargo volumes and "healthy" forward booking trends.

“The first quarter of 2026 was unsatisfactory for us, with weather-related supply chain disruptions and pressure on freight rates leading to significantly lower results,” said Rolf Habben Jansen, CEO of Hapag-Lloyd. He cited a nearly one percent decline in volumes while reporting the average freight rate fell 9.5 percent on weaker demand.

The company also pointed to operational disruptions during the first quarter. It said bad weather conditions in Europe and North America had caused disruptions in terminal operations and supply chain issues. Like all of the carriers, it also experienced issues with geopolitical issues and specifically the blockade of the Strait of Hormuz. In late April, the company said it still had four vessels stuck in the Persian Gulf. One ship, however, was able to make the transit during one of the lulls in the fighting. One other ship had come off charter while waiting in the Persian Gulf.

Hapag reported an 18 percent decline in first quarter revenues to $4.8 billion for its shipping segment and $4.92 billion for the group. The company also swung to financial losses on both an EBITDA and group profit level, reporting that overall profit went from $469 million in Q1 last year to a loss of $256 million this year.

Volumes, however, remained stable during the quarter at approximately 3.2 million TEU, which the company noted was largely on par with the year ago. Further, Jansen said the Gemini network (partnership with Maersk) had proven its resilience even under difficult conditions, helping the company to maintain a reliable service offering. The financial results were also helped by the weaker U.S. dollar, which contributed to a reported six percent decline in costs. Costs would have increased 4.6 percent if adjusted for currency.

While a smaller portion of the overall group, Hapag’s terminal operations helped to offset the pressures in ocean shipping. Revenues from its terminals were up for the quarter, in part due to the first incorporation of its acquisition of India’s JM Baxi into the results. Hapag also said it had strong volumes in both Latin America and India.

While Jansen expects the markets will continue to be highly volatile, he said Hapag was moving forward on its strategy while also maintaining rigorous cost controls.

Hapag maintained its financial forecast, which projects group EBIT in the range of a loss of $1.5 billion to a profit of $500 million for the full year.

CMA CGM Pledges $800 Million Funding to Kenya’s Mombasa Port

Mombasa, Kenya looks to expand its port capabilities with the CMA CGM investment (KPA)

CMA CGM has announced an investment of $800 million in Kenya’s Mombasa Port. The deal was signed on the sidelines of the Africa Forward Summit in Nairobi early this week, co-hosted by France with President Emmanuel Macron in attendance.

The investment will go into upgrading two Mombasa Container Terminals at a time when the Kenyan port is seeing increased cargo flows. Last year, Mombasa Port handled 2.11 million TEUs, recording a growth of 5.5 percent from the previous year.

With these record cargo levels, Mombasa port is said to be operating at almost its full capacity. This has prompted the Kenyan government to introduce some reforms, including transitioning the port into a landlord model. In April, the National Treasury said that it had opened up several Kenya Ports Authority (KPA) assets to private investors. These include Mombasa Port Container Terminal II (berths 20-22) and Mombasa Port Container Terminal (berths 23-224).

The CMA CGM investment is likely happening under this arrangement, as the company has pledged to reinforce its logistics and maritime capacities in East and Central Africa. Mombasa Port is a trade gateway for East Africa’s landlocked countries, including Rwanda, Uganda, and South Sudan.

While Mombasa Port attracted the French deal, Kenya’s greenfield port of Lamu also celebrated an operational milestone this week. The port received MV Baltimore Express, the largest containership to ever dock at any port in East and Central Africa. The Post-Panamax vessel, measuring 369 meters in length, arrived from Oman’s Salalah port. The vessel is operated by the German shipping line Hapag-Lloyd. The vessel is at the port to restow some of the dangerous cargo onboard. In 2025, Lamu’s cargo volume rose by over 900 percent, from 74,380 tons in 2024 to 799,161 tons last year. The growth can be partly attributed to the port’s rising transshipment role.

CMA CGM added that its funding for Mombasa port development follows its recent opening of an African regional office in Abidjan, Côte d'Ivoire. In the past few years, CMA CGM has become heavily involved in port upgrades on the African continent. In Nigeria, for instance, the company is part of the 100 percent electric barge project at the Lekki Deep Sea Port. In Egypt and Morocco, the company has also invested in container terminal infrastructure.

A startup confronts water shortages by pulling it out of the air

The large metallic white box sits in a Southern California parking lot, looking unremarkable until water starts flowing from a hose attached to it. Peer inside, though, and it’s nearly empty but for some wires, tubes and a container of light-colored material.

The water isn’t being conjured out of thin air by magic but by MOFs— metallic organic frameworks. MOFs are nanocrystalline structures engineered at an atomic level to attract specific molecules. In this case that’s H2O and the machine made by startup Atoco is silently harvesting molecules from the surrounding air and storing them in the material’s porous cavities that serve as microscopic water tanks.

Atoco founder Omar Yaghi shared the 2025 Nobel Prize in chemistry for pioneering MOFs and on an April morning he gave Bloomberg News an exclusive demonstration of the commercial prototype of its atmospheric water harvesterin the lot outside the company’s Orange County laboratory.

In the wake of the Iran war, interest in the technology has risen as the giant desalination plants that supply water to tens of millions of people in the Middle East have become military targets. “There’s a new realization of the vulnerability and security risk of centralized water systems,” said Samer Taha, Atoco’s chief executive officer, who is based in Irvine, California.

Set to go into production later this year,the shipping container-sized machine will produce up to 4,000 liters (1,057 gallons) of water daily and can be installed at data centers, hospitals and other critical infrastructure. An off-the-grid model that operates on ambient sunlight and produces less water can be deployed to communities where water must now be trucked in.

“This becomes absolutely essential in alleviating the problems we are facing on our planet in terms of water scarcity,” said Yaghi, 61, a University of California at Berkeley chemistry professor who started Atoco in 2021.

Climate change is only intensifying those risks as drought and heat waves dry up rivers and reservoirs, with half the global population experiencing water shortages, according to the United Nations. In the US, Colorado River flows that supply water to 40 million people are declining dramatically amid record-low snowpack. Communities across the country are battling artificial intelligence data centers that threaten to drain already depleted aquifers while nearly a million Californians lack access to safe drinking water largely due to agricultural pollution. Some 500,000 people in Corpus Christi, Texas, face running out of water next year from a lack of rain.

“You’re going to see more Corpus Christis around the world,” said Wendy Jepson, who researches water security at Texas A&M University, adding that crumbling infrastructure and poor policy decisions are exacerbating the water crisis.

Those cities have few options to acquire water. One is to build plants to desalinate seawater, a multibillion-dollar, years-long undertaking that requires enormous amounts of electricity and harms marine life.

“You have societies and economies that are highly dependent on desalination with few backups and alternatives,” said David Michel, a senior associate for water security at the Center for Strategic and International Studies. He said atmospheric water harvesting is unlikely to replace desalination in the near term but “seems very well placed to extend the water supply.”

Atoco’s technology, which can operate in arid climates, promises the advent of a new decentralized water source, just as solar panels and batteries have allowed homeowners and businesses to tap the sun and insulate themselves from an increasingly unreliable power grid.

For instance, in Ethiopia, where many residents have sporadic access to water, an off-the-grid Atoco atmospheric harvester could supply about eight households in a village. It would take around a dozen of the machines to service a water-efficient data center in California.

Yaghi, the son of Palestinian refugees, grew up in Jordan in a one-room dwelling shared with nine siblings and the family’s cows. The house had no electricity or running water and his task as a child was to fill as many containers as he could find when the government delivered water to his village every week or two.

“We want everyone on our planet to have water independence where you’re in control of your own water,” said Yaghi. “We’re showing this today to show the power of being able to harness an infinite resource of water that is the air.”

The unassuming appearance of the water harvester prototype belies its mind-bending physics. Largely constructed of common elements such as carbon, nitrogen, hydrogen, copper and aluminum, an ounce of MOF material can contain the surface area of a soccer field. (Imagine crumpling up a sheet of paper. It’s now a fraction of its original size but contains the same surface area within the folds.)

After the MOFs invisibly gather H2O, the harvester rumbles to life to apply heat to the material to dislodge the molecules. A condenser converts the water vapor into liquid, which starts pouring from a slender tube. Yaghi fills a glass for Taha and then grinning, drinks from the hose before handing a glass to Gray Davis, Atoco’s legal advisor and a former California governor.

There’s so much water in the atmosphere – more than all the world’s lakes and rivers – that’s constantly being replenished that harvesting H2O wouldn’t disrupt that cycle, according to Atoco.

Atoco expects to make and sell 200 harvesters in 2027.The company isn’t taking orders yet, but it said it has more expressions of interest in purchasing the machines than current production capacity. Samer said the company has been testing the machine with partners around the world, including in the desert southwest of the US. Atoco hasn’t disclosed pricing though it notes the production model will be capable of supplying water for a few cents a liter, which is more expensive than desalinated water.

But since the MOFs only attract H2O molecules, the water is free of PFAS, microplastics and other contaminants often found in the water supply. Atoco and competitor AirJoule Technologies are targeting data centers and semiconductor plants, which need pure water for cooling and manufacturing but often seek to operate in water-stressed communities.

“They’re under all kinds of pressure for water,” said AirJoule Chief Executive Officer Matt Jore, whose company expects to begin production later this year of a MOF-based atmospheric water harvester that can produce 2,000 liters a day. He said the company, a joint venture with GE Vernova, is testing its technology in the Middle East and has seen a spike in interest from the region since the Iran war.

In the US, atmospheric water harvesting could help alleviate water strains from the AI boom, according to Jepson, the Texas A&M professor. “If this kind of technology can be integrated into data centers, you’re offloading the pressure on water systems for people, which potentially is a really huge gain,” she said.

(By Todd Woody)

COAL

Sandvik Ground Support inks deal to establish local US manufacturing joint venture

Sandvik has signed an agreement to form a joint venture with Alpha Metallurgical Resources (NYSE: AMR) through which it will establish local manufacturing for its ground support business in the US market.

In addition to the joint venture, in which Sandvik will hold a 51% stake and Alpha 49%, the setup also includes a long-term exclusive supply agreement with Alpha.

“Re-entering the US ground support market with a local manufacturing presence is strategically important, and this initiative will allow our ground support business to strengthen customer relationships, shorten lead times and build a scalable platform for long-term growth in North America,” said Mats Eriksson, president of Sandvik Mining.

“Creating this joint venture with Sandvik is a step in securing our supply chain by manufacturing more of our mining materials here in Central Appalachia,” said Andy Eidson, chief executive officer of Alpha Metallurgical Resources. “We are excited about the expected benefit to Alpha and, more broadly, to West Virginia.”

Production is planned at a new 100,000-square-foot facility in West Virginia, primarily focused on rock bolt and resin capsule manufacturing, but with potential to expand the product offering over time.

In addition to the long-term supply agreement with Alpha, the joint venture will also support sales to third-party customers.

Alpha is a leading US-based producer of high-quality metallurgical coal, which is a critical component in traditional steel production. With a portfolio of mining operations primarily located in Central Appalachia, Alpha serves a global customer base across North America, Europe, South America and Asia.

POTASH/FERTILIZER

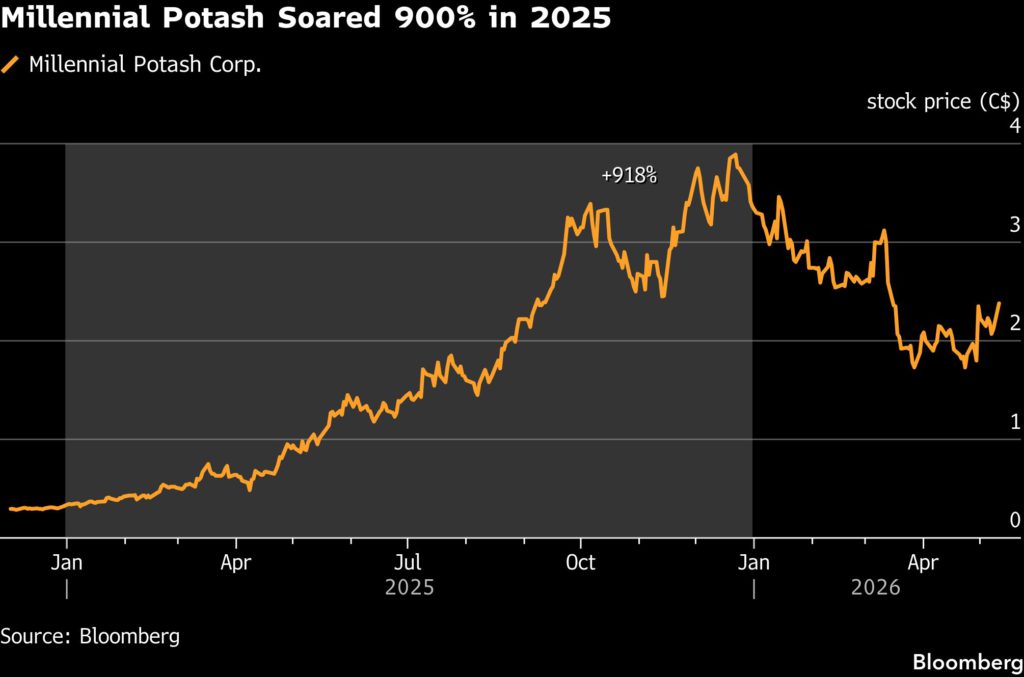

Family offices build stake in niche miner after stock soars 900%

Millennial Potash Corp. is advancing the Banio project, a large-scale potash development along Gabon’s southern coast. Credit: Millennial Potash Corp.

For decades, the risky world of early-stage mining ventures was the playground of institutional funds and commodity trading houses. But after a more than 900% rally in a little-known Canadian potash developer last year, a new class of investors is moving in: family offices.

Millennial Potash Corp. has attracted a group of ultra-high-net-worth clans that are increasingly bypassing traditional funds to take direct stakes in critical resources. Potash, a potassium-rich salt, is a fertilizer for crops ranging from cereals to potatoes, helping boost yields and plant resilience. The Vancouver-area miner is developing a potash project in Gabon and has no other revenue.

“We have actually seen very unusual interest coming from family offices,” said chairman Farhad Abasov. “Usually, we don’t see a lot of this capital coming into the junior mining sector.”

The investment push is led by The Quaternary Group, a Singapore-based investment entity representing Ross Hamou-Jennings, the former Asia chairman of Cargill Inc., the commodities and agriculture giant. Quaternary owns roughly 25% of the potash miner, and Hamou-Jennings is using his industry knowledge to bridge a valuation gap he identified in the company. He views potash as an essential, $30 billion niche market where global powers like the US and China lack self-sufficiency. The US added potash to its list of critical minerals in November, boosting Millennial’s shares.

The Banio project plans to use the deep-water port at Mayumba, along the west coast of Africa. That will allow shipments to reach major markets like Brazil while bypassing traditional choke points, according to Millennial’s website.

Despite a pullback after last year’s 900% surge, the company has a market value of about C$313 million ($228 million). SCP Research rates the stock a “buy,” banking on Abasov’s proven track record at Potash One and Allana Potash to drive the next phase of growth.

Millennial Potash shares rose 1.5% in early trading in Toronto Wednesday, trimming losses this year to 20%.

Another backer is Hong Kong’s Cavendish Investment Corp. This multi-family office, which generally invests between $5 million and $50 million, views fertilizers as strategic assets critical to navigating increasingly fractured global supply chains.

These firms are part of a growing club of private wealth that prefers direct ownership over managed funds. Colombia’s richest man, Jaime Gilinski, has repeatedly increased his stake in independent oil and gas producer GeoPark Ltd., seeing it as a vehicle to enter Venezuela’s recovering energy sector. Similarly, the heirs of Swedish tycoon Adolf Lundin spent nearly C$40 million in March to boost holdings in copper and diamond miners amid supply-chain squeezes.

Beyond Quaternary and Cavendish, Millennial Potash’s investor list is populated by family offices operating just below public disclosure thresholds. The company has attracted investments from a Canadian family office, a US-based office and another wealthy family from the Persian Gulf, all holding just under 5%, according to Abasov. He is talking to family offices in Hong Kong and Singapore to drum up more investor interest.

Jean-Sebastien Jacquetin, managing partner at Cavendish, notes that families are increasingly moving beyond passive investments.

“Sometimes families aren’t just managing wealth – they are active operators in sectors like mining, healthcare, or renewables,” said Jacquetin. “Given the current geopolitical environment and the war, people are going back to fundamentals.”

Many of these family offices, including Quaternary and Cavendish, already have a niche background in commodities.

Hamou-Jennings said he prefers to own large, direct stakes in bottleneck resources. Apart from Millennial Potash, he has invested in P2 Gold Inc., a Canadian precious metals explorer, and Surge Battery Metals Inc., another penny stock based in the Vancouver area.

“It is clearly happening,” Hamou-Jennings said of the rising interest from family offices in the natural resource space. “It seems to be increasing in Asia; I think it was more common a year ago in North America.”

He notes that many families wait too long to pull the trigger on these early-stage companies. “They shouldn’t think they can wait for the project to de-risk at a higher valuation and still get a private placement, because at that point, the company just won’t need the money,” he said.

Cavendish, the multi-family office run by the former chairman of a Hong Kong jewelry company, is heavily involved in commodities and metals. In August, the firm told Bloomberg that it was allocating roughly a third of its portfolio to the physical gold trade.

(By Diana Li)

Cameco halts Saskatchewan uranium operations after floods

A view of the area around Cameco’s McArthur River mine. (Image courtesy of Cameco.)

Canada’s Cameco (TSX: CCO)(NYSE: CCJ) has temporarily halted production activities at its Key Lake mill and reduced activity at its McArthur River mine after flooding damaged transport infrastructure in northern Saskatchewan.

The uranium producer said its sites were not directly affected by flooding, but the collapse of the Smoothstone River Bridge disrupted the primary route used to move supplies to McArthur River and Key Lake. Restrictions on an alternative road have also limited Cameco’s ability to reroute deliveries.

Cameco said it will not resume full operations until normal deliveries of critical operating materials can restart. The timeline remains unknown.

“If the Key Lake mill is down for a full month, McArthur River would almost certainly be forced into a total production halt,” Uranium Equities analysts said. They estimated the direct production impact could be about 1.5 million pounds of uranium.

The analysts said McArthur River’s slurry tanks and mobile truck containers can hold only about seven to 10 days of full production.

Cameco said the Cigar Lake mine continues to operate and its consolidated annual production plan remains unchanged. The company warned, however, that prolonged road restrictions and continued disruption to deliveries of critical operating materials could affect the 2026 production outlook for the McArthur River/Key Lake operation.

Any production shortfall may force the company to buy or borrow uranium to meet commitments, potentially weighing on free cash flow, BMO analyst Alexander Pearce said in a note.

Disruptions at McArthur River — one of the world’s largest uranium mines and a major contributor to global supply — could further tighten an already undersupplied uranium market and support spot uranium prices, Pearce added.

Kazzinc says its Zinc plants are running at reduced capacity after blast

Furnace operators at Glencore’s Kazakhstan precious metals refinery. Image: VisMedia

Mining company Kazzinc said on Tuesday that its zinc and lead plants at the Ust‑Kamenogorsk metallurgical complex in eastern Kazakhstan were operating at a reduced capacity after an explosion last week.

Three people were killed and five others injured in the explosion at Kazzinc’s zinc plant in Ust‑Kamenogorsk. The company, Kazakhstan’s largest producer of zinc, lead and precious metals – owned by Glencore – did not disclose how output has been affected.

Kazzinc said clean-up operations at the site and an investigation into the incident were ongoing.

(By Maiya Gordeyeva and Maxim Rodionov; Editing by Andrew Osborn)

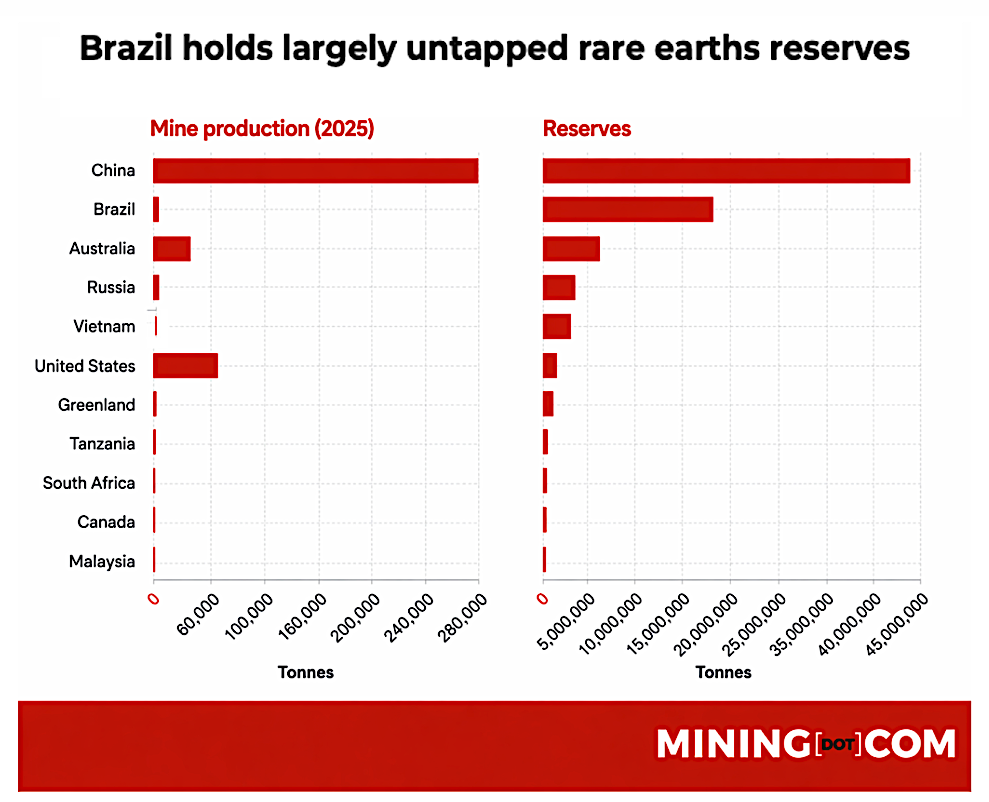

US President Donald Trump and his Brazilian counterpart Luiz Inácio Lula da Silva are forging an unlikely partnership around rare earths as Washington races to loosen China’s grip on critical mineral supply chains.

Their improvised White House meeting last week underscored how geopolitical competition over strategic minerals is reshaping alliances, with Brazil emerging as one of the few countries capable of helping the US diversify supply away from China.

Lula told Trump that Brazil’s vast rare-earth reserves are open to investment from any country willing to process minerals domestically, while Trump sought to signal renewed US engagement in Latin America ahead of a key China trip. The April agreement by Oklahoma-based USA Rare Earth to acquire Serra Verde Group for $2.8 billion highlighted the scale of the opportunity.

“The Lula-Trump meeting was less a bilateral reset than a bid to keep a politicised relationship manageable,” Mariano Machado, principal Americas analyst at Verisk Maplecroft, said in a note. “Among the items discussed, critical minerals emerged as the one topic where both leaders can claim a win without resolving deeper political tension.”

Reality-check

Yet Brazil’s long history with rare earths suggests the geopolitical enthusiasm may far exceed the industry’s near-term reality. Despite holding the world’s second-largest rare-earth reserves, the country has struggled for decades to turn geological potential into sustained production. Environmental licensing delays, bureaucratic hurdles, volatile commodity prices and periodic waves of resource nationalism have repeatedly stalled projects.

Mining companies can spend five to 10 years securing permits, while growing public opposition following deadly tailings dam disasters in Minas Gerais has hardened scrutiny of new developments.

The tensions expose a broader disconnect between global ambitions for critical minerals and local resistance to mining expansion. Rare earths are increasingly viewed as essential for semiconductors, AI infrastructure, electric vehicles and military technologies, but communities near prospective projects often see limited benefits and mounting environmental risks. Machado said the Serra Verde transaction illustrates both the opportunity and the constraints facing the two countries.

“The concrete test is Serra Verde in Goiás, Brazil’s only commercial-scale rare earths operation,” he said. “USA Rare Earth’s proposed $2.8 billion acquisition gives Washington a route into Brazilian production. But Lula’s message after meeting Trump was clear: Brazil has ‘no veto’ over US participation, yet also no intention to offer preferential access.”

Brazil’s Congress is advancing legislation that includes a $2 billion guarantee fund and $5 billion in tax credits to encourage domestic processing of critical minerals. Lula told Trump the country wants investment and technology transfer while ensuring more value-added processing remains domestic. Machado said that balancing act risks turning commercial development into a sovereignty debate that could slow approvals and delay investment.

“Critical minerals are not the simplest part of the bilateral agenda, even if they are the most practical,” he said. “Washington is going all-in on alternatives to China across rare earths, niobium, graphite, lithium, nickel and copper; while Brasília wants investment, technology transfer and domestic processing, without surrendering control over strategic resources.”

Second only to China

Brazil holds roughly 21 million tonnes of rare-earth reserves, second only to China and the Brazilian Mining Association projects $2.4 billion in rare-earth investment by 2030 as part of a broader $21.3 billion critical minerals pipeline.

But execution remains the central challenge. Licensing delays, land disputes, environmental scrutiny and limited processing capacity continue to cloud timelines for new developments.

“The risk for both sides is a development opportunity shifting into a de facto sovereignty debate, slowing approvals and dragging out business timelines,” Machado said. “This means Brazil can become a strategic rare earths supplier to the US — but not quickly nor on US terms alone.”

Race for critical minerals leaves EU struggling to keep up

Sunny footpaths under the Sandberg hill, Bratislava, Slovakia. Stock image.

For the European Union, the fate of a Cold War-era mine near Bratislava is becoming a litmus test for its ambition to break free from China’s chokehold over critical minerals.

Sitting in a wooded range of hills in Slovakia known as the Little Carpathians, the so-called Trojarova project is where Soviet engineers first discovered a rich seam of antimony in the 1980s. Its owners, Canada-based Military Metals Corp, are pitching the facility as a chance for Europe to secure access to an uncommon metal used in military equipment.

For crucial resources such as antimony, EU nations appear unable put up the money and act, leaving projects such as Trojarova open to being snapped up by rivals. So far, Military Metals hasn’t secured an offtake agreement from the bloc.

As US President Donald Trump prepares for summit talks in Beijing this week — and threatens to raise tariffs on Europe — the project serves to illustrate the dangers of getting left behind in a hotly contested race between superpowers.

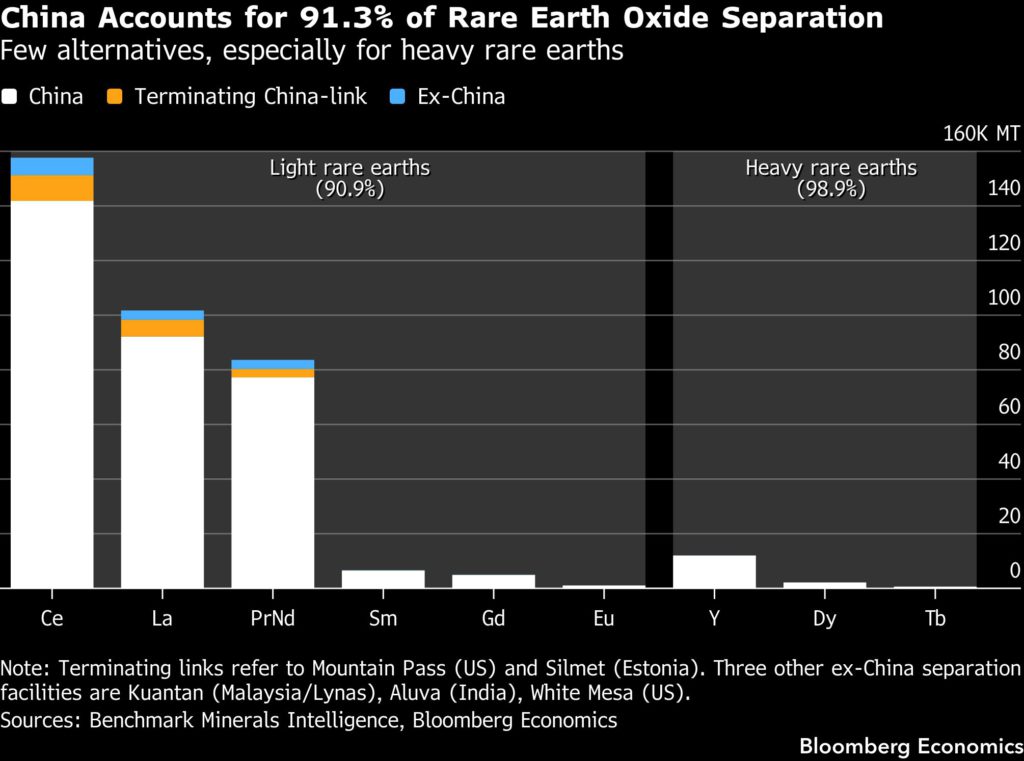

China imposed sweeping export controls on most critical minerals and rare earths last year. While the US has aggressively pursued partnerships with resource-rich nations and funded projects all over the world to catch up, Europe has lagged.

“Member states are still reluctant to pool resources for mining and processing projects beyond their borders, even as geoeconomic realities demand it,” said Sabrina Schulz, Germany director at the European Initiative for Energy Security. “Financing remains the central bottleneck.”

The bloc’s formal strategy was articulated in the European Critical Raw Materials Act of 2023, which set targets that included extracting at least 10% of annual consumption of key elements, and processing 40% of them. Those goals spurred action to identify vulnerabilities and to funnel investment to securing supplies of metals crucial for batteries such as lithium.

Global rivals have since pivoted toward resources with military uses such as antimony, gallium and germanium, but Europe has yet to follow suit. Brussels officials don’t have a mandate to pursue similar policies to the US, and lack money, people familiar with the internal deliberations said.

That leaves niche mining projects owned by thinly capitalized companies struggling to take off, not least because of the difficulty for them to raise finance in private markets.

With Europe, budgets are stretched, and many EU countries are unsure on how to engage. For example, in Germany there still isn’t consensus between the economy ministry, chancellery and foreign ministry of what exactly a de-risking strategy in critical minerals actually entails, the people said.

The result is an administrative impasse that leaves European officials worried about getting squeezed, with the feeling in Brussels and in capitals described as a fear of missing out.

Fretting about being left out of any deal Trump might cut with his Chinese counterpart Xi Jinping in their upcoming summit, the bloc last month reached an accord with the US to coordinate on policies to build secure critical minerals supply chains. For Military Metals, that’s a positive development that could result in joint US-EU investment and offtake partnerships for Trojarova.

Frank Hartmann, the official responsible for Asia at the German foreign ministry, told a March 24 event in Berlin that Europe is being too slow and operating on a “too limited scale.”

“What we have to do is long-term strategy, take money and funds into our hands to invest in these critical mineral funds for the next 10 years,” he said on a panel hosted by the German Council on Foreign Relations. “Otherwise, we never escape this dependency trap.”

The Trojarova project, acquired almost two years ago by Military Metals, epitomizes the challenge. The mineshaft there, protruding deep into the hillside, heads toward a murky gloom that seems endless, but a potentially bountiful opportunity might lurk within.

A shiny white metal that is often explored for alongside gold, antimony is largely found in China, Russia and Tajikistan. It’s essential for military applications such as munitions, night vision goggles and infrared sensors, which make up as much as 15% of demand. Other uses encompass fire retardants, and nuclear and renewable energy.

“Antimony is a textbook example of a small-volume mineral with outsized strategic impact,” said Schulz at the EIES. “Europe is almost entirely import-dependent, and supply is highly concentrated.”

She highlighted that China controls almost 80% of processing, pointing to another challenge. The Asian behemoth is pivotal not only as a source of such raw materials, but also as a refining hub. That’s one reason why Military Metals is pitching Trojarova’s riches to investors as a chance for Europe to catch up, with plans to produce ingots that can go direct to defense clients.

Alternatively, refining in Germany and Sweden could assist in smelting, meaning the facility could ultimately help establish an entire supply chain, from mining and processing, according to chief executive officer Scott Eldridge.

The mine, situated near the winemaking town of Pezinok in southwestern Slovakia, was first discovered and developed by the Soviets. When the Iron Curtain fell, the 1.7-km (1-mile) long excavation was abandoned, but it remained one of Europe’s most significant deposits of antimony.

Military Metals is too small a company to scale up the project on its own, and needs partners to invest and help develop an associated refining capacity. If reactivated, it could supply as much as a third of the continent’s annual demand, totaling about 6,000 tons, and be up and running in two or three years.

But the company — which has a market capitalization of less than $30 million — would need substantial funding.

Moreover, critical minerals are prone to wild price swings, and even in markets like lithium, several major projects have stalled as owners sought out government funding.

Whatever the merits of the company’s business case here, Europe’s money and resolve to secure such resources remain lacking. Germany’s own €1 billion ($1.2 billion) raw materials fund has only supported two projects so far and creates more hurdles for companies to qualify than it eliminates.

The EU Commission and member states have signed memorandums with producer countries — Spain agreed one with Brazil last month, for example — but US deals with the same countries are often bigger in funding terms and more ambitious on timelines for operationalizing the plans.

The Trump administration’s agreement with the EU reflects its push for so-called price floors, which guarantee minimum prices for producers that can’t be undercut by Beijing. European countries have been hesitant, but at some point might have little choice but to go along with the US-led initiative.

Meanwhile the region’s momentum to act has essentially taken a backseat to other more urgent crises. By contrast, despite the Trump administration’s recent focus on conflicts such as the Iran war, the president’s team of aides has been busy identifying mineral projects and bidding to secure them.

One American company has already approached Military Metals and asked to see the Trojarova project. Meanwhile just last month, the US government’s investment arm agreed on a $5 million deal to restart another dormant antimony mine in Northern Macedonia.

Thomas Hüser, the chairman of Military Metals, would like to prevent a similar outcome for Trojarova. The German native joined the company this year and was formerly a Glencore Plc manager.

“What we are still lacking is not ambition, but execution,” he said. “Europe’s raw materials strategy remains fragmented, slow, and often disconnected from industrial reality.”

(By Jenny Leonard and Jody Megson)

Japan’s Sojitz eyes Southeast Asia for new rare earths supply

Japanese trading house Sojitz Corp. is looking to Southeast Asia and other regions as new potential sources of rare earths outside Australia, as it aims to boost output and diversify its supply chain of the highly sought-after materials.

“Areas connected to southern China such as Laos, Cambodia and Vietnam will be potential regions that the company will look into,” chief financial officer Makoto Shibuya told Bloomberg News this week. The company will also consider India and other countries if suitable rare earths investment opportunities exist there, he added.

Rare earths are among the critical minerals used across high-tech manufacturing, including to build the powerful magnets used in electric vehicles, mobile phones and missile systems. China dominates the global supply chain for the materials, which has given it crucial leverage in trade and diplomatic negotiations, and countries including Japan are working to reduce their reliance on the Asian giant.

Sojitz, alongside Tokyo-backed energy agency Jogmec, has been in a joint venture with Australia-based Lynas Rare Earths Ltd. for more than a decade. They agreed in mid-March to start talks on mineral exploration and development of rare earth resources, including possible new mines “both in and outside Australia.” Sojitz has said its primary objective is to seek other sources besides Lynas’ major mining site at Mt. Weld in Western Australia.

As for its energy portfolio, Sojitz has no appetite either for a stake in the Alaska LNG project or to offtake volumes from the planned American venture as it’s simply too costly, Shibuya said. The proposed Alaska plant is backed by US President Donald Trump and often dismissed as fanciful by many in the industry.

Energy accounts for only around 10% of Sojitz’s total investments over the past decade and management has already been trimming that part of the business. Liquefied natural gas is one of its few remaining energy-related investments, but the company says it will only pursue projects that have been carefully scrutinized.

Japan’s government last year agreed with Washington to invest $550 billion in the United States, including possibly in the Alaska LNG project, in exchange for reducing tariffs on Japanese products to 15%.