It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

The global copper market enjoyed one of its best years in 2025. The threat of US tariffs on the industrial metal and its elevated status as a critical mineral, together with major supply disruptions globally, all played a part to help to lift prices 40% last year.

That run extended into 2026, as expectations of surging AI-driven demand and persistent supply constraints drove prices to a record of $14,500 a tonne in January. This week, copper is nearing another record.

The prospect of higher mining costs due to rising energy prices and a shortage of sulfuric acid, which is used in a fifth of the global copper production, is considered the next big catalyst for copper prices, a Sprott analyst recently said.

Goldman Sachs is also optimistic of copper surging higher again, due to the supply-side disruptions. The International Copper Study Group recently outright abandoned its previous surplus projections, now forecasting a 150,000-tonne deficit for 2026.

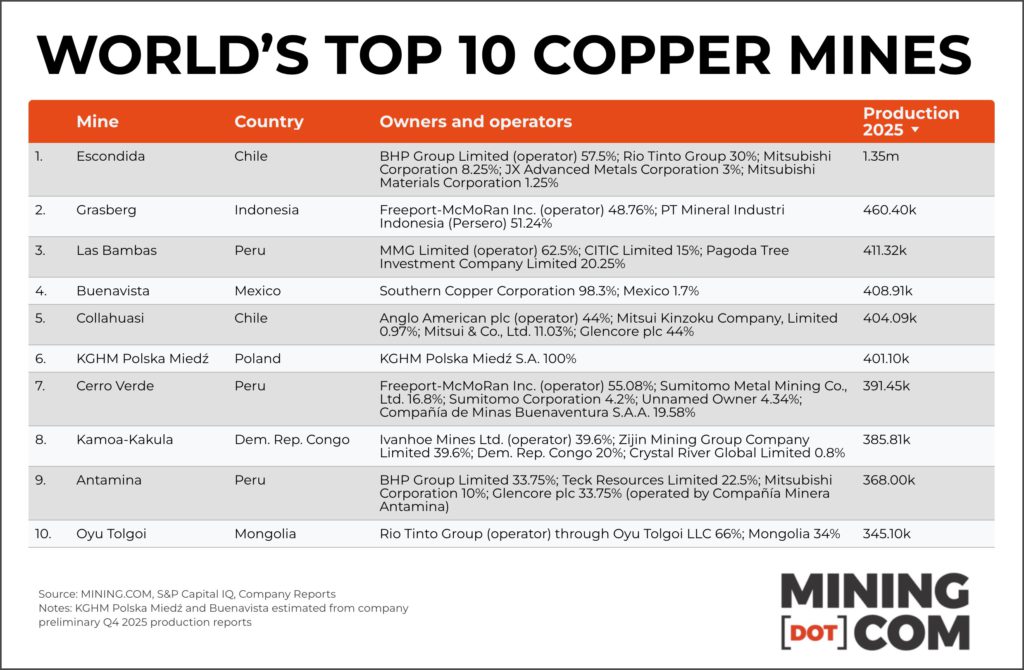

The top 10 mines, many of which have been in production for decades (some even trace roots back to the late 1800s) are responsible for more than a fifth of total global mined production – producing 4.9 million tonnes in 2025.

And surprisingly, after only recently being surpassed by BHP as the world’s number one copper producer on an attributable basis, Chile’s state owned Codelco does not have any of its operations qualify for the top 10.

As last year amply showed disruption at these giant operations (like the Grasberg and Kamoa-Kakula accidents that saw 100s of thousands of tonnes taken off the market,) can have a big impact on copper prices.

1. Escondida

Escondida in Chile, a joint venture between BHP, Rio Tinto, Mitsubishi, and JX Advanced Metals holds the top spot, producing 1,347.6 kts of copper metal in 2025. Escondida has long ranked the world’s biggest copper mine, but BHP’s operational review for the nine months to March 31 pointed to record material mined and concentrator throughput.

Las Bambas mine in Peru, owned jointly by China’s MMG, CITIC and Pagoda Tree Investment Company, churned out 411.3 kts in 2025. The mine was plagued by protests in 2024, but protesters agreed to lift a road blockade on a key Peruvian transport route, and operations resumed in April 2025.

4. Buenavista

Southern Copper’s Buenavista mine in Mexico moves up in this year’s ranking to fourth place with 409.4 kts produced. Copper has been mined at the historic site, 22 miles south of the US border, since 1899.

5. Collahuasi

Chile’s Collahuasi mine, a joint venture between Glencore, Anglo American and Mitsui produced produced 404.1 kts. In April this year, contractors finished building a system that will carry water from the coastal town of Punta Patache to the Ujina deposit, more than 4,400 meters above sea level, as part of a $1 billion infrastructure improvement project.

Cerro Verde in Peru, a joint venture between Freeport-McMohRan, Sumitomo and Buenaventura takes seventh place, producing 391.5 kts. The Peruvian government first mined Cerro Verde’s oxide ores and built one of the world’s first SX/EW facilities in 1972.

8. Kamoa-Kakula

The Kamoa-Kakula complex in the Democratic Republic of Congo, owned jointly by Ivanhoe Mines, Zijin Mining, Crystal River and the DRC government drops from third place last year to seventh — it produced 385.8 kts. Ivanhoe halted operations for three weeks in 2025 after seismic activity severely flooded the underground mine. In April, Ivanhoe slashed near-term production guidance, citing a shift toward underground development, rehabilitation and access work that will constrain ore delivery over the next 18 to 24 months.

9. Antamina

Antamina in Peru, co-owned by BHP, Glencore, Teck and Mitsubishi, moves up to ninth from 10th place, producing 368 kts. Last year, Antamina’s operators forecasted an almost 20% boost in cooper output.

10. Oyu Tolgoi

Oyu Tolgoi, a joint venture between Rio Tinto and the Mongolian government, churned out 345.1 kts. The government, which holds a 34% stake through state-owned Erdenes Mongol LLC., this year demanded earlier profit payments and a larger share of revenue, reopening negotiations over the $18-billion project’s commercial terms.

Honorable mentions: Morenci in Arizona, USA (313,100 tonnes), Quellaveco in Peru (309,900 tonnes), Los Pelambres in Chile (295,400 tonnes)

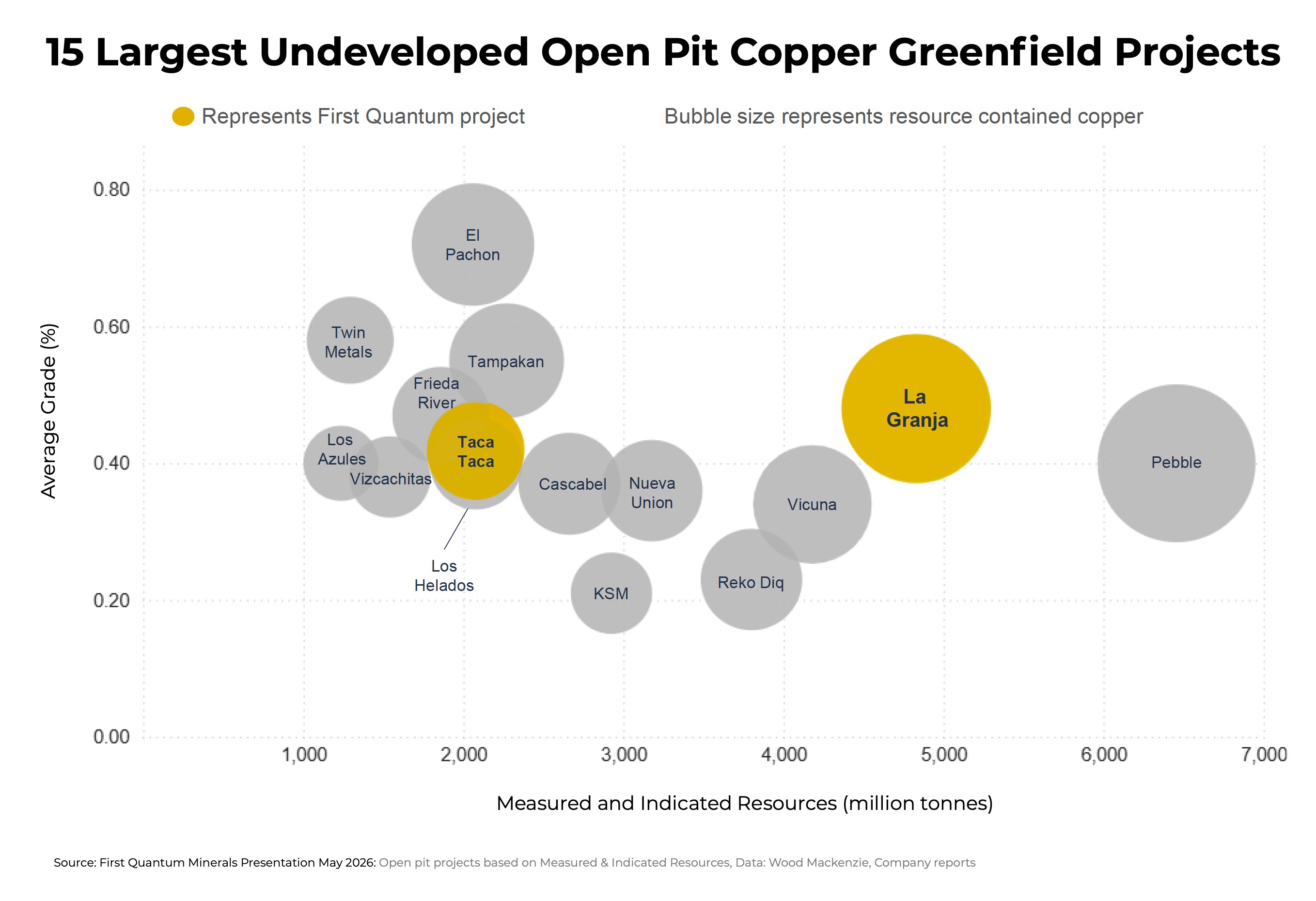

CHART: First Quantum’s Peru project joins ranks of copper giants

First Quantum has completed 370,000 metres of drilling at La Granja. Image: First Quantum Minerals.

First Quantum Minerals (TSX: FM) has filed a new NI 43-101 technical report for its La Granja project in the Cajamarca region of northern Peru it holds with Rio Tinto, outlining one of the copper sector’s largest undeveloped deposits.

First Quantum, said according to La Granja’s (meaning “the farm”) updated mineral resource, the orebody contains 4.8 billion tonnes of measured and indicated resources grading 0.48% copper, equal to 23.0 million tonnes of contained copper.

A further 5.2 billion tonnes grading 0.40% copper sits in the inferred category, containing another 20.7 million tonnes of copper, setting La Granja up as a tier-1, multigenerational asset, in the words of the company.

That places La Granja second among undeveloped copper projects in terms of measured and indicated resources behind only Northern Dynasty’s Pebble in Alaska and when including operating assets, also behind Kamoa-Kakula, the Ivanhoe Mines complex in the Democratic Republic of Congo.

First Quantum acquired the majority stake for only $105 million and has since spent $70 million out of a committed $546 million to advance the project.

Engineering challenges

In an interview conducted last year, First Quantum CEO Tristan Pascall said while the La Granja deal “wasn’t up there in the deals in terms of dollars, in terms of copper in the ground is one of the largest deals done in the last 10, 20 years.”

“Rio Tinto saw in First Quantum a partner that could want a challenging project, because it’s challenging from an engineering perspective, and particularly around deleterious elements like arsenic,” Pascall said. “We had a development hypothesis that we went to Rio with, and really that revolved around dealing with the orebody in a different manner.”

First Quantum says the drillhole database for La Granja now consists of a whopping 832 diamond holes totalling a whopping 370,000 metres, with more planned. The deposit remains open at depth with further exploration targets, according to the company.

Last month, ahead of the latest mineral resource estimate, Pascal told a group of reporters during a tour of its Zambian mines the company has spent the last three years of drilling validating this hypothesis:

“Our view was that it [the arsenic] wasn’t disseminated, that it was discreet and we could package it. That means you have assayable concentrate through a conventional flow sheet, and you don’t need any exotics in order to deal with arsenic.”

La Granja in Peru. Image: First Quantum Minerals

Water and tailings

La Granja’s pit optimization was based on a copper-only cut-off using a $4.00 a pound copper price (versus today’s price of $6.65 per pound, or $14,450 a tonne). Silver, gold and molybdenum should provide by-product upside, which may well lure streaming companies.

Other challenges at La Granja (and most sites in the South American copper belt) include water and tailings management. Unlike many copper projects in the Andean belt, La Granja sits at a moderate elevation between 2,000m and 2,800m above sea level.

First Quantum plans to carry out comminution near the pit, then move material by pipeline through a 7 km access tunnel to a flatter, arid Pacific coastal plain about 100 km from the mine where processing and tailings management would be located.

First Quantum said primary water supply would come from desalinated seawater, with site contact water captured and reused in processing to reduce impacts on local environmental flows.

Next up for La Granja is permitting, and progressing baseline environmental and social studies and continuing community engagement – a process that would take several years under Peru’s strict Environmental and Social Impact Assessment (ESIA) regulations.

A prior Peruvian government estimate put La Granja’s required investment at more than $2.4 billion. First Quantum is also advancing its Haquira project in the Apurímac region of southern Peru.

Annual output over the first 10 years at Taca Taca, which has qualified under Argentina’s fast-tracking program, is pegged at 291,000 tonnes of copper and 133,000 oz. of gold at cash costs of 97¢ per pound. Production over the mine’s life is projected at 209,000 tonnes of copper and 96,000 oz. gold at cash costs of $1.26 per pound.

Appian deepens Namibia push with $400M copper mine buy

Appian Capital Advisory has acquired Omico Copper in a deal giving the mining-focused private equity firm a 95% stake in Namibia’s Omitiomire copper project as it expands its exposure to a metal expected to face surging demand growth.

The mining-focused private equity firm plans to spend more than $400 million to develop Omitiomire into a mine producing about 30,000 tonnes of copper annually over a 15-year mine life, with first production targeted within three years.

The project, about 140 km northeast of Windhoek in Namibia’s Otjozondjupa Region, is considered one of the country’s most advanced undeveloped copper assets. Appian did not disclose the acquisition price for the asset, which was sold by Guernsey-based private equity fund Greenstone Resources LP and Australian mining company International Base Metals Ltd.

“Omico Copper is a technically robust development opportunity that aligns with Appian’s investment philosophy,” CEO Michael Scherb said in a statement. “The project complements our portfolio, offering near-term production alongside long-term growth potential.”

Scherb told Bloomberg News the firm could announce two more copper acquisitions before year-end involving projects at similar stages of development in South America, North Africa and southeastern Europe.

Mining investors are increasingly targeting copper assets amid expectations supply will struggle to meet rising demand from electric vehicles, renewable energy systems, power grids and AI infrastructure. S&P Global forecasts copper demand will climb 50% to more than 42 million tonnes by 2040 from 28 million tonnes last year.

The metal, crucial to electrification, is once again trading near a record high above $14,000 a tonne as a squeeze on Middle Eastern sulfur supplies threatens some operations, compounding disruptions at major mines elsewhere around the world.

Building a copper pipeline

Appian’s latest acquisition also builds on a broader strategy to expand its mining portfolio across Africa and Latin America. In October 2025, the firm established a $1 billion partnership with the International Finance Corp., the World Bank’s private-sector arm, to support mining investments in the regions.

The fund has already backed the development of an underground operation at the Santa Rita nickel mine in Brazil and the expansion of Asante Gold Corp.’s mines in Ghana, Scherb said. Namibia remains one of several “tier-one jurisdictions” where Appian is actively seeking investments alongside Morocco, Ivory Coast, Botswana and Zambia

The firm’s current portfolio includes operations producing about 480,000 ounces of gold annually, along with 55,000 tonnes of zinc and 19,000 tonnes of nickel.

Wreck of Fishing Vessel Nicola Faith Donated to Train Marine Investigators

Wreck of a fishing vessel recovered in 2021 will find a new life training future investigators (MAIB)

In a rare occurrence, a fishing vessel that was the subject of intense investigations after her capsizing and sinking in the UK waters will be used to train the next generation of accident investigators. This comes after the Marine Accident Investigation Branch (MAIB) donated the wreck of Nicola Faith to Cranfield University to be used in training investigators.

In January 2021, Nicola Faith attracted unprecedented attention in the UK after she disappeared off the coast of Wales during a fishing expedition. The 9.81-meter steel-hulled vessel that had been built in 1987 had three crew members when she disappeared, all of whom died. The bodies of the three crew members, identified as Ross Ballantine, Alan Minard, and Carl McGrath, washed ashore in different locations, the first of which was discovered 44 days after the accident.

The incident involving Nicola Faith ignited one of the most intense recovery efforts and an intensive investigation into her capsizing and subsequent sinking. Just days after the disappearance on January 27, a vessel owned by Trinity House conducted a side scan sonar search for the fishing vessel around her last transmitted position. The search was unsuccessful, while further searches could still not locate the wreck.

On February 8, MAIB commissioned a survey vessel to carry out an underwater search for the wreck, covering the vessel’s usual area of operation, but still there was no success in locating the wreck. MAIB went on to commission several survey vessels that used side scan sonar to cover a widened search area and re-survey the areas previously searched. The survey operations were severely hampered by storms.

It was not until April 3 that the wreck of Nicola Faith was located 319 meters east of its last transmitted position at a depth of 15 meters, with its identity confirmed 10 days later. In late May, the fishing vessel’s wreck was recovered from the seabed and moved to a local boatyard.

The MAIB investigation found that the vessel had been extensively modified during its life, something that had significantly reduced its margin of positive stability. Originally built as a steel-hulled potter, the vessel was modified to operate as a stern trawler but later converted back for use as a potter.

Investigators were able to conclude that the vessel was habitually operated in an unsafe manner and capsized because it was loaded with catch and pots to the point of instability. They believe that it capsized suddenly with little warning. The crew was trapped on board and taken down with the vessel when it sank.

Years later, MAIB has now decided to donate the wreck of Nicola Faith to Cranfield University for use when training students in accident investigation on its fundamentals of accident investigation course. Also donated is the factual evidence gathered as part of the investigation to enable the university to create a realistic scenario of a fishing vessel capsizing. The scenario will enable trainees to apply and test their knowledge by conducting a simulated accident investigation.

“Recovering Nicola Faith enabled MAIB to conduct a detailed inspection of the vessel and a full investigation into the circumstances that led to its loss. The report made recommendations to improve safety and prevent a similar accident from occurring,” said Rob Loder, Chief Inspector of Marine Accidents.

Following her donation, the vessel will be renamed Pisces II and will replace the vessel Pisces that has been used at Cranfield for many years.

U.S. Coast Guard Finalizes Five-Ship Icebreaker Order With Davie Defense

The U.S. Coast Guard has finalized its contract with UK-owned shipbuilder Davie Defense for the delivery of five Arctic Security Cutters, the new medium icebreakers that will complement the capabilities of the American-built Polar Security Cutter.

It is the first of three different Arctic Security Cutter contracts, and it builds on an initial contract with Davie announced earlier this year. The Arctic Security Cutter procurement is one program, but it is on track to order two vessel designs - much like the Coast Guard's twin-class Medium Range Cutter (WMEC) program or the Navy's twin-class Littoral Combat Ship (LCS).

"Finalizing this contract represents decisive action to guarantee American security in the Arctic," said Admiral Kevin Lunday, the commandant of the Coast Guard. "The Arctic Security Cutters will deliver the essential capability to uphold U.S. sovereignty against adversaries’ aggressive economic and military actions in the Arctic."

Davie's first hull is scheduled to deliver by 2028, within President Donald Trump's current term in office. The last of the series should deliver by early 2035. Two will be built at Helsinki Shipyard, and the other three will be constructed at the former Gulf Copper yards in Galveston and Port Arthur, where Davie says it plans to invest up to $1 billion in improvements.

The other two initial contracts went to Rauma Marine Constructions (for two hulls to be built in Finland) and Bollinger (for four hulls to be built to Rauma's design in Louisiana). Two more final contracts will be announced soon, the Coast Guard said in a statement, likely for these two yards. The overall procurement plan calls for a total of 11 vessels.

The Coast Guard is moving fast to commit to shipbuilding and infrastructure contracts. Its historic $25 billion budget boost from Trump's One Big Beautiful Bill Act will expire if unused by 2029. The service has already contracted for more than $13 billion in repair and recapitalization work.

USN’s Third and Fourth Ford Supercarriers Face Further Construction Delays

Mid-body for Enterprise was repositioned in late 2024 to permit Doris Miller to also start assembly (HII)

In a now all-too-common occurrence, the United States Navy is reportedly expecting further delays in the construction and delivery of the third and fourth carriers in the Ford class. USNI News broke the details, reporting that the Navy’s Fiscal Year 2027 budget presentation includes the schedule delays.

The third carrier of the class, named Enterprise, is now reportedly facing an additional eight-month delay, reports USNI News. Enterprise had been scheduled for delivery in March 2028 but had already seen its target date slipping. It had been moved to July 2030, and now the budget reflects the target date as March 2031.

Despite the delay, USNI writes that Enterprise would be completed in just 12 years. It points out that the second ship of the class, the carrier John F. Kennedy, will have taken about 16 years to build. Now, however, the fourth ship, the carrier Doris Miller, is likely to take 15 years, reports USNI.

Delivery of Doris Miller had been scheduled for February 2032. The new budget moves the date to February 2034, a full two-year delay.

Currently, the U.S. only has one shipyard, HII’s Newport News Shipbuilding, that builds the nuclear carriers. In late 2024, the yard had highlighted that it was gearing up to have two of the carriers in assembly at the same time. The yard completed renovations to its dry dock and then repositioned the early-stage assembly for the hull of Enterprise. They highlighted for the first time that two supercarriers would be assembled in the same dry dock at the same time.

Now, according to USNI, the yard is still preparing for the keel laying of Doris Miller. The Navy reportedly cites as an explanation “construction footprint constraints,” which USNI says are limiting the ability to build modules for CVN-81, the future Doris Miller.

In a statement to the outlet, Newport News Shipbuilding reportedly highlighted that the components for the fourth carrier continue steel fabrication and outfitting. However, they told USNI that a cascading series of delays and supply chain issues are impacting the carriers. Delays with Enterprise due to the supply chain reportedly have spilled over to Doris Miller.

All the carriers in the Ford class have faced construction delays of varying lengths. Last year, the delivery of John F. Kennedy was pushed back from August 2025 to March 2027 so that additional modifications could be completed. The carrier has now completed its first sea trials and continues to move forward on schedule.

However, the delay for CNV-79 has placed pressure on the U.S. Navy, which is mandated by the U.S. Congress to maintain an 11-ship carrier fleet. The Navy had highlighted with fanfare that USS Nimitz was completing her final deployment and heading into retirement. Nimitz, however, was given a last-minute reprieve and will continue in active status until Kennedy is ready. Nimitz is currently circumnavigating South America before taking up her final homeport in Norfolk, Virginia.

At the same time, USS Gerald R. Ford is reportedly on her way home after what will be an 11-month deployment. The carrier is anticipated to go into an extended maintenance period that could last for a year or more after the record-setting deployment.

The Society of Naval Architects and Marine Engineers (SNAME) was founded in 1893 by 13 leaders from across the U.S. maritime sector. They were responding to the weakened state of American commercial and naval shipbuilding after the Civil War and created a forum to advance “practical and scientific knowledge” in shipbuilding, marine engineering, and allied professions.

Headquartered in Alexandria, Virginia, SNAME is an independent, nonprofit professional society for naval architects, marine and ocean engineers, and related specialists. Its community includes more than 4,000 members in 69 countries organized into 20 professional sections in five regions: International, Atlantic North, Atlantic South, Central & Gulf, and Pacific. Its membership is broad enough to be globally relevant, but it is its local focus that provides the unparallelled networking and learning opportunities.

SNAME is largely member-funded, with limited sponsorship from companies and government agencies. This independence helps create a noncompetitive space where industry, government, and academia can compare notes, test ideas, and document what works through committees, panels, and publications. The benefits ripple outward to shipyards, engineering firms, equipment makers, owners and operators, ports, and public agencies that rely on better designs and better technical decisions.

In 2026, SNAME’s agenda reads like a roadmap of the modern maritime industrial base: machine learning, robotics, additive manufacturing, digital twins, alternative fuels and power, ice strengthening, port interfaces, dual-use technologies, and secure supply chains. As policymakers press for a U.S. maritime resurgence through public and private investment, naval architects and marine engineers will be central—integrating emerging technologies into producible ships and systems that stay safe, reliable, and sustainable over decades at sea.

SNAME Alignment with U.S. Maritime Industrial Base Aspirations

A closer look at today’s maritime industrial base proposals makes one point clear: many of the hardest problems are engineering problems—and they map directly to the expertise inside SNAME’s membership and technical committees.

Proposals to establish a national maritime policy advisor and a maritime security board will only succeed if they are informed by technical reality. Designers and engineers, including many SNAME members, should help assess feasibility, set practical innovation priorities, and shape standards. A high-level policy mechanism should be able to draw on SNAME committees as a dependable source of real-world expertise.

Long-term, predictable funding for shipbuilding and maritime R&D is essential because ship design and engineering are multi-year endeavors. Stable demand strengthens the professional base—naval architecture, marine engineering, and detailed design—and SNAME supports those professionals through training, technical exchange, and forums that keep practice aligned with the state of the art.

R&D leadership has long been foundational to SNAME. Many members have built reputations as world-renowned subject-matter leaders through committee work, research, and publishing. Any transformation of the U.S. maritime industrial base will need that kind of organized, readily available technical leadership.

SNAME members also bridge the gap between commercial and military shipbuilding—an advantage as policymakers emphasize ships that are commercially efficient yet militarily useful. Designing for dual requirements adds complexity in hull form, propulsion, survivability, and lifecycle support; specialized naval architecture many SNAME members practice.

Talent development proposals—professional hubs, workforce pipelines, and knowledge transfer—align with long-running SNAME activities. University programs at maritime schools train future naval architects and marine engineers, and SNAME’s 49 student sections and engagement in continuing education and professional licensure place the Society at the center of recruiting and development.

As the U.S. maritime sector looks outward for proven practices, SNAME can make global knowledge transfer practical by facilitating professional exchanges that connect members and students with leading design and production approaches worldwide.

SNAME Technical and Research Program

SNAME recently restructured its Technical and Research (T&R) program to reflect new priorities, including themes highlighted in the Maritime Action Plan (MAP). One central question was: what types of vessels does it make sense to build in the United States? Two areas drew particular attention—maritime nuclear power and autonomous marine vehicles.

The T&R program now includes a Maritime Nuclear Power Committee (panels on nuclear-powered ships and floating nuclear power plants) and a new panel on Autonomous Marine Vehicles.

Ship Design

Less flashy—but just as consequential—is work on schedule and cost realism as projects move from concept to Front End Engineering Design, Final Investment Decision, and detailed design. Programs stumble when requirements and engineering maturity aren’t de-risked early; late changes then cascade into disputes, overruns, and delays. SNAME’s cross-sector experience, including lessons from offshore and energy projects, helps teams set achievable assumptions and share practices that improve execution.

Ship Production

SNAME’s Ship Production Committee, working with the National Shipbuilding Research Program (NSRP), is leaning into modular construction, digitalization, and AI—while keeping focus on the fundamentals that determine whether yards can scale: workforce development and productivity. Modularization and distributed fabrication can also broaden the supplier base, supporting the MPZ concept by spreading skilled work across a region.

Together, these efforts position SNAME as a practical partner for rebuilding capacity: convening experts, translating lessons across sectors, and turning ambitious policy goals into designs, standards, and production methods that can be executed and sustained over a ship’s full life.

Maritime Prosperity Zones

The Maritime Action Plan proposes Maritime Prosperity Zones (MPZs) to link supply chains, workforce development, and financing to support new shipbuilding activity. Offshore floating wind is one example of a steel-intensive market where SNAME’s Offshore T&R Committee is positioned to contribute as projects scale.

Sharing Knowledge

A maritime resurgence will be built on shared knowledge as much as steel. That’s where SNAME’s publishing and convening roles matter: trusted technical content, peer review, and forums that let practitioners challenge assumptions and carry proven ideas back to yards, design teams, and fleets.

SNAME shares knowledge through several flagship channels, including:

- T&R Bulletins (guidelines, standards, white papers) produced by technical committees and panels

- Marine Technology magazine and peer-reviewed journals

- Books and reference texts (including Principles of Naval Architecture)

- Regional conferences, symposia, and the annual SNAME Maritime Convention (this year October 28-30th in Houston).

About the Authors

James Watson is a retired U.S. Coast Guard Rear Admiral and an independent maritime consultant. He is a co-author of Zero Point Four and a founding member of Maritime Accelerator for Resilience (MAR). He previously served as SVP at ABS Global Government Services and held senior safety and prevention-policy roles at the U.S. Department of the Interior and the U.S. Coast Guard. He is a proud SNAME member.

Elizabeth Bouchard is the Executive Director of SNAME. Prior this, Elizabeth served as SVP, Regulatory Administration for International Registries, Inc. and as Deputy Commissioner of Maritime Affairs for the Republic of the Marshall Islands Maritime Administrator. Her background is in maritime regulation and policy. She has served as a consultant for energy and shipping companies and as an advocate for the maritime industry in government.

On Wednesday, British defense shipbuilder Babcock told its investors that it would be taking a steep charge due to rework on the first two hulls in the Type 31 frigate class. The Type 31 is a much-needed replacement for the Royal Navy's aging Type 23, and Babcock said that the extra effort is interfering with productivity.

In a regulatory filing, Babcock said that it is experiencing higher than planned amounts of rework, and at a later stage of construction completion - when such work is more costly and complex to carry out. The excess rework is design-related, the company said, and affects only the first two hulls in the series. Vessels three and four are still in the early stages of construction, and are not affected by late-breaking design modifications.

Babcock said that the rework is impeding its efforts to raise yard productivity on the program - and since the contract contains fixed-price elements, the added costs from the extra work will affect its bottom line. The firm says that it will cost about $190 million over time, including extra labor, materials, and provisions for additional program risk. An engineering maturity review is under way.

The affected ships, HMS Venturer and HMS Active, have already been launched and are undergoing outfitting. The UK's national shipbuilding strategy of 2017 envisioned a 2023 in-service date for the first hull; this was later pushed to 2027. Timely delivery is essential, as the service's previous Type 23 frigates are in deteriorating condition and are rapidly aging out of service - just when their capability is needed most to deter an increasingly active Russian Navy.

The design change Babcock cited on Wednesday may relate to the confirmed selection of the Mk41 VLS cell system, the ubiquitous American design for launch of air defense interceptors and cruise missiles, according to British defense media. Several VLS options were proposed earlier in development, but in 2023, then-First Sea Lord Ben Key confirmed that a 32-cell Mk41 package would be aboard the Type 31.

The Mk41 units may be a "fitted-for-but-not-with" capability at the time of delivery of the first hulls, earlier reporting indicates. The ships are built to carry the cell modules, but the modules themselves might be installed during future maintenance availabilities, the service told Naval Technology in 2024 - thereby prioritizing the vessel delivery timeline.

IMO Maritime Safety Committee Convenes in London to Discuss Safety and Security

International Maritime Organization Secretary-General, Arsenio Dominguez

IMO Secretary-General Arsenio Dominguez opened the 111th session of the Maritime Safety Committee of the International Maritime Organization today, which brings together IMO's 176 Member States to discuss issues related to the safety and security of international shipping.

Key items on the agenda (18 to 22 May) include the adoption of the first non-mandatory Code to regulate autonomous ships, enhancing maritime security, updates on piracy and armed robbery against ships, and efforts to develop a a safety regulatory framework for alternative fuels.

The Committee will also discuss the impacts on shipping and seafarers of the situation in the Arabian Sea, the Sea of Oman and the Gulf region, particularly in and around the Strait of Hormuz.

Opening the session, Secretary-General Dominguez highlighted the ongoing challenges in the Strait of Hormuz, including 38 verified attacks on international shipping, 11 seafarer fatalities with around 20,000 still effectively stranded. IMO has developed an evacuation plan for vessels and seafarers, to be implemented once it is safe to do so.

"These seafarers are facing sustained security threats and severe psychological pressure. This is an unacceptable situation for a civilian workforce.... The longer this situation persists, the greater the risk of a serious maritime incident," he said.

The meeting runs from 18 May to 22 May.

Browse photo galleries of the MSC 111 opening + press event

Download a recording of the press Q&A with IMO Secretary-General

Download b-roll

Read Secretary-General's full opening statement

IMO incidents page Strait of Hormuz

The products and services herein described in this press release are not endorsed by The Maritime Executive.

In a blow for green shipping, the e-fuel maker Liquid Wind AB has entered bankruptcy administration and will be sold off, raising questions about the future of its methanol plant project pipeline. The industry already faces a supply shortage, and it is as-yet unclear where adequate quantities of e-fuels will come from in order to power shipping's green transition.

Liquid Wind is a specialist in e-methanol, an energy storage process that takes renewable energy and uses it to create a physical commodity - a liquid fuel, suitable for running an internal combustion engine. It is particularly suitable for hard-to-abate industries like shipping, where high energy density and long endurance between refueling stops are fundamental requirements.

The process requires a source of CO2; if the CO2 is derived from biomass combustion, the resulting product is fossil-free and net carbon-neutral. Liquid Wind has six different combined heat and power projects in its sights, each offering a plentiful stream of biogenic CO2 which could be captured and turned into methanol (using plenty of electricity, clean water and a bit of chemistry). It had hoped to have 10 projects under way by 2030, each producing about 100,000 tonnes of green methanol annually; given the low gravimetric energy density of methanol, the output of each plant would be enough to run one ULCV container ship for roughly 125-250 days of steaming, depending upon speed.

On Monday, Liquid Wind was declared bankrupt, and its management was handed to a court-appointed trustee. The entirety of the business is up for sale, including its Finnish and Swedish subsidiaries. The firm did not provide further details.

The bankruptcy comes despite many notable successes - partnerships with major industrial brands like Alfa Laval and Siemens Energy, a successful $44 million equity raise, project sponsorship from the Swedish Energy Agency, and financing from big names like Samsung Ventures and Uniper.

Just days before the announcement, Liquid Wind had submitted its environmental permit application for a project at a combined heat and power plant at Ornskoldsvik. The new e-methanol facility was designed to take biogenic CO2 from a biomass-fueled powerplant on the waterfront, output e-methanol, and provide district heating to nearby buildings using the waste heat from the process. The fuel for the powerplant comes mostly from forest industry waste products, and the electricity would come from nearby renewable-energy projects.

"With strong local collaboration and integration with Ovik Energi’s CHP plant, we can deliver locally produced volumes of sustainable eMethanol—especially in sectors where alternatives are still limited and reliance on imported fossil fuels remains high," said founder and then-chief executive Claes Fredriksson on May 5.

First Quantum has completed 370,000 metres of drilling at La Granja. Image: First Quantum Minerals.

First Quantum has completed 370,000 metres of drilling at La Granja. Image: First Quantum Minerals.

SNAME members also bridge the gap between commercial and military shipbuilding—an advantage as policymakers emphasize ships that are commercially efficient yet militarily useful. Designing for dual requirements adds complexity in hull form, propulsion, survivability, and lifecycle support; specialized naval architecture many SNAME members practice.

SNAME members also bridge the gap between commercial and military shipbuilding—an advantage as policymakers emphasize ships that are commercially efficient yet militarily useful. Designing for dual requirements adds complexity in hull form, propulsion, survivability, and lifecycle support; specialized naval architecture many SNAME members practice. Ship Production

Ship Production James Watson is a retired U.S. Coast Guard Rear Admiral and an independent maritime consultant. He is a co-author of Zero Point Four and a founding member of Maritime Accelerator for Resilience (MAR). He previously served as SVP at ABS Global Government Services and held senior safety and prevention-policy roles at the U.S. Department of the Interior and the U.S. Coast Guard. He is a proud SNAME member.

James Watson is a retired U.S. Coast Guard Rear Admiral and an independent maritime consultant. He is a co-author of Zero Point Four and a founding member of Maritime Accelerator for Resilience (MAR). He previously served as SVP at ABS Global Government Services and held senior safety and prevention-policy roles at the U.S. Department of the Interior and the U.S. Coast Guard. He is a proud SNAME member. Elizabeth Bouchard is the Executive Director of SNAME. Prior this, Elizabeth served as SVP, Regulatory Administration for International Registries, Inc. and as Deputy Commissioner of Maritime Affairs for the Republic of the Marshall Islands Maritime Administrator. Her background is in maritime regulation and policy. She has served as a consultant for energy and shipping companies and as an advocate for the maritime industry in government.

Elizabeth Bouchard is the Executive Director of SNAME. Prior this, Elizabeth served as SVP, Regulatory Administration for International Registries, Inc. and as Deputy Commissioner of Maritime Affairs for the Republic of the Marshall Islands Maritime Administrator. Her background is in maritime regulation and policy. She has served as a consultant for energy and shipping companies and as an advocate for the maritime industry in government.