It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Sunday, May 24, 2026

How Trump’s Cuba grudge threw a 99-year-old Canadian mining company into turmoil

The Trump administration’s hard line against Cuba pushed Sherritt International Corp. to the brink. Now, an ex-adviser to the US president may be the Canadian mining company’s salvation.

The nearly 99-year-old company, whose former chief executive was once known as Fidel Castro’s favorite capitalist, has staked its business on a bet few Western companies would touch. After entering Cuba in the 1990s, Sherritt developed a nickel-and-cobalt mine through a joint venture with the state before expanding into energy. The result was a sprawling business that’s survived commodity busts, US political pressure and economic instability on the island.

That wager abruptly unraveled this month, plunging Sherritt into turmoil. After President Donald Trump expanded sanctions on the communist country, Sherritt initially announced plans to dissolve its mining venture in Cuba. On Wednesday the US charged former Cuban President Raúl Castro with murder, sharply escalating a standoff with Havana as the Trump administration attempts to reshape the island’s political order.

But just days after Sherritt announced its retreat from Cuba, a potential rescuer emerged in the form of a Dallas family office linked to Ray Washburne, a real estate executive appointed by Trump in 2017 to lead the Overseas Private Investment Corp. Washburne’s Gillon Capital LLC signed a non-binding preliminary agreement on Wednesday that would hand the family office a controlling stake in Sherritt.

“It came out of nowhere,” Peter Hancock, Sherritt’s interim chief executive officer, said in an interview. “I would like to tell you that I’m a business genius and that I knew an American entity would see that it could create value in the situation that Sherritt was in. But no, I didn’t foresee that.”

As Trump’s foreign policy during his second term turns markedly more aggressive, Sherritt is still at risk of losing its Havana gamble. The saga underscores the dangers facing companies and investors from shifting geopolitics amid a rapidly changing world order. While major multinational firms have not been immune to conflict-driven losses, the threat is particularly acute for companies with assets concentrated in a single country outside of the US.

It’s not clear whether Sherritt’s preliminary pact with Gillon signals a potential shift in Trump’s Cuba strategy. On Wednesday, he played down the need to further ratchet up pressure on the Cuban government after the charges against Raúl Castro. Representatives for Gillon and the State Department didn’t immediately respond to requests for comment.

But for Hancock, the sudden backing from Gillon helped “bridge the huge gap” between Sherritt and the administration.

“This deal happened because an actor in the United States was able to make a case to the US State Department,” he said. “We were collateral damage in a larger policy objective for the United States.”

Sherritt was founded in 1927 and named after Carl Sherritt, a trapper who staked copper prospects in Manitoba. The company’s first foray into Cuba was steered by Ian Delaney, who became CEO after a proxy fight in 1990 and secured a deal with the Castro government one year later. The state agreed to sell Sherritt unprocessed nickel from Moa, a mine in eastern Cuba that was nationalized after the country’s 1959 revolution.

It was a milestone deal for the Canadian firm, which needed raw material to feed its key asset: a refinery in Alberta. The company entered into a joint venture agreement in 1994 with the state to operate Moa, which produces cobalt and nickel, both key metals for the energy transition and providing power to data centers.

For years, Sherritt was enormously successful in Cuba. Its market capitalization jumped to almost C$5 billion ($3.6 billion) in 2008, while the stock traded as high as C$18. Sherritt, by that time, had poured significant investment into the country, including stakes in electricity, oil and natural gas ventures alongside state companies.

Sherritt executives became the first people barred from entering the US under the Helms-Burton Act, a law passed in 1996 to target firms doing business in Cuba. But Canada and several European nations opposed the law and maintained diplomatic ties with Havana, allowing Sherritt to keep selling most of its nickel and cobalt into those markets as well as Asia.

Yet at the height of Sherritt’s rise following its success in Cuba, the company made costly bet on a nickel project in Madagascar. The decision would ultimately shred its balance sheet, driving debt to almost C$2.5 billion at its peak in 2013. Then came a prolonged slump in nickel prices, leaving the company periodically teetering on the brink of insolvency.

Saddled with a heavy debt load and years of weak cash flow, the company became even more reliant on Cuba, exiting other assets including its Canadian coal business to fund loan repayments and eventually writing off its Madagascar venture. Today, Cuba accounts more than 70% of the company’s asset base on a book value basis.

“They had an ample opportunity to eliminate their indebtedness entirely,” Jeffrey Gavarkovs, a managing partner at Northstream Capital Inc., said in an interview. But “the combination of Cuba and a debt load that was a little bit too heavy was their poison pill.”

While Sherritt continued receiving distributions from its power and nickel operations, the company spent more than C$100 million on an offshore well, a higher-risk category of oil exploration, Gavarkovs said. The effort yielded a well that was ultimately written off as uneconomic.

But according to Gavarkovs, who owns Sherritt bonds, the company’s biggest flaw was its bloated corporate overhead for what had effectively become a single-asset mining company. Directors on the board, rather than ensuring that unsecured note-holders received cash interest payments as required by the debt covenants, prioritized vesting cash-settled stock options, he said.

The company also spent millions trying to fend off several activist campaigns against it, he added. Last year investment firm Pala Assets Holdings won its battle against Sherritt, resulting in the resignation of CEO Leon Binedell and a shakeup of the board.

When US forces captured Venezuelan leader Nicolás Maduro in January, investors began speculating that Cuba could be the Trump administration’s next target. In Venezuela’s case, US oil majors and Western mining companies swarmed into the country after Maduro’s arrest, with Chevron Corp. emerging as one of the clearest winners.

But unlike Chevron, which has a diversified asset base, Sherritt was facing a worsening a fuel shortage as the US blocked Venezuelan exports to Cuba. The company announced plans to pause mining at Moa in February after receiving notice that planned fuel deliveries could not be fulfilled.

As Cuba’s economy continued to crumble, with mass blackouts sweeping the island as Trump tightened his squeeze on the nation of 10 million people, Sherritt faced a choice: keep operations going at a loss and at reduced capacity, or mothball the company’s most valuable asset. In late March, the company announced it was seeking an emergency cash injection of as much as C$50 million to support Moa.

Hancock was at home in Halifax on Monday, a public holiday in Canada, watching the Giro d’Italia cycling race on TV when the phone rang. On the other end was Washburne, calling with his offer for Sherritt.

Two days later, the Canadian company announced that it had signed a non-binding term sheet with Gillon. Sherritt said the US State Department had no objections to the discussions.

It’s far from certain that Ottawa will support a US investor taking majority ownership of Sherritt, however. Canada instituted a new policy in 2024 to make it more difficult for foreign companies to take control of Canadian critical minerals assets.

To Ben Rowswell, a former Canadian ambassador to Venezuela, the move by a Trump-friendly investor to take control of Sherritt in Cuba exemplifies what’s become known as the Donroe Doctrine, the US president’s take on Washington’s 19th-century push for hemispheric domination.

The latest move provides “further insight into the changing character of the US relationship with the region as it’s turning into an extractive predator” that uses its power over all countries, said Rowswell, now a consultant with strategic advisory firm Catalyze4.

The government of Prime Minister Mark Carney might be reluctant to attempt to block the takeover of Sherritt by a US investor to avoid complicating efforts to renew a free trade agreement with the US, Rowswell said, adding that he believes Carney’s administration should defend the company against US sanctions.

A spokesperson for Canada’s industry department said the government welcomes foreign investment that benefits Canada’s economy, but declined to comment on specific transactions.

Sherritt isn’t the only foreign company with mining operations in Cuba: Singapore-based commodities trading giant Trafigura has a lead-and-zinc mine there in a joint venture with the state. The company has said that it complies with all applicable sanctions and maintains a regular dialogue with relevant authorities.

Despite the potential deal with Gillon, Sherritt’s situation remains tenuous. Three board members have resigned from Sherritt, leaving just Hancock and one other director. Its chief financial officer and its auditor also departed earlier this month. The company now trades as a penny stock, with a market capitalization near C$80 million. Without essential nickel and cobalt supplies from Cuba, the available inventory at the company’s Alberta refinery will run out in mid-June, it said earlier this month.

“A lot of things will need to happen to get to the state where the full value is realized,” said Hancock, adding that sourcing key inputs such as fuel and sulfur would also be critical to unlocking Sherritt’s full potential. But, he added, “the posture of the US government with respect to this deal opens up a much wider world of financing.”

The Fort Saskatchewan refinery is one of just a few nickel processing facilities in North America. As governments and manufacturers race to build critical minerals supply chains outside of China, the facility carries growing strategic importance, according to Northstream’s Gavarkovs.

For Hancock, a former engineer with commodities trader Glencore Plc, there have been “a lot of very unexpected twists and turns” since he stepped in as interim CEO of Sherritt in December. If the Gillon proposal goes ahead, any easing of tensions between the Trump administration and Cuba would likely improve the payoff for the Washburne family office, he added.

Gillon is “very, very familiar with the business and the value that they see down the track,” he said. “This deal signals that they believe Sherritt has got a real bright future when things normalize in Cuba.”

(By Sybilla Gross, Paula Sambo and Stephen Wicary)

Sherritt in talks to hand control of Cuba mining business to ex-Trump adviser

US new sanctions revive a decades-old clash with Sherritt, rooted in the 1990s. (Image courtesy of Sherritt International.)

Sherritt International Corp. is in talks to hand a controlling stake to a family office linked to a former adviser of President Donald Trump, as the mining company seeks to navigate US sanctions tied to its Cuba operations.

The Toronto-based company said it signed a non-binding term sheet for a private placement involving a warrant, which would allow Gillon Capital LLC to acquire enough common shares to own 55% of the company on a fully exercised basis, according to a statement Wednesday.

Sherritt expects that the exercise price will be at a discount to the company’s closing price May 15. The company, which operates nickel and cobalt mining and refining businesses tied closely to Cuban state partners, on Tuesday reversed course on plans to unwind its operations in the Caribbean country.

Shares of Sherritt, which trades as a penny stock, rose 9% in early trading in New York.

Gillon Capital is the family office of Ray Washburne, a real estate executive whom Trump appointed in 2017 to head the Overseas Private Investment Corporation before later naming him to the Presidential Intelligence Advisory Board.

Sherritt said it has “engaged constructively” with the US Department of State, which confirmed no objections to Gillon Capital’s engagement with the company, according to Wednesday’s statement. The Department of State and Department of Treasury don’t view the negotiations as contrary to US law, the statement said.

Last week, Sherritt said it was considering steps to relinquish its 50% stake in a Cuban nickel-and-cobalt mine, as well as surrender its interest in an energy joint venture with the state. On Tuesday, it backtracked on that decision and flagged it was evaluating a “potential value preserving opportunity.”

Sherritt operates nickel and cobalt mining and refining businesses tied closely to Cuban state partners and has long depended on the country for a significant portion of its production.

The company has been in turmoil since Trump signed an executive order earlier this month targeting non-US individuals and entities doing business in Cuba, which has faced sweeping US sanctions since the 1960s. The upheaval triggered a wave of departures, including three board members and the chief financial officer, and triggered a plunge in its share price.

Sherritt International (TSX: S) has dropped plans to dissolve its mining assets in Cuba, though operations will remain suspended amid ongoing US sanctions.

In a statement on Tuesday, the Canadian miner said it will now keep its Cuban interests, namely the Moa nickel mining venture, and will not proceed with its application to the Court of King’s Bench of Alberta to disclaim the asset.

The decision was made following further “consultation with advisors, stakeholders and relevant governmental authorities,” and “in light of additional information” currently available to the company, it said.

The announcement comes just days after Sherritt said it would be dissolving the 50/50 Moa joint venture with the state-owned General Nickel Company, citing a “material change” from the JV shareholders’ agreement. It followed a recent executive order by US President Donald Trump that expanded sanctions on Cuba to include non-American entities, including Sherritt.

The extended US sanctions triggered a wave of departures within the company, including three board members, the chief financial officer, and led to a more than 50% drop in its share price.

Before that, the Toronto-based miner had already been struggling due to its heavy exposure to the Cuban market. Sherritt has been mining cobalt and nickel in the island nation since 1990. It also produces electricity, oil and gas through a stake in Energas SA, another joint venture with Cuba’s state electric and petroleum companies.

Sherritt International shares rebounded slightly off an all-time low of C$0.11 on the news. Its market capitalization is approximately C$81 million ($59 million), following a decline that extends to nearly two decades.

While the company is not longer seeking a dissolution of the Cuban assets, its participation in the Moa venture will remain suspended, Sherritt said on Tuesday, adding that it will “continue to work with stakeholders and advisors on steps to address the executive order as soon as practicable.”

The company also said it has been presented, on a preliminary basis, with “a potential value preserving opportunity”, which it will evaluate.

US Supreme Court Rules Cruise Lines Can Be Sued Under Cuban Libertad Act

There are other cases under the Libertade Act also pending in the U.S. courts based on Trump’s 2019 decision not to extend the suspension of the act. Presidents before Trump had suspended the enforcement of the act.Cruises docked at the piers in Havana between 2016 and 2019 working under U.S. licenses (GPH photo)

The United States Supreme Court handed down its ruling saying four cruise lines could be sued for their use of the pier in Havana, Cuba, under the Libertad Act passed by the U.S. Congress in 1996. The case has been seen as a potential watershed in the long-running fight for compensation for assets seized during the 1959 Cuban revolution and other events around the globe.

At issue was the cruise lines' use of the docks in Havana between 2016, when the United States lifted many of its restrictions on Cuba under President Barack Obama, and June 2019, when Donald Trump reinstated the restrictions and let a presidential waiver over enforcement of the Libertad Act lapse. The Havana Dock Company, which built and operated the docks under a 99-year concession before the Cuban revolution, sued Carnival Corporation, Norwegian Cruise Line Holdings, MSC Cruises, and Royal Caribbean Group, contending they profited from the use of confiscated property.

The case alleges the cruise lines carried nearly one million passengers to Cuba between 2016 and 2019 using the piers that were tainted property, seized by the Cuban government in 1960 from Havana Docks. Under the Cuban Liberty and Democratic Solidarity Act (known as the Libertad Act or the Helms-Burton Act for its sponsors), companies were given the right to sue for compensation from their seized properties.

A federal district court in Miami found for Havana Docks and awarded damages of $440 million. However, a U.S. Court of Appeals reversed the decision. The cruise line case was argued before the U.S. Supreme Court in February over the interpretation of the act. Among the defenses presented by the cruise lines is the argument that the concession for the piers was to have expired in 2004. Further, it is argued that the cruise lines were operating under permits issued by the U.S. government.

The Supreme Court, in an 8 to 1 decision, ruled that the property was, in fact, “tainted” by the 1960 seizure and that Havana Docks only had to show that the cruise lines had used the confiscated property. The majority opinion written by Justice Clarence Thomas disagrees with the appellate court’s ruling, finding that the act generally makes those who use property tainted by a past confiscation liable to any U.S. national who owns a claim on that property. Havana Docks' claim for the lost docks was certified at $9 million in 1960.

In a concurring opinion, Justice Sonia Sotomayor, joined by Justice Brett Kavanaugh, raises concerns that the majority opinion, however, is too broad. She believes it was unlikely that Congress intended in the act that “someone who suffered a finite loss to reap infinite recoveries.” She believes the claim should be finite and not go on so long as anyone continues to make any commercial use of the docks. Justice Sotomayor, in her opinion, raises another point, highlighting that the cruises were operated at a time when U.S. policy was that they were lawful and beneficial to both Cuba and the United States.

The solo dissent came from Justice Elena Kagan, who focused on the assertion that the Cuban government always owned the docks. She points to the 2004 expiration of Havana Docks’ contract. She warns the Supreme Court’s interpretation of the act “treats all property interests as if they were perpetual ones." She sides with the Appellate Court, saying that Havana Docks’ claim should fail because the cruise lines did not use the docks during the time-limited concession.

The ruling sends the suit against the cruise lines back to the lower courts for further arguments.

There are other cases under the Libertade Act also pending in the U.S. courts based on Trump’s 2019 decision not to extend the suspension of the act. Presidents before Trump had suspended the enforcement of the act.

The Supreme Court in February also heard a case under the act brought by Exxon Mobil seeking compensation from the Cuban state-owned oil company CIMEX. The U.S. energy company lost its oil and gas assets in Cuba, which were seized by the Castro regime after the revolution and handed over to the state oil company.

In 2022, it was noted that more than 40 Libertad Act suits had been filed, including cases against commercial shipping companies Maersk, MSC, Crowley Maritime, and Seaboard Marine. Some of the cases brought under the act, such as Crowley Maritime and American Airlines, have reportedly reached settlements, while others will be impacted by the decisions in the cruise line case and the yet-to-be-announced decision by the Supreme Court in the ExxonMobil case.

China probes causes of deadliest coal mine blast since 2009

The causes of a gas explosion at a coal mine in China’s Shanxi province are under investigation and officials with the company were detained following the nation’s deadliest such incident since 2009, state media said.

Authorities at a briefing late Saturday lowered the death toll to 82 from an earlier estimate of 90. They said two people remain missing and 128 are hospitalized after Friday’s blast, according to Xinhua. Rescue efforts continue.

Chinese President Xi Jinping urged stronger risk inspections and hazard controls, and called for heightened vigilance during the current season, when heavy rain and floods are more common. Premier Li Qiang echoed the directives, seeking transparent information disclosure and tighter enforcement of safety responsibilities across key sectors, Xinhua News Agency reported.

China’s State Council investigation team will conduct “a rigorous and thorough investigation to fully ascertain the causes of the accident, clarify the responsibilities of local authorities, industry regulators and the company, and impose severe penalties in accordance with laws and regulations,” Xinhua reported.

The investigation team also called for a nationwide review of mining safety measures and a crackdown on illegal practices, including hidden work sites, falsified monitoring data, unclear worker counts, and improper subcontracting.

Vice Premier Zhang Guoqing was sent to Shanxi to oversee the emergency response efforts, including search and rescue, medical treatment and handling of the aftermath, Xinhua reported. He urged authorities to verify the number of missing workers and prevent secondary casualties.

China has dramatically reduced coal mining fatalities in recent years, but the vast industry continues to juggle competing priorities. The government has pushed output to a record to meet energy security demands, even as safety officials crack down on over-stressed facilities and blame mine owners and operators for accidents.

The mid-sized Liushenyu mine, owned by Shanxi Tongzhou Coal & Coke Group, has an annual production capacity of 1.2 million tons of mostly coking coal — a modest sliver of the province’s overall output of 1.3 billion tons a year.

Even so, the explosion is classed as a very serious accident under Chinese regulations. Both the accident and the widespread security checks that will follow come at a challenging time for the domestic coal market, with supply already tight due to summer demand and upheaval in exports from Indonesia, a major supplier.

Even after years of dramatic renewable energy growth, coal remains a key pillar of China’s energy mix, underpinning power generation and industrial activity. It’s also one of few options to make up for current shortfalls in liquefied natural gas supply from the Persian Gulf.

Six teams totaling 345 people have been dispatched by the Ministry of Emergency Management to assist with the rescue, according to local reports, while victims are being treated for injuries including exposure to toxic gases. One miner interviewed by the Beijing News described being knocked out by the blast, only to awaken in darkness before crawling to safety through air thick with dust.

An executive at the company involved in the explosion has been detained, Xinhua reported, citing the rescue command headquarters.

The last coal mine accident that had a higher death toll was a 2009 explosion at the Xinxing mine in Heilongjiang province, near the Russian border, that killed 108 people.

At least 90 dead in China’s worst coal mine disaster in over 16 years

Rescue efforts after mine explosion. Credit: Xinhua | Weibo

At least 90 people were killed in a gas explosion at a coal mine in China’s northern province of Shanxi, the country’s deadliest mining accident since at least 2009.

The gas explosion occurred late on Friday at the Liushenyu coal mine in Qinyuan county, with 247 workers on duty underground, state media Xinhua reported.

The mine is operated by Shanxi Tongzhou Group Liushenyu Coal Industry, which was established in 2010 and is controlled by Shanxi Tongzhou Coal Coking Group, according to corporate database Qichacha.

Rescue operations were ongoing and the cause of the accident was under investigation, according to the local emergency management authority in Qinyuan. Shanxi is China’s coal-mining heartland.

President Xi Jinping called for authorities to “spare no effort” in treating the injured and conducting search and rescue operations, while ordering a thorough investigation into the cause of the accident and strict accountability in accordance with the law, according to Xinhua.

Premier Li Qiang called for timely and accurate release of information and rigorous accountability.

China has significantly reduced coal mine fatalities – often caused by gas explosions or flooding – since the early 2000s through more stringent regulations and safer practices.

In 2009, a coal and gas outburst in Heilongjiang Province killed 108 people and injured 133.

Executives of the company responsible for the mine have been detained, Xinhua reported.

Shanxi provincial authorities have dispatched seven rescue and medical teams totalling 755 personnel to the site, the emergency management bureau at Qinyuan said.

(Reporting by Shanghai Newsroom and Fabiola Arámburo in Mexico City; Editing by Tom Hogue, Kim Coghill and William Mallard)

CU

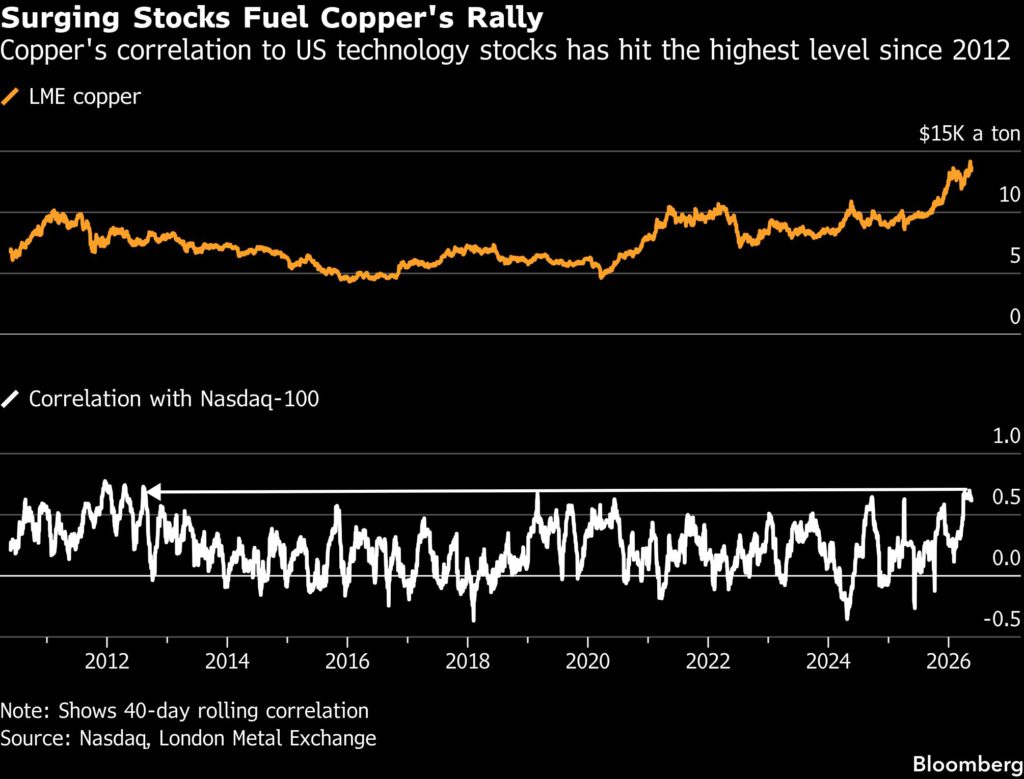

Bellwether industrial metal copper is trading like an AI stock

Copper, famed for tracking shifts in the global industrial economy, is trading like a high-flying tech stock as investors bet that skyrocketing power use for artificial intelligence will fuel a surge in demand.

The highly conductive metal that’s crucial for data centers and power grids has recently been moving in near-lockstep with stocks like Nvidia Corp. and ASML Holding NV. Prices climbed to a record close last week, then retreated as AI-related equities hit turbulence, and were rallying again on Friday as investors returned to the sector.

The gyrations reflect how copper’s exposure to all the transmission lines, transformers and electrical equipment needed to power AI has become a key pillar in the bullish outlook for the metal. For now, that’s outweighing mounting worries about the Iran war’s impact on the more traditional industrial bedrock of copper demand.

“This round of the rally is mainly driven by a structural AI-themed trade,” said Xu Shendi, director of base metal trading at DH Fund Management Co., one of China’s biggest hedge funds. She is neutral to bullish on copper’s outlook, and said further gains are likely to require a fresh wave of investor inflows into the tech sector, alongside tighter mine supplies.

AI isn’t the only force behind the rally. Investors have also been piling into hard assets like copper as a hedge against inflation, while chronic underinvestment in new mines sets the market up for a severe supply deficit.

“Commodities have gone from being an overlooked asset class to becoming increasingly attractive for multi-asset investors,” said Matt Miskin, co-chief investment strategist at Manulife John Hancock Investments. “This is really a three-legged stool for copper: AI demand, inflation hedging and a run-it-hot macro environment.”

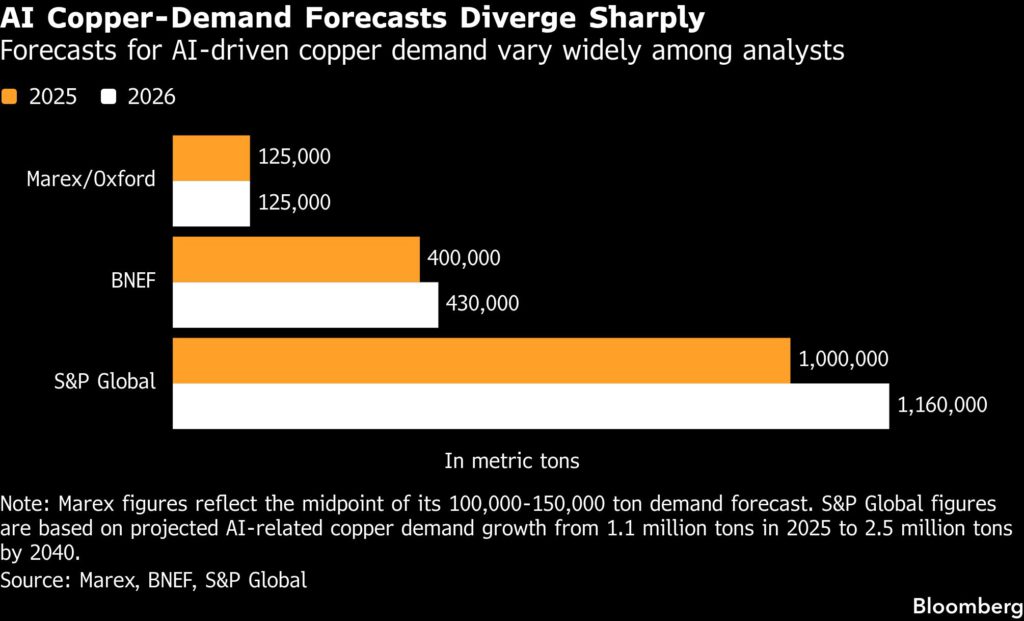

Analysts vary widely on AI’s impact on copper demand, with estimates ranging from about 125,000 tons annually over the past three years to 1.1 million tons projected for data centers in 2025. Commodities trader Mercuria expects about 350,000 tons of growth this year, up from under 400,000 tons in 2025.

While that’s only about 2.5% of annual demand, Mercuria’s head of metals research, Nicholas Snowdon, told an industry conference in Hong Kong earlier this month that he expects the AI industry’s growth to be similar to that of China’s electric-vehicle and renewables sectors, which have become a major source of copper demand in less than a decade.

Still, some warn that the copper market is pricing in the demand uplift far too early.

Recent research by commodities brokerage Marex Group and Oxford University notes that while Microsoft Corp., Alphabet Inc.’s Google and Amazon.com Inc. have committed some $580 billion to US data center projects this year, the industry is running into formidable bottlenecks in securing labor, power, equipment and permits.

“For copper, it’s not really the data centers themselves that matter most — it’s the power generation and transmission network required to support them,” said Guy Wolf, Marex’s global head of market analytics. “The AI narrative is bullish for copper, but the actual metals demand is probably further into the future than many investors assume.”

Even so, Wolf noted that there are risks for traders thinking of betting against the rally, given the sheer size of recent inflows into technology stocks.

Copper’s surge has come as money managers have added about $14 billion in net-long positions in futures markets in London and New York so far this quarter. Over the same period, the combined market capitalization of Nasdaq-100 companies has risen by $7.8 trillion, according to calculations by Bloomberg News.

“We haven’t really seen this kind of institutional interest since the China supercycle,” Wolf said, referring to the years earlier this century when rapid Chinese growth led to a commodities boom. “Even a small portfolio allocation shift into hard assets can overwhelm the market.”

Bearish investors also risk being burned by the re-emergence of a lucrative trading opportunity linked to the risk that the US will impose tariffs on imports of the metal. Copper prices on New York’s Comex have jumped above those on the LME in recent weeks, allowing traders to capture the arbitrage by shipping cargoes to the US.

LME futures were trading at about $13,630 a ton on the LME on Friday, while Comex prices were about $400 higher. Orders to withdraw copper from warehouses tracked by the LME jumped the most since 2013, in a sign that traders may be looking to move stock into Comex warehouses to capture the higher prices.

That dynamic could end up triggering fresh bidding wars among buyers seeking to secure available metal, even in an environment where demand is weakening.

Earlier in the year, a rebound in Chinese demand had supported copper’s rally, with buoyant spending in power grids and the renewable energy sector offsetting losses from the property sector, which was the engine powering copper demand for much of the 21st century. But close-to-record prices are starting to deter manufacturers.

The US premium is “driving all the metal flows that way, and China’s fundamentals do not matter any more,” said Harry Jiang, a trading manager with China Base Ningbo Group. “China is increasingly a price taker, not a price setter.”

In the past, investors have often been caught out as swift downturns in spot demand in China have upended their bullish bets on future growth. But Matthew Fine, who started investing in copper miners after joining Third Avenue Management as a portfolio manager in 2017, remains confident that the long-term trajectory is higher.

Even factoring in new demand from the AI sector, copper demand is only likely to grow at 2.7% annually through to 2040, he said. But crucially, miners look increasingly unable to keep pace, as new projects grow scarcer and more expensive to develop.

“AI may be the latest component of evolving demand, but the projected growth rates are no different than they’ve been for 125 years,” he said. “We look like, as a planet, we’re going to be short in a real way pretty soon.”

3D-Printed Copper Plates Could Cut Data Center Cooling Energy Use by 97%

A University of Illinois Urbana-Champaign team published research showing 3D-printed pure copper cooling plates could reduce data center cooling energy use from 30-40% of total power draw to just 1.1%.

The plates use a mathematical topology optimization algorithm to redesign internal fin structures into complex shapes that maximize heat transfer while slashing the pumping energy required to move coolant.

The plates are built using electrochemical additive manufacturing (ECAM), which can produce pure copper components with detail down to 30-50 micrometers -- finer than a human hair.

The artificial intelligence boom is creating an energy monster that the world is unprepared and unequipped to deal with. Providing enough energy to fuel the AI ambitions of the future as well as to support human demand and development will require advances in energy technologies that are as-yet undiscovered. “There’s no way to get there without a breakthrough,” Sam Altman, co-founder and CEO of ChatGPT firm OpenAI, said at the 2024 World Economic Forum in Davos, Switzerland.

More accurately, it will probably require several breakthroughs. Altman was referring to the need to fund nuclear fusion research when he made his infinitely quotable statement at Davos, but reigning in the AI energy monster will not only require next-gen energy generation, it will also require a great leap forward in data center design and energy efficiency. And a team of researchers from University of Illinois Urbana-Champaign, USA may have made just such a breakthrough.

An innovative form of 3D-printed copper cooling plates could revolutionize the design of data centers and slash the amount of energy needed to cool them, according to a new scientific paper published in the academic journal Cell Reports Physical Science. The team of researchers found that their innovative pure copper plate model, which was designed using a cutting-edge mathematical algorithm, uses just a fraction of the energy that conventional cooling plates use.

The potential impact of this discovery is enormous. The computer chips used to run the computations for large language models create an enormous amount of thermal energy in a process known as Joule heating. In the course of one hour, a single computer chip creates roughly enough heat to boil 50 cups of water. And AI data centers typically house hundreds of thousands of these kinds of computer chips. And, as computer chips become more and more powerful, their heat emissions climb ever higher.

As a result, cooling systems are of central importance to the functioning of data centers – and they require a whole lot of energy to run. Cooling systems currently represent a whopping 30 to 40 percent of AI data centers’ energy use. When implementing the new 3D-printed plates, that figure drops to just 1.1 percent, an astonishing and potentially game-changing savings.

“Cooling is the bottleneck in computer-chip design,” Behnood Bazmi, mechanical engineer and the paper’s first author, was quoted in a press release accompanying the publishing of the paper. “By bridging the gap between computational design and manufacturing capability, our approach provides a pathway for more energy-efficient liquid cooling of chips and other electronics.”

Cold plates are already in commercial use in data center applications, but they are designed for ease of manufacturing rather than for optimal performance. The solution presented by the University of Illinois Urbana-Champaign team addresses two critical downsides to conventional cooling systems by redesigning both the materials used as well as the way that those materials are configured.

“In a technique known as topology optimization, the researchers used a mathematical optimization algorithm to redesign the tiny internal fin structures from the conventional rectangular or cylindrical geometries into far more complex, jagged, and pointed shapes that maximize heat transfer and thermal performance, while minimizing the pumping effort required to move coolant through the plate,” New Atlas reported earlier this week.

To facilitate the construction of such a complex model, the team turned to 3D printing – more specifically, electrochemical additive manufacturing (ECAM), to build the plate’s intricate and craggy surface one layer at a time. This allows for an extremely delicate and nuanced approach to building a far more sophisticated – and therefore more energy efficient – cooling system. “ECAM can manufacture pure copper parts with very fine detail – down to 30 to 50 micrometers, less than the width of a human hair,” says study co-author Nenad Miljkovic.

Trafigura Group has moved to withdraw hundreds of millions of dollars of copper from London Metal Exchange warehouses as lucrative trading opportunities emerge in the US and China, according to people familiar with the matter.

The trading house was the main party involved in orders to withdraw more than 51,000 tons of copper from LME warehouses in the US and Asia on Friday, said the people, who asked not to be identified due to the commercial sensitivity of the matter.

The orders — which were the largest seen on the LME since 2013 — come as copper futures on New York’s Comex have surged above prices on the LME, creating a huge incentive for traders to deliver copper into the US.

Comex contracts have been trading at a premium over the LME for most of the past year, due to the possibility that the Trump administration will impose tariffs on the metal. Record volumes of copper were shipped to the country last year as traders cashed in on the arbitrage, and Trafigura’s withdrawal of stock is a sign that the seismic trading opportunity is gaining new momentum.

More than 30,000 tons of metal was ordered out of LME warehouses in New Orleans and Baltimore on Friday, and they’re likely to be delivered into Comex warehouses or to end buyers in the US market, the people said. The trading opportunity exists because Comex copper prices are inclusive of duties, while LME prices aren’t.

Nearly 20,000 tons of copper was also withdrawn from LME warehouses in Asia. While the US could be an attractive destination for some of that metal, rising prices in China are also creating incentives to ship copper there too.

With LME prices trading around $13,660 a ton on Friday, the total value of the metal that’s been ordered from the exchange is more than $700 million.

A spokesperson for Trafigura declined to comment.

(By Mark Burton and Jack Farchy)

Zambia’s Konkola reopens Chingola copper mine after 18-year shutdown

Nchanga mine in Chingola, in the Copperbelt Province of Zambia. (Image courtesy of Wikimedia Commons)

Zambia’s Konkola Copper Mines resumed mining at its Chingola “B” Mine on Thursday, 18 years after operations ceased, as Africa’s second-largest copper producing nation pushes to more than triple its annual output to 3 million tons by 2031.

The mine, part of the Nchanga mining complex, is projected to produce more than 200,000 tons of ore per month, KCM chief executive Deshnee Naidoo said in a statement.

The mine produced about 60,000 tons per month at an average grade of 2.5% between 1980 and 2003.

KCM, 79.4% owned by Vedanta Resources and 20.6% by Zambia’s state investment company ZCCM-IH, operates mines and processing plants in Chingola, Chililabombwe, Kitwe and Nampundwe.

Zambia produced 890,346 tons of copper last year, below its 1 million tons target.

(By Chris Mfula; Editing by Olivia Kumwenda-Mtambo and Peter Graff)

Codelco eyes $2 billion gain from unifying copper mines in Chile

Codelco is seeking a combined $2 billion in cost savings and additional revenue by integrating the operations of three copper mines as the state-owned Chilean company tries to offset the impact of stagnating output and rising debt.

The plan to integrate the Chuquicamata, Radomiro Tomic and Ministro Hales mines in the north of the country was recently presented by management to Codelco’s board of directors, according to people familiar with the situation, who asked not to be identified discussing confidential information

The plan envisages gains beginning to kick in as soon as 2027 as a result of unifying operational planning for the mines and sharing processing plants, possibly under a single management structure, the people said. Codelco didn’t immediately respond to requests for comment.

The proposed mine integration is part of a company-wide, four-year production plan that Codelco intends to present to the government in the coming months.

Like other copper producers, Codelco is facing inflationary pressures that have eroded the benefits of record prices for the metal. War in the Middle East has driven up the cost of energy and sulfuric acid, a key input for copper processing. Declining ore grades are also forcing producers to process a greater volume of rock to maintain output.

The need to improve efficiency is especially acute for Codelco given its heavy debt load and spending commitments. The company is already busy integrating a central Chile operation with an adjacent Anglo American Plc mine, and it increasingly relies on private-sector partnerships for exploration projects.

The proposed reorganization at Codelco’s northern mines would include sending ore from one pit to another’s plants and blending material to better align with customer needs, according to the people. One option would entail cutting management roles, although on-the-ground teams would remain intact, the people said. Talks with unions are already under way.

(By James Attwood)

India’s top copper producers oppose inclusion of scrap-based rods in standards

India’s top copper producers, including Adani, Vedanta and Hindalco, are opposing plans to make copper wire made by secondary refiners acceptable under government quality standards, saying products made from scrap pose safety risks.

The dispute has triggered a months-long standoff between large primary producers and smaller refiners over fire-refined high conductivity (FRHC) copper rods, which are mainly used in electrical applications such as transformers, power cables and wires.

Large producers argue that copper rods from smaller refiners, which mostly use scrap as raw material, should not be under the same standards because the products may not consistently meet the purity levels required for electrical applications.

“Indian fire (secondary) refiners may not have the requisite technology and hence are incapable of manufacturing the FRHC grade consistently,” the large producers said, according to the minutes of a March 23 meeting of the Bureau of Indian Standards (BIS) that was reviewed by Reuters.

The state-run BIS oversees product quality standards in India.

“Many of the manufacturers are not refining and just re-melting scrap to make substandard product,” the minutes said of the views expressed by the Indian Primary Copper Association (IPCPA).

The IPCPA’s partners include Adani, Vedanta, Hindalco and Hindustan Copper.

In the minutes, secondary producers defended their production method, saying fire refining is used to control the chemical composition of copper and meets conductivity requirements used internationally for cable manufacturing.

The BIS did not respond to requests from Reuters for comment.

IPCPA president Rohit Pathak said the industry body was seeking separate standards for FRHC copper because “fire refining which uses copper scrap as the primary input, cannot remove impurities to achieve 99.99% purity required for electrical applications.”

“Lower purity will increase overheating and fire risks. A separate standard will help ensure safe usage,” Pathak, who is also CEO of Hindalco’s copper business, told Reuters in a statement.

India’s total demand for copper rods in the fiscal year to end-March 2025 was estimated at 1.2 million metric tons, of which imports accounted for 0.1 million tons, while FRHC copper rod production stood at 0.4 million tons, according to industry estimates.

Imports are mainly sourced from the United Arab Emirates, although supplies have been disrupted this year by the Middle East conflict.

As a result of the dispute, about 400,000 tons of copper wire rod is currently being traded outside the quality control regime, an industry source said.

(By Neha Arora; Editing by Mayank Bhardwaj and Raju Gopalakrishnan)

CHART: Copper price surge mints 23 new unicorn mines

Tech venture capitalists invest in startups and get to call them unicorns. The official definition of a unicorn is a startup with a $1 billion valuation while still a private company. There are 1,765 unicorns globally, past and present.

MINING.COM believes the mining industry deserves a similar category of company to catch the imagination of the mainstream investor and compete against Silicon Valley, crypto and hyperscalers for smart (and dumb) investment dollars.

If we must, and it appears we do, we need to think of mines as the apps of the industrial economy (submissions for a better analogy welcome). Physical AI is, unfortunately, already taken.

While we’re at it, might as well rebrand junior mining. Let’s call them startups to attract more outside/bluesky capital from the likes of the Softbank Vision Fund, which, I’m happy to remind readers, invested $300 million in Wag!, a dog walking app that helpfully keeps you updated in real time about your pet’s excretions. (The app survived, the company didn’t.)

Even mining startups that have hastily added Critical Minerals to their names, or better still, Rare Earths (greater crustal abundance than copper to be fair so not that much of stretch) struggle to attract funny money from the Masayoshi Sons of this world.

Miners need to find a way to compete with world-changing companies like Opensea, a now defunct marketplace for Bored Ape Yacht Club NFTs, which peaked at a $13 billion valuation. Which is more than Ivanhoe Mines is worth today, sorry to say.

Copper is so hot right now and it seems apt that the second MINING.COM list of unicorns is also based on the bellwether metal. Data centres need copper by the block cave full (Cu can account for nearly 6% of initial outlays) and will help the industry siphon off some of the trillions of dollars flowing into compute.

The MINING.COM Unicorn Index does not seek to compare orange metal apples with tech apples. How can it? Mining simply has no equivalent to the $1 billion bike-sharing startup and NI 43-101 makes rug-pulling difficult, although not for lack of trying.

Last week copper set a new record at $6.667 a per pound, or $14,700 a tonne. Based on 2025 mine-level production numbers, at that price 75 mines throw off a nominal $1 billion or more per year just from the copper (and quite a few now do so at negative cost thanks to copper mining’s least best kept secret – byproduct credits). That’s 23 more than MINING.COM’s previous rainbow of unicorns.

US new sanctions revive a decades-old clash with Sherritt, rooted in the 1990s. (Image courtesy of Sherritt International.)

US new sanctions revive a decades-old clash with Sherritt, rooted in the 1990s. (Image courtesy of Sherritt International.)