Inflation Jumps, Propelled by War-Driven Energy Costs

Photograph by Nathaniel St. Clair

As expected, inflation was sharply higher in March than in prior months. The overall inflation rate for March was 1.3 percent, although inflation in the core index was just 0.2 percent. This brought the year-over-year rates in the overall index to 3.3 percent, and in the core index to 2.6 percent.

The jump in war-related inflation was expected, but it is important to note that inflation was already on an upswing even before the war started. The Personal Consumption Expenditure deflator (PCE) for February rose by 0.4 percent, as did the core PCE. Year-over-year inflation in the PCE was 2.8 percent overall and 3.0 percent in the core index.

The acceleration was clear in the annualized rate for the last three months. In the overall index it was 4.1 percent, while in the core index it was 4.4 percent. It is important to remember that inflation had been headed lower throughout 2023 and 2024. Most analysts expected the inflation rate to hit the Fed’s 2.0 percent target in 2025 or at least be very close to it.

As the first inflation data since the start of the war, the March CPI showed inflation is accelerating even further. The annualized rate in the overall CPI over the last three months was 5.3 percent. It was 2.9 percent in the core index.

Inflation in the core index was held down by some likely anomalous readings. The health insurance index, which accounts for just over 1.0 percent of the core index, fell by 1.4 percent in March. This index, which measures the operating costs and profits of insurers, is unlikely to keep falling.

The auto insurance index, which accounts for 3.4 percent of the core index, was flat in March. This index had been rising at double-digit rates from 2022 to 2024, but has risen just 0.8 percent over the last year.

There also appears to have been a sharp fall in the legal services index. While the sample was too small to post the index itself, it led to a March decline of 1.2 percent in the “miscellaneous personal services” index, which accounts for 1.2 percent of the core CPI. The prices rose for all the listed items in this category, except for the tiny non-laundry apparel services category, where prices fell 0.2 percent. Anyhow, this will likely not be repeated.

It seems inflation was accelerating even before the war. The surge in oil prices added fuel to the fire, but inflation will likely be well above the Fed’s 2.0 percent target for the foreseeable future, even if the ceasefire lasts and oil begins flowing through the Strait of Hormuz in the near future.

Individualized Medicine: Pay for the Research Upfront

The New York Times had an interesting column by Jeff Coller, the director of the RNA Innovation Center at Johns Hopkins University, on the promise of individualized medicine for treating rare diseases. The piece points out that while specific “rare” diseases are by definition rare, collectively they are not. It reports that 25 million people in this country have some form of genetic disorder. By Coller’s account, the medical costs from these diseases come to over $400 billion a year (1.3 percent of GDP or 40 percent of the military budget) in addition to the cost they impose on the patients’ lives.

The gist of Coller’s piece is that the normal structure of the FDA approval process for traditional drugs is not appropriate for the sort of gene editing that is being developed to treat these rare diseases. It is not really possible to have large-scale clinical trials to establish safety and effectiveness. As an alternative, Coller suggests a process whereby the FDA would establish accreditation to an institution or group of doctors that effectively follow procedures to treat conditions.

While this approach sounds promising, it is also worth commenting on the funding side of the equation. Coller’s point that the traditional regulatory process for approving drugs is not appropriate for these individualized treatments also applies to the patent-monopoly financing model for their development. Relying on patents could lead to an absurd situation where a researcher or company holds a patent on a treatment that may literally apply to just one patient.

Rather than try to recoup costs through this route, it would make far more sense to allocate funding to develop the technology, which then can be used at no cost, other than the direct cost to pay the doctors and other healthcare professionals involved in administering the treatment. This would also have the benefit that all the research can be made freely available to other researchers, since that could be a condition of the funding.

I have harped on this point endlessly, since government-granted patent monopolies both create the artificial problem of high prices and are a recipe for corruption in the pharmaceutical industry. It would be great to get more examples of the effectiveness of upfront funding of research.

This first appeared on Dean Baker’s Beat the Press blog.

Who’s Counting? Gas Prices, the Stock Market, and Dead Children

Photograph by Nathaniel St. Clair

Collapsing in panic over the price of gas is a characteristically incoherent American tradition. The highly paid press, political officials, and the same people who ignore as a matter of routine the rising costs of housing, health care, and higher education treat a 25-cent-per-gallon jump in fuel as tantamount to the apocalypse. Meanwhile, something similar to the apocalypse actually threatens livable ecology on Earth (the universe’s only habitable planet for those keeping count), largely due to the extraction of fossil fuels, but biodiversity in a boiling world is hardly relevant. Or, at least, that is what one could discern from watching CNN and MS-Now, formerly MSNBC, both of which keep a running tracker of the average cost of gas, breathlessly announcing a three-cent increase or one cent drop as if they are reporting live from the fall of the Berlin Wall. Evidently, they would consider it impolite to mention that, according to Car and Driver, most of the top 25 selling automobiles in the US are heavy-duty pickup trucks and large SUVS, notoriously unsafe and expensive vehicles that guzzle gasoline with the same speed and appetite of frat boys using beer bongs at a kegger. If Americans were actually concerned about paying for gas, they would drive fuel economy cars.

Of course, any increase in the cost of living hurts the poor, but many impoverished Americans in inner cities use public transportation, and for those who do own their own cars, rent, health insurance, and the financial barriers to college are much graver concerns.

The fixation on fuel going up or down by a couple of quarters per gallon allows Americans to display the narcissism that accompanies geographic and intellectual isolation. Drivers in the US already consume the highest amounts of gasoline, at the cheapest rates, in the developed world. Paying little attention to the devastating environmental effects, the country continues to build more highways, purchase more monstrous vehicles that belch fumes out of the exhaust pipe, and to quote Joni Mitchell, “pave paradise to put up a parking lot.”

Social psychologists and thoughtful economists have posited that the American fixation on the price of gas operates at the subconscious, symbolic, and ultimately, irrational level. Because they see the cost advertised at gas stations at every corner, they become emotionally invested in its fluctuation. It becomes emblematic of the cost of living in such a way that housing and health care never could, especially for those locked into fixed mortgage payments and with coverage from employer-based insurance or Medicare. To reduce it to the most simplistic terms, it’s a number; a number in the face of the average middle class or upper class American no matter where they go, typically by car, or what they do, just like the price of oil is a number, and the stock market, which often moves in the opposite direction of the cost of gas, is a number.

Here’s another number: 168. That is the number of people, most of whom were children, killed when the US fired a missile at an Iranian elementary school on February 28th, 2026. No major news outlet has flashed 168 on its airwaves or in its pages at anywhere near the rate that they dissect gas prices. Senator Raphael Warnock, of Georgia, has called for an investigation of the bombing, while denouncing Donald Trump’s war policy and Pete Hegseth’s leadership more broadly, but its has failed to register as a salient issue with his political party, the mainstream media, or any of the prominent podcast bloviators who have managed to replace public intellectuals in the discourse.

None of this is to say that the bombing was kept secret. The legacy press did report on it multiple times. Pete Hegseth, who, according to rumor, his aides have nicknamed “Dumb McNamara,” has dodged questions about it from the press, and his boss, Dumb Nixon (?), claimed that Iran was responsible for bombing itself. “They are very inaccurate with their munitions,” Trump said. The insult might have struck Iranians as rich, who, as they bury their children, might recall that, during his first term in the White House, Trump eliminated the standards that Barack Obama put in place to avoid killing civilians in drone strikes targeting alleged terrorists. Obama’s own record was abysmal, as his administration killed far more innocent family members and neighbors of supposed terrorists than terrorists themselves. But a dissatisfied Trump wanted even more death. And now he is getting it.

War in Iran is unpopular with the American people, but even among those who disapprove, there is little discussion about the Iranians who have died and who will die as a result of a mindless exercise of US power. There is far greater scrutiny of how the war will influence everything from the cost of groceries to the midterm elections, and of course, an obsessive monitoring of the number on the digital screen at the fuel pump. A review of other numbers demonstrates that American leaders and many voters have a long tradition of ignoring the blood on their hands. To remain within relatively recent history with only two of countless examples, journalist Nick Turse details in his extraordinary and disturbing book, Kill Anything that Moves: The Real American War in Vietnam, that the US killed two million civilians during the Vietnam War, most of them in deliberate acts with “heavy firepower.” After the war ended in 1975, the US left four million Vietnamese exposed to Agent Orange, which causes birth defects, brain damage, high rates of cancer, and early onset heart disease. Decades later, in 2003, the US invaded Iraq for the second time in thirty years, with a “shock and awe” campaign that led to an occupation that lasted for nearly nine years. Researchers at Brown University estimate that over 432,000 Iraqi civilians died during the US war of aggression, and that many more suffered premature deaths and debilitating diseases, in a repetition of Vietnam, due to the toxic chemicals, munitions, and military pollutants that lingered in the atmosphere long after the US press and population moved on to stories they found more fascinating, like the latest intrigue of Kardashian family and the guest list at Jeff Bezos’s wedding.

To track the priorities of the American attention span, one might want to consider a juxtaposition of stories from 2025, the contrast of which offers a nifty sociopolitical experiment. In July of that year, the Trump junta shut down USAID, an international organization that provided medical, infrastructural, and food assistance to millions of people in the developing world. Despite the too often violent and predatory aims of US foreign policy, USAID managed to save and otherwise improve the lives of many of the poorest people on the planet. For no discernible reason or purpose, other than racist psychopathy, Donald Trump and his then-henchman, Elon Musk, shuttered the agency, all while flashing wicked, deranged grins and making self-congratulatory posts on social media. As early as November of 2025, the Harvard T.H. Chan School of Public Health concluded that the end of USAID operations caused hundreds of thousands of people to die from starvation, complications of HIV/AIDS, and the effects of treatable diseases.

Also in the fall of 2025, the restaurant chain, Cracker Barrel, changed its logo, removing a depiction of an old man in bib overalls leaning on a barrel, in an attempt to adopt a more modern image. The fallout was intense. Republican lawmakers issued statements denouncing the corporate rebranding effort as “woke.” The political press summoned its resident geniuses to analyze what the logo change, and the anger it provoked, indicated about US politics, and the business press ran lengthy dissections of the decision and its aftermath. The conclusion is as painful as it is unavoidable: According to the calculus of US culture, as measurable by press coverage, political debate, and popular interest, Cracker Barrel’s logo is more important than the preventable deaths of hundreds of thousands of people in Africa and the Middle East.

Given the enormous precedent, it is hardly surprising that the deaths of 168 Iranians, mostly children, can barely rate in comparison to tomorrow’s gas prices. It is something to keep in mind the next time a member of the Trump junta, US Senator, or cable news pundit with a flag pin on his lapel clears his throat to repeat a bromide about America’s respect for “human life,” “freedom,” and “democracy.”

The Market Law of One Price – How the Donald Bombed Energy Consumers, Too

The Donald plunged into one hell of a hornets nest when he took the bait from Bibi Netanyahu and launched an all out “kinetic” war on Iran (as distinguished from the brutal economic war Washington has been waging for decades). But now that the gasoline pump price has breached $4/gallon and is heading higher, he’s desperately looking for an off-ramp.

Yet the one he has seized upon in the last 48 hours or so is not even remotely fit for purpose. To wit, he threatens to pick up Washington’s military football and go home, leaving what’s left of the Iranian government – mainly the brutish IRGC – in charge of the Strait of Hormuz. That is, operating a toll booth and military checkpoint on a waterway that had been open to world commerce free of charge until the Donald foolishly unleashed bombs and missiles on Iran on February 28th.

“we don’t import much oil from there anymore… within 2-3 weeks, we’ll leave. That’s not for us. A guy can take a mine, drop it in the water. That can be for France or whoever is using the strait”.

The presumption, of course, is that because the US imports virtually no petroleum from the Persian Gulf the new Hormuz toll booth is Europe’s and Asia’s problem, not Washington’s. And that’s technically true but here’s the spoiler alert: What matters is not the geography of where the barrels of hydrocarbon molecules are moving from and to at any given point in time, but the level of hydrocarbon prices embedded in the digital bits coursing through the global futures and cash markets all the time and everywhere.

That’s because the latter reflects the markets’ judgement about the state of global supply, demand and inventories in totality. Unlike the Donald, traders on the exchanges are fully familiar with the potent process of market arbitrage. In this case, it means that when the same hydrocarbon molecule has radically different prices around the planet, then some enterprising traders will buy them where the price is low and ship them to where it’s high, and pocket the profit, net of shipping costs, insurance, interest carry cost and other nits and nats of market operation.

The consequence, of course, is the “law of one price” worldwide. Rather than zero exposure to the Persian Gulf’s slow-steaming barrels of hydrocarbon molecules, the US has 100% exposure to Gulf-impacted digital price bits being digitally transmitted instantaneously around the planet on a 24/7 basis.

Accordingly, if the Donald thinks the oil price is going to be high in Europe and Asia because they get their hydrocarbon molecules from the Persian Gulf and low in the USA because we are 100% self-sufficient in oil and gas, he is sadly and utterly mistaken. The digital networks of the paper and cash markets will quickly equilibriate the price of hydrocarbons on a worldwide basis, and the physical barrels will not be far behind.

So lets start with the home team that the Donald thinks somehow operates as an economic island all by its lonesome, unconnected to the global markets. But for this purpose we must look at the entire oil and natural gas complex because under the law of one market petroleum and nat gas molecules are highly interchangeable. And we also measure everything in BOE (barrels of oil equivalent) in order to avoid apples and oranges on the price quotations.

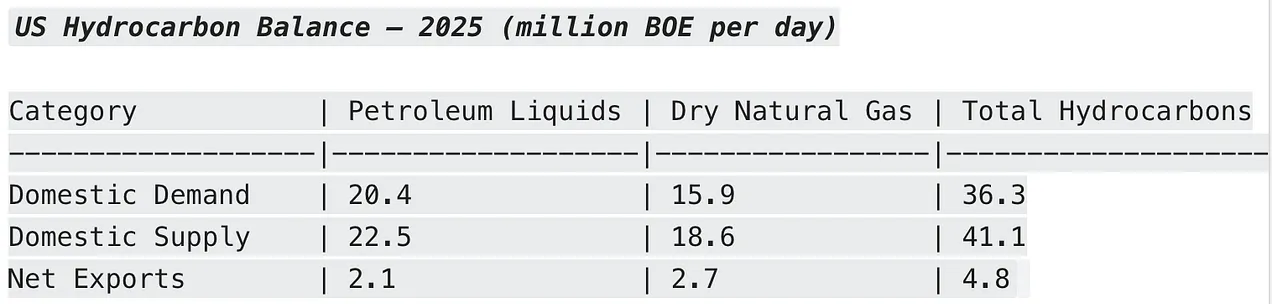

Thus, if we look at just the domestic energy patch, the massive output of the US natural gas industry – heavily driven by fracking – towers well above conventional US crude oil production, including fracked crude. To wit, in 2025 field production of natural gas (i.e. “wet gas”) was 26.5 million BOE/day while crude oil and condensate from the field was 13.6 million BOE/day.

In terms of physical molecules and pricing, however, upwards of 30% of field production (7.9 million BOEs/day) of so-called “wet gas” consists of NGLs (natural gas liquids), mainly ethane, propane, butane and natural gasoline. All of these go into the same end markets – heating, cooking, petrochemicals and transportation – as similar liquids obtained from refinery runs of crude oil. The common molecules from both streams, therefore, are subject to the law of one market.

Thus, the 22.5 million BOE per day of total “petroleum liquids” supply shown in the table below includes a very large component of Natural Gas Liquids (NGLs) as follows:

- Crude oil + lease condensate: 13.6 BOE/d

- Natural Gas Liquids (NGLs): 7.9 BOE/d

- Refinery processing gain: ~1.0 BOE/d

The above hints at the price linkage between the oil and gas markets. The U.S. petrochemical industry, for instance, uses ethane as the primary feedstock for steam crackers that produce ethylene, which is the building block for plastics, packaging, and countless other products. Ethane from two main sources competes for the feedstock requirements of the steam crackers:

- Field-produced NGLs (extracted from wet natural gas at gas processing plants)

- Refinery-sourced ethane (produced as a byproduct when refineries process crude oil)

At the present time, NGL-derived ethane is generally cheaper and more abundant — especially from shale gas basins like the Permian and Marcellus owing to the continuing oversupply of natural gas. So it has captured the lion’s share of U.S. cracker feedstock in recent years.

By contrast, refinery ethane tends to be more expensive and less consistent in volume, so it often serves as a secondary or swing feedstock. Moreover, when NGL supply surges or the global price of crude oil and its derivatives rise, the ethane cracker feedstock competition intensifies. On the margin, petrochemical operators shift even more heavily toward the cheaper NGL-derived ethane, thereby linking U.S. natural gas prices to the global petroleum markets.

In any event, the convention with respect to industry statistics is to include NGLs extracted from natural gas wells in the “petroleum liquids” category. So to avoid double counting, we include in the table below only the dry gas portion of nat gas field production, which gets distributed to end markets by pipelines.

Accordingly, as shown below the USA in 2025 produced 41.1 million BOE/day of combined oil and gas, which well exceeded domestic demand of 36.3 million BOE/day. The latter went into the slate of refinery products sold domestically and the pipeline delivery of nat gas to domestic end markets.

The resulting arithmetic, of course, shows that the balance of supply over demand was accounted for by 4.8 million BOE per day of exports. This was a mix of crude oil (@ 1.4 million BOE/day and refinery products (0.7 million BOE/day) under the liquids column and mainly LNG under the dry gas column.

Still, the fact that domestic supply was 113% of domestic demand, does not mean the US economy is insulated from the current massive shortfall of both gas and oil coming out of the Persian Gulf. To the contrary, it means only that the process of arbitrage between geographic markets and near-substitutes among the gas and oil streams is far more complex and subtle than the “drill, baby, drill” rhetoric that the Donald dispenses in justification of what amount to his own attack on domestic users of globally priced hydrocarbons.

Needless to say, it is the 2.1 million BOE of liquids and 2.7 million BOEs of mainly LNG under the dry gas column in the table above that provide the transmission arteries by which domestic prices are linked to global prices. In basic form, the equation is straight forward: To wit, high prices abroad and low prices domestically will cause a massive incremental draw on US exports.

That is to say, if Qatari LNG is scarce and high priced, LNG exports from the US will increase – first from fuller utilization of existing LNG plants and then over time via increased investment in liquefaction capacity. Moreover, at the present time the LNG export market draw will be especially potent if Gulf supply remains curtailed and world LNG prices stay high.

Specifically, Iran’s successful attack on the huge Ras Laffan LNG facility in Qatar (and the prospect that the plant will be out of commission for up to several years) caused the Rotterdam price for LNG to soar from an average of about $69 per BOE in 2025 to current spot market quotes of @$152 per BOE.

So here is where the hidden magic of Mr. Market comes in – notwithstanding the Donald’s illusion that America is an insulated island of energy plenty and cheap prices. To wit, the current spot market price for pipeline natural gas in the US at the Henry Hub terminal is about $18 per BOE. So in the language of Mr. Rogers, can you say arbitrage?

Right now the 5.8 million of BTUs in pipeline gas form at Henry Hub (Louisiana) is priced at only 12% of the landed cost of 5.8 million BTUs in LNG form at Rotterdam. In this circumstance, of course, Mr. Market would also factor in about $20 per BOE to convert US pipeline gas to liquid form at an LNG plant and another $14/BOE to ship it to Rotterdam in a specially equipped LNG tanker.

But still, the apples-to-apples cost gap would remain at about $100 per BOE – that is, $52 per BOE for US gas delivered by LNG tanker to Rotterdam versus the current spot price there of $152 per BOE.

Of course, the arbitrage doesn’t work instantly and overnight. US Gulf Coast LNG plants currently have about 2.8 million BOE/day of capacity but are nearly fully utilized. So in the short run, the US/Rotterdam gap would likely just drive up spot prices and profitability on existing LNG contracts. However, there is also currently nearly 2.6 million BOE of new LNG capacity under construction in the US Gulf coast, which would nearly double current LNG export capacity when it comes on stream during the next several years.

So it is virtually guaranteed that the current $100 per BOE price gap between Rotterdam LNG and Henry Hub pipeline gas will close substantially, if shipments from the Persian Gulf remain restricted owing to Iranian military threats or just due to the delay in rebuilding the badly damaged LNG plants in Qatar and elsewhere.

More importantly, something else would happen as a second order effect that the Donald obviously hasn’t reckoned with, either. The Henry Hub price for pipeline gas at $18 per BOE is low relative to WTI for light crude oil at $100 per BOE or LNG at $152 per BOE in Rotterdam owing to the nature of the pipeline gas business.

That is, domestic demand for delivered pipeline gas is pretty much driven by the level of GDP embodied in household spending and business production. So when investment in the oil patch – and especially the fracking plays – leads to excess gas supply, the spot price of pipeline gas falls. There is very little excess inventory/storage in the industry by its nature beyond the large seasonal working stocks held by the pipelines and middle men.

This is somewhat different than the case of crude oil where there is a huge long standing export market and giant waterborne tanker fleets. Prior to February 28th, there was ordinarily about 60 million BOE per day of crude oil on the blue water, carried by upwards 2,400 crude oil tankers.

So when the Brent or WTI crude oil prices rise owing to the huge supply restrictions out of the Persian Gulf the immediate impact has been the rerouting of tankers to the US crude oil terminals to take oil to Europe and Asia. In turn, that tightens the domestic supply/demand balance, pushing domestic prices higher, as well.

Accordingly, US crude and product export volumes have been and will continue to rise as long as the Gulf remains restricted and global marker prices remain high. All other things equal, in turn, this means that domestic petroleum prices will rise and stay high, as well.

In the case of natural gas, the response time and arbitrage pathways move a little more slowly, but the market dynamic is the same: As more excess US pipeline gas is drawn into the rapidly expanding US LNG plants and thereby into the global export markets, the Henry Hub pipeline gas price will rise as the current surplus of gas “deliverability” is reduced. In turn, the gas bills of homeowners and business users will go up.

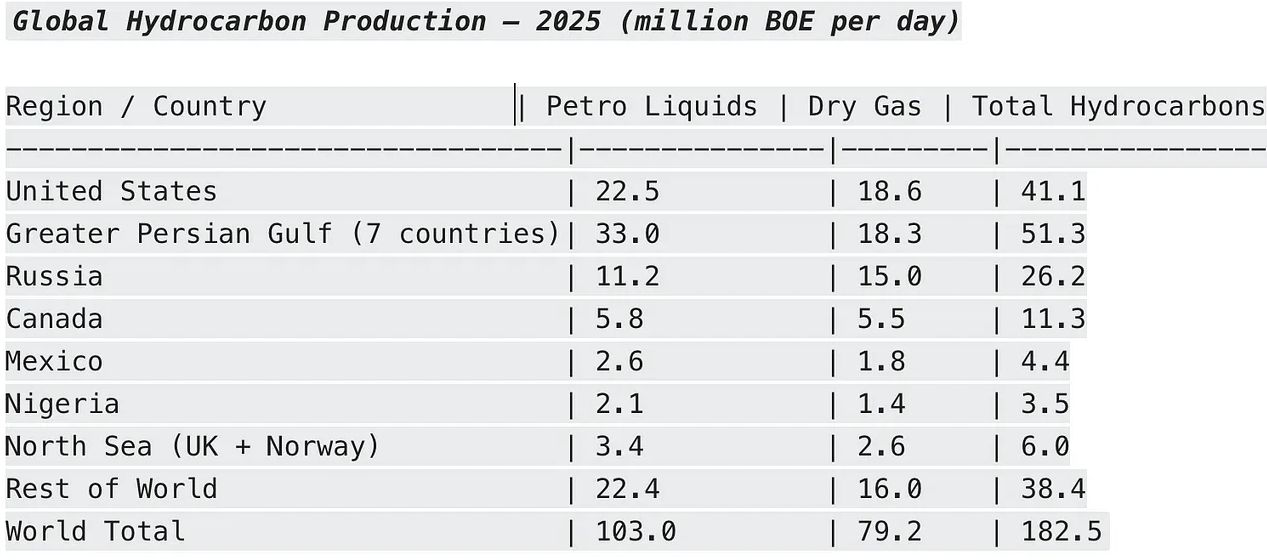

In short, the global hydrocarbon market is highly integrated and with the rise of the LNG sector and growing LNG tanker fleet has become more seamless than ever under the one price rule of markets. In this context, the US production in 2025 of 41.1 million BOEs per day of petro liquids and nat gas was nearly as large as the 51.3 million BOEs per day coming out of the Persian Gulf. ( (Saudi Arabia, Iraq, UAE, Iran, Kuwait, Qatar, and Oman).

By way of comparison, total Russian hydrocarbon production was 26.2 million BOEs or just 64% of the US output and Canada at 11.3 million BOE per day was barely 25% of the US total.

In short, when you look at the entire global oil and nat gas market at 182.5 million BOEs per day it is obvious that there are two giant hydrocarbon supply nodes – the USA and the Persian Gulf. There is no way on god’s green earth, however, that these giant hydrocarbon supply nodes could co-exist in splendid isolation.

Thus, having radically destabilized the world’s breadbasket of hydrocarbons and all their derivatives – LPGs, fertilizer, helium, sulfur and more – that Donald’s assurance that America can remain a low price oasis in a $100 +per barrel world is a barking delusion.

To the contrary, as the sign in the store used to say, if you break it, you own it. The Donald did – so now he does.

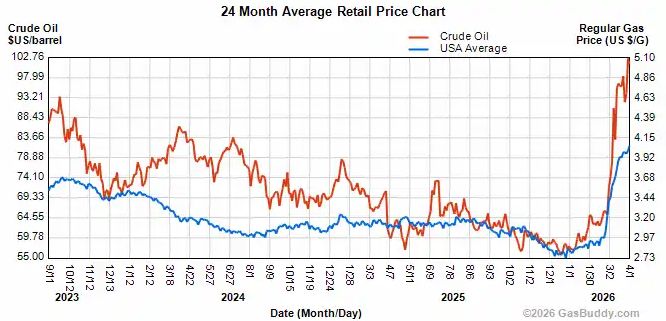

For want of doubt, here is the path of the global marker crude oil during the past 24 months versus the national average pump price of gasoline in the US. The correlation is tighter than a drum owing to the arbitrage mechanisms outlined above.

In any event, global crude oil was at $60 per barrel at the beginning of 2026 and the national average pump price stood at $2.75 per gallon, eliciting a noisy chorus of atta boys from MAGA-land.

No more. It’s a global market where pricing pressures transmit rapidly across markets and among various related elements of the hydrocarbon supply system. With global crude oil above $100 per barrel the domestic gas pump price is now at $4.03 per gallon for one reason and one reason only: The Donald kissed Bibi Netanyahu’s ass and joined his war of aggression not only against Iran but the entire Persian Gulf supply system for no good reason of America’s Homeland Security whatsoever.

David Stockman was a two-term Congressman from Michigan. He was also the Director of the Office of Management and Budget under President Ronald Reagan. After leaving the White House, Stockman had a 20-year career on Wall Street. He’s the author of three books, The Triumph of Politics: Why the Reagan Revolution Failed, The Great Deformation: The Corruption of Capitalism in America, TRUMPED! A Nation on the Brink of Ruin… And How to Bring It Back, and the recently released Great Money Bubble: Protect Yourself From The Coming Inflation Storm. He also is founder of David Stockman’s Contra Corner and David Stockman’s Bubble Finance Trader.

No comments:

Post a Comment