Global Recession Risk Spikes as World Powers Down, Markets Slump

(Bloomberg) --

A pandemic-driven global recession is becoming more likely by the day as the flow of goods, services and people face ever-increasing restrictions and financial markets slump.In just the past day or so, President Donald Trump curbed travel to the U.S. from Europe, Italy’s government ordered almost every shop to close, India suspended most visas and Ireland partially shut down. Twitter Inc. joined companies telling employees to work at home and the National Basketball Association suspended its season.

While such announcements are aimed at containing the coronavirus, each quarantined city, canceled flight, scrapped sporting event and scuppered conference will hammer demand this quarter and likely longer. An initial consumer rush to stock up on supplies may be followed by months of cautious restraint.

Investors are sounding the alarm that policy makers aren’t doing enough, with a deepening rout in global stocks and strains in credit markets compounding the concern over the economic outlook. Stocks were primed for more heavy losses in Asia on Friday after the worst Wall Street session since 1987.

The virus “has disrupted the global economy and has quickly morphed into a dislocation in financial markets too,” Morgan Stanley economists led by Chetan Ahya said in a report to clients in which they warned of a “rising risk” of a full-blown global recession.

“The need of the hour is a quick, sizeable response from public health, monetary and fiscal authorities,” they said.

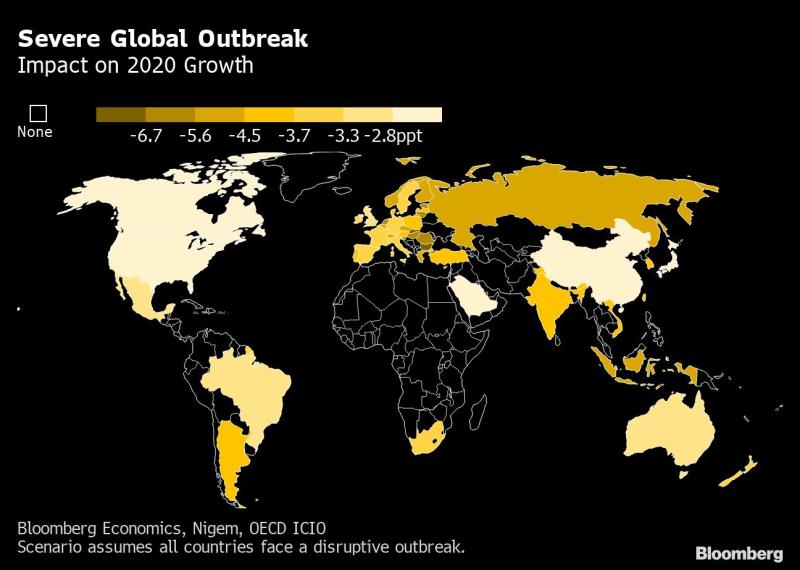

Dashed are the hopes from just a few weeks ago that the world economy would track a V-shaped trajectory -- a sharp first-quarter slump in growth followed by a second-quarter rebound. Now, the biggest economic shock since the 2008 financial crisis is raising the risk of a worldwide recession, with the debate shifting to how long and deep the slump will be.

China is already on course for what could be its first quarterly contraction in decades. In the U.S., a Bloomberg Economics model suggests a 53% chance that the 11-year expansion will end within a year. The economies of Japan, Germany, France and Italy were already shrinking or stalled before the virus outbreak, and the U.K. is wobbling amid Brexit uncertainty.

As the virus spreads, the threat grows of a phenomenon economists refer to as a feedback loop -- a vicious cycle in which a country that starts to recover domestically then suffers diminished demand from abroad as other nations succumb, prolonging the downturn.

At Pacific Investment Management Co., global chief economic adviser Joachim Fels says the U.S. and Europe face the “distinct possibility” of a recession. Former U.S. Treasury Secretary Larry Summers, a paid contributor to Bloomberg News, says the coronavirus may prove to be the most serious crisis of the century so far and puts the odds of a U.S. recession at 80%.Traditionally more conservative in calling a recession, Wall Street economists are also downgrading their forecasts. Those at Bank of America Corp. on Wednesday cut their global growth forecast for 2020 from 2.8% to 2.2%. That’s “in spitting range of a typical global recession” and well below the world’s long-term trend of 3.5%, they said.

Counterparts at JPMorgan Chase & Co. told clients this week that the risk of a global recession “has risen materially.” To revive their confidence, they said they need to see a fading of the virus, a stronger and more creative response by economic policy makers, and for firms and banks not to slash jobs or lending. They also argued that the tumble in the cost of oil may not necessarily boost growth as much as historically because consumers will pocket the windfall from cheaper fuel prices.

Policy makers are already struggling to keep up, adding to concern that falling demand won’t be cushioned enough by stimulus.

The Federal Reserve’s emergency interest rate cut of March 3 failed to buoy investor confidence, adding to pressure on its officials to ease monetary policy and perhaps even slash rates to zero when they reconvene next week if not sooner. There are also calls for it to follow the Bank of England in channeling assistance to parts of the economy in most need.

European Central Bank President Christine Lagarde got her chance to act on Thursday after telling regional leaders earlier in the week that their economy risked a shock that echoed the crisis of the last decade if they didn’t urgently. The ECB announced what it called a “ comprehensive” package that included more quantitative easing and tools to increase liquidity, but disappointed investor calls for interest rates to be cut.

No comments:

Post a Comment