Could An Energy Crunch Lead To A Worldwide Financial Crisis?

- Reduced capital investment in upstream sources for new supplies of petroleum, match the similar scenario of the 2008-9 financial crisis

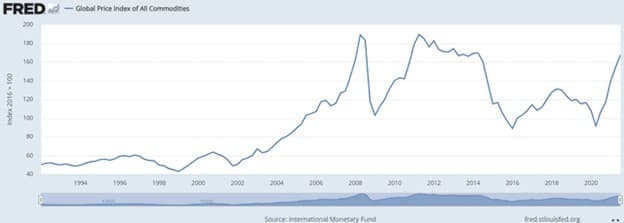

- Spending on fossil fuels has declined precipitously from 2014, reaching a bottom only last year

- The action of governments and activist shareholders to foster so-called "green energy" alternatives through edicts, tax subsidies, and regulatory barriers have discouraged upstream investment in oil and gas

- Two of the things that precipitated the financial crisis of 2008 were a leveraged asset bubble in housing and a maturing commodities super-cycle

There is a case that can be made that the present day liquidity profile and reduced capital investment in upstream sources for new supplies of petroleum, match the similar scenario of the 2008-9 financial crisis. In recent times, and partially as a result of the global pandemic, huge infusions of cash have been pumped into the market to achieve a number of objectives. Commodities began an extreme pricing upswing last year as a result of this cash infusion and pent-up demand from the shut-down phase of the pandemic. As a result, not only are there strong parallels to 2008, but current conditions are even more exaggerated as we approach 2022, thanks to continued governmental and financial intervention in the markets. In this article, we will examine some of the key causes of the 2008 financial meltdown, and compare them against relevant data in the present day. We will then tie that to current data on petroleum supplies and production to make our final case about the likelihood of a severe global financial crisis.

Lack of capital investment in upstream petroleum supplies

If you follow the news you will become quickly and acutely aware that things are different on the global energy front. Strikingly different from just a year ago. One of the things that drives the conversation is the speed at which the market has flipped from assuming that oil would be plentiful and low priced well into the future to just the inverse. There was even a catch-phrase to describe this scenario, used as recently as March of 2020-Lower For Longer.

So what happened? As you can see below spending on fossil fuels has declined precipitously from 2014, reaching a bottom only last year. Estimates vary from between $600 bn to $1.0 Trillion of capital has been lost to oil and gas extraction since 2014.

WSJ- Chart by author

Two primary reasons have been the cause of most of this capital restraint. The first is prices well below an acceptable rate of return for oil companies for much of this period. Lower for Longer carried an enormous financial impact onto the balance sheets of oil producers, and they did what oil companies do when oil prices drop. They stopped spending...on oil and gas. Even now, with prices that are much higher, domestic oil companies are choosing to pay down debt, buy back their stock, and raise dividends as opposed to increasing their capital budgets. This was discussed in detail in an OilPrice article in September.

The second principle chilling effect on global fossil fuel investment has been the action of governments and activist shareholders to foster so-called "green energy" alternatives through edicts, tax subsidies, and regulatory barriers. Following the Paris Accords, signatories have moved swiftly to reward investment in these alternative energy sources, primarily-wind, solar, and biomass. This, despite the fact that many of these alternative technologies are still evolving, and lack supporting infrastructure. We have in effect, "jumped" into the pool and then checked for water. We explored the actions by European governments in this OilPrice article.

International companies like, Shell, (NYSE:RDS.A), (NYSE:RDS.B) and BP, (NYSE:BP) are doing some of the same things, but also are diverting capital to renewable energy projects in an effort to reduce the carbon footprint of their operations. In a moment of candor and clarity, in response to an activist investor pushing the company to spin off its legacy assets, Shell CEO, Ben van Beurden said-

The needs of Shell’s customers, and the company’s efforts to pivot away from fossil fuels, were better served by keeping its range of assets and businesses. In particular, he said the company’s legacy oil-and-gas assets were needed to fund its investments in lower-carbon energy.

These companies are also scaling down their carbon-based operations, monetizing assets up and downstream. Shell in particular has led the way with their sale of their Permian assets to ConocoPhillips, (NYSE:COP). BP is considering further steps, but has not made any big moves in this regard recently. These actions will result in their portfolios becoming less carbon intensive as the alternative energies they are investing in now, come online mid-decade. Will they be as profitable? Doubts have emerged, but this is a question for a future article.

One need not worry about the financial viability of these green energy projects, over the short run at least, as there are ample government stipends in place to pay all or part of their costs. Domestically, and across the pond, governments have paved the road for a green energy transition. The market has already decided about this capital shifting as relates to these companies, bidding up their share prices by about half since the first of the year.

The problem for world energy consumption is that oil remains a fundamental driver of energy security globally and demand is running ahead forecasts with demand above 100 mm BOPD. Prices have gone higher. Much higher, and that could be problematic for the stability of the financial system if the thesis we are constructing comes into play.

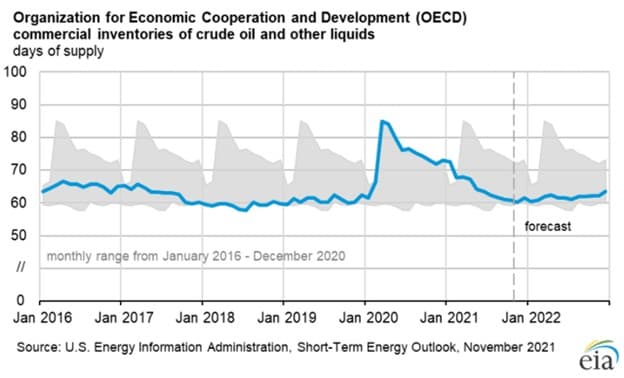

We see oil demand rebounding strongly as we come out of the global recession precipitated by the pandemic. Global growth-we add 120 mm people to the planet yearly, and pent up demand are the drivers here. It comes at the worst possible time for storage volumes, both domestically and internationally. In the U.S. we are near the bottom of 5-year averages for this time of year. 425 mm bbl may sound like a lot, but at 21.5 mm BOPD of consumption, it's less than a 20-day supply.

To no great surprise, European petroleum stocks are down at similarly low levels.

The great global liquidity influx and a commodity boom

Liquidity or lack thereof is stuff of which financial crises are made. If you hark back to 2008-the last financial crisis that wasn't related to the now winding down pandemic, an increasingly seized up financial system brought global markets to their knees as it metastasized. Liquidity in the form of massive government intervention righted the ship and by early 2009 green shoots were appearing in the market.

Two of the things that precipitated the financial crisis of 2008 were a leveraged asset bubble in housing and a maturing commodities super-cycle. Growth in commodities brought on by the Chinese economic boom led to oil topping out at nearly $150 per bbl in 2008. This boom continued to mid-2014, with oil regaining $110 bbl before succumbing to OPEC's desire to retake market share from U.S. shale producers, and lower growth in the Chinese market. Oil became plentiful as OPEC opened the taps, and prices stayed low for the next 6-years.That is one key difference from 2008 that will tend to extend and exacerbate a downturn if it occurs. Oil is not plentiful and prices are spiking.

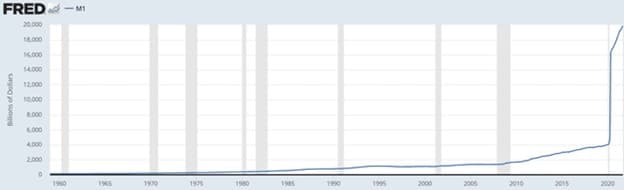

We are now seeing an asset pricing bubble on a scale never before seen. In the span of a year and a half, the money supply has increased from $4.5 trillion to nearly $20 trillion, and there is more coming. The recently passed Infrastructure Plan will bring another couple of trillion of direct and ancillary spending. The Build Back Better plan waiting in the wings for a reconciliation passage will add another $2.0 to $3.5 trillion to the Fed's balance sheet.

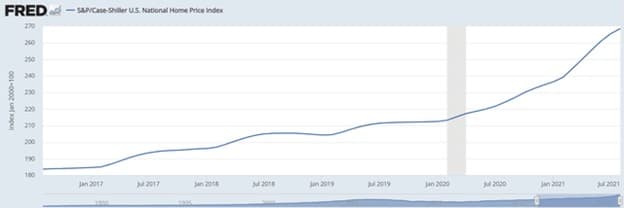

In the past 5-years the median U.S. home price has climbed 68% with much of that coming since the first of the year. Anyone who doesn't recognize the effervescence, or bubbliness in that number may have napped during Econ 101. You can argue that the world has changed since Covid rode the jet stream west, but there is no argument that house prices have not out-stripped wages of this time period.

Once again, FRED is helpful here as it reveals the median household cannot afford an entry level home at $270K. A buyer at the median level with a $25K down payment will only qualify for a $231K house.

In summary, the present situation has close parallels to the financial crisis of 2008. We think that the current situation may have consequences that are more extreme, as the amount of liquidity pumped into the system is vastly higher. Further, the stockpiles of energy are much lower than in the 2008 time frame, thanks in some measure to the diversion of capital toward renewables, the restraint of capital due to low prices, government intervention, and a rebounding element of demand.

Climate policy will directly impact economic growth

We are already beginning to see the second-order effects of the climate policies being adopted in the wake of the Paris Accords and its offspring the COP-26 love fest in Glasgow this year. I am referring, of course to the energy crisis in the UK, brought on by unanticipated underperformance of wind farms, and under-investment and early retirement of petroleum energy sources, over the last few years. This has all been pretty well documented, and I am not going to belabor them further now.

One of the things that astounds me about the green energy movement is the number of unasked, or unanswered questions related to its full spectrum adoption. Assumptions have been blithely put forward as fact with no supporting evidence. In fact, if you do ask questions you are labeled a "climate denier," and ignored or canceled.

So what is one assumption that seems to have not been entirely thought through? Let's start with the plan for wind power to provide up to 40% primary electricity generation by 2030, now codified virtually around the world in tax and carbon policy. I ran across a calculation by William Lacey on another site that was quite revelatory. I am paraphrasing his work on that site here in the next couple of paragraphs.

Can this really be done? A study promulgated by Arcelor Mittal, the world's leading steel producer is revealing.

“Steel will play an important role in all renewables, including and especially solar and wind. Each new MW of solar power requires between 35 to 45 tons of steel, and each new MW of wind power requires 120 to 180 tons of steel.”

According to the OECD the global capacity to make steel rests at about 2.5 mm metric tons. If we are going to replace the electricity supplied by fossil fuels, about 131 billion MWH, we would need to generate another 6 bn tons of steel. Or about 2.5X the annual present capacity of the global industry. Are we really going to divert 100% of the steelmaking capacity of the planet to building wind farms for 2.5 years? What about copper? What about other metals used in EV battery production. These are profound questions that just don't get asked.

After Lacey

In summary, I think the unasked questions will begin to be asked at some point. Will it be when some entity wants to build a car plant, and is told, "Sorry we don't have the power generating capacity." It is going to happen. It is "baked" into this cake from the under-investment in fossil fuels.

Your takeaway

I said at the beginning there is a reasonable case that a financial crisis could result from the lack of upstream investment we have discussed so far, and the continuing bashing of the industry that is vital to maintaining our standards of living. As I've noted and world events are beginning to reveal, the hour is very late in terms of being able to respond to a prolonged price spike, or physical shortage of oil. A renewed will accompanied by some acknowledgement of just how vital oil and gas are to our energy security might shorten the effects that could possibly emerge from a financial crisis. But, that is not the trend presently.

Even today, when the ink is barely dry on the Infrastructure bill, our political leaders are sending mixed messages as fuel prices spike. In an even more ironic dichotomy of thought, Middle-East producers are being asked to pump more to ease global energy prices. A request...plea, that they not so politely rejected in their recent meeting. At the same time, U.S. domestic producers are being hamstrung with enhanced regulations, reduced permitting, threats of a carbon tax on fuels, and being starved of capital by key nominees. You can't make this stuff up.

Even the hedge fund Green Energy zeitgeist, Larry Fink of Blackrock is back-peddling a bit on his dire pronouncements, and now acknowledges that-shock-horror, we are totally dependent on oil and gas. As an oily, it’s kind of fun to see Larry squirm a bit.

In summary, I am not predicting a financial crisis. I am saying there are strong parallels today to a recent past crisis, and that if one occurs tightness of the energy supply from lack of upstream investment could play a role in its depth and duration.

By David Messler for Oilprice.com

No comments:

Post a Comment