It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Wednesday, July 27, 2022

Platts to launch first carbon-accounted tanker assessments as shipping faces EU emission trading system coverage

July 27, 2022

Tsuneishi

S&P Global Commodity Insights has announced it will launch daily Platts price assessments for freight emissions under the European Union’s Emissions Trading System (ETS). The new assessments will show the cost of carbon dioxide emissions from fuel combustion to transport crude or fuel oil on an aframax tanker via an initial four European shipping routes, beginning August 1.

“As efforts to decarbonise the shipping sector continue, pricing transparency is crucial for the industry to act effectively,” said Peter Norfolk, editorial director, global shipping and freight at S&P Global Commodity Insights. “The effect of the EU ETS on the shipping industry will be profound, and will be followed by more such measures as the industry faces up to the challenge of energy transition.”

The new assessments build on the suite of freight carbon intensity values and freight carbon intensity premiums Platts began publishing in October 2021. Those earlier carbon intensity assessments show the volume of greenhouse gas emissions generated through transporting various crude grades from production storage terminals to typical refinery locations around the world, as well as the cost of offsetting those emissions using carbon credits on a per barrel of crude basis.

The new carbon-accounted aframax freight assessments show the cost of EU Emissions Allowances (EUAs) that would be required to comply with the EU ETS for some of the key tanker routes supplying Europe, and will be published in Worldscale points and in US dollars per ton.

Last July, the European Commission proposed adding shipping to the EU Emissions Trading System from 2023, with obligations phased in gradually between 2023-2026, requiring shipowners to hold EUAs covering all their emissions on routes and at ports inside the EU, and 50% of their emissions from third-country voyages beginning and ending in the EU. The European Parliament voted June 22 to push for a faster implementation, including 100% of emissions from intra-European Economic Area (EEA) from 2024, 50% of extra-EEA routes between 2024-2027, and 100% thereafter.

For its new assessments, Platts is employing baseline market norms for vessel speed and bunker fuel consumption, verified by extensive market surveys. The calculations will use Platts daily EU Emission Allowance Nearest-December price (EADLP00). The tank-to-wake carbon emissions based on the fuel consumption will be calculated using the carbon conversion factors published in Annex 1 of Regulation (EU) 2015/757 of the European Parliament and of the Council on the monitoring, reporting and verification of carbon dioxide emissions from maritime transport.

Mexico highlighted as potential zero emission fuels hub for shipping

July 28, 2022

Mexico has the potential to establish itself as a global leader in maritime decarbonisation by engaging in green fuel production and bunkering with swift and strategic action, according to a new report by P4G Getting to Zero Coalition.

Being placed between well-established shipping routes and trade relations to multiple continents in the Pacific and Atlantic Oceans, the report found Mexico could tap into new markets and by investing it itself, the country could create new revenue streams from scalable zero emission fuels (SZEF) exports and bunkering, establish green hubs and ports, as well as open possibilities for green corridors along key shipping routes.

“The massive demand for zero emission fuels that will arise constitutes a major growth opportunity for Mexico, having the chance to become a future powerhouse for international shipping in Latin America,” said Ingrid Sidenvall Jegou, project director at the Global Maritime Forum.

According to the report, the development of green fuel infrastructure to serve Mexico’s shipping sector could attract investments ranging from $1.9bn to $2.7bn in onshore infrastructure by 2030. It discovered three key opportunities for Mexico, including the port of Manzanillo, DH2 Energy activities in Central Mexico, and Baja California, all of which are said to benefit from SZEF production, offtake, and distribution.

A facilitative policy and financial framework capable of effectively motivating and convening key actors across sectors and value chains is critical to unlocking these opportunities. The 111-page analysis stressed that the country currently lacks a favorable ecosystem, both politically and economically, to leverage benefits from SZEF production and use, particularly given the current administration’s preference to continue exploiting the country’s fossil fuel resources.

The report suggested that with appropriate incentives and targeted action towards encouraging investments into renewable energy and fuel production, Mexico could gain a competitive advantage in the bunkering and export of fuels in Latin America as other countries in the region take steps to prepare their own bunker supply chains.

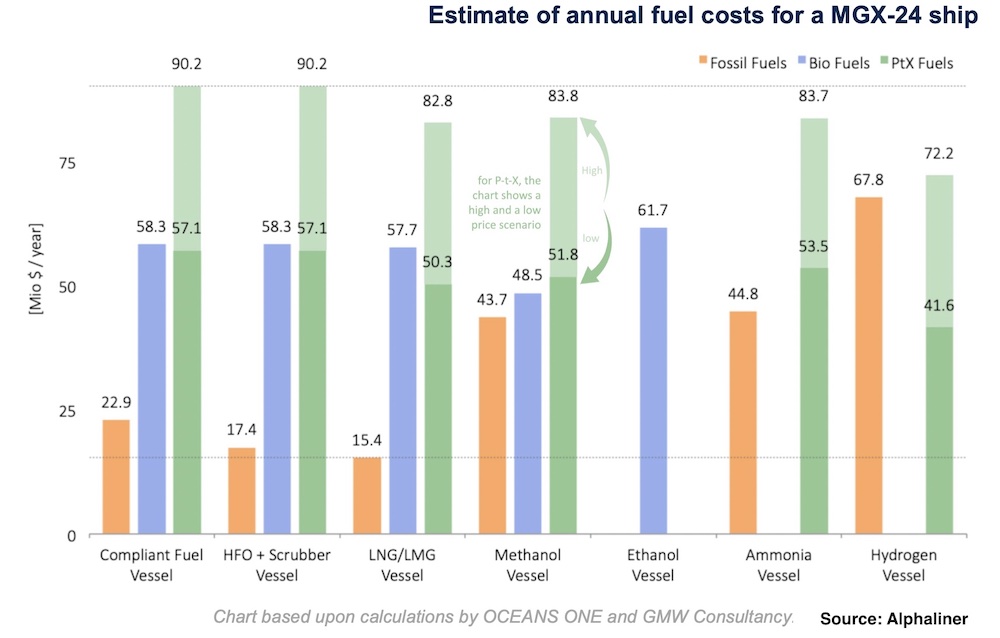

Liners get a preview of alternative fuel costs

July 27, 2022

Two German consultancies have collaborated to pen a detailed report on expected bunker costs for the largest boxships afloat, the 24,000 teu so called megamaxes. The study has since been analysed by liner experts at Alphaliner who warn of the significantly elevated fuel bills shipping will face once alternative forms of energy are adopted.

The joint study by OCEANS ONE and GMW Consultancy finds that bunker costs for alternative fuels will be significantly higher with biofuels, for instance, predicted to be at least a factor of 2.5, but most likely a factor of four times higher than in the past.

The technical and commercial comparison provides a clear insight into the impact of different fuel options on capex, open, slot costs and total costs of ownership for operating a megamax and key pricing considerations for the different fuels are neatly encapsulated in the chart below.

Investment costs will no longer be as important as the availability and prices of the appropriate fuel

“Considering that in the past bunker costs represented about one third of slot costs per loaded container, it is clear that in the future fuel costs will be a main driver for transporting containers around the world,” Alphaliner stated in its most recent weekly report, having studied the German report.

Alphaliner argued investment costs will no longer be as important as the availability and prices of the appropriate fuel.

“Vertical integration, cooperation and joint development projects for fuel supply will be solutions for a viable decarbonization strategy and will decide the future success of shipowners,” Alphaliner suggested.

No comments:

Post a Comment