It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Wednesday, October 22, 2025

Concerned carmakers race to beat China’s rare earths deadline

Global automakers are scouring the globe for crucial rare earths ahead of looming Chinese export controls, with executives worried they could lead to parts shortages and plant closures.

Rare earth magnets power motors in car parts such as side mirrors, speakers, oil pumps, windshield wipers and fuel leakage and braking sensors. They play an even bigger role in EVs.

While a US-China deal diverted a supply threat, stockpiles were depleted by similar restrictions earlier this year, while Beijing has also made it harder to get export licenses.

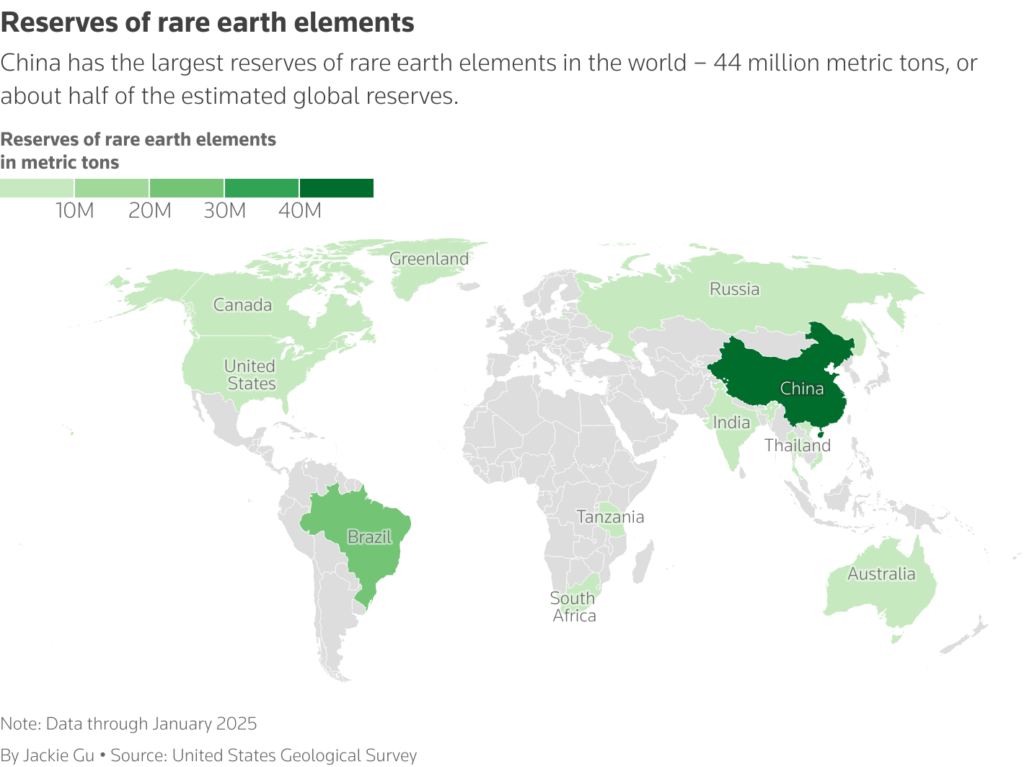

Consultancy AlixPartners estimates China controls up to 70% of global rare earths mining, 85% of refining capacity and about 90% of rare earths metal alloy and magnet production.

The new Chinese export control list includes elements like ytterbium, holmium and europium, also used in making cars.

“The situation is very tense,” said Nadine Rajner, CEO of German metal-powder supplier NMD, adding customers want to source rare earths from anywhere but China.

As part of efforts to counter Chinese dominance, on Monday President Donald Trump and Australian Prime Minister Anthony signed a critical minerals agreement that includes US investments in rare earth mining projects in Australia.

NMD’s Rajner said that while there are plenty of rare earths available in countries like Sweden, they do not have the mines or refining capacity to make them usable. And for heavy rare earths, China controls 99.8% of global refining capacity, making alternative sources negligible.

“We are pretty much sold out and have limited stocks,” Rajner said.

Rare earths can be recycled from old cars, but that industry is in its infancy. Neutral, a Renault-backed company, currently recycles rare earths from 400,000 cars a year in France and has contracts with 15 brands in Europe.

But “the challenge is scaling up these activities,” said Neutral CEO Jean-Philippe Bahuaud.

‘Already been depleted’

Even if Chinese suppliers can fulfil fresh orders before the November 8 export controls take effect, the journey by sea to Europe can take 45 days and the threat of a rare earth bottleneck is among several headaches facing the auto industry.

China has also placed export restrictions on lithium-ion batteries and battery materials, triggering concerns over parts supplies for electric vehicles.

And last week, an intellectual-property dispute between China and the Netherlands involving little-known Dutch chip-maker Nexperia, sparked fears of factory closures because it supplies a large amount of chips car parts and components.

Automakers also face the challenge of US tariffs and are expected to detail the costs in their third-quarter earnings.

But China’s hold over the industry through its control of rare earths ranks among the thorniest problems.

“They can shut us down in two months, the entire auto industry,” said Ryan Grimm, Toyota Motor’s North America group vice president of purchasing supplier development.

Bruno Gahery, president for France, Benelux, West and South Europe at supplier Bosch, said he expected the autos industry to “overstock rare earths” ahead of the deadline.

But an executive at a magnet supplier for Hyundai said that while it built inventories earlier this year, “most have already been depleted” and supplies are tight.

Some Chinese rare earths exporters received a rush of orders from overseas clients immediately after new export controls were announced on October 9, three industry sources told Reuters.

Rare earth-free motors

Automakers are taking steps to reduce their reliance.

Some such as General Motors and major suppliers such as ZF and BorgWarner are developing EV motors with low-to-zero rare earth content, while BMW and Renault have produced rare earth-free motors.

Monumo has used AI and deep-tech simulation to help clients cut rare earth content in motors already in production, which CEO Dominic Vergine said has led to an average reduction of 24% among the UK firm’s customers, which include several of the world’s top 10 carmakers, he said.

Automakers are also pushing hard to improve rare earth-free motors for the next generation of EVs.

Yet most of those motors are years away, as are efforts to develop new rare earth mines and processing plants outside China, which Beijing can undermine by keeping prices low, industry experts say.

Experts say the US government is taking the threat far more seriously than Europe.

Andy Leyland, co-founder of supply chain specialist SC Insights, said Beijing has focused on beating others on price and will continue to do so.

“The Chinese can always undercut them,” he said of efforts to develop rare earth-free motors, adding that faced with cheaper motors with rare earth magnets automakers may find it hard to justify more expensive components.

“So it’s a really risky investment.”

Meanwhile, China is expected to keep exerting its power over supplies of rare earths.

“This is not the end of export controls,” said Jan Giese, a senior manager at rare earth trader Tradium.

(By Nick Carey, Christina Amann, Gilles Guillaume, Heekyong Yang and Beijing Newsroom; Editing by Mike Colias and Alexander Smith)

America’s Auto Industry Faces a Rare Earth Reckoning

U.S. automakers remain heavily dependent on Chinese rare earths, making production vulnerable to export restrictions.

Companies like GM and Ford are investing in domestic mining and recycling to secure lithium, cobalt, and nickel supplies.

Despite ongoing shortages, new trade deals and domestic metal facilities offer cautious optimism for the auto sector’s resilience.

The Automotive MMI (Monthly Metals Index) moved sideways, rising a slight 1.39%. As a whole, the US automotive market is facing a number of challenges necessitating both innovation and resilience.

Why Are Critical EV Minerals in Short Supply?

Automakers are grappling with shortages of critical minerals needed for electric vehicles and high-tech components. Rare earth minerals are a prime example. This set of 17 metallic elements is integral to many car parts, from EV motors and batteries to windshield wipers and speakers.

CBS News reports that about 90%of the rare earths used by the US industry are sourced from China. This leaves the US automotive market highly dependent on foreign supply. In May, 2025, Ford Motor Co. had to temporarily halt production at its Chicago SUV plant due to a sudden shortage of rare earth magnets needed for electric power steering and other components.

Chinese Control Over Rare Earths Remains a Key Problem

Because China dominates the global rare earth supply chain, even a brief disruption can have a significant impact on the US automotive market. China also refines nearly 99% of the world’s heavy rare earth elements, resulting in a near-monopoly where any Chinese export curbs immediately ripple through manufacturing.

According to EHN, US automakers recently warned that vehicle assembly could grind to a halt within weeks if rare earth shipments didn’t resume. The crisis prompted urgent trade talks. But as of October 2025, China announced even stricter rules, ultimately tying rare earth magnet exports to national security considerations.

The lesson for US firms is clear: supply lines for critical EV minerals are vulnerable, and over-reliance on one country presents a significant strategic risk.

What Strategies Are Automakers Using to Secure Materials?

Facing the twin challenges of rising costs and scarce materials, US automakers are adopting new supply chain strategies to bolster resilience. Diversifying sourcing is priority number one, and manufacturers are seeking alternative suppliers for minerals outside of both China and traditional metal import channels. In some cases, companies are stockpiling critical parts and materials as a buffer.

For instance, German automakers like BMW and Mercedes-Benz reportedly entered 2025 with plans to build inventories of rare earth magnets and other key components when China’s restrictions hit. This kind of inventory hedging can keep production running through short-term disruptions.

Will the US Automotive Market and Car Makers Strike Lithium Gold in Nevada?

Automakers are also taking a more hands-on approach to raw material supply. A notable example is General Motors’ investment of around $650 million in a Nevada lithium mine (Thacker Pass) to secure a domestic source of lithium for EV batteries.

Other carmakers have signed long-term contracts with US and Australian mining firms for lithium, nickel and cobalt, all to ensure critical battery minerals remain available even if overseas supply chains falter.

Another strategy that is proving key for the US automotive market is recycling and circular reuse of metals. Recycling not only reduces dependence on mined imports but also aligns with sustainability goals. Therefore, manufacturers across the US are partnering with specialized firms to reclaim materials from scrap and end-of-life batteries. For example, Ford recently invested $50 million in Redwood Materials, a Nevada-based company, to integrate battery recycling into its supply chain.

By recycling old lithium-ion batteries, Redwood can provide Ford with a domestic stream of lithium, cobalt and nickel for new EV batteries. Companies like GM are also working with recyclers to harvest scrap from battery production for reuse.

What’s the Outlook for US Metal Procurement in Auto Manufacturing?

In the short term, volatility is the new normal. U.S. automotive procurement executives must continue to navigate unpredictable swings in both policy and supply. Tariffs can change with geopolitical winds, as exemplified by mid-2025’s rapid escalations and subsequent trade truces. Meanwhile, the critical mineral supply can be suddenly pinched by export controls abroad. This type of environment calls for a combination of vigilance and flexibility.

For instance, many firms are strengthening their risk management by locking in fixed-price contracts for steel and aluminum where possible, while closely monitoring inventories of at-risk materials. Building resilience is the name of the game, and dual sourcing, strategic stockpiles, vertical integration and recycling are becoming standard tools in the procurement playbook.

Not All Bad News

On a hopeful note, ongoing negotiations and investments may alleviate some pressures. The US and EU recently implemented a trade agreement that lowers certain auto-related tariffs and even exempts some raw materials like rare earths and graphite from duties.

Meanwhile, domestic capacity is inching upward. For example, new aluminum recycling facilities and steel mini-mills are coming online, and the Mountain Pass rare earth mine in California is increasing output. That said, the facility still ships its ore to China for processing, at least for now.

Ultimately, CFOs and sourcing leaders in the US automotive market are balancing a tough equation. To keep assembly lines running and costs manageable tomorrow, they must invest in supply chain resilience today.

Automotive MMI: Noteworthy Price Shifts

Hot-dipped galvanized steel prices dropped 3.44% to $1,009 per short ton.

Korean 5052 aluminum coil premium over 1050 prices moved sideways, dropping 2.19% to $4.09 per kilogram.

Chinese lead prices moved sideways, rising just 0.59% to $2,359.32 per metric ton.

Lastly, LME primary three-month copper prices rose by 5.54% to $10,332 per metric ton.

An auto supplier that manufactures electrified propulsion systems, among others, has closed a factory in Detroit because of the drop in demand for electric vehicles.

In a statement cited by CBS, Dana Inc. said that the closure decision was the result of an “unexpected and immediate reduction in customer orders driven by lower demand for electric vehicles, which has rendered continued operations at the plant no longer viable.” Some 200 workers at the plant will be laid off.

The Dana facility may be the first of many casualties of the change in federal policies towards electric vehicles. Fully supported by the previous administration, with billions in subsidies for both buyers and manufacturers, the sector fell out of grace this year with the change of the guard at the White House, with the Trump administration axing the buyer incentive for electric cars as of the end of September.

The move prompted a rush to buy EVs in the third quarter, leading to a whopping 40.7% jump in EV sales on the second quarter, which saw a dip, by the way. The third-quarter sales number also represented a solid 29.6% annual increase.

This was the last hurrah, it seems, at least for the time being, as large carmakers continue losing money on their EVs and would likely breathe a sigh of relief at the opportunity to let go f their electrification ambitions in the absence of subsidies.

Ford lost $1.3 billion on its EVs in the second quarter and has projected its total EV-related losses could hit $5.5 billion for the full year.

GM and Stellantis are also losing money on every EV they make, even though, per the latest Kelley Blue Book numbers, GM, along with Volkswagen, enjoyed a more than twofold increase in EV sales in the third quarter.

By Irina Slav for Oilprice.com

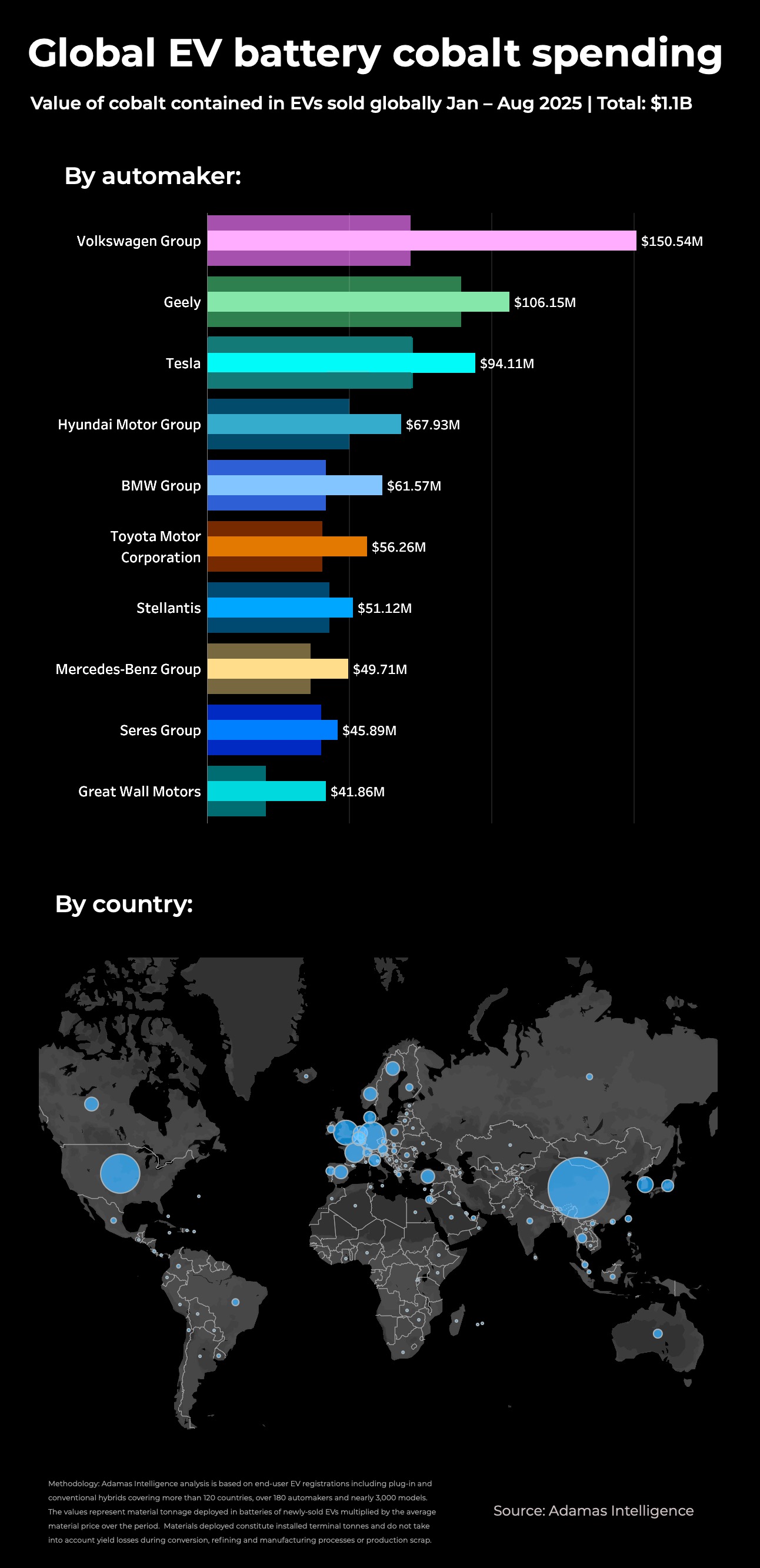

RANKED: Top 10 automakers by battery cobalt spending

Congo’s export quotas have lit a fire under cobalt prices and spending on the battery material is up 43% year on year despite ongoing thrifting.

A surge in supply from the Congo, responsible for 80% of the world’s cobalt output, coupled with cooling demand from the electric vehicle market, saw cobalt prices sink to historic lows at the start of 2025.

Copper production in the DRC increased by nearly 40% last year, but last week Kinshasa began implementing a quota system to replace a ban announced in February. Allowed base volumes of 87,000 tonnes per year is around half the total exports registered in 2024.

The price of cobalt sulphate entering the EV battery supply chain in China is now trading over 120% higher than at the start of the year – averaging $7,775 a tonne in September (still nowhere near the 2022 peak of $19,000 per tonne).

Tender cancelled

Cobalt prices would likely remain elevated and could rise further under the quota scheme put in place for 2026 and 2027. That would have played a part in the US Department of War cancelling a $500 million tender to stockpile the metal.

The CEO of the world’s number one producer of cobalt, China’s CMOC Group, also warned last week that cobalt at these levels could lead to demand destruction and substitution, although that has been a long-running trend for cobalt users.

Cobalt consumption in EV batteries overtook other sources of demand like aerospace several years ago and the downstream impact of the DRC strategy has been swift.

The latest data from Toronto-based research consultants Adamas Intelligence tracking global EV battery metal deployment paired with monthly prices shows the size of the battery cobalt market in September totalled an estimated $227.7 million. That’s the highest value since December 2022, and up just shy of 111% year on year and 32% month on month.

So far this year the value of installed cobalt tonnes in EV batteries totals $1.3 billion, up 51% compared to the same period last year. The sales weighted average value of the cobalt contained in EV batteries has hit $73 per vehicle, up from less than $40 at the start of the year.

Keeping in mind that the installed tonnage does not take into account any losses during processing, chemical conversion or battery production scrap (often well into double digit percentages), so required tonnes and revenues are meaningfully higher at the mine mouth.

Thrifting

The turnaround in fortunes comes despite years-long thrifting by EV battery manufacturers and the rise of LFP, or lithium iron phosphate batteries. Models fitted with LFP batteries now make up more than 40% of global EV sales, even when including conventional hybrids where nickel metal hydride power packs dominate. Excluding HEVs, the number of EVs sold this year without nickel, cobalt or manganese rises to 55%.

The top 10 includes only three Chinese brands, an indication of LFP’s grip on the world’s largest EV market by a country mile.

The top automaker based on cobalt spending is Volkswagen at $150.5 million. Volkswagen, and its many brands, including Audi, Skoda, Cupra and Porsche, is having a bumper year with full electric and plug-in hybrid sales up 45% year on year for the first eight months of 2025. In turn Wolfsburg’s spending on cobalt is up more than 110%.

That it tops the charts on cobalt spending is an indication of its heavy reliance on NCM (nickel-cobalt-manganese) battery chemistries compared to rivals.

Number two Geely, which owns, among others, the Volvo and Polestar brands, spent $106.2 million over the first eight months of the year, a 19% jump, while Tesla’s spending increased by 31% year over year to $94.1 million.

Tesla first introduced LFP batteries into its line-up in 2020 and now 44% of Tesla battery packs hitting roads for the first time this year sport this cathode. That helps explain why the automaker sits at number three for cobalt while consistently topping the charts for overall battery metal consumption.

Lord of LFP

Other notable spenders include BMW Group (up 47% to $61.6 million) and rival Mercedes-Benz at $49.7 million, a 37% jump compared to last year. LFP is absent from both the German luxury brands’ EV portfolio.

NCM is still the preferred battery for higher end and sporty models, but LFP has been eating into NCM’s market share in these segments too, with BMW introducing the technology in its upcoming Neue Klasse EVs scheduled to go on sale next year.

Conspicuous by its absence is BYD, the world’s number one EV maker. The Shenzhen-based company switched to an all-LFP model line-up when it introduced its Blade battery packs in 2020, giving it an edge over rivals in the cutthroat market in China and its expanding tireprint in the rest of the world. With lithium prices also showing signs of life, BYD’s cost advantage will erode over the coming months.

For a fuller analysis of the EV battery metals market check out the The Northern Miner print and digital editions.* Frik Els is Editor at Large for MINING.COM and Head of Adamas Inside, providing news and analysis based on Adamas Intelligence data.

No comments:

Post a Comment