It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Tuesday, June 09, 2026

AU

Ex-CIA agent created fake spy program to amass $40M gold stash: reports

A former CIA official who was caught hoarding $40 million worth of gold bars allegedly created a “fake” classified intelligence program that US federal investigators say was used to channel government funds for personal gain, according to media reports.

David J. Rush, the former CIA employee, was arrested last month and charged with theft of public funds after FBI agents discovered 303 gold bars valued at roughly $40 million, along with about $2 million in cash and dozens of luxury watches, stashed in his Virginia home.

The search was conducted after the CIA became suspicious of his past military history, including his claim of being part of the Navy Reserve, and tipped the Bureau to act. Before his arrest on May 19, Rush had reportedly worked as a CIA officer for 17 years.

The Washington Post, citing US officials with knowledge of Rush’s investigations, reveals that Rush had created a fraudulent operation dubbed as the “special access program” into which he used to convince another agent to transfer the money. TheNew York Timesalso reported the findings.

‘Made-up contract’

According to both publications, Rush allegedly brought at least two CIA colleagues on the fraudulent operation and persuaded one of them to transfer the cash and gold into the program. To convince them, he claimed the money was to keep the government running in the event of a catastrophic event, such as destructive weather or a military attack, the reports said.

“He made up a contract,” one of the officials told The Washington Post.

However, it was not clear how the ex-CIA officer was able to create the program and obtain the funds without involving superiors in the agency.

According to court documents released following his arrest, Rush had received “a significant quantity of foreign currency and tens of millions of dollars in gold bars for work-related expenses” between November 2025 and March 2026. When conducting an internal review, the CIA could not locate these funds, it said in the document.

In response to the charges, Rush’s attorney, Jessica Carmichael, argued that many of the government’s allegations remain unproven, and some are unrelated to the charge currently before the court. For instance, the discovery of gold bars was “basically a non-issue”, Carmichael told reporters, stating that his client never claimed ownership of the bullion.

“This is about $65,000 worth of time card fraud,” she said.

Following a detention hearing last week, Rush was ordered to remain in jail until his trial, as a US District Court ruled him to be a flight risk.

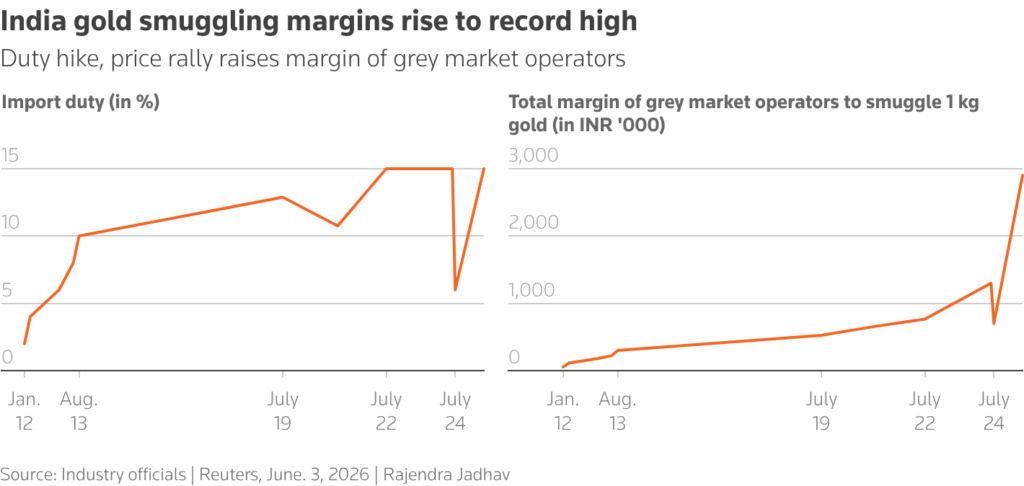

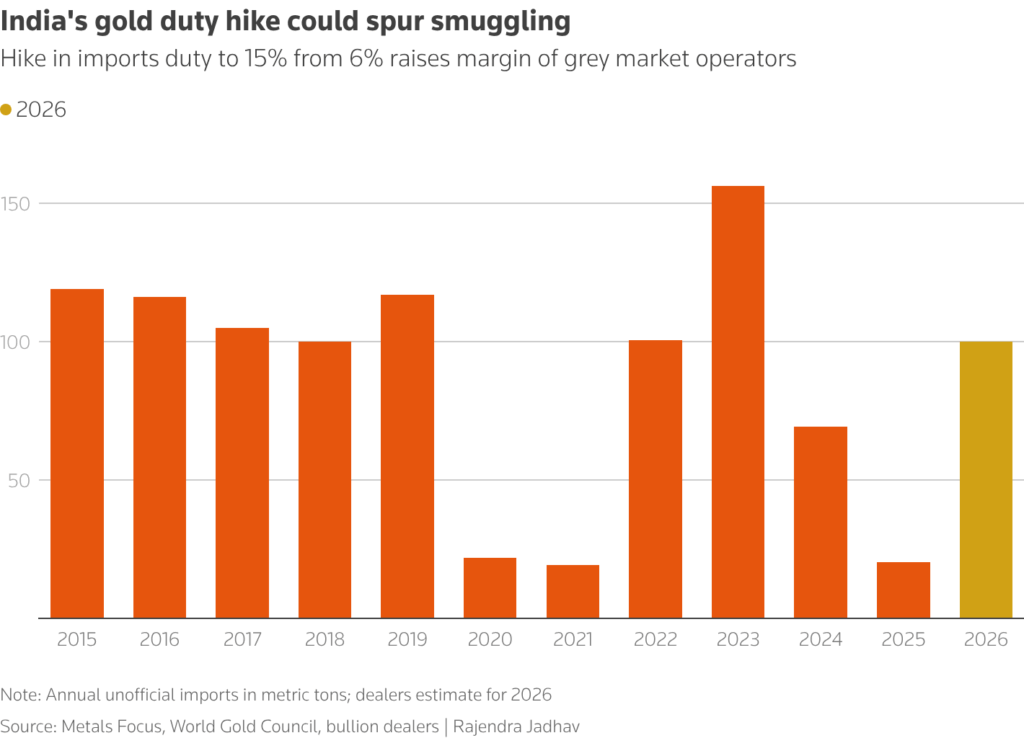

India’s sharp increase in gold import tariffs is fuelling a resurgence in smuggling that could exceed 100 metric tons this year, as soaring grey market margins allow smugglers to undercut banks and refiners of the precious metal, industry officials and bullion dealers said.

India, the world’s biggest gold market after China, more than doubled import tariffs to 15% in May to curb demand, cut the trade deficit and ease pressure on the rupee. But the move has created an opportunity for smugglers who are able to offer prices legitimate importers cannot match, they said.

The grey market discount has gone beyond $200 per ounce, or more than 4%, said a Mumbai-based bullion division head at a private gold importing bank, adding that banks were unable to offer even a $10 discount, let alone one of three digits. He declined to be named because he was not authorized to speak to media.

The recent resurgence in the grey market suggests illegal imports could exceed 100 tons in 2026, said another dealer who also declined to be identified because he was not authorized to speak to the media.

Four other dealers interviewed by Reuters shared the view that illegal gold imports could exceed 100 tons in 2026.

At current prices, 100 tons of gold would be worth about $14.35 billion, implying roughly $2.65 billion in lost tariffs and sales tax.

Smugglers can offer steep discounts because they do not pay taxes on gold, including import tariffs and goods and services tax that total 18.45%, the bullion dealers said.

“There’s a margin of more than 2.5 million rupees ($26,121.25) on bringing in a one-kilo bar, which is roughly the size of an iPhone. It is natural that people will try to make quick bucks,” the second dealer said.

“Even if grey-market operators sell at a 4% discount, they are still making a killing,” said a Kolkata-based bullion dealer.

Smuggling tarnishes legal market

Gold smuggling fell from 156.1 tons in 2023 to 69.2 metric tons the following year, and declined further in 2025 to 20.4 tons after India cut import duties on gold.

Before the duty cut, an average of 108 metric tons of the precious metal was smuggled into the country each year over the previous decade, according to data compiled by the World Gold Council.

India imported 45.6 tons of gold in April, but imports may have halved in May as banks and refiners scaled back overseas purchases amid deep discounts, said a Hyderabad-based bullion dealer.

Hefty discounts in the grey market have disrupted legal trade, pushing domestic discounts on legal gold to more than $100 an ounce as stocks imported before the duty hike are sold at steep discounts, making refining uneconomical, said James Jose, managing director of refiner CGR Metalloys.

New Delhi levies a 0.65% lower import duty on gold dore, a semi-pure alloy, than on refined gold, but the alloy has also been affected by the tariff change.

“Gold refiners typically operate on margins of around 0.65%. With discounts now well above that level, refiners have little incentive to import dore,” Jose said.

(By Rajendra Jadhav; Editing by Mayank Bhardwaj and Kate Mayberry)

Debt cycle points to stronger case for gold price: Sprott

Gold’s long-term bull market is increasingly being driven by a force larger than inflation, interest rates or geopolitical tensions: the world’s growing debt burden.

That is the central thesis of Sprott’s latest market outlook, which argues that investors are witnessing the later stages of a decades-long debt cycle in which rising government borrowing, persistent deficits and mounting interest costs are beginning to undermine confidence in sovereign debt markets.

As governments accumulate liabilities faster than economies can grow, policymakers face difficult choices between fiscal austerity, higher inflation, financial repression or some form of debt monetization, the asset manager said.

In such an environment, gold’s role changes, as the report highlights. Rather than simply serving as an inflation hedge, the metal becomes a store of value independent of governments and financial systems.

Sprott argues that the world is moving toward a regime where preserving purchasing power matters more than generating yield, creating a favorable backdrop for gold over the long term.

Central banks are voting with their reserves

According to Sprott, one of the strongest signals supporting gold comes from central banks themselves.

Official sector purchases reached 244 tonnes during the first quarter of 2026, extending a buying trend that has persisted for several years. At the same time, some countries have reduced holdings of US Treasuries and other sovereign debt instruments to raise liquidity during periods of market stress.

Sprott highlights Turkey’s recent actions as an example. Faced with rising energy-import costs, the country liquidated most of its Treasury holdings while largely retaining gold reserves through swap transactions rather than outright sales. The distinction is significant. Treasuries were treated as transactional assets that could be sold when cash was needed, while gold remained core collateral.

The broader trend suggests central banks increasingly view gold not as a speculative asset but as a strategic reserve. Amid growing geopolitical tensions, sanctions risks and concerns about long-term currency stability, gold offers something sovereign bonds cannot: an asset with no counterparty risk.

This sustained central-bank demand has also helped establish a durable floor beneath the gold market, with purchases often accelerating during periods of price weakness.

Bond markets are flashing warning signs

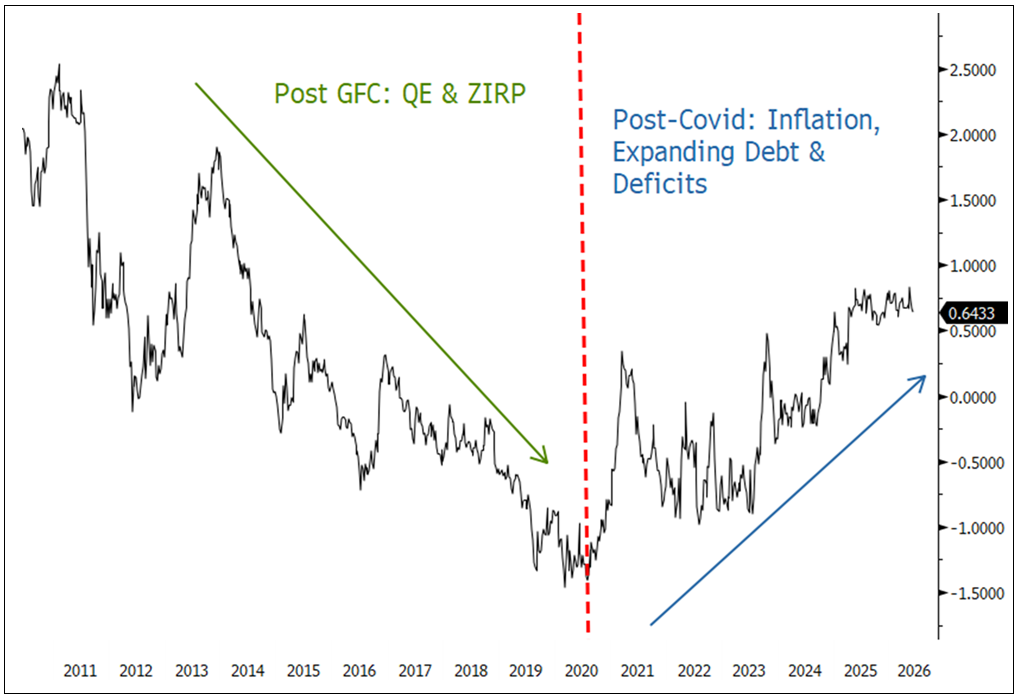

The report argues that the most important development in global markets is occurring not in gold but in government bonds.

Across major economies, yields have climbed sharply despite efforts by central banks to ease monetary conditions. In the United States, long-term Treasury yields have risen to levels not seen since before the global financial crisis, while similar moves have occurred across Europe, Japan and other developed markets.

Traditionally, lower policy rates helped pull bond yields down. That relationship is beginning to weaken. Investors are increasingly demanding higher compensation for inflation uncertainty, growing debt issuance and concerns about fiscal sustainability.

U.S. 10-year Treasury term premium, weekly. Source: Sprott

The US illustrates the challenge. Federal debt has climbed to roughly 120% of GDP, while annual deficits remain near 5% of GDP and are projected to increase further. Interest payments on the debt are approaching $1 trillion annually and continue to rise as governments refinance obligations at higher rates.

According to Sprott, investors are beginning to focus less on central-bank policy and more on the long-term ability of governments to manage debt loads. The result is rising term premiums, higher borrowing costs and growing questions about the future role of sovereign bonds as safe-haven assets. As confidence in debt-backed assets weakens, demand for hard assets such as gold tends to strengthen.

Gold’s structural bull case remains intact

While gold faces short-term headwinds from rising yields and periodic liquidity pressures, Sprott believes the larger forces supporting the metal remain firmly in place.

The report describes an emerging environment characterized by fiscal dominance, where governments become increasingly constrained by debt levels and rising interest costs. Policymakers may be forced to prioritize financial stability and debt management over strict inflation control, creating conditions that historically lead to currency debasement and negative real interest rates.

At the same time, mine supply growth remains limited while central banks continue to absorb a significant share of newly available metal. This combination of constrained supply and steady official-sector demand strengthens the market’s underlying fundamentals.

For Sprott, the current gold market is not simply reacting to inflation or geopolitical headlines. It reflects a broader reassessment of monetary assets in a world where debt continues to expand faster than confidence in the financial system.

If that debt cycle continues along its current path, gold’s role as a store of value may become increasingly important—not only for central banks, but for investors seeking protection from the long-term consequences of rising deficits, growing debt burdens and the gradual erosion of purchasing power.

In the short term, gold remains subject to market conditions such as inflationary pressures from the US-Iran war. On Tuesday, the metal extended its decline to about $4,230/oz., once again erasing its gains for the year.

China’s PBOC adds gold again as bullion remains under pressure

The People’s Bank of China headquarters in Beijing – Image courtesy of Wikimedia Commons

China’s central bank extended its gold-buying streak in May, adding to holdings as prices of the precious metal remained under pressure.

Bullion held by the People’s Bank of China rose by 320,000 troy ounces last month, according to data released on Sunday. The latest addition extended its buying streak to 19 months, the longest since at least 2015, when the PBOC began publishing more regular updates on its gold reserves.

Gold edged lower in May, marking a third consecutive monthly decline after it hit a record in late January. Persistent inflation concerns and expectations for higher-for-longer interest rates triggered by the war in the Middle East have weighed on the appeal of non-yielding assets.

Global central-bank purchases have been a key pillar of support for bullion in recent years. Goldman Sachs Group Inc. said last month it expects the buying to be stepped up as geopolitical developments are likely to reinforce a push to diversify reserves.

Stock image.

Stock image.

{kind=link}

No comments:

Post a Comment