Mexico’s Forced Pivot Away from US Gas Dependence

- Mexico’s near total reliance on U.S. natural gas (covering 70–75% of its consumption) has shifted from an economic convenience to a geopolitical vulnerability as Washington’s pressure intensifies.

- President Claudia Sheinbaum, long opposed to fracking, is now pivoting toward shale gas development as dependence turns into strategic risk.

- With domestic output stuck at 2.3 Bcf/d, unconventional gas is emerging as the only viable path to rebalance supply - despite higher costs and infrastructure gaps.

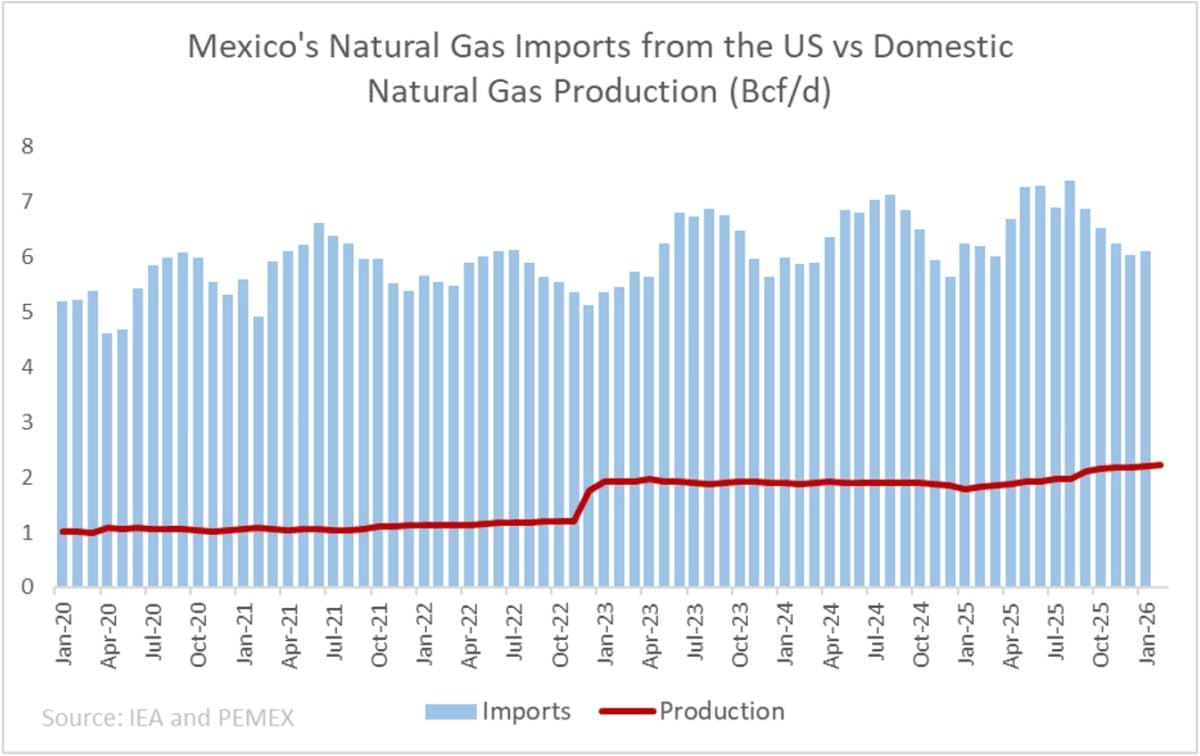

Who could ever transform a climate activist into a shale gas champion? Apparently, Donald Trump. This is exactly what is happening to President Claudia Sheinbaum, who is finally coming to terms with her country’s worsening imbalance between natural gas production and imports. Domestic demand stands at around 9 Bcf/d, while production covers only 2.3 Bcf/d, leaving roughly 6.8 Bcf/d - or 70–75% of consumption – to be met by imports from the United States. This is not just dependence, it is near-total reliance on a single external supplier for the backbone of the country’s energy system. That imbalance is now colliding with geopolitics. Now, with pressure from Washington intensifying, that dependence is turning into leverage.

Mexico’s natural gas dependency on US imports has deepened steadily over the past decade, with pipeline imports rising from 2.2 Bcf/d in 2015 to an average of 6.6 Bcf/d in 2025. The arrangement has been underpinned by favourable pricing: Mexico effectively accesses US domestic gas markets through Henry Hub-linked purchases, currently below $3/MMBtu, making it one of the cheapest sources of supply globally.

This affordability has shaped Mexico’s energy mix. Natural gas now accounts for more than 60% of power generation, embedding US supply directly into the country’s electricity system. More than 70% of imported gas is used to generate roughly half of Mexico’s electricity, with gas consumption reaching approximately 5.5 Bcf/d during peak summer demand in 2025. The scale of this reliance currently leaves the system exposed not so much to price fluctuations but rather to geopolitical risk, particularly as US foreign policy becomes more assertive.

Domestic vulnerabilities are amplifying the risk. Mexico’s grid is increasingly strained by heatwaves, hurricanes, and seasonal volatility, while hydropower (once a key buffer) is losing reliability. Summer output in 2023–2025 fell to around 2 TWh, roughly half of 2018 levels, forcing greater reliance on gas-fired generation and tightening the link between weather shocks and gas demand. At the same time, domestic supply is struggling to respond. Production declined until 2018 and has only seen sporadic gains since, with the last meaningful increase in 2023 – up by over 600MMcf/d, driven by Quesqui and Ixachi. Since then, output has plateaued, leaving unconventional gas as the only viable path to materially lift supply.

Mexico is once again confronting the question it has long avoided, whether to fully embrace shale gas. Its share of the Eagle Ford formation offers clear potential, and Pemex tested it through pilot projects and dozens of fracked wells between 2010 and 2016. But the 2014 oil price collapse and a policy shift under Andrés Manuel López Obrador (including a halt to shale bidding rounds) stalled development. That stance is now shifting. President Claudia Sheinbaum, an environmental scientist and long-time opponent of fracking, is reconsidering unconventional gas as import dependence becomes a strategic risk. On April 8, she announced a new committee to evaluate shale development, focusing on making the process less environmentally damaging.

Yet even with political backing, the transition to large-scale shale development would be far from straightforward. The US experience illustrates both the potential and the challenge. Over the course of the 2010s, technological advances in horizontal drilling and hydraulic fracturing (combined with scale efficiencies across the Lower 48 states) reduced the marginal cost of shale gas production from nearly $15/MMBtu to around $4/MMBtu by 2014. This transformation enabled the US to offset declines in conventional production and establish itself as the world’s lowest-cost large-scale shale gas producer. Replicating this model in Mexico could significantly improve project economics, potentially reducing breakeven costs from the $5–6/MMBtu range typical of other regions to approximately $3-4/MMBtu, bringing domestic production closer to parity with imported gas.

However, the ’Lower 48 US model’ is not simply a set of technologies but an integrated system, combining extensive pipeline infrastructure, a mature oilfield services sector, and a high degree of operational scale. Mexico lacks much of this supporting framework, meaning that even with regulatory backing, development timelines would be longer and costs structurally higher.

This creates a fundamental economic constraint. Even under improved conditions, domestically produced shale gas would likely struggle to compete with imported US pipeline gas priced at Henry Hub levels. Sustaining investor interest in large-scale shale development would therefore require either direct state support – a significant burden on already constrained public finances – or access to higher-priced export markets.

In that context, Asia may be the only commercially viable outlet. Spot LNG prices in the region, as reflected by the JKM benchmark, are currently in the range of $15–18/MMBtu, and even prior to the latest supply disruptions were trading at $10–11/MMBtu. At those levels, exporting domestically produced gas would materially improve project economics and potentially make upstream development profitable. Yet this solution introduces a new layer of contradiction. Prioritizing exports would leave domestic demand structurally reliant on U.S. imports, preserving (rather than resolving) Mexico’s exposure to external pressure.

Mexico does, in fact, have an LNG export project under development: the Energía Costa Azul terminal. However, it does not serve domestic production. The project is a joint venture involving TotalEnergies and Japanese buyers and is operated by the U.S.-based Sempra Infrastructure. Its business model is to liquefy U.S. pipeline gas for export to Asia. As a result, Mexico’s emerging LNG capacity reinforces the existing dependency rather than alleviating it. Dedicated infrastructure for exporting domestically produced gas is effectively absent, and building it would require substantial additional investment, likely led by state-owned Pemex alongside private partners (assuming sufficient capital can be mobilized).

This duality defines Mexico’s current position. The existing system delivers low-cost energy and supports industrial competitiveness, but it also concentrates risk in a single external supplier. The alternative – developing domestic unconventional resources – offers greater autonomy but requires substantial investment, technological transfer, and a recalibration of environmental policy. As external pressures mount and internal vulnerabilities become more pronounced, the balance between these two models is becoming increasingly difficult to sustain.

By Natalia Katona for Oilprice.com

No comments:

Post a Comment