This is "the worst oil crisis in history", says Goldman Sachs

US investment bank Goldman Sachs says we are facing the “worst oil crisis in history” as a result of the shut down of Gulf state hydrocarbon exports.

A Goldman Sachs report represents an upgrade in the severity of the crisis the world is now facing. As IntelliNews reported, the conflict quickly metastasised from a disruption to destruction after a week. Goldman Sachs is now calling it a “crisis”, whereas two weeks ago the International Energy Agency (IEA) labelled this the “largest energy supply disruption in history”.

A global oil supply crunch is approaching as inventories decline and shipments coming out of the Persian Gulf have dwindled to a trickle. Prices of all commodities in the supply chain have already risen, but the US bank warned that problems will intensify in the coming months.

A briefing note cited by analysts at JPMorgan Chase (JPM) also described the situation as a “ticking time bomb”, warning that “physical scarcity of oil is about to unfold across the globe, spreading sequentially through April from east to west”. The disruption is already being felt in Asia and is expected to reach Europe and the US in the coming weeks as tanker arrivals slow.

Separately, The Guardian reported on a looming food crisis as the lack of fertilisers will reduce crops this autumn, putting millions of people in danger of hunger and even starvation.

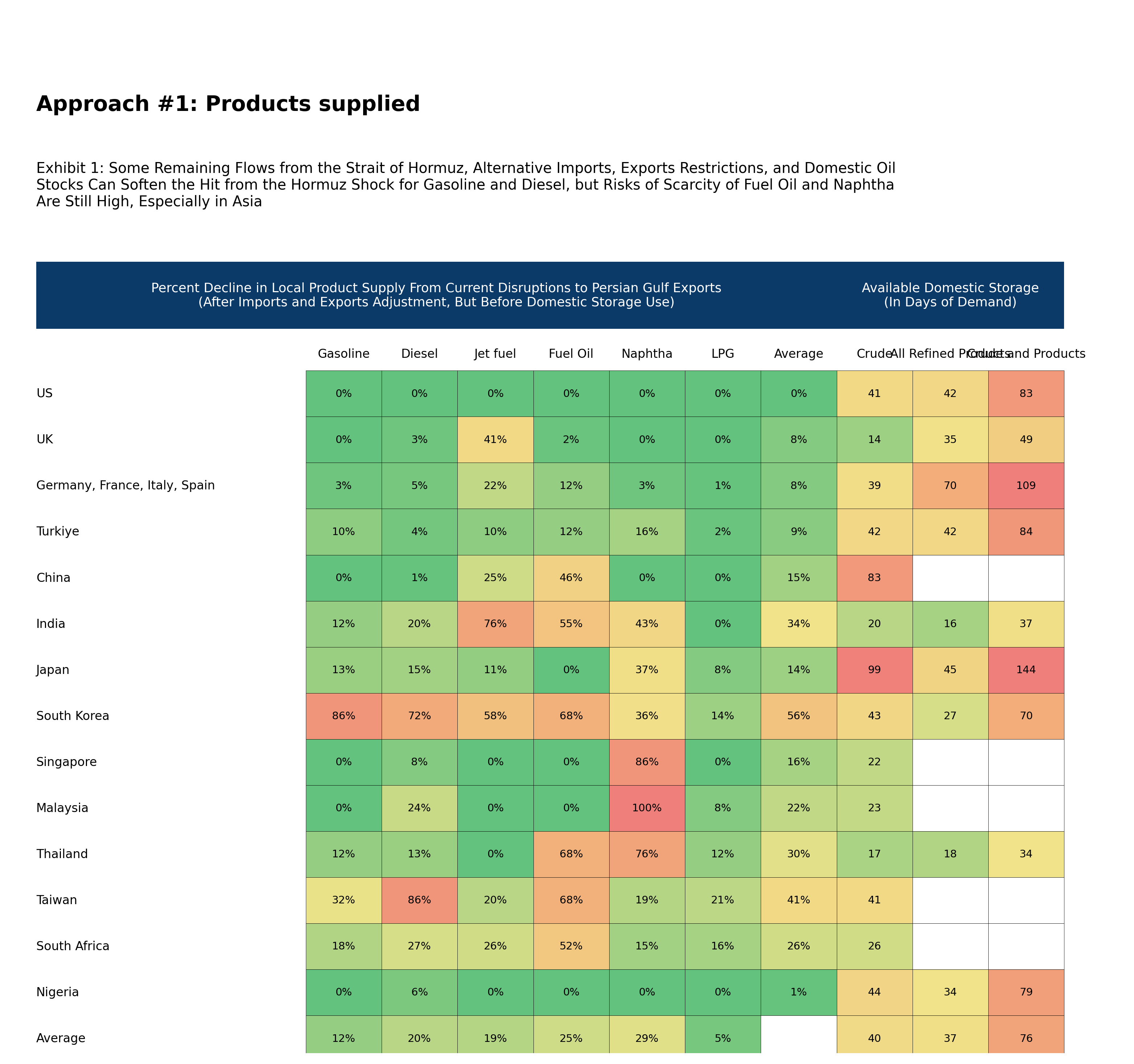

Data from Goldman Sachs indicate that major economies hold an average of about 40 days of crude oil in storage, with significant regional disparities. The UK is described as “uniquely exposed” with only 14 days’ supply, while India holds roughly 20 days. For refined products, inventories average 37 days, with India again among the lowest at 16 days and Japan the highest.

Strategic reserves are being drawn down rapidly. Japan holds the largest crude stockpile in Asia at 99 days, compared with 17 days in Thailand. Countries are increasingly turning to more expensive alternative imports, although analysts note these flows are insufficient to offset the loss of Gulf supplies.

The disruption stems in part from damage to energy infrastructure in Gulf states, alongside a sharp reduction in exports. Analysts warn that these adjustments are finite. “If Persian Gulf flows remain near zero, there is no further offset available and outright supply rationing becomes inevitable,” the JPMorgan note said.

Shipping data indicate that remaining cargoes are already en route, with the last tankers from the region expected to arrive in consuming markets over the coming days. Europe is projected to receive its final shipments shortly, including a last jet fuel delivery scheduled for April 9.

The consequences are expected to be severe. Analysts warn of “demand destruction” through factory shutdowns and flight cancellations, alongside surging prices as Asian buyers pay premiums to divert shipments. In Europe, trucking companies are facing rising costs, with diesel expenses increasing by €1,200 ($1,382) a month. In Germany, up to 100,000 truck driver jobs — about 15% of the sector — are estimated to be at risk.

The disruption will be prolonged thanks to the destruction already wrought. Qatar said that damage to its Ras Laffan LNG plant could take up to five years to repair taking 17% of global supplies off the market.

In the meantime, frustrated with the lack of progress in destroying Iran’s military machine, the US-Israeli coalition are increasingly targeting Iran’s industrial base in the hope of undermining its military. Iran has been responding in kind, putting the industry of the entire region in danger.

Trump set a deadline for Iran to reopen the Strait of Hormuz or face “irreversible damage” to its power grid that expires on April 6. Tehran has vowed to reciprocate and hit the power sectors of all non-friendly countries in the Gulf if the US carries out its threat.

Global recession on the cards

Oil prices would need to average $140 per barrel for two months to trigger a global recession, according to Oxford Economics, as markets brace for prolonged disruption linked to the conflict in the Gulf.

Capital Economics has projected that Brent crude could average $150 per barrel over the next six months if the conflict persists for another three months, pointing to sustained pressure on energy markets already strained by supply constraints.

“The world’s most important price for real-world oil barrels surged above $140, the highest since 2008,” economist Mohamed A. El-Erian said in a post. “Dated Brent, the price of shipments bought and sold in the North Sea, reached $141.37, surpassing levels seen when Russia invaded Ukraine, according to S&P Global, which publishes the data.”

Brent has risen more than 60% since the war began, reflecting escalating risks around the Strait of Hormuz, a critical chokepoint for global oil flows. The International Energy Agency has responded with the largest co-ordinated emergency stock release in its 52-year history, making 400mn barrels available to the market. However, analysts say the intervention has so far failed to stabilise prices.

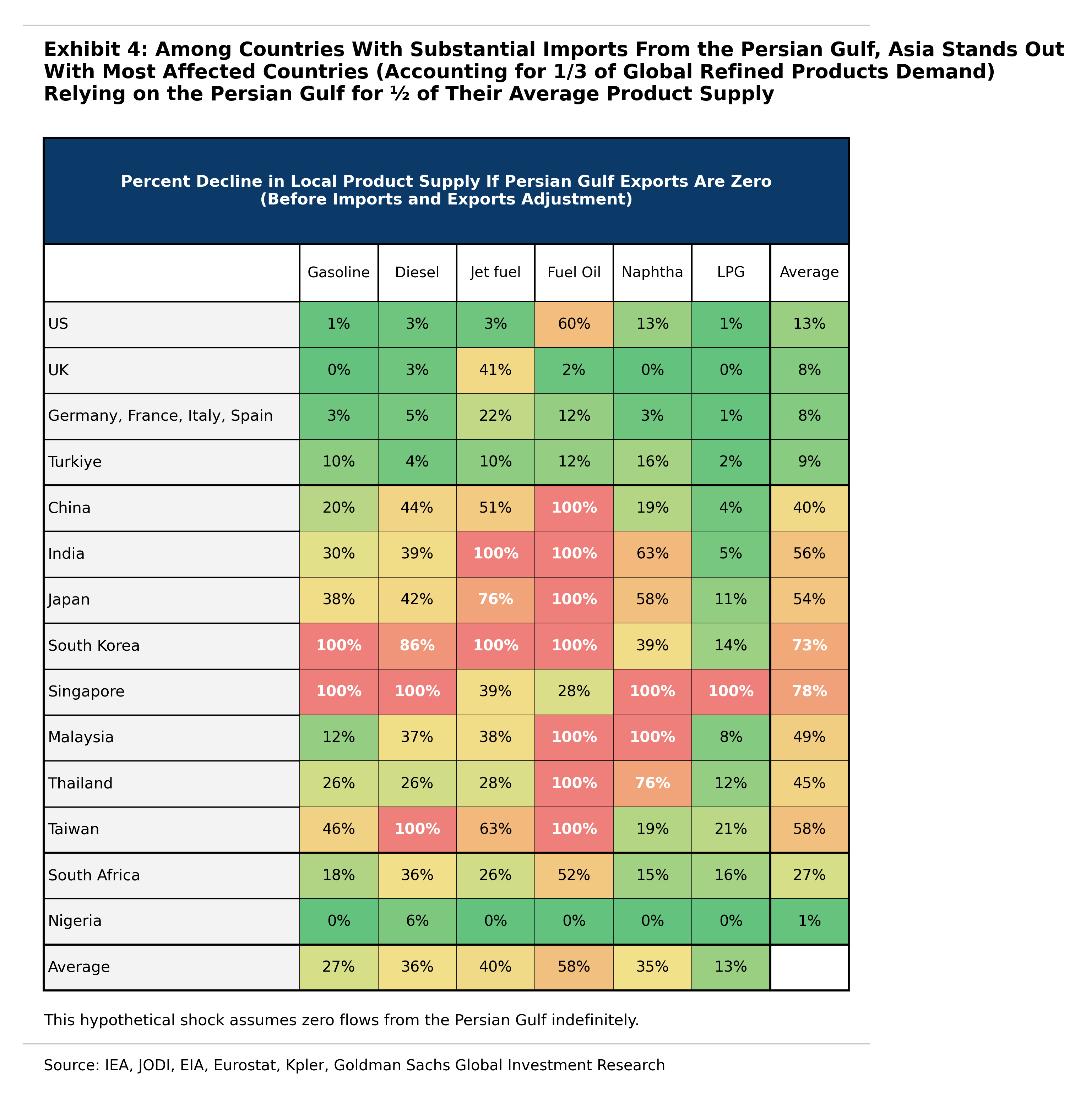

The disruption carries particular significance for Asia, where approximately 80% of oil imports transit through Hormuz. Several economies in the region face acute vulnerability to supply interruptions. Vietnam, for example, is estimated to hold fewer than 20 days of strategic reserves, leaving it exposed to prolonged price spikes or physical shortages.

In Europe, the economic impact is expected to be uneven but significant. Germany, the UK and Italy are seen as having the highest exposure to recession risks due to their dependence on imported energy and sensitivity to price shocks.

The European Central Bank has already adjusted its policy stance in response to rising inflationary pressures, postponing anticipated rate cuts and revising its inflation forecasts upwards as energy costs feed through to the broader economy.

The combination of constrained supply, limited spare capacity and geopolitical uncertainty has heightened concerns that energy markets could become a central driver of a wider global slowdown.

No comments:

Post a Comment