How Iran’s Dark Fleet Is Quietly Keeping Oil Markets Afloat

- Iran’s “dark fleet” is quietly sustaining global oil flows despite visible disruptions, with exports still near pre-war levels and masking the true supply picture.

- The Strait of Hormuz is not fully closed but effectively controlled, creating a parallel system where sanctioned and opaque shipping continues while regular traffic collapses.

- Markets are mispricing risk, as this shadow system stabilizes supply short term but introduces long-term fragility and greater vulnerability to sudden shocks.

It almost looks like an eternal story or an Australian boomerang approach, but the global oil market is once again being misread, very badly. Headlines speak of disruption, paralysis, and the near closure of the Strait of Hormuz. International tanker trackers all report traffic collapsing, while Gulf exporters are shutting in production. Every single visible metric indicates that the system is under extreme stress. And yet, there is still oil flowing. This time it is not open, not as usual able to be measured by markets, or in volumes that are immediately transparent. Still, flows are there, moving steadily and deliberately, in quantities large enough to reshape the current balance of the global market. The real mechanism is a paradox, built on Iran’s so-called “dark fleet”. It is still working as a shadow logistics system that evolved from a sanctions workaround and has become a strategic instrument of geopolitical power.

It should no longer be seen as a marginal phenomenon but has become one of the central pillars of how the global oil system functions under stress. The real uncomfortable truth of it all is that, for now, it is not only tolerated by the international system but also indirectly relied upon.

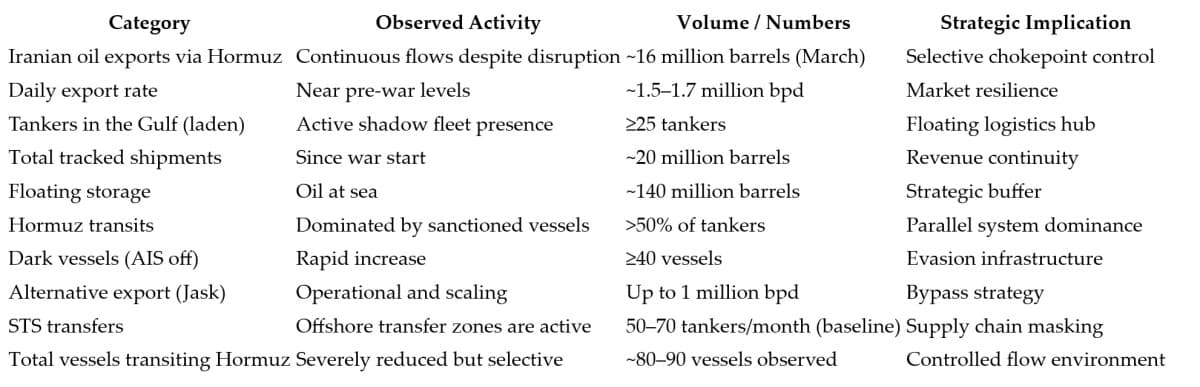

While the conventional flows in the Strait of Hormuz are effectively closed, the reality is that it has not been “totally” closed. The flows have been transformed. Instead of a global artery open to all, Hormuz has become a selectively controlled corridor. Yes, overall commercial traffic has collapsed, with a decline of more than 90 percent compared to normal levels. It should, however, be recognized that this collapse is uneven. It applies primarily to Western-linked shipping, major Gulf exporters, and vessels operating within regulated insurance and compliance frameworks. At present, there is a well-functioning parallel system in place that continues to operate beneath this visible collapse. Iranian-linked tankers, sanctioned vessels, and ships operating under opaque ownership structures are still clearly moving through the strait, often with tacit or explicit tolerance from Iranian naval forces. The ultimate result is a bifurcated maritime system: one visible, regulated, and largely immobilized; the other opaque, flexible, and still active.

For markets and pundits, this distinction should matter enormously. Because Saudi Arabia, the UAE, and other Gulf producers are seeing exports constrained or rerouted at great cost, Iran has managed to sustain flows at strikingly resilient levels. Current estimates indicate that Iranian exports have remained in the range of 1.5 to 1.7 million bpd, which is surprisingly at pre-war levels. In March alone, more than 16 million barrels are estimated to have transited through Hormuz under these conditions. Again, markets need to realize that the chokepoint is not closed, but Iranian-controlled.

The current situation is not accidental at all, as Tehran has been setting it up over years of adapting to sanctions pressure, drawing on lessons learned from Russia’s post-Ukraine shadow-fleet operations. Even though it is hard to admit, Tehran has managed to set up a system that is sophisticated, decentralized, and remarkably difficult to disrupt without escalating into a full-scale maritime conflict. At its core, the dark fleet relies on ownership opacity, the manipulation or outright deactivation of AIS signals, and the extensive use of ship-to-ship transfers. At the same time, these tankers are transparent and shell companies, often in jurisdictions with limited transparency, and flagged in states with weak enforcement. As has been seen again in the last few weeks, all of these vessels routinely “go dark” during critical phases of their voyages. At the start of the conflict, it was reported that at least 40 vessels were observed disabling AIS signals, a number that has likely increased as operations intensified.

None of these vessels operates in isolation; they are part of a network in which Iranian ports, especially Kharg Island, serve as initial loading points. At the same time, the Persian/Arabian Gulf continues to function as a staging area, with multiple laden tankers serving as floating storage and logistical buffers. In contrast, the Indian Ocean and Southeast Asian waters serve as transfer zones. Most cargoes are frequently transferred between vessels before being delivered to end buyers, with China as the primary destination. By the time the oil reaches its final market, its origin has been effectively obscured. This is not a loose collection of opportunistic actors; it is a structured, resilient supply chain.

The most persistent misunderstanding in current market analysis is the scale of these operations. At present, the assumption is that a collapse in visible tanker traffic equates to a collapse in supply. This is at present incorrect, as available intelligence suggests that between 1.0 and 1.7 million bpd of Iranian crude continues to move. Most of these barrels are moving through the very chokepoint that is presumed to be closed. It is known that within the Gulf itself, at least 25 laden Iranian tankers have been operating as part of this shadow system. They have collectively handled tens of millions of barrels since the start of the conflict. Iran has also been able to build up a substantial floating storage buffer, with estimates suggesting as much as 140 million barrels of crude held at sea. They are currently serving as both a revenue stabilization mechanism and a strategic reserve that can be released into the market when conditions permit.

At the same time, Iran has been, beyond Hormuz, activating alternative export infrastructure, most notably the Jask terminal on the Gulf of Oman. Even though it is still limited, Jask provides critical redundancy, allowing exports to bypass the strait entirely. With its almost 1 million bpd capacity, Jask represents a significant hedge against a complete maritime closure. Both options form a hybrid export model that combines controlled chokepoint access, offshore storage, alternative routing, and shadow logistics. Even though it is not as efficient as traditional operations, the system is highly effective under conditions of geopolitical stress.

For all, including policymakers, the most uncomfortable question to be answered is: why has it not been stopped? The possible answer, however, lies in a fundamental contradiction at the heart of current policy. Even though the USA and allies want to constrain Iran’s revenues and limit its geopolitical influence, they also understand that removing Iranian oil from the market entirely would trigger a supply shock of potentially historic proportions. With 15–20 percent of global oil and LNG flows already disrupted by the Hormuz crisis, the real risk in the market at present is further supply losses. The margin for additional losses is extremely thin. A full blockade of Iranian exports would not only drive prices sharply higher but would also almost certainly destabilize global economic conditions at a time of already heightened uncertainty.

We are at present looking at a form of strategic ambiguity. Enforcement actions are selective. Sanctions remain in place, but their application is uneven. Markets are even prevented from overheating by temporary waivers or tacit allowances. Reality at present is, maybe not to the liking of most people, that Iran’s dark fleet is being allowed to operate within certain limits. Policymakers and advisors in Washington and elsewhere see it as an instrument serving as a stabilizing function, keeping barrels flowing that the market cannot easily replace. This is not a sustainable equilibrium, but it is the one currently in place.

Mispricing, however, is clearly in sight, as financial markets continue to focus on the system's visible layer. Financials are tracking tanker movements through conventional channels, monitoring official export data, and responding to headlines about infrastructure damage and production cuts. They, however, fail to recognize or incorporate the scale and persistence of the shadow system operating alongside it.

A series of mispricings seems to be in the market, as supply disruptions are often overestimated in the short term, while longer-term risks are underestimated. In the short term, Iran’s dark fleet is mitigating risks, but the system sustaining these flows is fragile and opaque. Also, markets need to reassess the impact of the control that Iran has achieved. By effectively regulating access to Hormuz while maintaining its own exports, Iran has shifted from being a constrained producer to a gatekeeper of regional flows.

We could not be looking any longer at a temporary distortion but at the buildup of an outline of a new market structure. The old global oil system seems increasingly divided into two parallel layers: a transparent, regulated system governed by formal rules, and an opaque, politically mediated system in which flows are determined by access, relationships, and the ability to operate outside conventional constraints. Tehran is clearly dominating the second level but will not be alone for long. Russia has already developed similar capabilities, while it can be expected that others will follow too. This move could result in a system in which sanctions become less effective, and control over logistics becomes as important as control over production itself.

Even though it is currently highly effective, the dark fleet system remains inherently unstable. The vessels involved are often old and poorly maintained. The vessels have limited or no insurance coverage, and operational standards are inconsistent. Any risk, disaster, or collision could remove significant volumes from the market overnight, trigger environmental damage, and provoke a more aggressive enforcement response. It also operates at the behest of the powers in place. The system works because it exists in a grey zone. It is neither fully legal nor fully suppressed but tolerated because it is useful. That tolerance, however, is conditional.

While the Gulf conflict is often framed in terms of missiles, drones, and military escalation, attention should be increased for a more consequential struggle that is unfolding at sea. Attention is needed for the quiet, persistent movement of oil through networks that operate beyond the reach of conventional oversight. For Iran, its dark fleet is not a workaround but a strategic asset that not only generates revenue but also sustains exports, supporting its influence over a global system still deeply dependent on Gulf energy flows.

This also shows the fundamental shift in how energy markets function under geopolitical stress. The conventional link between production, transport, and pricing is being replaced by a complex, less transparent system controlled by movement rather than ownership.

This system is currently keeping the market afloat by cushioning the shock of disruption and preventing a more severe supply crisis. It also stores risk, as it makes clear that the more the global economy depends on flows that cannot be fully seen, measured, or controlled, the more vulnerable it becomes to sudden and unpredictable shocks.

By Cyril Widdershoven for Oilprice.com

No comments:

Post a Comment