It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Despite VW’s Dieselgate scandal in 2015, and most carmakers choosing otherwise, Volkswagen AG has made a bold statement with its commitment to diesel-powered vehicles.

Although diesel-engined cars and SUVs are a dying trend the world over, Volkswagen has demonstrated its commitment to diesel power by developing engines that can use adapted diesel fuels, claimed to reduce CO2 emissions by up to 95 percent over conventional diesels.

In fact, all VW models with the four-cylinder TDI powertrains delivered in Europe since June this year can be used with paraffinic diesel, a newly developed fuel containing bio-components.

VW to continue developing electric and combustion powertrains

VW diesel engines can run on paraffinic fuel to reduce emissions by up to 95 percent

Paraffinic diesel is produced from biological residual and waste material

Volkswagen's global diesel strategy

While Volkswagen has focused its efforts on ramping up its electric vehicle line-up, the firm’s commitment to diesel shows that it is receptive towards other ways of reducing its carbon footprint, in its bid to decrease carbon emissions by 40 percent by 2030 and become carbon-neutral by 2050.

It is a different approach compared to its competitors – who have made bold statements about going fully electric in the next 10 years. By comparison, Volkswagen has said it plans to increase the share of all-electric cars sold in Europe to over 70 percent by 2030.

Meanwhile, diesel cars' share, in particular, has seen steep decline – a trend that started with VW's Dieselgate scandal in 2015. In India, the share of diesel cars fell from 40 percent in FY2017 to just 19 percent by the first half of FY2021. In markets such as the UK, where diesel once accounted for roughly half of new car sales, it now makes up only 5 percent.

“Alongside [the] accelerated ramp-up efforts in the area of electric mobility, Volkswagen is further developing the existing range with combustion engines," a VW spokesman told our sister publication, Autocar UK. “In this way, the company is responding to different customer needs, while at the same time, taking into account the internationally varying drive system preferences and the respective general conditions.”

Scope of paraffinic diesel and other e-fuels

The firm added that paraffinic diesel fuel could be attractive to fleet customers, who run a mix of electric and conventionally powered vehicles. It anticipates that the fuel's market share in the road transport sector could increase to 20-30 percent in Europe, within 10 years.

Paraffinic fuels are produced from biological residual and waste materials such as hydro-treated vegetable oil (HVO). These are then converted into hydrocarbons and can be added to diesel in any quantity. V-Power Diesel and HVO are currently available in the UK.

Volkswagen added that other e-fuels such as Power-to-Liquid (PtL) will be offered in future, which are produced from regenerative sources using CO2 and electricity. In this process, excess green energy could be used in their production.

Volkswagen's petrol and diesel fuel boss Thomas Garbe said: “Through the use of environmentally friendly fuels in the approved Volkswagen models, we are making it possible for customers throughout Europe to significantly reduce their CO2 emissions as soon as the fuel is locally available.”

Volkswagen’s diesel strategy in India

Diesels used to be a big part of the Volkswagen Group’s model line-up here as well. Starting with the Polo's 1.2-litre TDI engine and going all the way to the higher-end 4.2-litre TDI in Audi models like the Q7andA8.

Volkswagen, however, decided to pull the plug on diesel engines in India as we transitioned into the stringent BS6 emission norms last April. The cost of after-treatment systems on diesels to clear the BS6 norms would have invariably driven up the prices, making little sense in small cars. And while Volkswagen had previously hinted on the return of diesel engines for larger models in the India 2.0 strategy, there’s currently no news of diesel being brought back. Thus, unlike the firm’s global portfolio, the VW Group models here will continue to be petrol-only for now.

Volkswagen diesel engines now approved for use with paraffinic fuels; up to 95% savings in CO2 emissions

Volkswagen hasn’t completely foregone diesel, it has shown, with its announcement that its latest generation of four-cylinder diesel engines which it has approved for use with paraffinic fuels. These are newly developed diesel fuels which contain bio components that enable significant savings in CO2 emissions, between 70% and 95% compared with conventional diesel, it said.

All Volkswagen models with four-cylinder diesel engines delivered from the end of June this year received approval for operation with paraffinic diesel fuels in compliance with the European standard EN 15940, said the automaker.

“Through the use of environmentally friendly fuels in the approved Volkswagen models, we are making it possible for customers throughout Europe to significantly reduce their CO2 emissions as soon as the fuel is locally available,” said Volkswagen head of petrol and diesel fuels Thomas Garbe. The use of these paraffinic diesel fuels is a sensible option, particularly for companies with a mixed fleet also comprised of electrified vehicles, Garbe added.

Volkswagen Golf 2.0 TDI engine

There are several types of paraffinic diesel fuels; one such type is produced from biological residual and waste materials such as HVO (hydrotreated vegetable oil), which is converted into hydrocarbons through reacting with hydrogen, and can be added to diesel in any quantity, or used entirely on their own as a fuel, said Volkswagen.

Vegetable oils such as rapeseed oil can also be used in the production of HVO, though its maximum environmental benefit can only be obtained through the use of biofuel residual and waste materials such as used cooking oil, sawdust and others. Biofuels using HVO are already on the market, says Volkswagen, and their share in the energy market could increase to 20 to 30% for road transport in Europe within the next 10 years, it said.

In the future, there will also be e-fuels, otherwise known as power-to-liquid (PtL), and will be produced from regenerative sources with the use of CO2 and electricity. Also known by X-to-liquid (XtL), GtL and PtL acronyms, these begin with the initial production of a synthesis gas from different raw materials, which is then converted to standard-compliant diesel through the Fischer-Tropsch process. Excess green energy can be used in this production process, says Volkswagen.

The latest diesel engine development is Volkswagen’s additional effort towards reducing CO2 emissions for becoming climate-neutral by 2050, in addition to the industry-wide push for electrification. The German manufacturer’s goal for 2030 is to reduce per-vehicle emissions in Europe by 40% compared to its figure in 2018.

Volkswagen has delivered not one but two good news stories this week. The first aims to alleviate climate change, by introducing diesel engines that can run on green fuels; the second will help Golf drivers change their own climate more easily, with a major update to the infotainment system.

Volkswagen has been rolling out its fleet of new battery-electric vehicles in a bid to reduce its carbon footprint by 40 per cent in Europe by 2030. But to minimise the carbon legacy of the diesel cars it will deliver between now and then, it has made all its four-cylinder TDI engines able to run on paraffinic fuels. This modification applies to vehicles delivered from the end of June this year.

Prof. Thomas Garbe, Volkswagen's Head of Petrol and Diesel Fuels said: "Through the use of environmentally friendly fuels in the approved Volkswagen models, we are making it possible for customers throughout Europe to significantly reduce their CO2 emissions as soon as the fuel is locally available. For example, the use of paraffinic fuels is a sensible additional option particularly for companies with a mixed fleet made up of models with electric and conventional drives."

Paraffinic fuels that meet European standard EN 15940 aren't blended with any regular diesel. They are made with the Fischer Tropsch process from natural gas (GTL), biomass (BTL) or through the hydrotreatment process of vegetable oils or animal fats (HVO). They have next to no sulphur and aromatics, and can lower CO2 emissions by up to 95 per cent compared with conventional diesel.

True enough, EN 15940-compliant fuels aren't actually widely available at the moment, but they are out there and include C.A.R.E diesel, NEXTBTL and HVO. It's more common to see a mix of paraffinic and regular diesel, such as Diesel R33, V-Power Diesel, OMV MaxMotion and Aral Ultimate Diesel. Volkswagen has said these mixed fuels can be used in all its diesel engines, even the older ones.

The second piece of good news is that help is finally coming for those experiencing problems with the latest Volkswagen infotainment system. You almost certainly will be, because the MIB3 system is, relatively speaking, a shocker. Company insiders we've talked to have said many of its problems relate to the poor integration between its outside software developers and the inhouse team at Volkswagen. The issues have been manifest and delayed the launch of the ID.3; even now the software is unresponsiveness and full of bugs.

The latest Golf is the first to come with the infotainment upgrade, which is both hardware and software. There is a more powerful System on Chip (SoC) central processor that trebles the graphics performance and adds 25 per cent more computing capacity. The software improvements are said to make the infotainment more stable and useable when using the touchscreen, although the gesture control and natural voice control have been enhanced, too. You can use the former from farther away now, and the voice control has a new digital microphone, which it's claimed can distinguish between the driver and passenger - so when asked to alter the interior temperature, it knows which side to adjust. Volkswagen also says its comprehension rate is up to 95 per cent.

Although the changes are currently for the Golf, it seems logical that they will be extended to the ID.3 and ID.4. And Volkswagen has said it plans to roll out the new software to existing Golf models in the coming months.

Thursday, December 07, 2023

Report Zero-Emission Fuels Could Add 50% to Container Shipping Costs

Early adopters face the highest costs and hard decisions highlights new report on cost of zero-emission fuels

The early moves both among the container carriers and the shippers face substantially higher costs for transporting containers using the new generation of zero-emission vessels and fuels. A new report from independent UK consultancy UMAs seeks both to quantify some of the potential costs and contribute to the discussions by highlighting the challenges that lay ahead for the industry, echoing similar concerns raised by industry CEOs attending the current COP 28 conference and other reports that highlight the potential near-term shortages in the supply of alternative fuels.

“The role of the early movers including cargo owners, and their willingness to pay is therefore vital in setting up a zero-emissions shipping market,” writes UMAS. “This report contributes to that dialogue by providing examples of baseline additional cost per container required to bridge the cost gap considering only technological savings. It shows the room that cargo owners, governments, and other stakeholders have to contribute.”

UMAS used a variety of models to estimate the costs that will be incurred concluding that they could add as much as half to the current price of moving boxes on some routes. Initially, the report predicts there will be a significant cost gap between conventional fossil fuels and scalable zero-emission fuels. For example, in 2030 on the transpacific route, under the best-case fuel price scenario, the cost difference can be $150 per TEU for green ammonia, $210 per TEU for green methanol, and as high as $350 per TEU for green ammonia and $450 per TEU for green methanol in a high fuel price scenario. The lowest cost they find would be $90 per TEU transpacific and even on a Chinese coastal route could range between $30 and $70 per TEU.

The fuel cost gap is now acknowledged as the main blocker for shipping’s transition and tackling it requires a frank conversation about the dimension of the challenge,” said Camilo Perico, Consultant at UMAS, and author of the report. “We need “numbers on the table” and more visibility on how stakeholders can help to cover it.

The report details significant financial burdens, especially for the early adopters which will be needed to move the market forward. The industry has cited these same concerns. The CEOs of five leading carriers last week called for regulatory efforts and a move to level the cost difference between traditional and alternative fuels spreading the premium across all fuels.

UMAS calculates that a vessel operating transpacific would require an additional $20 to $30 million annually by 2030 when you consider both the capex investment in the vessels and operational expenditure. Fuel they highlight would be $18 to $27 million of the added annual cost.

Early adopters will have some choices according to UMAS which will also have an impact on the market. They could go with cheaper but non-scalable fuels such as the much-touted bio-methane, which they conclude will however become more expensive as demand outstrips supply. The alternative will be to invest in fuels with a higher capital expense but it would stimulate the market and become less expensive as production ramps up. UMAS expects that the cost gap will not narrow until 2050.

“The analysis shows fuel costs are a major component of the overall cost and therefore the primary driver of the total cost of operation. With the right demand signals and corporate action during the emergence phase, production and supply of zero-emission fuels and freight services can make a head start in lowering the cost gap that this work has shown,” said Dr. Nishatabbas Rehmatulla, Principal Research Fellow at UCL and co-author of the report.

They are calling for increased dialog and using the data to help plan the long-term approach for the shipping industry. The report notes that there are already emerging subsidies that could close the gap between conventional fuels and the new scalable alternatives. They highlight the regulatory efforts in the EU and U.S. that have the potential to help cover the cost difference on specific routes as well as future initiatives such as programs in the UK and Norway that would specifically support hydrogen fuels.

UMAS concludes that the window of opportunity for corporate action before regulation increasingly closes the gap is only available for a few years. The full report and the analysis are available online to help guide the discussion and the decision that the shipping industry needs to undertake.

Why Clean Shipping Fuels Need Solar-Industry Style Support

Shipping receives nowhere near the media coverage given to aviation, yet the sector also accounts for around three percent of global energy-related carbon dioxide emissions. Its footprint must be tackled rapidly if international climate targets are to be met. Solutions to decarbonize shipping exist, most notably in the form of green methanol, and some shipping firms are investing heavily in a greener future. However, the regulations and financial support needed to scale up the sector and push down costs are still found wanting.

The wind and solar industries are today mainstream players in the power sector. Costs, in particular for solar, have fallen massively everywhere. However, this positive trend would not have happened without significant government backing as these industries were starting out. The shipping industry has been used to accessing cheap fuels and, without similar financial and legal assistance, cleaner shipping fuels will remain an expensive pipe dream.

The shipping sector must reduce its emissions by 45 percent by 2030 compared with 2010 to come in line with the Paris Agreement commitment to keep global heating below 1.5°C above pre-industrial levels, says the Copenhagen-based Mærsk Mc-Kinney Møller Center for Zero Carbon Shipping, a not-for-profit research center. Meeting this target will be challenging, but the technology to achieve it exists and companies are engaging with the transition.

First, the technology. Methanol is a chemical compound that has long been in great demand for a variety of industrial applications. It is a relatively benign substance and, as a light liquid, it is easy to transport and store at room temperature. Almost all methanol today is, however, produced from coal and natural gas. Green methanol, on the other hand, is generated from clean energy sources either as bio-methanol or e-methanol. Bio-methanol can come from biogas or the gasification of sustainable biomass sources like agricultural and forestry residues and municipal waste, while e-methanol is produced from green hydrogen from renewable electricity and captured carbon dioxide.

Danish company Maersk has leapt ahead of global regulatory requirements through a commitment to procure only vessels compatible with green fuels and is taking steps towards retrofittings. As part of this transformation, the company has ordered 25 green methanol vessels it expects to come into service in the next three to four years. These decisions will help drive the creation of new green methanol supply chains as Maersk develops extensive off-take partnerships with energy companies.

Maersk is not the only company changing the way it does business. The global order books for low emissions vessels grew six-fold from 2019 to 2022 and changes to bunkering and fuel supply are also beginning to happen. In 2016, there were almost no shipping ports planning green fuel bunkering; by the end of 2022, ports representing around 16 percent of global shipping volume had announced plans to build out green fuel bunkering.

Green methanol supply has also been growing rapidly with total global production capacity increasing by 450 per cent from 2020 to 2023. This figure may sound impressive, but it comes from a very low base. Today, there are less than 0.2 million tonnes of green methanol on the market; we need at least 20 million tonnes by 2030. Further, production costs remain high, leaving large numbers of projects stuck in early-stage development. They will remain there unless we can secure long-term offtake at a price that makes these projects viable — but shipping companies cannot simply pass all of these higher costs to the owners of the cargo they move.

Governments can help solve this affordability gap between the cost of production and customer willingness to pay through "demand pull" initiatives, like the mandates for green hydrogen in the EU’s Fit for 55 package. Such policies create a clear demand signal and the industry can examine how to meet that at the lowest cost. We also need "supply incentives" like the EU's Hydrogen Bank and the US Inflation Reduction Act to help bridge production cost gaps.

Corporate leaders surveyed for Global Corporate Stocktake carried out by We Mean Business, with support from the UN Climate Champions team and consultancy Bain & Company, ahead of the COP28 climate summit, cited the lack of infrastructure to support fuel production and bunkering, commercial constraints and uncertainty surrounding technology pathways as important blockages to system change in the shipping industry. They also emphasized the need for governments to support collaboration between different actors in the shipping sector to push initiatives like "green corridors" where low-emissions vessels are incentivized.

Ultimately, green methanol will not be the only solution to decarbonize shipping. In the coming years, other low-emission fuels, like ammonia, are likely to come onto the market, with the end result being a complementary patchwork of solutions. For the moment, though, governments, and industry, should be focused on green methanol as a proven, easy-to-use solution that, with the right support, can be scaled up immediately.

Brian Davis is CEO of C2X, a standalone company founded by A.P. Moller Holding (APMH) and its shipping arm Maersk to "defossilize" the fuel used by shipping.

The opinions expressed herein are the author's and not necessarily those of The Maritime Executive.

Report: Financial and Regulatory Barriers Delay Zero-Emission Fuel Supply

Barriers are holding back the projects needed to produce shipping's zero-emission fuels

Zero-emission fuels such as methanol and ammonia are an important focus in the efforts to reach the shipping industry’s decarbonization targets, but a new report highlights that leaders across the industry believe financial and regulator hurdles are slowing the developments. Presented as a perspective on how to start addressing the barriers affecting zero-emission fuel projects, the report calls for unconventional partnerships and business models supported by regulatory and financial collaborations to overcome the barriers to lay the foundations for a zero-emission future in shipping.

While there has been a lot of publicity and discussion about these zero-emission fuel projects, the report concludes that “more than 95 percent of the projects centered on producing these fuels have not yet passed the final investment (FID) phase.” They highlight that this is despite the rising demand for the fuels as indirectly indicated by the more than 180 dual-fuel ships already on order and more planned.

“We are in the middle of what needs to be the decade of action if maritime shipping is to achieve net-zero emissions by 2050,” writes Mette Asmussen of the World Economic Forum and Peter Jonathan Jameson of Boston Consulting Group in the forward of their new report. “We need to eliminate these emissions through scaling of technologies that can power deep-sea vessels.”

Despite the positive momentum, the report highlights that the shippers and carriers that helped to launch the First Movers Coalition for shipping in 2021 are saying that barriers in the maritime value chain and beyond are hindering decarbonization from progressing at the speed needed.

Interviewing industry stakeholders, the report highlights that the nexus between demand and supply is an important dynamic and will help to increase the confidence to invest in the supply side. The interviews with more than 20 stakeholders shed light on the barriers that they believe are holding back the investment decisions and progress that is required.

Ten barriers were identified as limiting the projects from getting past the key FID milestone. The report categorizes the barriers into segments including customer and consumer demand, economic and financial issues and regulatory, as well as supply chain and infrastructure challenges and organizational issues within the companies. They point to issues such as the “green premium” and the lack of clear signals and willingness to cover the costs as well as the gap in offtake agreements and the lack of credible cost estimates.

Existing financial instruments and funds they also conclude are “not fit for purpose in terms of horizons and risk appetite.” At the same time, they point to a lack of near- and mid-term mandates or a global carbon price. Finally, they point to infrastructure issues for the storage and transportation of e-fuels.

The report concludes that while collaborations are underway to overcome the barriers, more needs to be done to get the first movers to take bold actions to advance the development of alternative fuels. “Although daunting, these barriers need not all be overcome simultaneously,” the report asserts.

They call for steps in addition to the support of green corridors that can consolidate shipping’s demand for methanol and ammonia with other sectors to hedge end-market risk. They also see the need to drive offtake agreements suggesting steps including reverse auctions using public-private demand aggregation.

The report also calls for using innovative contracting and financing mechanisms. They suggest that steps such as capacity payments, dynamic contract pricing, and offering equity stakes to strategic buyers could help to overcome the current financial challenges.

The report follows on from a statement last Friday, December 1, by five of the CEOs of the largest shipping companies highlighting the challenges they see in meeting the decarbonization objective. Their message called for greater collaboration and regulator efforts to support the industry during this period of transition.

Friday, July 21, 2023

Environmentalists Say FuelEU Maritime’s Transition is Too Slow

T&E recommends further enhancements to the EU's emissions regulations (iStock)

Environmentalists continue to be critical of the maritime industry as well as regulators in their efforts to get shipping to align with the broader climate goals of the Paris Agreement on global warming. The influential group Transport & Environment (T&E) released a new study looking at the potential impact of the FuelEU Maritime legislation finalized earlier this year and how it will address shipping and specifically container shipping’s use of fossil fuels. Reporting that it will be a slow transition, T&E is recommending that the European Commission make further improvements to the “Fit for 55” package for the shipping sector.

The group calls the FuelEU Maritime component “arguably the most important shipping-related legislation,” in the EU’s new package and said the program which reached a political agreement in the spring of 2023 is a welcome step in tackling shipping’s emissions. They said the regulation is “a positive step,” citing the introduction of mandates to transition to lower carbon fuels and the small, initial sub-target which they said will “kick-start the use of sustainable e-fuels.”

T&E’s new study aimed to analyze the impact of FuelEU Maritime combined with the European Union’s Emission Trading System (EU ETS) by modeling how shipping companies are most likely to act in the face of different regulatory constraints and pricing. The model, they reported, allowed them to predict potential demand from container operators in the EU for a range of marine fuels. The study projects what mix of technologies and fuels will be in demand from the containership segment across a period of 30 years from 2025, as well as the primary costs involved.

“Given the limited ambition of the GHG intensity reduction targets, FuelEU Maritime green-lights a slow-motion transition away from fossil fuels in shipping, with oil-based fuels and fossil gas still likely to make up the majority of fuel demand until 2045,” the group reports. “We find that under the existing regulation, the industry would see a slow transition away from polluting fossil fuels, such as LNG, which ships could continue using into the 2050s, towards more sustainable e-fuels.”

Under their base case pricing scenario, T&E’s study suggests that the current legislation will fall short of encouraging significant extra demand for non-biologic renewable fuels. They expect that demand for fossil LNG will continue to grow until at least 2035 when e-ammonia could begin to rapidly grow. They also looked at the impact of lowered biofuel prices or delays in the feasibility of ammonia engines.

Pricing they find could impact demand for other shipping fuels, including bio-methanol, e-methanol, e-diesel, and e-methane. They, however, speculate that in the “base case,” demand and efficiency assumptions, could lead to unsustainable volume demands for biofuel. They find it could reach an equivalent to 114 percent of current consumption by all EU transport. T&E believes that a sustainable transition is possible under an alternative scenario with lower demand growth and improved energy efficiency. However, they report that e-fuels’ share of shipping fuel demand would still need to reach 18 percent in 2035 and 85 percent in 2040 respectively to decarbonize the shipping sector.

“The shift to cleaner fuels is likely to be driven almost entirely by the progressive reduction in GHG intensity targets,” contends T&E. Based on that belief along with the conclusions that the current regulation permits “unacceptably heavy use of fossil LNG and also does too little to guarantee demand for renewable fuels,” T&E is recommending further “improvements” to the Fit for 55 package for shipping.

They continue to call for the greenhouse gas intensity targets to be aligned with the Paris Agreement. To achieve their targets, they want higher and additional targets for renewable fuel along with expanding the FuelEU package to cover more ships, including below 5,000 gross tons as well as offshore vessels and other non-cargo ships. They also want mandates for more sustainable fuels, such as ammonia, methanol, and hydrogen, to replace the existing LNG bunkering infrastructure.

T&E concludes its recommendations by calling for the implementation of mandatory energy efficiency requirements on European shipping. They also want strong penalties for non-compliance to discourage the shipping industry from simply paying for compliance instead of making significant changes to reduce emissions.

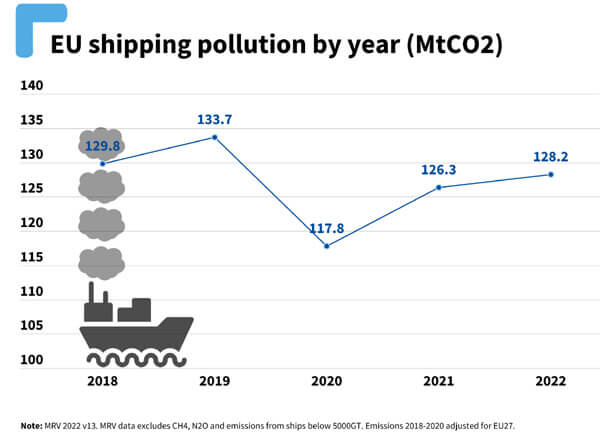

T&E Highlights Continuing Rise in European Shipping’s CO2 Emissions

T&E cites containerships along with LNG carriers and cruise ships as contributing to the rise in CO2 emissions in Europe (file photo)

Harmful emissions for ships operating in Europe grew to a three-year high as the industry edges closer to pre-pandemic levels reports the NGO Transport & Environment (T&E). Performing an analysis and review of the data released under the European Commission’s Monitoring, Reporting, and Verification requirement, T&E contends the shipping industry is continuing to move closer to the point of no return in the efforts to stop global warming.

The outspoken environmental group used the 2022 data released at the beginning of July from the EC’s monitoring of vessels. They sought to adjust the historic data to reflect the change in geographic scope when the UK exited the EU and reporting in 2021. Emissions they showed have risen in the past two years from a low in 2020 during the pandemic.

Total emissions were up about three percent in 2022 versus the prior year and are up nearly nine percent from the low point in 2020. Despite the increases in the past two years, emissions measures in metric tons of CO2 are down from both 2018 and 2019 levels. Despite being up last year, levels are still down over four percent from the 2019 peak.

“Carbon emissions are at a three-year high as shipping companies continue to go all guns blazing. Europe’s shipping giants are up there with coal plants and airlines as the continent’s biggest polluters,” said Jacob Armstrong, shipping manager at T&E. “Without stricter regulations, shipping companies will continue to spurn investments in efficiency and green fuels.”

Breaking down the nearly 130 million tonnes of CO2 emissions recorded in 2022, T&E reports containerships accounted for the largest portion or nearly 30 percent of total emissions in Europe. Bulk carriers and tankers were a distant second and third, each around 15 percent of emissions.

The largest increases came from liquified natural gas shipments. LNG gas carriers’ emissions were up 58 percent according to T&E’s analysis. They cited Europe’s efforts at ramping up sanctions on Russian oil, and the push for more seaborne imports to meet gas needs. Similarly, cruise ship emissions were almost double in 2022 over the prior year as the industry continued to overcome previous disruptions to international travel due to the pandemic.

As expected, the largest shipping companies are also the ones T&E cites are the largest emitters. MSC, they contend is currently Europe’s 11th biggest polluter and the largest in the shipping industry with 10 million tonnes of emissions in 2022. MSC was followed in T&E’s analysis by CMA CGM, Maersk, COSCO, and Hapag-Lloyd in the list of shipping emitters.

The group does not address the potential impact going forward from either the EU’s ETS scheme due to start in 2024 or the IMO’s revised targets to cut emissions. They do highlight a small increase in port carbon emissions, saying that this could be easily fixed by greater shore-side electrification. European ports are moving quickly to expand shore power availability in response to coming mandates.

While the environmentalists highlight the growth over the past two years, industry analyst Xeneta issued its analysis showing that CO2 emissions overall were down in the container segment in the first quarter of 2023. They reported the declines were found on 10 of the 13 top ocean freight lanes. Emily Stausbøll, Xeneta Shipping Analyst, said that much of the improvements are down to carriers reducing speeds, which delivers fuel efficiency gains while also allowing them to cater to considerably lower demand in a subdued macroeconomic climate.

Xeneta expects that the container carriers will continue to slow down the speeds of deployed ships which will also help to balance against the addition of newbuilds that were ordered over the past few years. They expect that the segment will continue to seek a balance between speed, size, and filling factor going forward which will contribute to declines in overall emissions.

Monday, February 06, 2023

The future of flight in a net-zero-carbon world: 9 scenarios, lots of sustainable biofuel

Steve Davis, Professor of Earth System Science, University of California, Irvine

Candelaria Bergero, Ph.D. Student in Earth System Science, University of California, Irvine

THE CONVERSATION Mon, February 6, 2023

Some airlines are already experimenting with sustainable aviation fuel.

Several major airlines have pledged to reach net-zero carbon emissions by midcentury to fight climate change. It’s an ambitious goal that will require an enormous ramp-up in sustainable aviation fuels, but that alone won’t be enough, our latest research shows.

The idea of jetliners running solely on fuel made from used cooking oil from restaurants or corn stalks might seem futuristic, but it’s not that far away.

Several airlines arealready experimenting with sustainable aviation fuels. These include biofuels made from agriculture residues, trees, corn and used cooking oil. Other fuels are synthetic, made by combining captured carbon from the air and green hydrogen, made with renewable energy. Often, they can go straight into existing aircraft fuel tanks that normally hold fossil jet fuel.

United Airlines, which has been using a blend of used oil or waste fat and fossil fuels on some flights from Los Angeles and Amsterdam, announced in February 2023 that it had formed a partnership with biofuel companies to power 50,000 flights a year between its Chicago and Denver hubs using ethanol-based sustainable aviation fuels by 2028.

In a new study, we examined different options for aviation to reach net-zero emissions and assessed how air travel could continue without contributing to climate change.

The bottom line: Each pathway has important trade-offs and hurdles. Replacing fossil jet fuel with sustainable aviation fuels will be crucial, but the industry will still need to invest in direct-air carbon capture and storage to offset emissions that can’t be cut. Scenarios for the future

Before the pandemic, in 2019, aviation accounted for about 3.1% of total global CO₂ emissions from fossil fuel combustion, and the number of passenger miles traveled each year was rising. If aviation emissions were a country, that would make it the sixth-largest emitter, closely following Japan.

In addition to releasing carbon emissions, burning jet fuel produces soot and water vapor, known as contrails, that contribute to warming, and these are not avoided by switching to sustainable aviation fuels.

Aviation is also one of the hardest-to-decarbonize sectors of the economy. Small electric and hydrogen-powered planes are being developed, but long-haul flights with lots of passengers are likely decades away.

We developed and analyzed nine scenarios spanning a range of projected passenger and freight demand, energy intensity and carbon intensity of aviation to explore how the industry might get to net-zero emissions by 2050. Nine scenarios illustrate how much carbon offsets would be required to reach net-zero emissions, depending on choices made about demand and energy and carbon intensity. Each starts with 2021’s emissions (1.2 gigatons of carbon dioxide equivalent). With rising demand and no improvement in carbon intensity, a large amount of carbon capture will be necessary. Less fossil fuel use and slower demand growth reduce offset needs. Candelaria Bergero

We found that as much as 19.8 exajoules of sustainable aviation fuels could be needed for the entire sector to reach net-zero CO₂ emissions. With other efficiency improvements, that could be reduced to as little as 3 exajoules. To put that into context, 3 exajoules is almost equivalent to all biofuels produced in 2019 and far surpasses the 0.005 exajoules of bio-based jet fuel produced in 2019. An exajoule is a measure of energy.

Flying less and improving airplanes’ energy efficiency, such as using more efficient “glide” landings that allow airlines to approach the airport with engines at near idle, can help reduce the amount of fuel needed. But even in our rosiest scenarios – where demand grows at 1% per year, compared to the historical average of 4% per year, and energy efficiency improves by 4% per year rather than 1% – aviation would still need about 3 exajoules of sustainable aviation fuels.

Why offsets are still necessary

A rapid expansion in biofuel sustainable aviation fuels is easier said than done. It could require as much as 1.2 million square miles (300 million hectares) of dedicated land to grow corps to turn into fuel – roughly 19% of global cropland today.

Another challenge is cost. The global average price of fossil jet fuel is about about US$3 per gallon ($0.80 per liter), while the cost to produce bio-based jet fuels is often twice as much. The cheapest, HEFA, which uses fats, oils and greases, ranges in cost from $2.95 to $8.67 per gallon ($0.78 to $2.29 per liter), but it depends on the availability of waste oil.

Fischer-Tropsch biofuels, produced by a chemical reaction that converts carbon monoxide and hydrogen into liquid hydrocarbons, range from $3.79 to $8.71 per gallon ($1 to $2.30 per liter). And synthetic fuels are from $4.92 to $17.79 per gallon ($1.30 to $4.70 per liter).

Realistically, reaching net-zero emissions will likely also rely on carbon dioxide removal.

In a future with similar airline use as today, as much as 3.4 gigatons of carbon dioxide would have to be captured from the air and locked away – pumped underground, for example – for aviation to reach net-zero. That could cost trillions of dollars.

For these offsets to be effective, the carbon removal would also have to follow a robust eligibility criteria and be effectively permanent. This is not happening today in airline offsetting programs, where airlines are mostly buying cheap, nonpermanent offsets, such as those involving forest conservation and management projects. Some caveats apply to our findings, which could increase the need for offsets even more.

Our assessment assumes sustainable aviation fuels to be net-zero carbon emissions. However, the feedstocks for these fuels currently have life-cycle emissions, including from fertilizer, farming and transportation. The American Society for Testing Materials also currently has a maximum blend limit: up to 50% sustainable fuels can be blended into conventional jet fuel for aviation in the U.S., though airlines have been testing 100% blends in Europe.

How to overcome the final hurdles

To meet the climate goals the world has set, emissions in all sectors must decrease – including aviation.

While reductions in demand would help reduce reliance on sustainable aviation fuels, it’s more likely that more and more people will fly in the future, as more people become wealthier. Efficiency improvements will help decrease the amount of energy needed to power aviation, but it won’t eliminate it.

Scaling up sustainable aviation fuel production could decrease its costs. Quotas, such as those introduced in the European Union’s “Fit for 55” plan, subsidies and tax credits, like those in the U.S. Inflation Reduction Act signed in 2022, and a carbon tax or other price on carbon, can all help achieve this.

Additionally, given the role that capturing carbon from the atmosphere will play in achieving net-zero emissions, a more robust accounting system is needed internationally to ensure that the offsets are compensating for aviation’s non-CO₂ impacts. If these hurdles are overcome, the aviation sector could achieve net-zero emissions by 2050.

This article is republished from The Conversation, an independent nonprofit news site dedicated to sharing ideas from academic experts.

While it is clear that the shipping industry is taking its first tentative steps toward decarbonization, DNV in the latest edition of its Maritime Forecast highlights significant hurdles and costs that lay ahead. The classification society points to the race to develop both the solutions aboard ships as well as more critically the need to develop the shoreside infrastructure and production to make sufficient quantities of fuel available to meet the industry’s needs.

DNV cites the changes in the orderbook and steps taken by the shipping companies as evidence that the fuel transition has already started. They calculate that only 5.5 percent of the global fleet in service today can operate on alternative fuels. However, they point out that a third of the vessels on order (based on gross tonnage) will be able to use alternative fuel sources. Currently, they point out that liquified natural gas (LNG) is the runaway leader with over 900 ships in service and another third of current orders or more than 500 ships due in the near term.

However, they predict that fossil fuels including fossil-based LNG will be in rapid decline by mid-century or phased out completely. They highlight the efforts to develop many options ranging from ammonia to methanol and methane as well as fuels produced from sustainable biomass such as bio-LNG, bio-MGO, and bio-methanol. They also point to a strong growth in electronification saying it could easily double in the future while also believing that lower sulfur fuels with carbon capture and storage will remain a part of the industry for years to come.

“The search for the best alternative carbon-neutral fuel options and technologies is underway as the entire world seeks to decarbonize,” said DNV Maritime CEO Knut Ørbeck-Nilssen. “Two thousand ships are expected to be ordered annually to 2030 but there is still no silver-bullet fuel solution available."

While there remain large uncertainties about the future price and availability of alternative fuels and which ones will emerge as the primary sources for the industry, DNV highlights that significant investments are required to achieve the accelerated adoption that is required for the industry to meet its goals. DNV forecasts that the investments for onboard technology will range from $8 to $28 billion per year (depending on which fuel type has the largest uptake) between 2022 and 2050. However, that is dwarfed by required investments for production and onshore infrastructure which DNV projects at between $30 and $90 billion per year to 2050. The total investment could reach $2.5 trillion says DNV and, of course, it will impact contribute to higher shipping costs.

To meet the challenges that lay ahead, Orbeck-Nilssen called for greater cooperation in the industry and fewer rivalries, and attempts at establishing blame among the different scenarios for future fuels. In the forecast, they focus on the ultimate hurdle of availability discussing the challenges among all the contenders for production, distribution, and bunkering.

“No industry can decarbonize in isolation so global industries need to make the right choices together, and sustainable energy should be directed to where it has the biggest impact on reducing GHG emissions,” said Orbeck-Nilssen. “The key challenge is the availability of fuels. The shipping industry cannot resolve this issue alone.”

The next few years will be critical in the industry transition. While the greatest interest continues to be ammonia and hydrogen, DNV forecasts it could be up to eight years until the onboard technologies will be available for the shipping industry. They also point to significant infrastructure and bunkering technology investments required because of the unique challenges in handling these fuels.

While much is already happening, DNV expects that the start of the IMO’s carbon intensity regulations (CII and EEXI) in 2023 will further accelerate the changes. As these rules become operational, DNV expects a significant impact on ship design and operations.