It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Monday, October 23, 2023

MONOPOLY CAPITALI$M Brazil’s J&F to invest more than $1 billion in mining assets bought from Vale Reuters | October 20, 2023 | 8:09 am Latin AmericaIron Ore Iron ore briquettes. Image: Vale.

Brazilian holding firm J&F Investimentos will invest more than $1 billion in the mining assets it bought from Vale last year, it said.

The firm, owned by the billionaire Batista family that owns the meat industry giant JBS SA, plans to boost its output in iron ore and manganese mines in Mato Grosso do Sul state in Brazil. Since taking over the mines, J&F has managed to double its 2021 production to 4 million tons of ore.

With the investment, the goal is to reach 10 million tons by the end of next year, as well as improve logistics.

EU, US could agree on critical minerals despite steel failure, says France

Ferromagnetic fluid magnetized by a neodymium magnet (Stock Image)

The European Union and the United States could reach a deal on critical minerals over the coming weeks or months despite their failure to agree an accord on steel and aluminum, French Trade Minister Olivier Becht said on Friday.

US and EU trade negotiators had hoped to agree on how to end Trump-era metals tariffs and to lessen the impact of the US Inflation Reduction Act (IRA) by Friday in time for a meeting between US President Joe Biden’s and top EU officials.

The meeting is now expected to be dominated by the crisis in the Middle East.

“It’s clearly a disappointment that we could not advance more quickly with our American friends. The discussions were intense and I hope they will restart as soon as possible,” Becht said before an EU ministers’ meeting on trade in Valencia, Spain.

He said, however, he expected there would be an agreement “in the next weeks, in the next months” so that critical minerals used in electric vehicle batteries sourced from Europe would be eligible for some of the IRA’s consumer tax breaks.

“It’s in both the interest of Europe and the United States to have this agreement,” Becht said.

The United States has suspended import tariffs on EU steel and aluminum imposed by then-President Donald Trump in 2018, but on condition both sides agree measures to address overcapacity in non-market economies such as China, and promote greener steel.

They had set an end-October deadline. Negotiators now target a deal by the end of the year.

But the sides are apart as Washington wants the EU to apply the metal tariffs to imports from China and Brussels has said it cannot not do so before a year-long investigation to comply with World Trade Organization rules.

(By Belén Carreño; Editing by Philip Blenkinsop and Barbara Lewis)

Kazakh miner ERG plans $800 million revamp of DRC copper, cobalt mine

Comide copper-cobalt mine in DRC. Credit: Eurasian Resources Group

Kazakh miner Eurasian Resources Group (ERG) plans to invest $800 million to revamp its Comide copper, cobalt mine in Democratic Republic of Congo, it said on Friday.

“The project includes the construction of a hydrometallurgical plant, an extensive exploration and drilling programme, as well as mine development,” the company said in a statement.

ERG expects the hydrometallurgical plant to be complete by the end of 2025.

The plant is designed for phased operational output, with expansion potential to produce approximately 120,000 tonnes of copper cathode and 15,000 tonnes of cobalt hydroxide annually.

(By Ashitha Shivaprasad; Editing by Daniel Wallis)

Panama’s president gives final approval to First Quantum copper mine contract

President Laurentino Cortizo had previously ordered a halt of commercial operations at Cobre Panama. (Image courtesy of Government of Panama)

Panama’s president on Friday gave final approval of a law authorizing a new long-term contract for a major copper mine following lengthy negotiations that will ultimately provide state coffers with much more revenue from the project.

The contract covers operations of a local subsidiary of Canadian miner First Quantum Minerals Ltd at the Cobre Panama mine.

The bill was overwhelmingly approved earlier on Friday by lawmakers in Congress. President Laurentino Cortizo’s approval, made official in the government’s gazette, was the last step to green-light the contract.

The new contract’s terms guarantee a minimum annual income of $375 million to Panama’s government, and will be effective for 20 years with the option to renew.

First Quantum paid $61 million in royalties in 2021.

Cortizo’s administration and the Canadian miner initially agreed on text for a renewed contract covering the Cobre Panama project in March. But approval then proved elusive, as some legislators demanded changes to some clauses.

An earlier version of the contract was modified to remove clauses such as one allowing the subsidiary to request airspace restrictions, and another that would have extended its remit beyond copper and its associated minerals to also include gold and silver.

Contract negotiations sparked local protests over the mine’s environmental and economic impacts. Several streets were closed in the Panamanian capital as hundreds of people demonstrated against the massive open-pit mine.

Felipe Argote, an economist, criticized the contract on social media, claiming First Quantum will take much more from the country economically that it contributes.

Trade and Industry Minister Federico Alfaro said the company’s remit is limited to copper and its associated minerals, but no precious metals, in an area of some 13,000 hectares.

He said the contract’s final approval will send a positive message to future investors.

(By Elida Moreno and Isabel Woodford; Editing by Kylie Madry, David Gregorio and Lincoln Feast)

How you can shape B.C.'s push to become a global supplier of critical minerals

Province seeks feedback as it aims for official strategy in early 2024

B.C.'s provincial ministry responsible for mining is looking for input on a discussion paper to guide the province as it tries to become a global supplier of critical minerals, while also respecting First Nations' rights and protecting the environment.

The Ministry of Energy, Mines and Low Carbon Innovation wants to take advantage of minerals deemed critical for technologies such as batteries, electric vehicles, wind turbines and solar panels that are hoped to help the world slow the pace of climate change.

Despite the promise, the province has not moved quickly to institute changes, or produce the strategy considering the minerals have been touted since at least 2017 by the World Bank, and others, as a necessary component of a low-carbon future.

"In British Columbia we have an opportunity to take advantage of this in a way that really feeds the world's energy transition," said Energy, Mines and Low Carbon Innovation Josie Osborne. "We're going to do it in a responsible way, a safe way and, absolutely key, in respect of First Nations."

B.C. has known deposits of critical minerals such as copper and nickel, which are shown in these core samples. (Steve Karnowski/The Associated Press)

The province has promised a strategy by early 2024 for how the industry can achieve this. Central parts of the plan will include collaboration with First Nations, in whose territories much of materials currently exist, and strict guidelines and environmental requirements for companies.

The plan is "to transform the mining sector and bring together First Nations, communities, industry … to do this work and get critical minerals out to the world in a safe, responsible way," Osborne said.

Since the 2017 provincial election, the B.C. NDP has been promising to keep mining and major industry in the province, with critical minerals becoming an enduring source of value.

B.C.'s mining industry was worth $7.3 billion to the provincial gross domestic product in 2022, which is about three per cent of the total, and more than any other natural resource sector.

Non-compliant Mineral Tenure Act

An overhaul of the province's Mineral Tenure Act, which governs, in part, how exploration can be done in the province is also needed in tandem with a critical minerals strategy.

In September, the B.C. Supreme Court ruled that the province's mining permit system does not comply with the government's duty to consult Indigenous groups and gave the province 18 months to correct it.

"We are firmly committed to implementing Mineral Tenure Act modernization, this has to be done in consultation with rights and title holders," Osborne said.

Earlier this month, the ministry published a discussion paper that lays out the critical minerals strategy framework and asks for input on six goals, which include advancing recognition and reconciliation with Indigenous Peoples, public transparency, innovation and environmental stewardship.

Anyone can submit feedback on the paper until Nov. 6 at 4 p.m. PT.

This week the province announced an advisory committee co-chaired by ministry officials and the First Nations Leadership Council tasked with providing a review this fall of work done on a draft critical mineral strategy.

A dozen experts from the sector, academia, labour and environmental organizations are on the committee.

Last December, the federal government launched its national critical minerals strategy, which has many of the same values and initiatives B.C. says will make up its own.

Critics, such as Mining Watch Canada, say that a push for critical mineral exploration in B.C. should be tempered by the disruption it can potentially cause and the risk of never finding anything or being able to extract it.

GOOD NEWS

Foreign control in the Canadian economy is shrinking: StatCan

Business competition weakening in Canada: study It's the big mergers that get the headlines

Global News

Foreign control in the Canadian economy has been steadily declining over the last decade, government data shows. According to a Statistics Canada report published Monday, the share of assets owned by foreign-controlled enterprises in Canada dropped 0.2 percentage points between 2020 and 2021, from 15.1 per cent to 14.9 per cent.

That amounts to $2.4 trillion out of a combined $15.9 trillion controlled by both Canada-based and foreign-based entities, the report stated.

The change is a result of Canadian-controlled assets growing faster than foreign-controlled assets.

Eight countries account for about 90 per cent of foreign-controlled assets in Canada, with enterprises controlled from the United States accounting for the largest share (52.3 per cent).

Entities based in Europe account for about 30 per cent of foreign-controlled assets, led by the United Kingdom.

Meanwhile, enterprises in Asia accounted for just under 15 per cent of all foreign-controlled assets in the country in 2021, with companies or persons in Japan and China controlling seven per cent and less than four per cent, respectively.

The StatCan report distinguishes between assets in the finance and insurance industries and the non-financial sector.

The share of foreign-controlled assets in the financial sector “maintained its steady downward trend and was at a 12-year low of 8.7 per cent in 2021,” the report states, while the percentage of foreign-based companies in the non-financial sector held steady at 23.5 per cent.

The report also shows foreign ownership in the non-finance sector is concentrated in wholesale trade (referring to businesses that deliver goods from producers to consumers), which accounts for 48.2 per cent of all assets in that industry.

The manufacturing sector has the next highest level of foreign-controlled assets at 44.3 per cent, followed by the oil and gas sector at 40 per cent and then Canada’s mining industry at 30 per cent.

In the finance sector, foreign-based entities continue to concentrate on credit and debt lending.

“Enterprises in these highly regulated industries are predominantly Canadian-controlled, resulting in foreign-controlled assets representing less than a tenth of the total,” the report states.

Companies based in the U.S. control about 43 per cent of assets in the financial sector, followed by the United Kingdom and Japan with about 21 per cent and 13 per cent, respectively.

Canadian mining capex reached decade high in 2022

Friday, October 20, 2023- Pro - Capital expenditure (capex) in Canada’s mining industry increased by 14% to C$13.5 billion last year, its highest in a decade, the latest figures published by Natural Resources Canada showed. The sector’s capex intentions in 2023 are also showing notable growth, rising 21% to C$16.4 billion.

The 2012 peak was driven largely by the rapid growth in demand in China and other emerging economies. Supply eventually caught up with demand, causing metal prices and spending both to decrease. Commodity prices rose again after 2016, albeit much more gradually than earlier in the decade, and mining capex also rose until 2019.

In 2020, the price of many metals dropped quickly at the beginning of the pandemic, as the associated response measures constrained global consumption. Prices later recovered and surpassed pre-pandemic levels as demand initially returned in China — the world’s top consumer — while pandemic-induced supply constraints plagued parts of the global production.

In early 2022, the prices of several metals reached record high levels after Russia invaded Ukraine. Russia is a major producer of precious, base and industrial metals, and it trades significant volumes of metals with Europe and Asia. Supply chain disruptions, economic sanctions and retaliatory measures contributed to price increases for several commodities, including palladium, nickel, aluminum and potash.

NRCan noted that the clean energy transition is anticipated to continue to be a key driver of increased demand for a host of critical minerals, particularly those used in electric vehicle batteries, such as cobalt, graphite, lithium and nickel.

On a broader scale, capex within the entire Canadian minerals sector, which also takes into account support activities for mining and downstream mineral-processing industries, grew 15% to C$17.7 billion in 2022.

Why measuring the clean energy economy is a game of catch-up

Bloomberg News | October 21, 2023 The Long Island Solar Farm (LISF), a 32-megawatt solar photovoltaic power plant built through a collaboration including BP Solar, the Long Island Power Authority, and the Department of Energy.

(Image by the Brookhaven National Laboratory, Flickr.)

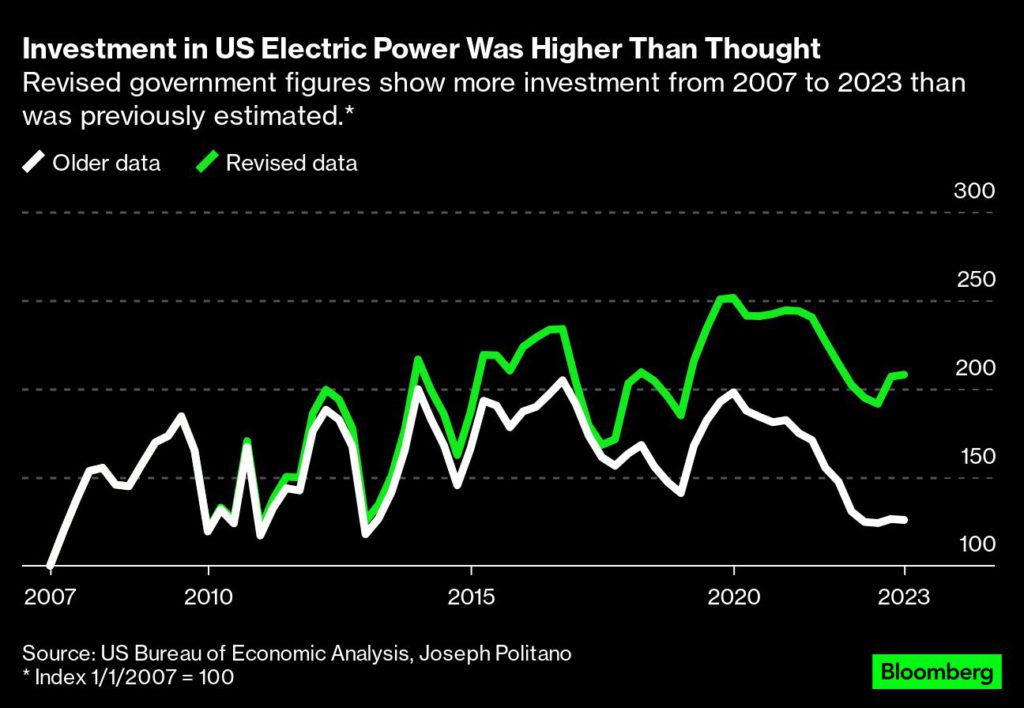

Last month, the US Bureau of Economic Analysis published its annual revision to US national accounts — key economic figures such as gross domestic product, national income and household savings rates. The upshot: The US economy is bigger than previously thought. The revised numbers show the economy grew faster than the bureau had estimated in 2017, 2018 and 2019, and shrank less in 2020.

One of the updates is particularly relevant to clean energy and climate. It is more than a data revision. It is a story about how established systems react (or don’t) to rapidly evolving signals of significant economic change. And it is a story of two sharp-eyed economists and one thoughtful institution making an effort to reflect reality at a noisy time.

The first economist is Neil Mehrotra of the Federal Reserve Bank of Minneapolis. In a thread on X, the site formerly known as Twitter, Mehrotra reflected on how, while working on the climate provisions of the Inflation Reduction Act, he came across the previous BEA data, and it showed a steadily increasing price index for “investment in electric power structures” (essentially, rising costs to build electric power generation plants or assets) from 2010 through 2023.

But as many Bloomberg Green readers will know, costs for renewable power assets have been steadily and significantly declining for almost that whole time. The big buildout of renewables means costs ought to be going down, not up.

The bureau had used a private data series called the Handy-Whitman Index for its price index. Mehrotra pointed it toward data from the US Energy Information Administration, the US Census Bureau and other sources, which showed more or less flat costs for natural gas plants and falling costs for wind and solar.

A spokeswoman for the bureau confirms that Mehrotra’s questions nudged its economists to research the topic further. “BEA is constantly looking for ways to improve our statistics, including partnering with outside researchers, data providers and data users to improve our methodology and how data are presented,” she said.

The end result should please government data aficionados: After contacting the EIA for better data on wind and solar investment, the economists arrived at a lower cost estimate for power structures — and a picture of more physical investment for the same invested dollars.

That improvement in data flows through, if in a small way, to newly revised US GDP figures.

Which brings us to the second economist. Joseph Politano is a former analyst at the US Bureau of Labor Statistics who now publishes his own economics newsletter . He found that the BEA’s downwards-revised cost estimates resulted in a 65% upward revision in the amount of real investment in the US power sector.

The revisions, Politano said, “allow official GDP data to reflect a reality we’ve known for a long time — renewables are getting cheaper and more efficient while becoming a larger share of America’s economy.”

They also exemplify the lag between any new, disruptive technology and official attempts to reckon with its impact, he noted. “Nonexistent tech can’t yet be measured by definition, so agencies are fundamentally unable to prepare for upcoming technological revolutions, and in practice they have to wait until goods gain significant market share before they can collect reliable data worthy of official endorsement,” Politano said in an email.

Or in Mehrotra’s words, “the clean energy transition and climate change will involve a host of challenges for economic measurement.” To help address that, there “can probably be a lot of useful collaboration between climate scientists, economists and statistical agencies,” he said.

New technology not only requires us to measure it as clearly and as quickly as we can. It also requires us to have a clearly articulated theory of change — how technologies themselves change, and how they change the systems into which they expand. In the case of renewables, wind and solar have experienced both exceptional growth and exceptional cost improvement, and that calls for high-frequency price indexing of their specific data.

The BEA has embraced the change. As Mehrotra said at the end of his thread, “I was impressed by the thoughtfulness and thoroughness of [bureau employees who] looked into this. Their work is incredibly important and too often overlooked or dismissed.”

Fortunately, the new assessment doesn’t overlook the reality of investment in clean power. And more generally, the BEA’s efforts provide an example of how a government agency can do its best to assist the future. Measuring the impact of new technologies, especially when those technologies are growing from a low baseline, gives investors and planners the information to better reflect not just on what is, but what could be.

(By Nathaniel Bullard)

Asset managers are updating bond models to capture a new risk

Socio-environmental catastrophe caused by the collapse of Vale’s tailings dam in Brumadinho, Brazil. CYANIDE

(Reference image by the Brazilian Institute for the Environment and Renewable Natural Resources, Wikimedia Commons.)

A growing number of asset managers is reassessing bond values tied to real assets, as a spike in the frequency of flash floods, fires and storms hits conventional pricing models.

Mitch Reznick, head of sustainable fixed income at Federated Hermes, says climate risk is a key reason why the investment manager is now underweight real estate credit. Jonathan Bailey, global head of ESG and impact investing at Neuberger Berman Group LLC, says he’s increasingly looking at whether issuers have enough capital to deal with the fallout of climate change. And analysts at Barclays Plc say nature-related risks are being mispriced across sovereign bond markets, and will ultimately trigger downgrades.

“There are often times where two otherwise very similar looking investment opportunities have very different physical risk profiles from a climate perspective,” Bailey said in an interview. A bond issuer that’s been able to protect itself from physical climate risk is likely to be the better investment over time, he said.

The credit ratings industry has yet to figure out how best to incorporate climate risk in its models, so fixed-income investors are largely having to rely on their own assessments to navigate the new landscape they face. According to the Institute for Energy Economics and Financial Analysis, bond investors can’t turn to credit ratings for a useful evaluation of environmental risks.

In a recent report, the IEEFA said that inside the biggest ratings firms, “alarm bells have been sounding for months.” But those internal warnings have gone largely unheeded, which is concerning, according to Hazel Ilango, an energy finance analyst focused on debt markets at IEEFA.

As large swaths of the planet get battered by extreme floods, droughts, storms and wildfires, failure to gradually reflect such risks in credit ratings is exposing issuers to bigger, sudden losses further down the road, the IEEFA said.

Barclays analyst Maggie O’Neal is among those to have spoken out about the potential for nature-related risks to trigger downgrades and dent portfolio values for bond investors who don’t react in time. And sovereign downgrades would in turn lead to higher borrowing costs, ultimately “compounding credit risk for bondholders,” she said in a September report.

Maria Drew, director of research for responsible investing at T. Rowe Price Group Inc., says there are big gaps in how cities and governments are preparing for the fallout from a more threatening natural environment. It’s become a “big area that the market probably just hasn’t fully factored in,” she said.

Cities and governments still need to do a lot more investing to address such risks, she said.

Bailey says Neuberger Berman is now looking at an issuer’s exposure to risks associated with natural geography, including whether they have put in place the capital spending to adapt.

A single extreme weather event “is probably not going to make the difference,” Bailey said. But over time, it adds up. And if local authorities aren’t taking timely steps to protect assets from heat waves and floods, it will likely “have an impact on property valuations, on tax receipts from local real estate,” he said.

“On a sovereign level, it may have an impact on economic growth, which will impact the ability of sovereigns to raise taxes and be able to meet their debt obligations,” Bailey said.

Reznick says Federated Hermes incorporates physical risks into internal ESG (environmental, social, governance) scores that feed into investment decisions. The asset manager is underweight the real estate sector due to climate risks and governance concerns, he said.

Climate risk also has been factored into decisions including exits and choosing between different maturities of bonds for a lower risk profile, Reznick said. Another area of mispricing he’s watching is biodiversity and natural capital risks, in sectors such as agriculture, cattle production, mining, paper and packaging, he said.

According to the IEEFA, regulators urgently need to step in and ensure that investors are getting the information they need to help them tackle the growing array of environmental risks. Without better rules, the industry is likely to remain “reactive, rather than proactive,” Ilango said.

(By Sheryl Tian Tong Lee)

Lithium company executive seeking federal backing was key figure in Alberta Energy Regulator spending scandal

Zeeshan Syed, a former Alberta Energy Regulator (AER) executive who was engulfed in a public sector spending scandal in Alberta only four years ago, welcomed two Liberal cabinet ministers to the Thunder Bay site of his junior mining company’s proposed lithium refinery last week, and is optimistic he can attract taxpayer funding for the venture.

Before joining Toronto-based Avalon, Mr. Syed worked for AER for five years as vice-president of national and international relations, one of its highest-ranking executive positions. In 2019, he was censured by Alberta’s Auditor-General, and the province’s ethics commissioner, for financial mismanagement during his tenure at AER.

The allegations included profligate spending of public-sector funds, secretly setting up a for-profit venture within the public-sector entity and working with AER chief executive Jim Ellis to make sure they both would profit from it handsomely. The side-venture, called the International Centre for Regulatory Excellence (ICORE), was disbanded about two years after it was launched. In total, approximately C$5.4 million in taxpayer money was misappropriated, investigations by public agencies concluded.

In an interview this week, Mr. Syed declined to comment on any of the specific allegations made around his time at AER. He said his focus instead was on Avalon’s “exciting” future and he would be happy to talk about that. He dismissed the AER controversy as insignificant and inconsequential.

“There was an investigation, it’s old news, the matter was resolved, and there was a finding of no wrongdoing,” Mr. Syed said. “And I refer you to the Auditor-General’s decision.”

When reached for comment by The Globe and Mail, Cheryl Schneider, executive director, engagement and communications with the Auditor-General, confirmed that there was, in fact, no decision by the AG that subsequently exonerated Mr. Syed.

Earlier this year, Mr. Syed was appointed president of Avalon Advanced Materials, a tiny mining exploration company that is attempting to both develop a lithium deposit in Ontario and build a lithium refinery in the province.

The federal government has made it a priority to strengthen Canada’s weak positioning in critical minerals. As part of that strategy, Ottawa is spending C$3.8-billion over eight years to support the industry, and it has doled out tens of millions to junior companies that are trying to build electric-battery metals infrastructure. Against that backdrop, scores of small critical-minerals companies are jockeying to attract a credibility boost in the form of a public site visit from a federal politician,which they hope will lead to funding.

Credit: Avalon Advanced Materials.

Avalon won such a credibility boost last week by attracting a visit to the site of its proposed lithium refinery by the Federal Industry Minister and Indigenous Services Minister. Both Mr. Champagne and Ms. Hajdu spoke publicly, and posed for photos, as they enthusiastically plugged Mr. Syed’s company.

“You need to bring everyone here,” Mr. Champagne told Mr. Syed in front of the television cameras. “This needs to go viral.”

Mr. Champagne also told reporters that Avalon’s proposed plant is “one of the most promising” he’s ever seen in Canada.

Ms. Hajdu also spoke highly of Avalon, telling media, “We can grow the economy and we can protect the environment together and that’s what this project represents.”

But given Mr. Syed’s checkered past at AER in such a high-profile public spending scandal, the presence of the ministers at Avalon’s site raises questions about how closely Ottawa is vetting the individuals behind small critical-minerals companies.

Richard LeBlanc, professor of law, governance and ethics at York University, said that it appears that the federal government “dropped the ball” on basic vetting standards, and evidently was not aware of Mr. Syed’s history at AER.

With not one, but two ministers showing up at Avalon’s facility, and talking positively about its future, the company earned a crucial vote of confidence from a key stakeholder.

“This is not someone grabbing your hand at a political event,” Mr. LeBlanc said. “This is something that is contemplated and staged. It’s laudatory.”

It also looks unlikely, he added, that the politicians checked the financial condition of the company, which would have revealed one that is on shaky ground.

In its most recent quarter, Avalon disclosed it is holding less than C$1-million in cash, flagged uncertainty about its ability to raise additional funds, and told investors it is a going concern risk.

Mr. LeBlanc said that neither Mr. Champagne nor Ms. Hadju can pass the buck, that due diligence should be done by the ministers, and they should be peppering their staff with tough questions about Avalon’s financials and its executive team.

“The tone is set from the top, by the ministers,” Mr. LeBlanc said. “You have to have personal accountability.”

Zeus Eden, press secretary for Ms. Hajdu, wrote in an e-mail to The Globe that seeing “as Minister Champagne was leading on the visit, we defer to his office.”

Audrey Champoux, press secretary for Mr. Champagne declined to answer whether Mr. Champagne knew about Mr. Syed’s history at AER.

In an e-mail to The Globe, he downplayed the significance of Mr. Champagne’s visit to the Avalon site. The main purpose of such visits, he said, is to learn more about new or prospective projects, as well as their effects on workers and the community.

“A presence from the minister should not be interpreted as an indication of financial support, or otherwise, for the company,” Mr. Champoux said.

Earlier in his career, Mr. Syed worked in government. From 2001 to 2003, he served as executive adviser to the director of communications for Liberal prime minister Jean Chrétien.

Mr. Syed stepped down from AER in 2019, and shortly after started working as a consultant on government affairs for Avalon. Last year, he was made an officer of the company and, in March, he was promoted to president, and has since become the public face of Avalon.

During his time at AER, the Auditor-General said that Mr. Syed ran up business travel expenses that were far and above what was deemed appropriate. One of his round-trip airfares from Calgary to Copenhagen and London cost C$8,089.

The Auditor-General’s report said that text messages between Mr. Ellis and Mr. Syed showed that many of their international trips were made under the banner of AER, but were actually to conduct ICORE business.

{kind=link}