The History of Debt Cancellation and Austerity in Europe

Rees Jeannotte [00:00:05] Hello and welcome. I’m Rees Jeannotte, and you are watching Know Your Stuff. Joining me today is economist and anthropologist Michael Hudson. He is a professor of economics at the University of Missouri, Kansas City, and an author of many books, including Killing the Host, J for Junk Economics, and his most recent “…and forgive Them their Debts”. Today, we’ll be talking with him about his latest book …and forgive them their debts, the eurozone crisis and the problem of ever-increasing rental and home ownership costs around the world. Professor Michael Hudson, thank you for joining us.

Michael Hudson [00:00:41] It’s good to be here.

Rees Jeannotte [00:00:43] How did you come to be both an economist and an anthropologist and in fact, combine the two the culmination of which is in large part at least is your latest book “…and forgive them their debts”?

Michael Hudson [00:00:55] I began as an economist on Wall Street dealing with third world debt for the Chase Manhattan Bank in the 1960s, and then by the 1970s for the United Nations Institute of Training and Research (UNITAR) writing about how the Third World was unable to pay its foreign debts to the United States and other creditors. That is, unable to pay without submitting to the IMF austerity programs, without having to sell off its raw materials and its industry and impose a permanent debt crisis on itself.

At Mexico City at a UNITAR meeting in 1979/78, I gave a speech to point out that the Third World could not pay its debts. This was four years before Mexico’s debt default. There was a riot, and I realized that the issue of debt cancelation – and the basic idea that debts chronically could not be paid – led me to want to write a history of debt cancellations and how society had handled the problem of debts growing beyond the ability to be paid. The problem is that compound interest rises steadily, compounding the debt much faster than an economy can grow.

It took about a year to write about Greece, Rome and the biblical lands. But then, while I was studying Israel, I realized that there were hints of an earlier tradition of debt cancelation in Babylonia and Sumer in Bronze Age Mesopotamia. So I began to read the literature on Sumer and Babylonia. The word “debt” almost never appeared in the index. I had to read through the whole book in order to find out about debt and its context.

I soon realized that most histories of antiquity were based on assumptions about what would happen if a modern economist – especially a Thatcherite kindred right-wing economist – would get into a time machine and go back to 3000 BC. How would they have created an economy? Of course, it would have been an economy just like Argentina or Greece. It would have gone bankrupt in a hurry and soon been conquered by the surrounding lands. Civilization wouldn’t have been able to take off from such an economy.

So I got very interested, and wrote a draft of a history of debt cancelation in Sumer and Babylonia by about 1984. A friend of mine at Harvard introduced me to the head of the anthropology department there, Carl Lamberg-Karlovsky. Anthropology included the archaeology department, and I became a research fellow in Babylonian archaeology. By the 1990s we decided that because most Assyriologists had never talked specifically about debt, we would begin to have some conferences on it. How did property and land ownership begin? How did economic rent begin? How did the economics of enterprise, interest-bearing debt and credit contracts began in Mesopotamia?

We decided on a series of three volumes, to culminate in the third volume, which to review debt cancelations in Mesopotamia. Well, I submitted the first draft to a university press and they sent it out to readers, as academic presses do. The readers replied that a debt cancellation was inconceivable, that this was a crazy book. Three decades ago it seemed inconceivable that any country, any society could have canceled the debts – because then the creditors wouldn’t lend any more money. Just about everybody believed that in the 1980s and early ‘90s.

What they did not understand was, number one, that most debts were owed to the palace. The palace had a choice when crops failed or debts mounted up: It could insist on all debts being paid. That would have reduced much of the population to bondage, in which case the palace doesn’t get any taxes or rent or labor services. The creditors would get all the crop surplus and an oligarchy would take form. In that case the local city was likely to be defeated by invaders. Or, the palace could cancel debts so as to restore economic order.

We decided to invite archaeologists and Assyriologists, and ask them to provide everything they knew from their particular period of Babylonia, Sumer, the Neo-Babylonian period and Israel. They explained how enterprise and economic techniques and profit seeking contracts began in the palatial sector of the economy. Money did not begin as barter as the free-enterprise boys say. Money was created as a means of paying taxes and fees to the palace. Basically, you had enterprise and private property beginning in the palatial sector, often with a symbiotic connection to private entrepreneurs.

Rees Jeannotte [00:06:19] The key here is that barter wasn’t the key to money or credit. That is, barter didn’t happen in the way that most people would imagine.

Michael Hudson [00:06:25] Right. The German firm Springer just published a Handbook of Money and Credit, in which I wrote the lead article on the origins of money, showing that the barter theory was made up by right-wing Austrian economists who hated governments acting in the public interest. Almost all the mainstream monetary theories are by right-wing anti-socialists claiming that government can play no positive role at all. Their conclusion is that money is best without government, and should be left to the private banks. The idea is that they would plan society better. So basically the libertarians, the free-enterprise boys, advocate a highly centralized economy – much more centralized than Soviet Russia, much more centralized than China. They want everything centralized in Wall Street or the City of London, that is, in the banks. They want the banks to be in charge of everything. They say that all this is all for the best.

So we find in antiquity, through Sumer, Babylonia, Greece and Rome, that whenever a financial oligarchy has taken power, it has created a depression – a disaster and an economic collapse. Almost all ancient historians have found this. This is what Livy and Dionysius wrote about in their histories of Rome. And Plutarch. That’s why the free-enterprise boys today in the United States have stopped teaching economic history in the economic curriculum. If you go to get an economics degree in the United States, you no longer study history. It’s out of the curriculum. You don’t even study the history of economic thought. It’s as if economics began in 1980 with Margaret Thatcher, Milton Friedman and other right wingers.

The result is a censorship about how civilization has been evolving for the last few thousand years, and how it has dealt with debt issues. I edited five big colloquia volumes for Harvard on the origins of money, privatization and land ownership, labor and economic accounting. After finishing five colloquia, I decided to write the popular summary of it all. That’s my book “… and forgive us our debts.”

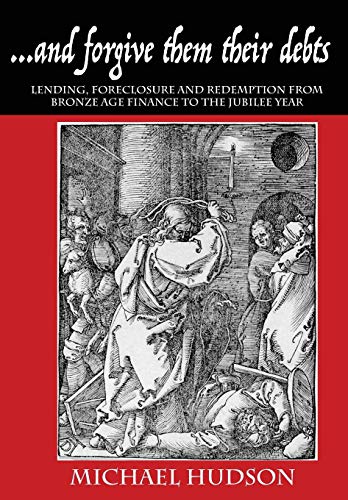

Rees Jeannotte [00:08:52] It would be interesting to know why you chose that title. The image on the cover of the book is depicts Jesus as a mercilessly whipping a moneylender or tossing him out of the temple. I can imagine photoshopping someone like Jamie Diamond’s head on top of moneylender. You know, many people would think that’s why you chose those images. Why that image and that title?

Michael Hudson [00:09:16] I don’t think that I ever have chosen the title to any of my books. I’m not very good at choosing titles. I had wanted to call the book Bronze Age Finance. But my publisher said that nobody knows what the Bronze Age means. She said that what I’ve really written about is Jesus’s first sermon. He unrolled the scroll of Isaiah and talked about the Year of our Lord, meaning the Jubilee Year, and said that he had come to proclaim that. That is the revolutionary part of my book. People think that the Lord’s Prayer is all about forgiving sins. But in the time Jesus spoke, there was a fight over the debt issue just as there was in Rome. There also were riots demanding debt cancelation in Greece and indeed a long war with Mithridates in the Near East over debt cancelation. That is what Jesus’s first sermon was about, and that is what the Lord’s Prayer was about. That is what the original Judaism had been about, before the rabbinical class, the Pharisees – basically from the wealthy creditor class – took over and subverted the older Jewish religion that Jesus came to try to revive. So my publisher thought that I should tie my book into the origins of Christianity, because we’re living in a Christian society and more people are familiar with the Lord’s Prayer, forgiving their debts than they are about Bronze Age finance.

Rees Jeannotte [00:10:54] This is where the creditor class, I guess around the time of Christ, won the battle against central power, palaces and temples, at least in the western Roman Empire. There was a paradigm shift in how to treat debt.

Exponential growth of debt at compound interest, compared to the economy’s slow S-curve

Michael Hudson [00:11:15] That makes Western civilization different from everything that went before. Earlier civilization in the Near East had an idea that the economy always tends to get out of balance, always polarizing between the rich and the poor and causing poverty and ultimately depopulation and military loss as a result of creditors enslaving their debtors. Reducing debtors to clientage or bondage in the Near East was different. They had a different economic model, a much better economic model, much more mathematically sophisticated than any model that I’ve seen in modern academia. Their model said that you have interest-bearing debt growing exponentially, doubling every five years in Mesopotamia. But the overall economy grows in an S-curve, more slowly. So again and again, you have an inherent instability. If you don’t have a central authority to keep wiping out the arrears, to keep restoring balance, then you’re going to have an unbalanced economy.

Modern economic models are based on equilibrium theory. Its mathematics are based on circular reasoning. It says that the business cycle is self-correcting – without needing any government intervention. The guiding idea is that it is impossible that people become impoverished, because there are automatic stabilizers. If you just get the government out of the way and let Wall Street run everything, everybody will be happy and prosperous. Look at the stock market.

Well, the problem is that in America, 10 percent of the population owns 80 or 85 percent of the stocks and bonds. The stock market has gone way up. Government debt has gone way up. But the income for 90 percent of the people have gone down since 2008. The minimum wage has not gone up at all. So you have the financial economy growing at the expense of the real economy of goods and services. The population is being impoverished. Yet economists say that we’re getting richer, meaning that theirclass, the financial class, is getting richer.

That is the travesty of modern economies. It’s amazing that in the Bronze Age, 3000-1200 BC. They had better models. We have the training manuals they taught the scribal students. The mathematics they used were superior to the mathematics underlying today’s mainstream right-wing models, which say debt can never be a structural problem.

Rees Jeannotte [00:13:57] In those days they had an inverted concept of moral hazard. Right. It’s been completely flipped around. So can you explain what moral hazard is, and how democratic societies really should be thinking about debt? We often think about just personal debts, or maybe someone had murdered somebody. America is a great example where you get life imprisonment. There is no redemption, it seems. How do we deal with those concepts? Should we be moving away from them?

Failure to cancel personal and other non-business debts leads to chronic depression

Michael Hudson [00:14:31] Well, the right-wing economic fashion in the United States is that of Douglass North following the Austrian school, saying that civilization progresses if there is a sanctity of contracts. A contract is a contract, and you need enforcement, even if the contract is unfair. Therefore, you must not cancel debts, because that would cheat the wealthy people who’ve made the contract to get their money, even if enforcing the debt contract means that the rest of the economy has to starve. Suicide rates go up. The economy impoverishes itself. But a contract is a contract, and that’s called progress, as if it’s Darwinian economics.

In Bronze Age antiquity, by contrast, rulers put economic balance as being the key consideration. They recognized that you have to have a palatial or civic authority come in to cancel the debt contracts. If the price of making the debtors pay these contracts –which they’re forced to sign under “Your money or your life” conditions – is to cause economic collapse, as it ultimately did in Rome. For five centuries you had economic revolts of the plebeians and the poor wanting debt cancelation. In every case the right wing, the creditors won – not by argument, but by assassinating populist political leaders. They ended up killing Caesar. Long before that, there was century after century of assassination, for instance the Gracchi brothers and a long series of other reformers, just like today.

The basis of Chicago School economics is you cannot have a free market if you’re not willing to assassinate your major critics. They went to Chile, sent in their economists who named the labor union leaders that Pinochet had to assassinate. They named the land reformers he had to assassinate, and the socialists. This started a wave of thousands of assassinations, from Chile to Argentina. That huge assassination program was sponsored by the CIA, saying this was necessary to create a free market. “We’re doing this for freedom; we’re doing this for democracy.”

But even the wealthy elites in antiquity knew that was debt causing a problem, and that the problem with society basically was caused by greed. That is what Socrates said. That’s what the Solon of Athens wrote in his poetry when he canceled the debts. It’s what Livy and all the other major Roman historians and the Stoics wrote. Nowhere in antiquity do you ever find the idea that rich people should be able to enslave and impoverish society at large.

How do we deal with that problem? A system of laws to prevent wealthy creditors from reducing the rest of the population to bondage. That was their idea of economics in a social context.

Rees Jeannotte [00:17:47] There’s lots of light-bulb moments when one reads your book. But one thing that struck me is that revolutions really only started happening in earnest when these debt cancelations stopped happening. Right? There are so many interesting things in the book. I’d like to ask you about what the modern equivalents of these ancient institutions would be – the palace and the temple.

Michael Hudson [00:18:26] What I found out, looking at Bronze Age Mesopotamia, is how different it was from modern society. I’d been known as a futurist in the 70’s, working at the Hudson Institute and The Futures Group. It’s easier to forecast the future than it is to understand the Bronze Age palaces and temples. There were three groups: a palace, the temples (basically controlled by the royal family), and the landed communities at large with their own body of common law. Hammurabi’s laws, for instance, weren’t a code. They applied to the palace sector in its relations with the rest of society. Their structure was narrower than that of common law. I found in order to explain the origin of debt and commerce, interest rates, profits and land ownership, I had to describe a society quite alien from ours. I had to go beyond the debt issue itself and talk about the broad social context.

Rees Jeannotte [00:19:45] Do we have institutions that might be similar to something like a centralized institution? I don’t know – like the central banks of today.

Michael Hudson [00:19:56] No, they only have exactly the opposite aim. Central banks work for the commercial banks and their creditors. In 1913 in America, the Federal Reserve was broken off from the Treasury in order to shift monetary management away from the Treasury in Washington to the private banks of New York City and other commercial centers. Central banks are the antithesis of ancient palaces, because they represent the creditor interests. They act as the lobbyists for the banks. You actually had a Wall Street lobbyist, Alan Greenspan, head the Federal Reserve. Their job is to bail out the banks and to make the banks solvent, even when that impoverishes their customers, even when the banks make fraudulent loans such as the junk mortgage crisis that burst in 2008. The banks were saved despite the fact that this was the largest bank fraud that been seen in American history. They were saved, and the fake fraudulent debts were imposed on the hapless mortgaged homebuyers. That resulted in a million families kicked out of their homes. The result has been that rents are going up very rapidly here. Housing prices are going up rapidly. And Americans pay so much money to financial sector for debt service – for mortgages, student loans, car loans and credit card loans – that have less and less disposable income to spend on goods and services. That’s why the American economy has been shrinking now for 12 years, since 2008. Since the Obama crisis the economy has gone down because the banks and bondholders were saved, not the economy.

Rees Jeannotte [00:21:51] This is what you call regulatory capture.

Michael Hudson [00:21:54] Yes, and not only regulatory capture of the Federal Reserve, but beyond that, the intellectual capture of society. I tried to write my book and its sequel, The Collapse of Antiquity, to provide a mind-expansion exercise to understand that if you don’t write down the debts, there’s going to be a chronic financial crisis and austerity. You’re going to end up looking like Greece or Argentina or Latvia.

Rees Jeannotte [00:22:28] This is what we’re now seeing in Greece. This is an interesting example, because the Greek crisis is still on. At the time it was all over the news. You had the situation where they were demanding that Greece pay its debts. You often say that debts can’t be paid, won’t be paid.

Michael Hudson [00:22:53] The trick was to say that Greece should pay its debts. But these debts where the debts owed to pay for crooked tax evasion. The Greek debts to foreigners were about 50 billion euros. Christine Lagarde of the IMF had a list of all the Swiss bank accounts that Greek shipowners, industrialists and financiers had illegally put their money outside of Greece into Switzerland. All the money was there. It was stolen from the tax authorities. So it wasn’t the Greek people that owed the debts. These were debts that the wealthy people owed to the tax authority but were not paid. They were tax-evasion debts. But the European Community said that the Greek people have to pay the debts that the wealthy class had crookedly avoided paying. It stood up for the crooks.

The IMF had the usual junk economics theory that Greece would be much better off and would recover once it paid. But of course it hasn’t recovered. If there’s any institution that should be abolished, it’s the IMF, which seems basically to serve as a branch of the Defense Department to keep other countries subservient to the United States. I discussed the Greek crisis in Killing the Host, which is published as Der Sektor in Germany by Klett-Cotta. I outline the Greek debt crisis, the Argentine crisis and others.

Rees Jeannotte [00:24:41] What I was trying to get at was the disingenuousness from the EU that they would say constantly repeat that Greece must pay its debts, when they must have known they could not be paid back. And as you pointed out, who had to pay them back is also a question – or who really owed the actual debts. But they must know that. So what is the real aim of doing this? I remember seeing a website reporting that they’re auctioning off Greek islands. This is the key. I think it is what the oligarchs in ancient times did too – asset grabbing.

Michael Hudson [00:25:25] Yes, that’s it. It is an asset grab. In economics you have something called revealed preference. You assume that what happens is what is intended. So you can say that what the central bankers of Germany intended was to reduce Greece’s population, to increase the suicide rate, to shorten life spans, to collapse its economy to the point where Germans could come in and insist that Greece buy expensive submarines and military hardware, and that Greece would have to sell to German investors its electric utilities and other assets. Germany made this a power grab that it had its eyes on for over 50 years, ever since it backed the colonels and the assassinations of the Greek communists after World War II.

Rees Jeannotte [00:26:18] To think about a more sensible way to deal with a debt crisis. Maybe you can use the most recent example of a national debt cancellation, namely here in Germany.

Michael Hudson [00:26:32] That’s right. The German Economic Miracle was the Allied debt reforms of 1947/48. They essentially wiped out all debts except for what employers owed their employees – you know, the workers’ wages and minimum working balances at the banks. It was easy for the Allies to cancel the debts owed to German creditors. because the creditors were mainly Nazis. The whole idea was to wipe them out. They didn’t the want to leave the former Nazis with financial power to take over the economy again. They wanted a Clean Slate.

Canceling the debts created the German Economic Miracle. Because the economy was able to operate without personal debt, and without much public debt or corporate debt. It was able to take off. Today, essentially you’re dealing with a criminalized banking class that I think we should treat in the same way that the Allies treated the Nazis. If you don’t cancel the debts owed to them, the economy is going to shrink and shrink, and polarize. We’re going to have essentially a neo-feudalism controlled by the creditor class, like you had in Rome in the Dark Ages. Do you really want a new Dark Age?

Rees Jeannotte [00:27:53] No, not particularly. This leads us into the financial crisis of 2008, where you were among the few people to predict it accurately. It was largely based on a giant private debt bubble. Private debt is something that we don’t hear much about. I tried to look for the totals on private debt worldwide. You find out the debt to GDP ratio for public debt. For government debt, but it’s never about private debt.

Michael Hudson [00:28:24] That is because the right-wing politicians want to abolish government and the social services it provides. Apart from the money governments owe for military spending and NATO, they owe pensions and health care. The right-wing program in Germany and Europe is to get rid of pensions, to lower them, to financialize and privatize the pension system instead of Germany’s pay-as-you-go system, which is quite good. They want to get rid of social spending.

Also, they look at government debt as the adversary of private debt. For instance, in the United States, President Clinton finally ran a budget surplus in the last year of his rule. What happens when a government runs a surplus? That means that it doesn’t spend money intothe economy. The economy has to rely on banks to get credit, because every economy needs credit to function and grow. Bankers realize that if the government doesn’t provide the economy with money – by spending deficits into the economy to promote employment – then people will have to borrow from the banks. But if they keep borrowing from the banks to buy homes rising in price and just to maintain their living standards, their families will end up looking like Greece or Argentina. They’re going to have to pay more of their income as interest. Bankers will end up with the houses, and with private industry. They will end up controlling everything, including the government.

For thousands of years the leading tension of civilization has been over who is going to dominate and plan society’s economy. Will it be democratic governments or wise rulers seeking stability and military security? Or, will it be a financial oligarchy that wants to get rich by impoverishing the rest of society?

The problem is that one person’s debt is another person’s savings. The situation you have today is that 10 percent of the population – the savers – are holding 90 percent of the population in debt. 90 percent in Americans are paying debt service to the top 10 percent. That is the key to today’s economic warfare. It’s not the kind of class warfare that the socialists talked about a century ago. It’s the old-fashioned financial warfare between creditors and debtors that’s been going on for thousands of years. That’s why I wrote the book to explain how this whole fight began.

Rees Jeannotte [00:31:14] So austerity obviously plays a key role here as well. It’s intimately linked with the expansion of private debt. Can you explain how that is?

Michael Hudson [00:31:23] Suppose you’re in Germany and your real estate prices are going up, while real estate prices going up. A home or an office building is worth whatever a bank will lend against it. Banks now find the way to get rich is to do what American and British banks do: Eighty percent of American and British bank credit is mortgage credit. They lend against houses, and the result is a huge inflation of real estate prices. If Germans have to pay more and more of their monthly income, either for rent or for mortgage interest or for debt service as in America, then they’re going to have less to spend on goods and services. You’re going to end up looking like New York, where the stores are going out of business. Fifth Avenue. Madison Avenue. Broadway – you go down the streets and block after block, “For Rent” signs in front of empty stores.

Rees Jeannotte [00:32:27] The same thing happening in the street that I live in in this three-block area. It’s sort of like a high-street area and boutique street. There are at least twelve shops closed. People just can’t afford the rents. We have a mayoral race coming up. One of the big topics is rental prices in Munich. It’s just everywhere the same in major cities. There’s lots of talk about capping rents for six years, and this kind of thing. But rents are too high already. You cap them at the rate they’re at, but that doesn’t make it more affordable. What should they be doing?

Michael Hudson [00:33:10] There’s a simple way to keep housing prices down: You prevent land prices from going up by doing what Adam Smith, John Stuart Mill and the whole 19th century of classical economics advocated. Land prices go up not because of enterprise, not because of population growth, but mostly because of bank credit. If you tax the increase in the land value, then the banks will not be able to lend against that. Now Germany has the lowest real estate taxes of almost any country. That’s because it has a tradition of not having a real estate class dominating society, not a Donald-Trump type economy. But if Germany begins to follow the U.S. and English pattern and you let the banks lend more and more to inflate housing prices, then you’re going to continue to shrink. Germany’s economy is beginning to shrink. I’ve seen bank reports that say that if German living standards can be lowered by 20 percent or 30 percent, German technicians and workers will have to emigrate. The German population would fall by 30 percent in 20 years. Your disposable personal incomes would have to fall by 50 percent in order to let the banks make the German real estate market look like the U.S. market.

Rees Jeannotte [00:34:45] Who was saying that?

Michael Hudson [00:34:47] The bank models predict that Germany’s population must fall, living standards must fall by 20 or 30 percent and your lifespans must shorten, your suicide rates must go up and your skilled labor must emigrate in order for your real estate market to provide the revenue to the keep banking system solvent as private-sector debt increases at today’s rates. That will make your banking system look like the American and British banking system, where eighty percent of bank credit goes into real estate. It’s a circular flow, pushing up the price of housing, causing an umbrella for rents to go up. Germany will end up looking like Greece. That is the “business as usual” economic plan. Your economic leaders of all your parties except the Linke want Germany to end up looking like Greece.. They say that that’s progress, but it’s only progress for the banking class. This is the implicit war, which somehow is not being discussed in Germany.

Rees Jeannotte [00:35:53] You often have talked about Europe as a dead zone. I’d like to know why you think it’s a dead zone. Where are we heading? What does the future look like for Europe?

Michael Hudson [00:36:05] The term “dead zone” was formulated by the U.S. Defense Secretary Donald Rumsfeld under Bush. He disparaged what he called “Old Europe.” The reason the eurozone is a dead zone is that it cannot run budget deficits of more than 3 percent. You believe that budget deficits should be avoided in order to make sure that all of the credit that the economy needs is created by banks at interest. And how do banks create this credit? They lend mainly for landlords to buy housing. Making Germans pay more rent is the new “growth area” of its economy – inflating asset prices. So the eurozone has a plan of asset-price inflation for real estate, stocks and bonds. Their prices are being supported. You’ve created about four trillion euros just to support the stock and bond markets. You could have spent this into the “real” economy, you could have made Europe into a utopia. Instead, you just used that government money to push up stock and bond prices for the 10 percent – whose economic model involves impoverishing you. That is a crazy policy to follow, because it imposes austerity.

Rees Jeannotte [00:37:16] So what’s the answer here? I’ve heard that in the United States there is some movement on public banking. Should we be looking toward something like that, democratizing the central banks?

Michael Hudson [00:37:30] You cannot democratize a central bank. They are the lobbyists for the commercial banks. You need to have the treasury take charge, appointed by democratically elected representatives, not unelected bankers. Central bankers are pretty much brainwashed. They believe that the way to make an economy prosperous is to impoverish 90 percent of the population. Instead of re-educating such people, you have to create a new institution – and the new institutions should be developed within the Treasury. But as long as you have the eurozone not permitting budget deficits of more than 3 percent – and believing that a balanced budget is an ideal – it really means letting the central banks and their clients, the commercial banks, take over and provide the economy’s money.

Commercial banks lend differently from what a public bank would do. They lend for corporate takeovers, for asset stripping and for raiding. They lend against assets. That inflates prices for real estate or for corporate raiders. Public banks can spend money into the economy to make it richer.

The German economy is shrinking. It doesn’t have to be this way, but in order to have an alternative, you have to have a different economic theory. That’s not taught in German universities. Your economic departments are very right wing. They’re looking at a parallel universe, a kind of science fiction world in which private enterprise, creditors and banks will make everybody rich, not impoverishing them by imposing financial and fiscal austerity. Academic economics is an inside out world.

Rees Jeannotte [00:39:24] You have released a German version of Killing the Host. It’s called Der Sektor. I highly recommend people go and check it out. I’ve read it twice, back to back. I found it so interesting. I would like to ask if there’s going to be a German addition of “…and forgive them their debts”.

Michael Hudson [00:39:43] Yes, it’s being translated now. It’s taken about a year to be translated in Berlin. I’m hoping that Klett-Cotta may publish it, as they did my Finance Imperium, which my Super Imperialism book. I wanted to have my own translation done by somebody who knew Assyriology instead of just turning it over to a publisher or to someone who didn’t know the Assyrian legal terms. So that should be finished in about a month or two. Then I’ll be turning it over to the publisher and it will probably take them until next year to produce it.

Rees Jeannotte [00:40:26] You also said that there will be a sequel. You mentioned it today. When can we expect that?

Michael Hudson [00:40:34] I’m just finishing it now in English, The Collapse of Antiquity. That will be published later this year, I hope. It shows that Greece and Rome collapsed because of debt. It’s part of a trilogy. The final volume will be The Tyranny of Debt, from the Middle Ages to the present. If you look at England and countries in the 12th and 13th century, you had the papacy treating the royal governments just like the IMF treats countries today. You had the protests by Matthew Paris and other English historians about how paying Peters Pence to Rome was impoverishing the country. What is happening today is part of an age-old story that happens in every era. So I want to have a whole history of debt leading up to the 20th century.

Rees Jeannotte [00:41:30] Professor Michael Hudson, thank you so much for joining us.

Michael Hudson [00:41:33] It’s been very good to be here. Thank you for having me.

[00:41:36] And thank you for watching. Please don’t forget to subscribe to our YouTube channel. Click on the bell if you’d like to receive notification when we release new material. And if you’d like what you just saw and would like to support us in our work, you can do so by way of donation. All the information on how to donate. You can find at activism.org. Thanks once again and we’ll see you next time.

No comments:

Post a Comment