NAKED CAPITALISM

The Bizarre and Widely Disparaged Fitch Downgrade of US Government Debt to AA+

The Bizarre and Widely Disparaged Fitch Downgrade of US Government Debt to AA+

Posted on August 2, 2023 by Yves Smith

Fitch shot a rocket at Treasuries that turned out to be a dud, in the form of its downgrade of US debt from AAA to AA+. This leaves Moodys alone among major rating agencies scoring Treasuries as AAA.

One might think, given all the hand-wringing about US debt, that the press and investors would be in a funk over this action. After all, when S&P threatened to downgrade Federal obligations from AAA to AA+ in 2011, business commentators, nearly all analysts, and the press spoke with one voice that this would be a meteor-wiping-out-the-dinosaurs-level event, an end of the financial universe as we knew it. Your humble blogger was virtually alone in disputing this view.1

Unlike S&P in 2011, Fitch did not broadcast its plans in advance. Even though investors and commentators seemed surprised, and the White House predictably got huffy, Mr. Market shrugged. Not only did the usual Democratic party economists like Larry Summers, Paul Krugman, and Jason Furman come out swinging on Twitter, but so to did highly respected, perceived-as-nonpartisan analysts like Mohamed El-Erian.2

Mind you, none of these arguments rely on the MMT point, that the US can always meets its Federal obligations. As a currency issuer, it cannot run out of money. It can engage in net fiscal spending (aka deficits) in excess of economic capacity and generate too much inflation.

The one way Fitch was correct is the US could make a voluntary default due to failed debt ceiling negotiations. But with the US economy showing pretty good groaf and inflation weakening (according to the Fed’s preferred measures), the idea that the US situation is worsening and therefore debt wobbles are becoming more likely is not an imminent worry.

Another way the debt critics could be correct, but it is an argument that is virtually never made, is that deficits should not be as big a worry as where the spending goes. If net fiscal spending is directed significantly to investments and programs that increase the productive capacity of the economy, like infrastructure, basic R&D in high potential sectors, education, cheaper broadband, the deficit spending will pay for itself via higher GDP growth.

Now if you want to make a case for poor US prospects, there is plenty of grist for that argument: falling US lifespans; rentierism by the health care, higher eduction, real estate, and arms sectors, which hurts productivity and competitiveness; rising partisanship; and as we and others (see Andrei Martyanov, for instance) a serious and accelerating fall in strategic and operational capability on a widespread basis.

But even with the US in decline, it is still faring better than Europe and some other areas of the world. And the elites are very good at preserving their interests even as the prospect of decline looms. Recall that even in the Dark Ages, the nobility did not fare too badly. Archeologists have found evidence they still were able to procure luxuries from around the world, like spices and fine china.

So the US sell-by date is coming but it is not imminent. That does not mean the US will not take yet more self destructive action, but the charges Fitch made largely did not stand up to scrutiny.

____

1 From an August 2011 post:

Remember Y2K? The world was gonna end because there was tons of legacy code that couldn’t accommodate the rollover to the new century. I know people in who went into survivalist mode, stocking up months of supplies, and others who took less extreme precautions, like having lots of cash on hand in case ATMs were disrupted.

As we now know, January 1, 2000 came in without major incident, since the widespread publication of this software threat to End the World as We Know It led to lots of preventive action. Perversely, the big effect of the Y2K scare was that it accelerated tech spending, since many firms bought new systems and upgraded hardware as part of their overhaul. That increased the severity of the post-bubble economic downturn….

It isn’t yet clear what the impact of the S&P downgrade of the US to AA+ will have. There are good reasons to believe, despite the media hyperventilating, that it won’t add up to much, and may perversely hit wobbly stock markets more than Treasury yields.

But there is a much bigger issue, namely S&P’s highly questionable conduct, the lack of any analytical process behind this ratings action, and the political implications.

2 For instance: Mohamed El Erian says Fitch downgrade of the US is a strange move, likely to be dismissed ForexLive.

3 Cynical and seasoned observers know that this debt/budget game of chicken is in large measure a play act and the principals won’t precipitate a default. Congresscritters if nothing else have too much in the ways of investments to be in the net worth self-harm business. However, given the way the US acting against its self-interest by escalating with China while things are not going at all well in Ukraine, it is not impossible that some ideologues down the road will get their hands on the wheel and not steer out of a crash.

Treasury yields fell, meaning investors were buying more, not fewer Treasuries at the margin, and the softening of the dollar is expected to be fleeting:

The financial press didn’t even give the story prominent billing this morning.

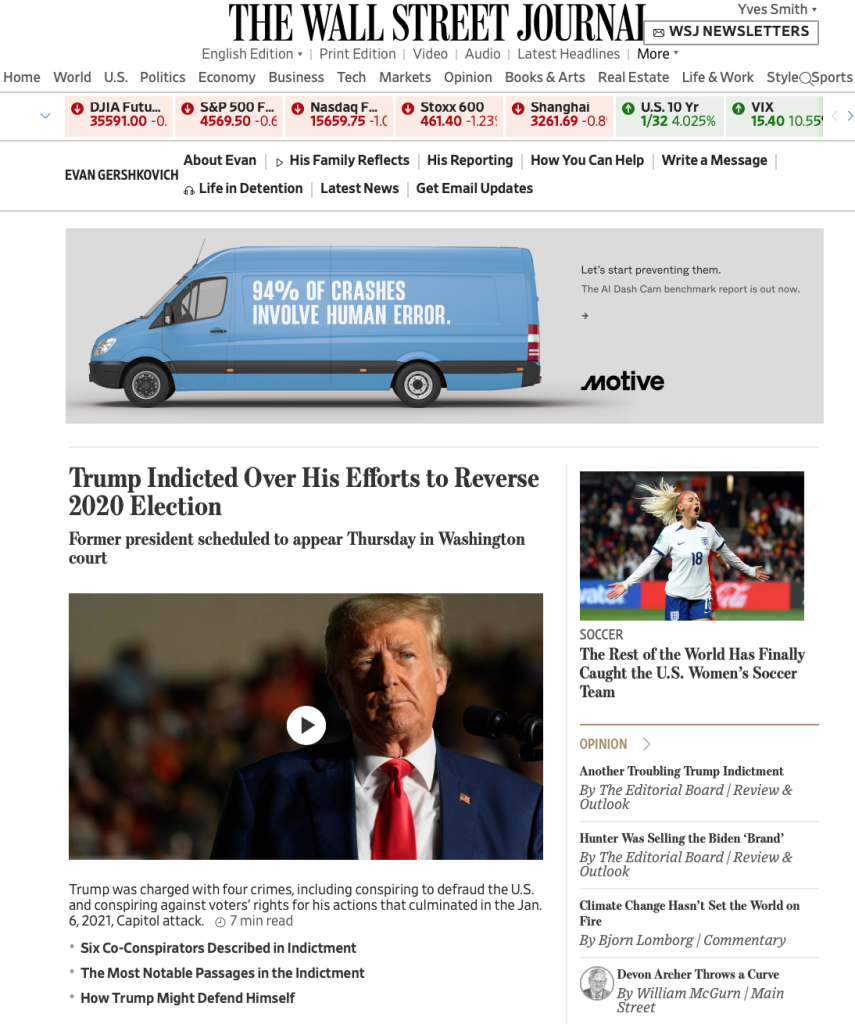

The latest Trump indictment was the hot news:

At the Wall Street Journal, the Trump story is given so much real estate that the Fitch downgrade is

below the fold (admittedly, it is the top story on the left once you scroll down):

So what exactly happened here?? As we’ll explain, one element of Fitch’s critique is correct,

that the ugly and too frequent debt ceiling and budget cliffhangers are a sign of political

dysfunction and raise the specter of a disastrous miscalculation.3

But the big reason for the collective yawn is Fitch’s economic case was weak and contradicted

But the big reason for the collective yawn is Fitch’s economic case was weak and contradicted

by recent data. We’ll turn the mike over to Twitterati as representing common views among

the economist and investor cohorts:

Note that Zandi is super orthodox and we have criticized him regularly on this site, so for him

to blow the downgrade off is telling:

And just because Jason Furman is an administration defender does not make this argument wrong:

7 COMMENTS

floraAugust 2, 2023 at 7:52 am

After the ratings agencies helped pump up the subprime market which imploded in the 2008-2009 Financial crisis, they afterward claimed their ratings were not advice but mere opinion (a free speech issue, so they could not be sued). Many people decided – fairly or not – that the rating agencies were not impartial and might be engaged in pay-to-play.

Who would benefit from this downgrade? Would it be a lever the Fed can use to justify raising rates? Inquiring minds… / ;)

Reply ↓

egAugust 2, 2023 at 9:05 am

Yeah, these sovereign debt ratings don’t seem terribly credible in a world of fiat currencies, and it’s even more bizarre to me when applied to the risk free asset against which all other assets denominated in $USD are priced.

And I’m with Yves that it’s not the right metric by which to measure US relative decline — look there to the real metrics as she outlines.

Reply ↓

chrisAugust 2, 2023 at 9:12 am

Re: Trump above the fold, it makes you wonder what is going to happen if Trump ever goes away? Do they have more headlines that they want to obscure? I can see them all now…

“Trump indicted for 50th time!” California runs out of potable water in Southern part of state, emergency declared…

“Trump brand valued at 50% less than previously, loans called in” average US worker needs 55 hours a week to earn a living wage…

“Trump smells like a fart when he talks, advisers suspicious he’s drunk all the time…” Glorious Leader Biden gets standing ovation from Congress while signing bill enshrining Freedom from Privacy act, “all those terrorists have nowhere to hide now”…

Reply ↓

NotThePilotAugust 2, 2023 at 9:17 am

This is getting into inner arcana of the finance world that I know really nothing about, but I did see this in the news. And I wondered if there’s another explanation for why Fitch did this so suddenly and everyone else is blowing it off.

Is it possible someone at Fitch was tipped off about something most of us don’t know (and that other well-connected people have to extricate themselves from more slowly)? Sort of like signaling in a game of bridge?

Otherwise, while I consistently underestimate America’s ability to memory-hole bad news and “extend & pretend”, I always get a bad feeling a hammer’s about to fall when people talk like in the one tweet by Cullen Roche.

Reply ↓

LASAugust 2, 2023 at 9:22 am

The Congressional Budget Office recently published a study of what would happen to the national debt and the economy if social security benefits were reduced by 25% in 2034. Who ever requested that study might be under pressure to slash benefits to avoid raising taxes on corporations and the well-to-do for budget balancing, even though it will likely lead to a recession in the short-term at least. As to forces at work behind the smokescreen, any or more than one large corporate/finance entity that makes regular use of Fitch might have been influential.

Reply ↓Yves SmithAugust 2, 2023 at 9:47 am

It is hard to say enough bad things about the CBO but we have tried to do our part. Some examples:

Jeff Madrick: Why the CBO Can’t Be Trusted

Jeff Madrick: CBO’s Lack of Independence Means We Need a Shadow CBO

CBO – Still Pushing Deficit Scaremongering Propaganda

Dean Baker Exposes How CBO Cooks Inflation Forecasts to Promote Deficit Scaremongering

Fed Budgetary Experts Demolish CBO Health Cost Model, the Linchpin of Budget Hysteria

And I agree completely with your suspicion that someone pressured Fitch. That could even account for the peculiar timing, that they were being arm-wrestled to get this out while the deficit fights were in progress, but some processes (vetting? editing? internal debates against being manipulated?) meant it come out late.

Reply ↓

Clint Olsen WrightAugust 2, 2023 at 10:54 am

Furman identifies in his tweet: “Factors that could, or collectively, lead to negative rating action/ downgrade”.

The second bullet point- “Structural”, and the third “Macroeconomic policy…” read as though Fitch should have considered downgrading the U.S. to BBB-.

Reply ↓

After the ratings agencies helped pump up the subprime market which imploded in the 2008-2009 Financial crisis, they afterward claimed their ratings were not advice but mere opinion (a free speech issue, so they could not be sued). Many people decided – fairly or not – that the rating agencies were not impartial and might be engaged in pay-to-play.

Who would benefit from this downgrade? Would it be a lever the Fed can use to justify raising rates? Inquiring minds… / ;)

Reply ↓

egAugust 2, 2023 at 9:05 am

Yeah, these sovereign debt ratings don’t seem terribly credible in a world of fiat currencies, and it’s even more bizarre to me when applied to the risk free asset against which all other assets denominated in $USD are priced.

And I’m with Yves that it’s not the right metric by which to measure US relative decline — look there to the real metrics as she outlines.

Reply ↓

chrisAugust 2, 2023 at 9:12 am

Re: Trump above the fold, it makes you wonder what is going to happen if Trump ever goes away? Do they have more headlines that they want to obscure? I can see them all now…

“Trump indicted for 50th time!” California runs out of potable water in Southern part of state, emergency declared…

“Trump brand valued at 50% less than previously, loans called in” average US worker needs 55 hours a week to earn a living wage…

“Trump smells like a fart when he talks, advisers suspicious he’s drunk all the time…” Glorious Leader Biden gets standing ovation from Congress while signing bill enshrining Freedom from Privacy act, “all those terrorists have nowhere to hide now”…

Reply ↓

NotThePilotAugust 2, 2023 at 9:17 am

This is getting into inner arcana of the finance world that I know really nothing about, but I did see this in the news. And I wondered if there’s another explanation for why Fitch did this so suddenly and everyone else is blowing it off.

Is it possible someone at Fitch was tipped off about something most of us don’t know (and that other well-connected people have to extricate themselves from more slowly)? Sort of like signaling in a game of bridge?

Otherwise, while I consistently underestimate America’s ability to memory-hole bad news and “extend & pretend”, I always get a bad feeling a hammer’s about to fall when people talk like in the one tweet by Cullen Roche.

Reply ↓

LASAugust 2, 2023 at 9:22 am

The Congressional Budget Office recently published a study of what would happen to the national debt and the economy if social security benefits were reduced by 25% in 2034. Who ever requested that study might be under pressure to slash benefits to avoid raising taxes on corporations and the well-to-do for budget balancing, even though it will likely lead to a recession in the short-term at least. As to forces at work behind the smokescreen, any or more than one large corporate/finance entity that makes regular use of Fitch might have been influential.

Reply ↓Yves SmithAugust 2, 2023 at 9:47 am

It is hard to say enough bad things about the CBO but we have tried to do our part. Some examples:

Jeff Madrick: Why the CBO Can’t Be Trusted

Jeff Madrick: CBO’s Lack of Independence Means We Need a Shadow CBO

CBO – Still Pushing Deficit Scaremongering Propaganda

Dean Baker Exposes How CBO Cooks Inflation Forecasts to Promote Deficit Scaremongering

Fed Budgetary Experts Demolish CBO Health Cost Model, the Linchpin of Budget Hysteria

And I agree completely with your suspicion that someone pressured Fitch. That could even account for the peculiar timing, that they were being arm-wrestled to get this out while the deficit fights were in progress, but some processes (vetting? editing? internal debates against being manipulated?) meant it come out late.

Reply ↓

Clint Olsen WrightAugust 2, 2023 at 10:54 am

Furman identifies in his tweet: “Factors that could, or collectively, lead to negative rating action/ downgrade”.

The second bullet point- “Structural”, and the third “Macroeconomic policy…” read as though Fitch should have considered downgrading the U.S. to BBB-.

Reply ↓

No comments:

Post a Comment