Electrifying Asia – where EVs are reshaping power demand and fuel use

Asia’s electric vehicle revolution is no longer simply a transport story. Across much of East and Southeast Asia it is now becoming a major electricity story, altering how power is generated, accelerating investment in renewable energy and, over time, reducing the existing demand for imported oil and LNG. The shift is uneven though.

China dominates in scale, as might be expected, while countries such as Thailand, Vietnam and Indonesia are quickly emerging as manufacturing and policy hubs. Taiwan, meanwhile, has carved out its own distinctive niche through electric scooters and battery swapping technology.

The most immediate effect of EV adoption in recent years is largely straightforward. Every battery-powered car, bus or scooter replacing an internal combustion engine reduces petrol or diesel consumption. And what replaces those fuels depends on the electricity mix in any given country. Where coal still dominates, emissions savings are smaller – for obvious reasons. Where renewables are expanding rapidly, however, electrified transport increasingly runs on solar, wind or even hydropower.

China offers the clearest and by far the world’s best example. It is the world’s largest EV market by a wide margin and has simultaneously built the world’s largest solar and wind generation capacity. Beijing is increasingly shifting energy demand away from imported crude oil and towards domestically generated electricity, according to the International Energy Agency’s (IEA) Global EV Outlook 2026 and figures from China’s own National Energy Administration (NEA). That does not eliminate fossil fuels from the system. What it does though is change where they are consumed and in turn reduces the exposure to the ever volatile oil markets.

The interaction then between EVs and renewable electricity is becoming increasingly important. Vehicle charging typically occurs overnight when cars and scooters are not being used. This helps to absorb off-peak generation, while smart charging systems increasingly encourage motorists to recharge when renewable output is abundant – and in some cases when power being supplied to homes is cheaper. In the future it has been speculated that millions of vehicle batteries could even provide grid balancing services through vehicle-to-grid technology, although commercial deployment of such remains limited, the IEA says.

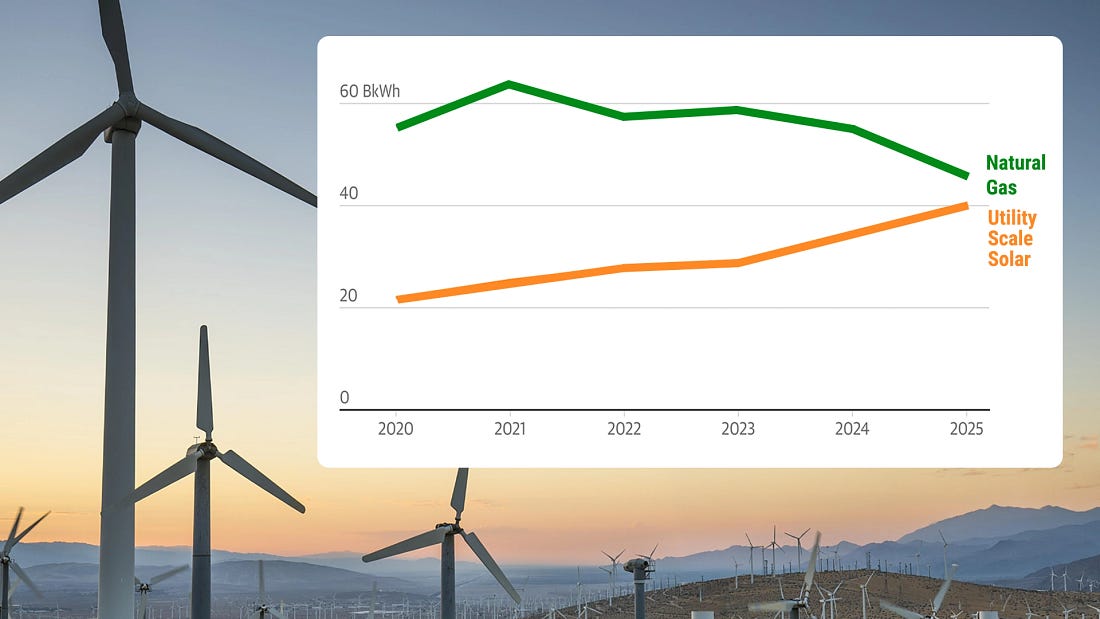

For LNG exporters, this matters – and hurts. Gas-fired generation has often been viewed as the natural partner for intermittent renewable energy because it can ramp output quickly. Yet rapid growth in battery storage in China and across Asia is beginning to challenge that assumption.

As battery costs fall – and they are, rapidly - utilities can increasingly pair solar farms with storage rather than relying solely on gas-fired peaking plants, according to BloombergNEF’s Energy Storage Market Outlook.

The IEA’s Southeast Asia Energy Outlook 2026 meanwhile, expects electricity to become the backbone of Southeast Asia’s energy system over the coming coming decades. EV sales in the region more than doubled during 2025 to about half a million vehicles, representing nearly 20% of all new vehicle sales. Electric two- and three-wheelers are expected to account for almost 60% of these sales figures by 2035.

And as electricity demand will continue rising rapidly, oil use in transport will grow much more slowly than vehicle ownership. One day it will start to drop.

Thailand has emerged as arguably Southeast Asia’s leading EV production centre. Generous incentives have attracted Chinese manufacturers including BYD, Great Wall Motor and Shanghai Automotive Industry Corporation (SAIC), alongside domestic investment in charging infrastructure. The country’s own expanding solar industry complements the transport transition, allowing an increasing share of vehicle charging to come from renewable electricity rather than imported oil, according to Thailand’s Board of Investment (BOI) and the IEA.

Vietnam is also following a similar path. Domestic manufacturer VinFast has driven rapid EV adoption across the country’s main cities of Ho Chi Minh, Hanoi and Da Nang, while the government continues expanding solar and wind capacity after one of the world’s fastest solar installation programmes. This combination is gradually shifting transport energy demand from imported fuels towards domestically generated electricity, according to the International Renewable Energy Agency (IRENA).

Indonesia to the south and Southeast Asia’s most populous nation, presents a different model. Rich in nickel reserves, it has positioned itself as a battery manufacturing hub rather than simply an EV market.

As such, Chinese and South Korean companies have invested heavily in battery plants and vehicle assembly. At the same time, Indonesia continues adding geothermal, hydropower and solar capacity, although coal still dominates electricity generation for now. As the power mix gradually decarbonises, however, the climate benefits of EVs will increase correspondingly, Indonesia’s Ministry of Energy and Mineral Resources states.

Neighbouring Malaysia and Singapore are pursuing complementary strategies. Singapore’s emphasis lies in charging infrastructure, smart grids and fleet electrification rather than vehicle manufacturing for which it simply does not have the space. Malaysia has focused on attracting investment into battery components and EV assembly as Kuala Lumpur expands solar generation through large-scale solar auctions, according to the Jakarta-based ASEAN Centre for Energy (ACE).

Taiwan, also limited in size, has taken a distinctive approach centred on two-wheel transport. Rather than prioritising electric cars, it has become synonymous with Gogoro’s battery-swapping ecosystem although there are others now trying to carve a niche for themselves. Millions of battery swaps occur every month across thousands of stations, allowing riders to exchange depleted batteries in seconds instead of waiting for charging. The model reduces range anxiety while providing a potentially valuable distributed energy asset, according to Gogoro’s annual sustainability and investor reports even if customers do complain of battery capacities, even when fully charged, gradually decreasing.

Similar battery-swapping concepts are now being explored elsewhere in Asia, including India, Indonesia and the Philippines, although none has yet matched Taiwan’s scale.

Electric scooters are particularly significant because two-wheelers dominate urban transport across much of Southeast Asia and into the South Asia region.

Indonesia, Vietnam and Thailand collectively have well over 200mn motorcycles. Even Taiwan with a population of around 24mn has 14mn registered scooters on the road.

Electrifying even a fraction of that fleet produces immediate reductions in petrol demand while requiring relatively modest battery capacity compared with passenger cars. Gogoro has reportedly sought partnerships in Indonesia, India and other regional markets to export its battery-swapping model.

And with renewable energy infrastructure increasingly following EV deployment, China remains the clear leader, manufacturing most of the world’s solar panels, batteries and EVs while continuing massive investment in wind and solar generation.

But with Vietnam an important solar manufacturing base, while Thailand and Indonesia are expanding both renewable generation and battery supply chains, these countries too increasingly see transport electrification and renewable power as parts of a single industrial strategy rather than separate sectors.

That does not mean LNG demand disappears or will, overnight. In many Asian electricity systems, gas remains the preferred flexible generation source capable of balancing intermittent solar and wind output. The IEA’s Southeast Asia Energy Outlook 2026 expects natural gas to continue playing an important role in regional power systems, particularly where coal is displaced. However, stronger renewable deployment combined with battery storage could moderate long-term LNG demand growth compared with earlier expectations. And much sooner than expected.

Oil on the other hand faces a more direct challenge. Every additional EV permanently removes future demand for petrol or diesel. While aviation, shipping and heavy industry will continue consuming hydrocarbons for decades, passenger road transport is steadily shifting towards electricity. According to the IEA’s Southeast Asia Energy Outlook 2026, EVs and biofuels in Asia and worldwide could eventually displace oil demand equivalent to a substantial share of the region’s crude imports under more ambitious policy scenarios.

To this end, and given that electrification, coupled with domestic renewable generation, offers greater energy security as well as lower emissions, the result is a structural shift in Asia’s energy landscape. Transport is becoming increasingly tied to electricity rather than oil, while electricity itself is becoming progressively cleaner. The winners are likely to be countries capable of building integrated ecosystems spanning renewable generation, batteries, charging networks and EV manufacturing.

Driving Influence: China’s EV Strategy In South Asia And Implications For India – Analysis

An XPeng electric car showroom at the Taikoo Li Sanlitun shopping center in Beijing, China. Photo Credit: Raysonho, Wikipedia Commons

s

July 29, 2026

Observer Research Foundation

This expansion creates long-term structural dependence on Chinese technology, standards, spare parts, and critical minerals, while raising security concerns over data collection from connected vehicles and potential intelligence risks.

The trend erodes India’s traditional advantages in automobile and petroleum trade with its neighbors and challenges New Delhi’s efforts to expand its own EV manufacturing and regional influence.

In April 2026, Asia became the largest buyer of Chinese electric vehicles (EVs), as Chinese exports jumped by almost 40 percent. Within this broader trend, South Asian nations – Nepal, Bangladesh, Sri Lanka, Pakistan, Bhutan and the Maldives – are emerging as important markets. Through the export of vehicles, batteries, charging infrastructure and digital ecosystems, Beijing is steadily restructuring South Asia’s technological standards. China exports not just products but complete mobility systems designed to generate long-term structural reliance that binds importing nations to Chinese manufacturers, standards and supply chains. This will have long-term implications for the region by creating dependency and security challenges, and by eroding India’s trade advantages.

China’s Domestic EV Transformation and Global Leadership

China’s dominance of the global EV industry is the outcome of three decades of sustained state-led effort. Between 2009 and 2023, China invested over US$230.8 billion in the EV industry. Government spending has been the primary driver, accounting for 60 percent of total global spending in 2025. Schemes such as purchase tax exemptions, performance-linked incentives and scrappage schemes have accelerated adoption, while large-scale investment has enabled China to account for 80 percent of the world’s installed charging capacity. In 2025, it sold 13 million electric cars, accounting for 65 percent of global EV sales, with sales projected to reach 14 million in 2026. Chinese automobile firms – BYD, SAIC, Geely, Changan, NIO and Xpeng – have emerged as major players across the world. At the centre of this ecosystem is Contemporary Amperex Technology Co., Limited, which controls 38 percent of the global lithium-ion battery supply, exemplifying how vertical integration has solidified China’s position.

China’s drive to dominate the sector is fuelled by both ambition and vulnerability. It seeks to break the historical pattern of Western and Japanese dominance in the conventional automobile sector. EVs offer a domain in which China can set standards, shape supply chains and gain a long-term technological advantage, while reducing its exposure to oil import shocks and advancing its 2060 carbon neutralitytargets. It has built a highly integrated system spanning the mining, refining and processing of key minerals, large-scale battery and component manufacturing, and software and charging infrastructure. China controls around 70 percent of global rare earth mining, 90 percent of separation and processing, and over 80 percent of lithium-ion battery manufacturing. Additionally, China has been expanding abroad because of its overcapacity and domestic price wars amid slowing demand.

Expansion of Chinese EV Ecosystem in South Asia

South Asia has emerged as an increasingly attractive destination for China’s EV industry. The West imposes high tariffs and other non-tariff barriers on the country, whereas South Asian markets offer expanding consumer bases, favourable investment conditions and policy alignment with national green transition agendas. Nepal aims for carbon neutrality by 2045, Sri Lanka targets net-zero by 2050, Bhutan emphasises sustainability via Gross National Happiness, and Bangladesh pursues 30 percent EV deployment by 2030. Furthermore, the rising cost and risk of importing fuel, along with multiple economic shocks since COVID-19, are motivating countries to embrace this transition. This creates a window for monopolistic Chinese firms to systematically exploit South Asian markets.

Chinese EVs also stand out for their competitive pricing. In Nepal, Chinese manufacturers account for the majority of new EV sales, owing to their affordable pricing. Dealers earn higher margins on Chinese vehicles than on those of other players. A mature manufacturing supply chain, lower input costs and favourable financing conditions allow China to offer the world’s lowest battery prices. Another tool of expansion is Government-to-Government assistance. For instance, in January 2026, China donated 100 electric buses to Sri Lanka for its major Colombo-Kandy and Colombo-Galle routes; similar gestures have been extended to Nepal. Such grants build familiarity and consumer appeal, while also creating dependence on Chinese spare parts and maintenance services. Recently, Sri Lanka requested Chinese assistance in building charging stations nationwide.

Chinese firms have also pursued assembly operations in the region. In Pakistan, BYD has established a facility, but operations remain limited, with no local R&D or component manufacturing. Bangladesh shows a similar pattern. Since the 2021 National Electric Mobility Action Plan was initiated, China has continued to establish distributor networks and explore battery assembly in export zones, though investments are yet to materialise. At the same time, Bangladesh’s structural dependence on Chinese capital across sectors gives Chinese firms preferential access that Asian and European competitors lack. With supply lines and local partnerships already in place, market entry is easier for Chinese firms. This also provides a way to bundle in vehicle software and connected charging networks, and to integrate them.

There has been a significant increase in both the value and the number of Chinese EV units imported into South Asia between 2019 and 2025 (as Table 1 and Graph 1 show). The year 2019 is taken as the baseline, given the noticeable shift in EV trade that year. In Nepal and Bhutan, around 90 percent and 60 percent, respectively, of vehicles imported from China are EVs. Graph 1 shows that imports have increased significantly in Sri Lanka, and moderately in Pakistan, the Maldives and Bangladesh. The demand for EVs has fuelled an increase in total imports of Chinese vehicles since 2019, with Bangladesh as an exception. Table 2 shows that Chinese EV imports dominate the EV market in the region, with Bangladesh and the Maldives being exceptions. While Japanese vehicles and two-wheelers have dominated the Maldivian market, Bangladesh, until recently, lacked a policy framework and public appetite for EVs. This is gradually changing.

Table 1. China’s Vehicle and EV Trade with South Asia

Source: Authors’ collation from UN Comtrade and official trade statistics from respective countries’ ministries. Note: *Figures are approximate and represent average estimates, as reported values vary across sources. **Total Vehicle Imports are derived from WCO HS Code 8703: Passenger vehicles (all types), whereas EV Imports are derived from HS 870380: Battery electric vehicles (pure EVs) category.

Source: Authors’ collation from UN Comtrade and official trade statistics from respective countries’ ministries. Note: *Figures are approximate and represent average estimates, as reported values vary across sources. **Total Vehicle Imports are derived from WCO HS Code 8703: Passenger vehicles (all types), whereas EV Imports are derived from HS 870380: Battery electric vehicles (pure EVs) category.Graph 1. China’s Share of EVs in Imports into South Asia

Table 2. Chinese Dominance in the South Asian EV Market

EVs as a Diplomatic Instrument and Their Strategic Implications

China’s expanding EV footprint risks creating a new form of “dependency diplomacy,” in which technological and industrial reliance translates into long-term economic influence. Sri Lanka, for example, possesses critical minerals but lacks the processing capacity to convert them into battery-grade materials. For South Asian economies, developing even parts of the full value chain requires large investment, sustained policy action and time. Furthermore, these countries depend on China for critical minerals, advanced components and chips. When batteries degrade, nations face expensive replacements or premature retirement of vehicles, owing to a lack of battery recycling capacity. Given China’s technology-transfer restrictions, assembly lines are expected to generate only logistics and retail employment. This makes it difficult for South Asian economies to develop genuine domestic manufacturing capacity.

Security concerns also persist regarding these imports. Modern, internet-enabled Chinese vehicles generate detailed location data, driving patterns and camera feeds, which are stored on cloud servers. The most advanced variants function as ‘smartphones on wheels‘, equipped with facial recognition, AI systems and over-the-air software updates. This is further complicated by China’s National Intelligence Law, which obliges individuals and companies to assist state intelligence, opening up the possibility of Chinese authorities accessing this data. In sensitive environments, this could enable the tracking of movements near ports, diplomatic sites or military installations, as well as remote interference with vehicle fleets. Such concerns have already been raised in Norway and Denmark.

The Belt and Road Initiative’s (BRI) Green Finance Agenda, which has directed US$11.8 billion into renewable infrastructure, also feeds into China’s EV expansion. Pakistan’s BYD assembly facility, linked to the China-Pakistan Economic Corridor (CPEC), illustrates how EV investments are being integrated with geopolitical objectives. Future BRI projects, especially highways, are likely to be designed with EV integration in mind. If this trajectory continues, South Asia’s transport, energy and data infrastructures will become highly vulnerable.

Finally, beyond these strategic and security challenges, Chinese dominance of the EV industry poses a significant threat to India’s trade in the region. India has traditionally been South Asia’s principal source of automobile and petroleum imports. Firms such as Tata, Mahindra, Ashok Leyland, Maruti Suzuki and TVS have built strong market positions through extensive dealer networks, joint ventures, readily available spare parts and well-established service ecosystems. As such, the growing preference for Chinese EVs is likely to affect India’s automobile and petroleum trade with all countries in the region (by 14 to 33 percent, as shown in Table 3), barring the Maldives and Pakistan.

Table 3. India’s Trade with South Asian Countries

India is accelerating its EV transition to expand manufacturing and exports, and is deploying it as a foreign policy instrument — yet the scale of this expansion remains modest compared to China’s. Between 2020 and 2025, India’s EV sector attracted around US$25 billion in investment, well short of its targets, leaving China to dominate the market. At a time when India is investing significantly in energy and oil connectivity and easing trade and transit networks for its neighbours, the surge in Chinese EVs — and their potential transit through strategic regions, especially the Northeast — could add to existing economic and security risks.

China’s EV expansion in South Asia goes beyond commerce, reflecting a broader pattern of tactical economic integration. By exporting the entire EV ecosystem and offering India’s neighbours access to finance, technology and clean transport solutions, China builds leverage over them without resorting to coercion. For South Asia, affordable Chinese EVs — combined with growing climate commitments and the need to reduce dependence on imported fossil fuels — present a new set of choices. Taken together, these dynamics suggest that South Asia’s clean transport future lies as much in the realm of geopolitics as in markets and climate policy. While geography and commercial ties continue to favour India overall, these advantages alone may not be sufficient to sustain its primacy in trade.

About the authors:

Sakshi Kapoor is a Research Intern at the Observer Research Foundation.

Source: This article was published by the Observer Research Foundation.

Disclaimer: ChatGPT 5.5 was used to generate infographics and tables.

About Observer Research Foundation

ORF was established on 5 September 1990 as a private, not for profit, ’think tank’ to influence public policy formulation. The Foundation brought together, for the first time, leading Indian economists and policymakers to present An Agenda for Economic Reforms in India. The idea was to help develop a consensus in favour of economic reforms.

View all posts by Observer Research Foundation