By Metal Miner -

US steel prices have significantly increased due to new tariffs, causing buyers to rush into the market and mills to constrain output.

Despite rising prices, concerns about long-term demand sustainability persist as the manufacturing sector shows signs of slowing growth and new orders are contracting.

The steel futures market indicates potential for a price peak, with backwardation suggesting spot prices may soon decline after the tariff-induced surge.

![]()

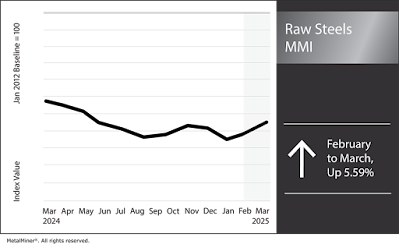

Rising steel prices saw the Raw Steels Monthly Metals Index (MMI) jump by 5.59% from February to March.

Steel Prices Surge on Tariff News

As of mid-March, steel prices remained decidedly bullish and in search of a new peak as U.S. tariffs set the market on fire. Hot rolled coil prices hit their highest level since February 2024, up over 34% since the start of the year. Meanwhile, the steel plate market, which closed last year plagued by oversupply, saw prices jump nearly 38% during the same period, a development recently covered in MetalMiner’s weekly newsletter.

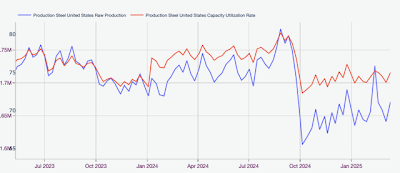

Buyers rushed back into the market ahead of tariffs, attempting to refill inventories before the duties hit steel prices. Simultaneously, service centers reported increased difficulty obtaining material from mills, which continued to capitalize on the chaos by constraining output to keep the market tight. As of March 12, American Iron and Steel Institute data showed that U.S. raw steel production remained constrained, more than 6% below its 2024 peak.

Source: MetalMiner Insights, Chart & Correlation Analysis Tool

Mill Lead Times Extend

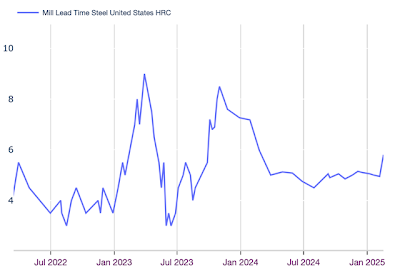

Meanwhile, mill lead times reflected the increasingly tighter market. For example, HRC mill lead times lengthened significantly, increasing back to where they stood in February 2024. It is worth noting that the current busy market contrasts sharply with where things stood at the end of last year. Suppliers faced weak conditions throughout 2024. While some attributed falling steel prices to the pressure of competitively priced imports, others noted slower demand caused by the long-term contraction of the U.S. manufacturing sector.

Source: MetalMiner Insights, Chart & Correlation Analysis Tool

Will High Prices Kill High Prices?

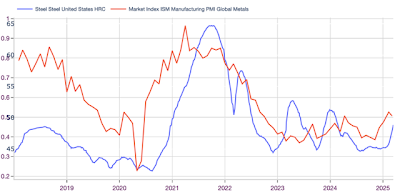

Despite what appears to be surging demand, questions remain as to how long tariffs can prop up prices. After more than a year of shrinking, the U.S. manufacturing sector only recently returned to growth over the past two months.

Source: MetalMiner Insights, Chart & Correlation Analysis Tool

However, that growth trend appeared to slow by February, with the ISM Manufacturing PMI moving from 50.9 in January to 50.3. Not surprisingly, bullish material prices helped the Prices Index jump 7.5 percentage points to 62.5. But while prices rose, the New Orders Index echoed fears of demand destruction. That index dropped 6.5 percentage points to 48.6, returning back to contraction.

Long-Term and Short-Term Outlooks

While the trend of manufacturing nearshoring will offer long-term support to the Manufacturing PMI, rising prices remain a short-term threat. Indeed, some steel suppliers expressed concern as to how long demand would last. While many buyers have already locked in volume commitments for the year, the spot-demand outlook appears increasingly murky.

Amid the sharp price increases, suppliers anticipate demand to pull back, which will likely be worsened by still-elevated interest rates. After tariffs go into effect, steel buyers appear likely to pause. This could help steel prices find a peak, as suppliers saw no meaningful change in overall market conditions outside of the tariffs.

Although few expected any relief to come in the form of carveouts and exemptions, sources noted having little confidence that U.S. demand would sustain the uptrend at its current pace. Thus far, President Trump has maintained his intentions to forgo exemptions or quotas like those implemented after he imposed Section 232 duties in 2018.

Backwardation Returns as HRC Three-Month Futures Peak

Like suppliers, investors also appear weary of the current bull trend. This comes as HRC three-month futures found a peak in late February, followed by a modest downside correction. That decline saw spot prices secure a premium over futures for the first time since April 2024.

Source: MetalMiner Insights, Chart & Correlation Analysis Tool

While futures are not always accurate in determining where spot prices will peak, they typically lead when it comes to shifts in trend. This makes them a reliable indicator when markets are on the verge of shifts. Should the recent inversion of the two price points from contango to backwardation hold, spot prices may soon follow futures into the downside. Read MetalMiner’s 2025 steel price forecast in our Monthly and Annual Metal Outlook reports.

By Nichole Bastin

Mar 18, 2025

US steel prices have significantly increased due to new tariffs, causing buyers to rush into the market and mills to constrain output.

Despite rising prices, concerns about long-term demand sustainability persist as the manufacturing sector shows signs of slowing growth and new orders are contracting.

The steel futures market indicates potential for a price peak, with backwardation suggesting spot prices may soon decline after the tariff-induced surge.

Rising steel prices saw the Raw Steels Monthly Metals Index (MMI) jump by 5.59% from February to March.

Steel Prices Surge on Tariff News

As of mid-March, steel prices remained decidedly bullish and in search of a new peak as U.S. tariffs set the market on fire. Hot rolled coil prices hit their highest level since February 2024, up over 34% since the start of the year. Meanwhile, the steel plate market, which closed last year plagued by oversupply, saw prices jump nearly 38% during the same period, a development recently covered in MetalMiner’s weekly newsletter.

Buyers rushed back into the market ahead of tariffs, attempting to refill inventories before the duties hit steel prices. Simultaneously, service centers reported increased difficulty obtaining material from mills, which continued to capitalize on the chaos by constraining output to keep the market tight. As of March 12, American Iron and Steel Institute data showed that U.S. raw steel production remained constrained, more than 6% below its 2024 peak.

Source: MetalMiner Insights, Chart & Correlation Analysis Tool

Mill Lead Times Extend

Meanwhile, mill lead times reflected the increasingly tighter market. For example, HRC mill lead times lengthened significantly, increasing back to where they stood in February 2024. It is worth noting that the current busy market contrasts sharply with where things stood at the end of last year. Suppliers faced weak conditions throughout 2024. While some attributed falling steel prices to the pressure of competitively priced imports, others noted slower demand caused by the long-term contraction of the U.S. manufacturing sector.

Source: MetalMiner Insights, Chart & Correlation Analysis Tool

Will High Prices Kill High Prices?

Despite what appears to be surging demand, questions remain as to how long tariffs can prop up prices. After more than a year of shrinking, the U.S. manufacturing sector only recently returned to growth over the past two months.

Source: MetalMiner Insights, Chart & Correlation Analysis Tool

However, that growth trend appeared to slow by February, with the ISM Manufacturing PMI moving from 50.9 in January to 50.3. Not surprisingly, bullish material prices helped the Prices Index jump 7.5 percentage points to 62.5. But while prices rose, the New Orders Index echoed fears of demand destruction. That index dropped 6.5 percentage points to 48.6, returning back to contraction.

Long-Term and Short-Term Outlooks

While the trend of manufacturing nearshoring will offer long-term support to the Manufacturing PMI, rising prices remain a short-term threat. Indeed, some steel suppliers expressed concern as to how long demand would last. While many buyers have already locked in volume commitments for the year, the spot-demand outlook appears increasingly murky.

Amid the sharp price increases, suppliers anticipate demand to pull back, which will likely be worsened by still-elevated interest rates. After tariffs go into effect, steel buyers appear likely to pause. This could help steel prices find a peak, as suppliers saw no meaningful change in overall market conditions outside of the tariffs.

Although few expected any relief to come in the form of carveouts and exemptions, sources noted having little confidence that U.S. demand would sustain the uptrend at its current pace. Thus far, President Trump has maintained his intentions to forgo exemptions or quotas like those implemented after he imposed Section 232 duties in 2018.

Backwardation Returns as HRC Three-Month Futures Peak

Like suppliers, investors also appear weary of the current bull trend. This comes as HRC three-month futures found a peak in late February, followed by a modest downside correction. That decline saw spot prices secure a premium over futures for the first time since April 2024.

Source: MetalMiner Insights, Chart & Correlation Analysis Tool

While futures are not always accurate in determining where spot prices will peak, they typically lead when it comes to shifts in trend. This makes them a reliable indicator when markets are on the verge of shifts. Should the recent inversion of the two price points from contango to backwardation hold, spot prices may soon follow futures into the downside. Read MetalMiner’s 2025 steel price forecast in our Monthly and Annual Metal Outlook reports.

By Nichole Bastin

No comments:

Post a Comment