It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Tuesday, April 08, 2025

U.S. and EU Seek to Counter Russian Nuclear Dominance

Russia's state-controlled nuclear entity, Rosatom, has captured a significant share of the global nuclear energy market, increasing its revenue and building a large portion of the world's nuclear reactors.

Russia's influence over uranium supplies, particularly through its relationships in Niger and Central Asia, gives it leverage in international diplomacy and strengthens its economic position.

The United States and European Union are now actively seeking to diversify their uranium sources and engage with Central Asian states to counter Russia's dominance in the nuclear energy sector.

Far removed from the battlefields of Ukraine, the United States, European Union and Russia are facing off on a second front in a struggle over the nuclear energy sector and control of uranium supply chains. While the war in Ukraine may have ground to a stalemate amid a halting search for a ceasefire, Russia is clearly winning the fight over nuclear energy – at least for now.

Rosatom, the Russian state-controlled nuclear entity, holds commanding field position in the decarbonized power sector, which allows the Kremlin to punch far above its geopolitical weight class and deepen key economic relationships in defiance of Western sanctions, all while filling government coffers with much-needed funds to stay in the fight in Ukraine. By some estimates, Rosatom has captured 50 percent of the global nuclear energy market, even operating in NATO member states, namely Turkey and Hungary.

Not having been subjected to Western sanctions to date, Rosatom has seen its revenues climb from about $12 billion in 2022, the year Russia unleashed its full-scale attack on Ukraine, to $18 billion last year, a 50 percent increase over two years. Today, Rosatom is building 26 of the 59 nuclear reactors currently under construction in the world, only two of which are in Russia.

Rosatom’s grip on the international market stands to grow even tighter over the near term, given its strengthening influence over supplies of uranium needed to operate reactors. A coup that made few headlines in 2023 resulted in the toppling of a pro-Western government in the African state of Niger, an outcome with major ramifications for the global uranium supply chain. Niger mines about 5 percent of global high-grade uranium ore supplies. Russia now controls those supplies, as US and French forces have withdrawn from the country. This undermines the resilience of the French nuclear sector and deepens American dependence on Russian imports of enriched uranium.

A recent article in Le Monde described Africa as a frontline between Russia and the West. If that is the case, the fight there is mainly over uranium and other critical minerals. This key fact helps to explain why Russia has worked so hard to reduce French and American influence on the continent. The loss of Niger will surely have a detrimental impact on France, the country’s former colonial overlord, which became a nuclear power in part because of its access to Niger’s uranium.

Russia’s broader outreach across the Sahel region includes security partnerships, resource deals, and propaganda campaigns, but these tools of statecraft are anchored in Russia’s proven ability to extract and refine natural resources that are critical for the development of nuclear energy. Indeed, Russia’s expansion into Africa demonstrates an unrelenting focus on controlling every part of the nuclear energy supply chain, from sourcing raw materials to constructing, maintaining, and decommissioning reactors.

The Kremlin has long maintained a dominant position over Central Asia’s uranium supplies. According to the World Nuclear Alliance, Kazakhstan is responsible for producing an estimated 43 percent of the world’s supply, while Uzbekistan produces 6.7 percent and Russia itself 5.1 percent. Kazakhstan and Uzbekistan export uranium to various countries, but Russia presently retains an ability to pressure Astana and Tashkent in ways that can potentially disrupt uranium supplies to other countries.

Russian nuclear diplomacy extends far beyond Africa and Central Asia. Thanks to its influence over uranium supply chains, Russia has found ready partners in Southeast Asia, where it trades energy for diplomatic backing. In the words of one analyst quoted in a New York Times report on ties between Russia and Myanmar, “Russia is the last diplomatic resort” for states sanctioned by the West. More than that, Russia offers its partnership to states looking for a middle ground between the US and China, as demonstrated by a recent partnership with Vietnam.

Moscow can even use its uranium-supply-chain power as leverage in its dealings with the United States. According to the US Energy Information Administration, 12 percent of uranium imports to the US flows in from Russia, in addition to 36 percent from Uzbekistan and Kazakhstan. To counter this potential vulnerability, the Trump administration adopted rules in March to boost domestic production of critical minerals, including uranium.

While the Kremlin now has the upper hand in the global rivalry over nuclear energy and associated supply chains, its longer-term dominance is far from assured. The United States and European Union now have an opportunity to claw back a share of the market in Central Asia, Russia’s backyard.

So far, nuclear energy and critical minerals have dominated Central Asia’s diplomatic agenda in 2025. Two states in the region, Kazakhstan and Uzbekistan, have formal plans in place to build at least two nuclear reactors, likely more. Discussions have also taken place on building nuclear power plants in Kyrgyzstan and Tajikistan.

Critically, regional leaders have not yet made any decisions on who will get the lucrative construction and maintenance contracts for the envisioned facilities. They have indicated a preference to strengthen the sovereignty of their respective states by diversifying investments in the nuclear energy and mining sectors. Uzbekistan, in particular, is leery of excessive Russian influence over Tashkent’s economic affairs.

US and European leaders, meanwhile, have expressed keen interest in helping Central Asian states develop nuclear power capabilities, and in the region’s rare earths. The Central Asia-EU summit that concluded April 4 spent a lot of time talking about enhancing cooperation in the mining sector.

The mutual interest is evident. Now, it is up to the United States and European Union to follow through on all their talk and come through with solid and substantial investments to recapture market share, and, ultimately, weaken Russia’s global reach. So long as Russia continues to dominate the world's nuclear energy markets, it will continue to threaten Ukraine – and the world.

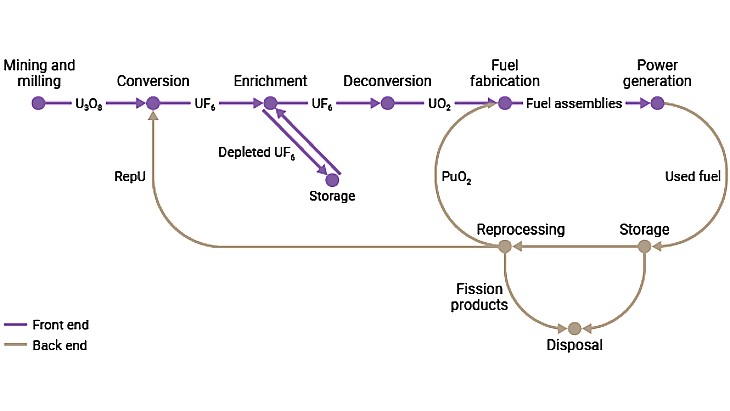

The nuclear fuel cycle is the series of industrial processes that turns uranium into electricity. Claire Maden takes a look at the steps that make up the cycle, the major players and the potential pinch-points.

Yellowcake (Image: Dean Calma/IAEA)

The nuclear fuel cycle starts with the mining of uranium ore and ends with the disposal of nuclear waste. (Ore is simply the naturally occurring material from which a mineral or minerals of economic value can be extracted).

We talk about the front end of the fuel cycle - that is, the processes needed to mine the ore, extract uranium from it, refine it, and turn it into a fuel assembly that can be loaded into a nuclear reactor - and the back end of the fuel cycle - what happens to the fuel after it's been used. If the used fuel is treated as waste, and disposed of, this is known as an "open" fuel cycle. It can also be reprocessed to recover uranium and other fissile materials which can be reused in what is known as a "closed" fuel cycle.

The World Nuclear Association's Information Library has a detailed overview of the fuel cycle here. But in a nutshell, the front end of the fuel cycle is made up of mining and milling, conversion, enrichment and fuel fabrication. Fuel then spends typically about three years inside a reactor, after which it may go into temporary storage before reprocessing, and recycling before the waste produced is disposed of - these steps are the back end of the fuel cycle.

The processes that make up the fuel cycle are carried out by companies all over the world. Some companies specialise in one particular area or service; some offer services in several areas of the fuel cycle. Some are state-owned, some are in the private sector. Underpinning all these separate offerings is the transport sector to get the materials to where they need to be - and overarching all of it is the global market for nuclear fuel and fuel cycle services.

(Image: World Nuclear Association)

How do they do it?

Let's start at the very front of the front end: uranium mining.

Depending on the type of mineralisation and the geological setting, uranium can be mined by open pit or underground mining methods, or by dissolving and recovering it via wells. This is known as in-situ recovery - ISR - or in-situ leaching, and is now the most widely used method: Kazakhstan produces more uranium than any other country, and all by in-situ methods.

Uranium mined by conventional methods is recovered at a mill where the ore is crushed, ground and then treated with sulphuric acid (or a strong alkaline solution, depending on the circumstances) to dissolve the uranium oxides, a process known as leaching.

Whether the uranium was leached in-situ or in a mill, the next stage of the process is similar for both routes: the uranium is separated by ion exchange.

Ion exchange is a method of removing dissolved uranium ions from a solution using a specially selected resin or polymer. The uranium ions bind reversibly to the resin, while impurities are washed away. The uranium is then stripped from the resin into another solution from which it is precipitated, dried and packed, usually as uranium oxide concentrate (U3O8) powder - often referred to as "yellowcake".

More than a dozen countries produce uranium, although about two thirds of world production comes from mines in three countries - Kazakhstan, Canada and Australia Namibia, Niger and Uzbekistan are also significant producers.

The next stage in the process is conversion - a chemical process to refine the U3O8 to uranium dioxide (UO2), which can then be converted into uranium hexafluoride (UF6) gas. This is the raw material for the next stage of the cycle: enrichment.

Unenriched, or natural, uranium contains about 0.7% of the fissile uranium-235 (U-235) isotope. ("Fissile" means it's capable of undergoing the fission process by which energy is produced in a nuclear reactor). The rest is the non-fissile uranium-238 isotope. Most nuclear reactors need fuel containing between 3.5% and 5% U-235. This is also known as low-enriched uranium, or LEU. Advanced reactor designs that are now being developed - and many small modular reactors - will require higher enrichments still. This material, containing between 5% and 20% U-235 - is known as high-assay low-enriched uranium, or HALEU. And some reactors - for example the Canadian-designed Candu - use natural uranium as their fuel and don’t require enrichment services. But more of that later.

Enrichment increases the concentration of the fissile isotope by passing the gaseous UF6 through gas centrifuges, in which a fast spinning rotor inside a vacuum casing makes use of the very slight difference in mass between the fissile and non-fissile isotopes to separate them. As the rotor spins, the concentration of molecules containing heavier, non-fissile, isotopes near the outer wall of the cylinder increases, with a corresponding increase in the concentration of molecules containing the lighter U-235 isotope towards the centre. World Nuclear Association’s information paper on uranium enrichment contains more details about the enrichment process and technology.

Enriched uranium is then reconverted from the fluoride to the oxide - a powder - for fabrication into nuclear fuel assemblies.

So that's the front end of the fuel cycle. Then, there is the back end: the management of the used fuel after its removal from a nuclear reactor. This might be reprocessed to recover fissile and fertile materials in order to provide fresh fuel for existing and future nuclear power plants.

In-situ recovery (in-situ leach) operations in Kazakhstan (Image: Kazatomprom)

Who, where and when

That's a pared-down look at the processes that make up the front end of the fuel cycle - the "how" of getting uranium from the ground and into the reactor. But how does that work on a global scale when much of the world's uranium is produced in countries that do not (yet) use nuclear power? And that brings us to: the market.

The players in the nuclear fuel market are the producers and suppliers (the uranium miners, converters, enrichers and fuel fabricators), the consumers of nuclear fuel (nuclear utilities, both public and privately owned), and various other participants such as agents, traders, investors, intermediaries and governments.

As well as the uranium, there is also the market for the services needed to turn it into fuel assemblies ready for loading into a power plant. And the nuclear fuel cycle's international dimension means that uranium mined in Australia, for example, may be converted in Canada, enriched in the UK and fabricated in Sweden, for a reactor in South Africa. In practice, nuclear materials are often exchanged - swapped - to avoid the need to transport materials from place to place as they go through the various processing stages in the nuclear fuel cycle.

Uranium is traded in two ways: the spot market, for which prices are reported daily, and mid- to long-term contracts, sometimes referred to as the term market. Utilities buy some uranium on the spot market - but so do players from the financial community. In recent years, such investors have been buying physical stocks of uranium for investment purposes.

Most uranium trade is via 3-15 year long-term contracts with producers selling directly to utilities at a higher price than the spot market - although prices specified in term contracts tend to be tied to the spot price at the time of delivery. And like all mineral commodity markets, the uranium market tends to be cyclical, with prices that rise and fall depending on demand and perceptions of scarcity.

The spot market in uranium is a physical market, with traders, brokers, producers and utilities acting bilaterally. Unlike many other commodities such as gold or oil, there is no formal exchange for uranium. Uranium price indicators are developed and published by a small number of private business organisations, notably UxC, LLC and Tradetech, both of which have long-running price series.

Likewise, conversion and enrichment services are bought and sold on both spot and term contracts, but fuel fabrication services are not procured in quite the same way. Fuel assemblies are specifically designed for particular types of reactors and are made to exacting standards and regulatory requirements. In the words of World Nuclear Association's flagship fuel cycle report, nuclear fuel is not a fungible commodity, but a high-tech product accompanied by specialist support.

Drums of uranium from Cameco's Key Lake mill are transported to the company's facilities at Blind River, Ontario, for further processing (Image: Cameco)

Bottlenecks and challenges

Uranium is mined and milled at many sites around the world, but the subsequent stages of the fuel cycle are carried out in a limited number of specialised facilities.

Anyone unfamiliar with the sector might wonder why all the different stages of mining, enrichment, conversion and fabrication are not done at the same location. Simply put, conversion and enrichment services tend to be centralised because of the specialised nature and the sheer scale of the plants, and also because of the international regime to prevent the risk of nuclear weapons proliferation.

Commercial conversion plants are found in Canada, China, France, Russia and the USA.

Uranium enrichment is strategically sensitive from a non-proliferation standpoint so there are strict international controls to ensure that civilian enrichment plants are not used to produce uranium of much higher enrichment levels (90% U-235 and above) that could be used in nuclear weapons. Enrichment is also very capital intensive. For these reasons, there are relatively few commercial enrichment suppliers operating a limited number of facilities worldwide.

There are three major enrichment producers at present: Orano, Rosatom, and Urenco operating large commercial enrichment plants in France, Germany, Netherlands, the UK, USA, and Russia. CNNC is a major domestic supplier in China.

So the availability of capacity, particularly in conversion and enrichment, can potentially lead to bottlenecks and challenges to the nuclear fuel supply chain. Likewise, interruptions to transport routes and geopolitical issues can also potentially impact the supply of nuclear materials. For example, current US enrichment capacity is not sufficient to fulfil all the requirements of its domestic nuclear power plants, and the USA relies on overseas enrichment services. But in 2024, US legislation was enacted banning the import of Russian-produced LEU until the end of 2040, with Russia placing tit-for-tat restrictions on exports of the material to the USA.

The fabrication of that LEU into reactor fuel is the last step in the process of turning uranium into nuclear fuel rods. Fuel rods are batched into assemblies that are specifically designed for particular types of reactors and are made to exacting standards by specialist companies. Most of the main fuel fabricators are also reactor vendors (or owned by them), and they usually supply the initial cores and early reloads for reactors built to their own designs. The World Nuclear Association information paper on Nuclear Fuel and its Fabrication gives a deeper dive into this sector.

So - that’s an introduction to the nuclear fuel cycle - and we haven't even touched on the so-called back end, which is what happens to that fuel after it has spent around three years in the reactor core generating electricity, and the ways in which used fuel could be recycled to continue providing energy for years to come.

In pictures: Akkuyu 3 conventional island equipment delivered

Monday, 7 April 2025

The first large-scale equipment - the feedwater reserve tank - has been placed within the turbine building of unit 3 at Turkey's Akkuyu nuclear power plant.

(Image: Akkuyu Nuclear)

The feedwater reserve tank is a thick-walled vessel weighing 259 tonnes and measuring more than 40 metres in length. A supply of water for the nuclear power plant feed pumps is stored in the feedwater tank during the plant commissioning and operation stages. The tank also accepts water discharged from other components of the turbine hall equipment, such as the moisture separator reheaters and the high-pressure heater.

(Image: Akkuyu Nuclear)

The large-scale dimensions of the feedwater reserve tank make it possible to transport and move the tank by lifting equipment only in parts. Two half-housings of the tank were delivered to the Akkuyu plant construction site and transported to the installation site. The assembly will be completed after the equipment is installed on the supports provided by the project.

(Image: Akkuyu Nuclear)

The feedwater reserve tank, which is an important component of the turbine heat exchange equipment, was transported to the turbine building on an automatic wheeled platform. Then workers moved the tank to the turbine maintenance level using a self-propelled crawler crane with a lifting capacity of 1300 tonnes.

"We are gradually preparing the turbine hall of Akkuyu NPP unit 3 for the installation of the turbine plant main equipment," said Akkuyu Nuclear JSC CEO Sergei Butckikh. "The main technological elevation of the building located at a height of 18.2 metres from ground level is ready to withstand heavy equipment loads, so the feedwater tank was transported to the turbine hall immediately after unloading at the Eastern cargo terminal and completing the necessary customs procedures. After installing the special supports, the specialists will move it to its design location and weld the two parts of the body."

(Image: Akkuyu Nuclear)

The Akkuyu plant, in the southern Mersin province, is Turkey's first nuclear power plant. Rosatom is building four VVER-1200 reactors, under a so-called BOO (build-own-operate) model. Construction of the first unit began in 2018. The 4800 MWe plant is expected to meet about 10% of Turkey's electricity needs, with the aim that all four units will be operational by the end of 2028.

The feedwater reserve tank - manufactured by ZiO–Podolsk Plant, part of Rosatom's Machine Building Division - is designed to be operational for the entire life cycle of the VVER-1200 reactor power units.

Fourth steam generator for new Kaiga units completed

Monday, 7 April 2025

Indian engineering company Larsen & Toubro has dispatched the fourth of eight steam generators intended for units 5 and 6 at the Kaiga nuclear power plant in Karnataka State.

(Image: L&T)

With the dispatch of the component - about 24 metres in length, with a diameter of about 4 metres and weighing more than 200 tonnes - from its A M Naik Heavy Engineering Complex in Hazira, Gujarat, Larsen & Toubro (L&T) said it has now "completed the delivery of a set of four steam generators (SGs) for one unit for the indigenously developed 10x700 MWe Pressurised Heavy Water Reactor Fleet Programme".

Steam generators are heat exchangers used to convert water into steam from heat produced in a nuclear reactor core. In PHWRs, the coolant is pumped, at high pressure to prevent boiling, from the reactor coolant pump, through the nuclear reactor core, and through the tube side of the steam generators before returning to the pump.

The previous three steam generators for Kaiga 5 and 6 were delivered to the construction site between August 2024 and early February this year.

"The fourth SG has been dispatched nine months ahead of the contractual schedule, while the full set of four SGs has been delivered in 45 months," L&T noted. "Setting a global benchmark, the first of the lot was delivered in just 33 months."

Anil V Parab, director and senior executive vice president at Heavy Engineering and L&T Valves, said: "L&T Heavy Engineering's nuclear team continues to be the industry trend-setter. Our large talent pool, trained in robust nuclear quality culture, ensures consistent first-time-right execution and globally benchmarked deliveries. This accomplishment is in alignment with the Honourable PM's Viksit Bharat 2047 vision of achieving at least 100 GWe nuclear power generation."

Kaiga 5 and 6 will be the first of ten Indian-designed 700 MWe pressurised heavy water reactors (PHWRs) to be built using a fleet mode of construction to bring economies of scale as well as maximising efficiency, which have been given administrative approval and financial sanction by the Indian government. Excavation works for the units began in May 2022.

Two 700 MWe PHWR units have already been built at Kakrapar, in Gujurat, and are already in commercial operation, while another, Rajasthan unit 7, was connected to the grid last month and is expected to begin commercial operation later this year.

Deep Fission, Deep Isolation ink MoU

Monday, 7 April 2025

Under the memorandum of understanding, the partnership will explore the management of used fuel from Deep Fission's advanced underground reactors using Deep Isolation's patented underground disposal technology.

Deep Isolation CEO Baltzer (left) and Deep Fission CEO Muller (Image: Deep Isolation)

The partnership aims to enable Deep Fission to offer an end-to-end solution that includes both energy generation and long-term waste management, the companies said.

Deep Fission will integrate Deep Isolation's deep borehole repository technology into its operations, providing a "seamless, long-term waste solution", they added. For the USA, it also provides a "promising storage option while efforts toward a long-term repository continue". "Nuclear power generation requires a waste disposal solution, and responsible users should plan for waste management from the start," said Deep Fission co-founder and CEO Elizabeth Muller, who is also the co-founder, former CEO and current chairman of Deep Isolation. "Deep geological disposal is the globally preferred approach, and while other countries are advancing underground repositories, there is an opportunity for the US to take further steps in this direction. Deep Isolation's solution presents an attractive option for Deep Fission as we work toward a sustainable nuclear future."

California-based nuclear startup company Deep Fission announced its emergence from stealth mode last August. It aims to locate 15 MWe pressurised water reactors (PWRs) about one mile (1.6 km) underground in a 30-inch borehole. The heat is transferred to a steam generator at depth to boil water, and the non-radioactive steam rises rapidly to the surface where a standard steam turbine converts the energy to its electricity. The company envisages deploying the reactors in scalable arrays, allowing customers to order multiple reactors in discreet bespoke configurations to meet diverse end-user needs.

Deep Isolation is working to leverage proven drilling practices to manage nuclear fuel and radioactive waste by encapsulating it in corrosion-resistant canisters placed within deep boreholes in suitable isolated rock formations, some 1-3 kilometres below ground. The California-based company has some 70 patents issued to date. Earlier this year, it announced the manufacture of a first-of-its-kind disposal canister prototype in a collaboration with the UK Advanced Manufacturing Research Centre, NAC International, Inc, and the University of Sheffield.

"Deep Isolation is proud to partner with Deep Fission to deliver a practical, scalable solution for managing nuclear waste," said Deep Isolation CEO Rod Baltzer. "As new nuclear technologies emerge, a forward-thinking approach to waste disposal is critical. Ensuring that nuclear waste has a reliable and permanent disposal method is essential for the industry's long-term success."

_88592.jpg)

_78020.jpg)

No comments:

Post a Comment