National News | February 5, 2020 by Brittany Hobson

Members of a peace camp opposing the development of a silica sand mine project in Manitoba are celebrating a “small victory” after the company in charge of the project announced it has been delayed due to financial reasons.

“It was a relief. I figured at least we’re going to have some more time to educate more people,” Marcel Hardisty, one of the camp organizers, told APTN News by phone Wednesday.

Hardisty is part of a group from Hollow Water First Nation, located approximately 200 km northeast of Winnipeg, who set up Camp Morningstar last winter after exploration began on the project.

The group had concerns about the environmental impacts on the community including the destruction of a community trap line.

Canadian Premium Sand Inc. (CPS) is in charge of the project called Wanipigow Sand, which was approved last year to develop an industrial plant to extract silica sand from Hollow Water and the neighbouring communities of Seymourville and Manigotagan.

The project was slated to begin production last year but CPS now expects to begin production in early 2022.

The company had to start from scratch after the original design for the plant was deemed too costly.

“This set us back. We lost a year,” said Glenn Leroux, president and chief executive officer for CPS.

The company expected the project to cost $120 million but the old design came with a price tag of $220 million.

Leroux says the group is lining up investors and financing this year with the hopes of beginning construction next year.

“We spent the last several months going back into the project basically with a white sheet of paper so we had all the approvals and everything in place, and still have those in place, but if you can’t get the money, you can’t get the project,” he said.

“It’s hard to raise money if you’re connected to the oil and gas business because the oil and gas business is in a downturn and it’s under fire from every single environmentalist on the planet.”

Leroux believes the delay will not affect the final outcome of the project.

The Manitoba government approved the environmental licence necessary for the project in May 2019.

The company may have to apply for an extension as well as make changes to their environmental licence based off the new plant design.

This could result in new consultations processes because of the change.

However, part of the reason Camp Morningstar was created was because the group didn’t believe a proper consultation took place.

“It was show and tell by the company to gain support,” said Hardisty.

Hollow Water chief and council along with CPS hosted meetings with men, women, youth and elder groups.

Community leadership is in favour of the project.

Chief Larry Barker told APTN last year the industry would bring much needed jobs to his community.

Hardisty says in the meantime Camp Morningstar will remain up and running for educational purposes.

“We’re not shutting it down,” he said.

“We may have an international Sundance, for sure a land-based learning centre for young people to learn about the environment to learn about what’s in this forest, what’s beneath the silica sand.”

Camp Morningstar will be hosting a celebration for it’s one-year anniversary on Feb 15.

Brittany Hobson

Opinion Analysis

Frac-sand project faces major hurdles, competition

By: Don Sullivan Posted: 12/11/2019

Artist’s rendering of the planned Canadian Premium Sand facility at Hollow Water.

The problem facing Canadian Premium Sand (CPS) is that it needs to overcome some big internal hurdles, and if successful, then face stiff competition from existing frac-sand operations should it succeeds in getting its mine fully operational near Hollow Water First Nation.

Northern White Sand (NWS), the gold standard in frac sand, is mined mostly in Wisconsin, and like many frac-sand operators is an end-to-end user-integrated operation.

The term "end-to-end user-integrated operations" means these operations in Wisconsin have long established large-volume contracts for their frac sand with various oil and gas fracking operations in all of the major oil and gas fields throughout North America, including Canada.

These Wisconsin frac-sand companies, in addition to owning the frac-sand mines and processing facilities, also tend to own or have a financial stake in all of the necessary on- and off-loading transportation infrastructure to move their frac sand as close as possible to their markets, such as the rail transload facilities needed to load and unload their frac sand.

In addition, these Wisconsin companies have long-term contracts with major rail companies, such as CN and CP, to pick up and deliver their frac sand to their rail transload facilities located near their markets, they then contract out last-mile truck services to deliver their frac sand to the wellhead.

These highly integrated operations are designed to deliver frac sand to their markets at the lowest price possible. Many of these frac-sand companies in Wisconsin have been doing this for a decade or more, and are able to undercut freight on board (FOB) prices for their frac sand when a new startup operation, such as Canadian Premium Sand, wants to enter the market.

In short, these Wisconsin frac-sand operations have captured nearly 70 per cent of the North American market by offering a superior product and by being fully integrated end-to-end user frac-sand operations.

However, given the downturn in oil and gas prices, and the need for oil and gas fracking operations to reduce their costs, all these operations are now looking to acquire frac sand that is situated much closer to where they operate in the major North American oil and gas fields. This is what is precisely occurring now, both in Canada and the U.S., and this drive to find "in-basin frac sand deposits" has created an oversupply of frac sand, which in turn has further reduced the market and price for NWS.

For CPS, the closest markets, should they become operational, would be Bakken oil and gas fields located in Saskatchewan, North Dakota, Montana and a small part of southwestern Manitoba.

Given the distance between CPS’s proposed frac-sand mine and a major rail transportation hub — almost 200 km away in Winnipeg — and with no frac-sand transload facilities currently located in Winnipeg (and with the possibility of no processing facility to be constructed at its frac-sand mine site location as part of their as-yet-incomplete cost-optimization measures), these will be some major hurdles that CPS will need to overcome, first and foremost, to even get in the game.

CPS will also need to secure frac-sand contracts beforehand from fracking operations in North America’s oil and gas fields, then secure offload rail transload facilities located near their potential markets. CPS will have to do all this at a very competitive price against frac-sand operations in Wisconsin that are currently operating in these areas and which have a huge cost-savings advantage over CPS, precisely because they are fully integrated operations.

No doubt, CPS is trying to figure out how to overcome these many hurdles as it prepares its cost-optimization report, but it is fairly evident that CPS will need to radically alter its original plans, for which it has already received government of Manitoba approval.

Don Sullivan is a landscape photographer, former director of the Boreal Forest Network and served as special adviser to the government of Manitoba on the Pimachiowin Aki UNESCO World Heritage site portfolio. He is a research affiliate with the Canadian Centre for Policy Alternatives Manitoba and a Queen Golden Jubilee medal recipient.

Fast Facts: Canadian Premium Sand Frac Sand Mining Project About to Hit a Financial Wall

AUTHOR(S):

Don Sullivan

SEPTEMBER 17, 2019

There are important new developments regarding the proposed frac sand operation adjacent to Hollow Water First Nation on the east side of Lake Winnipeg that will have a large impact on the entire project.

Canadian Premium Sand (CPS), a publicly traded and Canadian-owned mining company, received an Environmental License from the Government of Manitoba in early 2019, which allowed CPS to proceed with the construction phase of a frac sand processing facility and the mining of 1 million tons per year of frac sand on a designated community trap line adjacent to Hollow Water First Nation.

The processed frac sand would then be transported by trucks, from the mine location to Winnipeg, where it would be transferred to rail to be used in fracking operations for the oil and gas industry throughout North America.

CPS estimates that the capital cost of getting this project up and running would be around $300 - $335 million, and the project would require approximately an additional $29 million per year in operating costs thereafter.

In addition, CPS has yet to estimate the unforeseen costs as a result of having to meet the 98 conditions in the Environmental License they received from the government of Manitoba. These costs are substantial but unknown.

In a 2018 Investors Presentation, CPS based the economic viability and profit margins of its entire frac sand project on selling the frac sand they produced at between $150 a ton (low end) and $250 a ton (high end). The problem for CPS is that, based on the most recent market analysis done by a number of market research firms, frac sand is now selling for less than $30 a ton in North America.

Moody’s, one of the largest bond rating agencies, has stated that the market price for frac sand will not change in the foreseeable future as there is a large over supply of frac sand in the North American market which is driving down prices. At this price CPS cannot even cover of its annual operating costs of $30 million, let alone begin paying down the start-up cost of $300 - $335 million associated with getting the whole project up and running.

Obviously CPS has seen the writing on the wall as they have not made a Final Investment Decision to proceed with construction phase of the project and recently announced they were undertaking a Cost Optimization Study to reduce their total expenditures related to the project. This study is to be completed by September of 2019.

Some insight as to where CPS is headed with this Cost Optimization Study was obtained recently from local community members in Hollow Water First Nation, where there was an information meeting held with a select few people in the first week of September. At this information meeting it was learned that CPS is now toying with the idea of barging wet unprocessed sand to Gimli, on the west side of Lake Winnipeg, where an operating rail line exists.

If this new plan proves to be accurate, then this would be an entirely new project, and one that is radically different from what CPS proposed to the government of Manitoba back in early 2019, and for which CPS received an Environmental License for.

It would also mean that the 127 jobs that CPS stated would be created in the region would disappear, as they would not be constructing a processing facility at the proposed mine location, nor would they be transporting processed frac sand via truck from the mine site to market.

In short, it would be my understanding that CPS would need to submit a whole new Environmental Act Proposal, and obtain a new Environmental License from the government of Manitoba, as this new plan is far more than just an alteration to the company’s existing Environmental License.

Further, there would be far more federal government oversight required should CPS choose to barge unprocessed frac sand via Lake Winnipeg to Gimli, as this body of water is federally designated navigable waters. The Department of Transportation would also need to approve the barges needed to ship this unprocessed frac sand to Gimli. The Coast Guard I am sure would have some regulatory interest, as well as the federal Department of Fisheries and Oceans.

Finally, there are a whole host of new potential adverse impacts that would need to be identified and addressed before CPS could move forward with this new plan. At the end of the day, CPS is unlikely to be able to reduce their costs to the level needed to make a profit, given the current low market price for frac sand, even if this new plan were to be in place and approved.

Clearly, CPS has some very tough decisions to make in the months ahead.

Sources of Information

Canadian Premium Sand Environmental Act Proposal Canadian Premium Sand NI 43-101 Technical Report – May, 2019

Environment Act Licence No. 3285 – May 6, 2019 Claim Post Resources Inc. Investor Presentation – March 2018

Forbes - Shale Bonanza Subsiding For U.S. Frac Sand Miners As Low Prices Bite - Gaurav Sharma – May 29, 2019

Canadian Premium Sand News Release – July 18, 2019

ATTACHED DOCUMENTS:

Canadian_Frac_Sand_About_to_Hit_financial_Wall.pdf

385.92 KB

by Don Sullivan

November 22, 2018 | Manitoba Offic

by Michael Bradfield

October 27, 2014 | Nova Scotia Office

INTEREST IN THE MANIGOTAGAN DEPOSIT

Silica Frac Sand

Gossan holds a significant royalty on a high-quality frac sand deposit, owned and operated by Canadian Premium Sand Inc. (TSX.V:CPS), known as the Seymourville Frac Sand Project. Canadian Premium Sand is currently in the process of developing this permitted project into production in the near-term.

Under the terms of the royalty agreement, semi-annual advance royalty payments of $50,000 each are payable as of June 18th and December 18th of each year. All frac sand produced, sold and paid from the nine Manigotagan leases (formerly held by Gossan) is subject to a $1.00 per tonne production royalty payable quarterly and all other products are subject to a $0.50 per tonne production royalty. Although the royalty is solely payable on production from the Manigotagan leases, the agreement also provides for a minimum production royalty from both the Manigotagan and the adjacent Seymourville properties held by Canadian Premium Sand, based on their relative mining reserves of frac sand at the time of permitting. Canadian Premium Sand can acquire one-half of Gossan’s production royalty interest for $1.5 million during the three years after commencing commercial production and $2 million for a further two years.

On June 12, 2019, Canadian Premium Sand announced the results of a new Preliminary Feasibility Study (PFS); a new Mineral Resource; and that it had obtained all necessary approvals from the Hollow Water First Nation, the local community of Seymourville and the Province of Manitoba. Additionally the Canadian Minister of Environment and Climate Change confirmed that the project would not require environmental assessment under federal law CEAA 2012.

As part of the PFS, and based on an additional 93-hole sonic drill program, a NI 43-101 Mineral Resource was defined at 49.6 million tonnes of Measured & Indicated and 97.3 million tonnes of Inferred. Additionally, a 30.6 million tonne Proven & Probable Mineral Reserve was defined.

The PFS estimated a 25-year mine life; initial capex of $220 million and sustaining capital of $110-$115 million; an after-tax net present value of $220 million (discounted at 8%); and an after-tax internal rate of return of 20.2%. The mining method is expected to be a conventional open pit quarry employing typical truck and excavator operations. The project is expected to produce an average of 1.2 million tonnes of product per year. Subsequently, On July 18, 2019, Canadian Premium Sand announced that it was conducting a comprehensive capital optimization review to identify cost reductions to capex outlined in the PFS and a scaled market-entry strategy. Refer to SEDAR or www.canadianpremiumsand.com/ .

The Manigotagan Property is located 170 km northeast of Winnipeg where Gossan held a silica sand deposit at Seymourville, on the east shore of Lake Winnipeg, directly across from Black Island where silica sand was extensively quarried prior to the island becoming a Provincial Park.

On June 25, 2013, Gossan entered into a purchase and sale agreement to vend its Manigotagan Silica Frac Sand Project, comprised of 9 quarry leases located near Seymourville Manitoba, to Claim Post Resources Inc., now Canadian Premium Sand Inc. Gossan had been seeking a joint-venture partner or a purchaser for the Project since completing a marketing study in late 2010. In 2012, Claim Post acquired the adjacent Seymourville Property to the south and announced plans to develop a frac sand operation. A consolidation of the two properties should improve the viability of the project.

To June 18, 2019, Canadian Premium Sand, formerly Claim Post Resources, has made total property payments of $1.28 million cash; 4 million shares of Claim Post (subsequently sold); and advance royalty payments of $400,000. The next advance royalty payment of $50,000 is due December 18, 2019.

In 2006, Gossan conducted a 23-hole core and auger drill program at the 306-hectare Manigotagan Silica Property and in 2008 followed up with a 26-hole sonic drill program. These drill programs were successful in outlining two material zones of high-purity silica sand with limited overburden.

In 2009, Gossan commenced testing the silica sand for use as frac sand proppant, resulting in consistent ISO 9K Proppant ratings for various mesh fractions. Pressure conductivity tests were also conducted with positive results.

In 2010, Gossan retained a marketing consultant for the project. The marketing study established that the highest and best use of Manigotagan silica sand is as frac sand proppant used in the oil and gas sector. The study provided an analysis of 17 companies producing frac sand proppant in North America and an assessment of candidates suitable for a strategic partnership in Gossan’s Project.

Of the million-odd horizontal wells in North America, most use frac sand that comes from a rich seam of 'white silica' sand that cuts beneath the Great Lakes region in Wisconsin

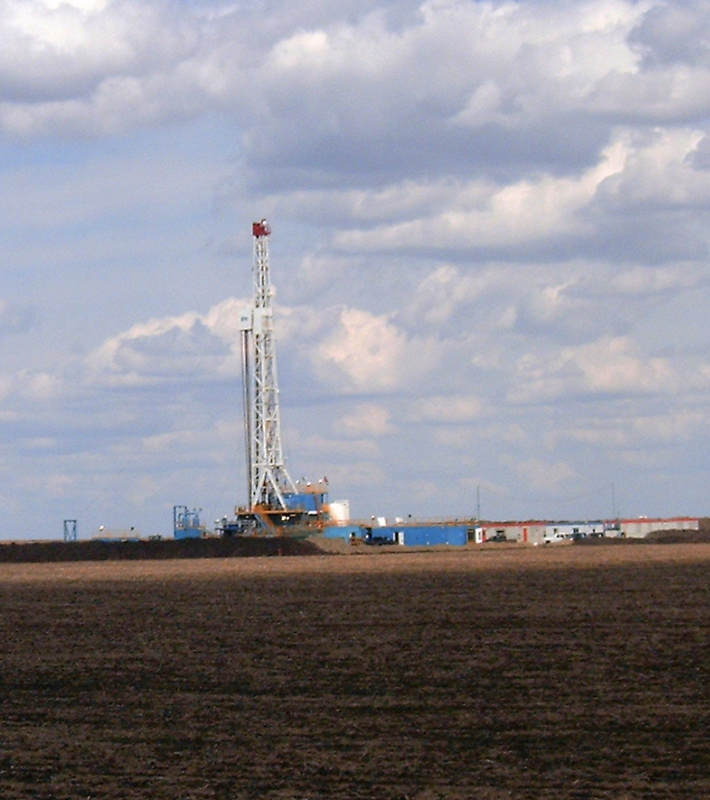

A fracking operation in Alberta.

CALGARY — Even the smallest grain of sand is of consequence to Brad Thomson, the CEO of Calgary-based Source Energy Services Canada LP.

The company is one of Canada’s largest suppliers of frac sand, a material that is injected into wells during hydraulic fracturing operations to prop open rock fractures and allow oil and gas to flow to the surface.

Of the million-odd horizontal wells scattered around North America, most use frac sand that comes from a rich seam of so-called “white silica” sand that cuts beneath the Great Lakes region in Wisconsin. It is prized for the superior quality of its grains, which are said to more effectively lodge themselves into shale rock fractures, allowing producers to boost well performance.

“You need sand that’s very round, very hard and very pure,” says Thomson, whose company owns a mine and processing facility in Wisconsin. “There’s sand everywhere in North America but generally it lacks one of those three characteristics.”

Thomson estimates Wisconsin white silica, sometimes called “Ottawa White,” supplies roughly 90 per cent of the Canadian frac sand market. And all of that sand is meets tight specifications: Samples are sent to far-off laboratories to be tested for crush resistance, consistency, shape and the concentration levels of quartz minerals, all according to specific American Petroleum Institute (API) standards.

Demand for frac sand is expected to double in the coming years as oil producers focus on wringing as much oil and gas as possible from every well. That has kicked off a race among sand suppliers to take advantage, either by developing new mines in Canada or by shipping product from the U.S. Midwest.

Todd Korol for National Post

While chronically low commodity prices have reduced drilling activity in recent years, producers continue to squeeze tremendous volumes of oil and gas from hard rock formations. That has placed more attention on the market for frac sand, which is expected to total between US$850 and US$950 million in Canada in 2017, according to IHS Markit.

In the Montney Formation of northern B.C. and Alberta, producers in 2013 used an average of around 500 pounds of sand per foot of a horizontal well; today that number is closer to 1,000 pounds, according to research by RS Energy Group. And wells are getting longer: horizontal wells now stretch around 9,000 feet, compared to 5,000 feet just four years ago.

It’s had a massive impact. Today, a producer in the Montney might blast 100 rail cars of sand down a single well.

Analysts expect that figure to increase, particularly in the Montney, as companies begin to pump higher volumes of sand, led by producers like Encana Corp. and Seven Generations Energy Ltd.

“So far the more aggressive operators they’re well above that 1,000 pound-per-foot average, and I think eventually everyone will end up settling where they are,” says Trevor Goertzen, an analyst with RS Energy Group in Calgary.

As a result of the increased demand, U.S. and Canadian suppliers are vying for market share by expanding their rail and terminal infrastructure into highly sophisticated networks.

“Without exception everybody is going through a phase of growth,” Source Energy Services’ Thomson says.

The company plans to spend $25 million this year to build three rail terminals in Edson and Fox Creek, Alta., and Taylor, B.C., to receive rail shipments from Wisconsin. The company plans to nearly double its capacity in coming years to 3.8 million tonnes per year.

Major U.S. suppliers are also expanding. U.S. Silica Holdings Inc. expects to expand its sand flows into several prolific shale basins by 68 per cent in 2017, while Emerge Energy Services LP, a Texas- based company, continues to expand its sand division by building out its rail infrastructure and loading facilities.

“The entire objective is to get volumes into the basin in a location that minimizes your trucking distances,” he says.

Without exception everybody is going through a phase of growth

Analysts are now wondering whether Canada’s rail infrastructure can absorb the addition demand as capacity is running near its peak. “This doesn’t yet appear to be a critical issue, but with every 1-2 wells effectively drawing a unit train of sand, it seems reasonable to question whether there is the logistical network to properly facilitate all of this,” Raymond James analysts wrote in a recent research note.

More worryingly, low commodity prices have gutted the stock valuations of some companies in recent months. Source Energy completed an initial public offering in April at $10.50 per share, well below the $17 to $20 range it had floated earlier in the year.

“Financial markets have been soft,” Thomson says. In early June its stock was trading around the $8.50 range.

U.S. sand suppliers have also seen their market valuations shrink. U.S. Silica’s stock price is down roughly 36 per cent from its February levels, while Emerge Energy Services LP’s stock price has been halved over the same period.

Meanwhile, several would-be Canadian suppliers have proposed building sand mines in Western Canada as a way to undercut Wisconsin-based shippers.

Julia Schmalz/Bloomberg

Edmonton-based Athabasca Minerals Inc. and Saskatoon-based Hanson Lake Sands Corp. both aim to secure a hold in the frac sand market from their gravel and nickel mines, respectively. Vancouver-based Stikine Energy Corp. had proposed two sand mines in B.C., but the company wasn’t able to raise the necessary capital and currently appears to be nearing insolvency. Calgary’s LaPrairie Group operates a sand mine near Grande Prairie, Alta.

Often times, domestic mines are not well connected to rail infrastructure, and depend on high-cost trucking services to deliver their product. Others have grains that are angular rather than spherical, which can cause the sand to bond with water molecules and plug a well.

“Everybody thinks they’ve got frac sand,” says Ray Newton, a co-founder of Canadian Sandtech Inc., a private company with a sizeable stake in an upstart sand mine near Saskatoon.

Proving the quality of sand is crucial. Canadian Sandtech recently sent several five-gallon pails of sand to a laboratory in Langley, B.C. to test the mettle of its sand particles. It also completed in-house tests, Newton says.

Newton, like other domestic suppliers, disputes whether silica sand is necessary to boost well returns. His local mix of “Bradley Brown” is equal in quality, he argues.

For now, however, producers seem willing to pay a premium for Ottawa White, even as they face pressure to continuously reduce well costs.

Producers in the northern reaches of B.C., for example, might pay $150 per tonne for frac sand, while companies in the southern Montney might pay $75. Domestic supplies cost a fraction of that price.

For now, Thomson is confident firms in Western Canada will continue to transport their sand over thousands of kilometres rather than risk using inferior grains of sand.

“There’s certainly a bit of a quality trade-off.”

MORE

How a ‘meteoric rise in demand’ has triggered a frack sand race

The Permian Basin: An existential threat to Canadian oil as war on cost heats up

Public fracking: Source Energy said to seek C$250 million in Toronto IPO

A fracking operation in Alberta.

CALGARY — Even the smallest grain of sand is of consequence to Brad Thomson, the CEO of Calgary-based Source Energy Services Canada LP.

The company is one of Canada’s largest suppliers of frac sand, a material that is injected into wells during hydraulic fracturing operations to prop open rock fractures and allow oil and gas to flow to the surface.

Of the million-odd horizontal wells scattered around North America, most use frac sand that comes from a rich seam of so-called “white silica” sand that cuts beneath the Great Lakes region in Wisconsin. It is prized for the superior quality of its grains, which are said to more effectively lodge themselves into shale rock fractures, allowing producers to boost well performance.

“You need sand that’s very round, very hard and very pure,” says Thomson, whose company owns a mine and processing facility in Wisconsin. “There’s sand everywhere in North America but generally it lacks one of those three characteristics.”

Thomson estimates Wisconsin white silica, sometimes called “Ottawa White,” supplies roughly 90 per cent of the Canadian frac sand market. And all of that sand is meets tight specifications: Samples are sent to far-off laboratories to be tested for crush resistance, consistency, shape and the concentration levels of quartz minerals, all according to specific American Petroleum Institute (API) standards.

Demand for frac sand is expected to double in the coming years as oil producers focus on wringing as much oil and gas as possible from every well. That has kicked off a race among sand suppliers to take advantage, either by developing new mines in Canada or by shipping product from the U.S. Midwest.

Todd Korol for National Post

While chronically low commodity prices have reduced drilling activity in recent years, producers continue to squeeze tremendous volumes of oil and gas from hard rock formations. That has placed more attention on the market for frac sand, which is expected to total between US$850 and US$950 million in Canada in 2017, according to IHS Markit.

In the Montney Formation of northern B.C. and Alberta, producers in 2013 used an average of around 500 pounds of sand per foot of a horizontal well; today that number is closer to 1,000 pounds, according to research by RS Energy Group. And wells are getting longer: horizontal wells now stretch around 9,000 feet, compared to 5,000 feet just four years ago.

It’s had a massive impact. Today, a producer in the Montney might blast 100 rail cars of sand down a single well.

Analysts expect that figure to increase, particularly in the Montney, as companies begin to pump higher volumes of sand, led by producers like Encana Corp. and Seven Generations Energy Ltd.

“So far the more aggressive operators they’re well above that 1,000 pound-per-foot average, and I think eventually everyone will end up settling where they are,” says Trevor Goertzen, an analyst with RS Energy Group in Calgary.

As a result of the increased demand, U.S. and Canadian suppliers are vying for market share by expanding their rail and terminal infrastructure into highly sophisticated networks.

“Without exception everybody is going through a phase of growth,” Source Energy Services’ Thomson says.

The company plans to spend $25 million this year to build three rail terminals in Edson and Fox Creek, Alta., and Taylor, B.C., to receive rail shipments from Wisconsin. The company plans to nearly double its capacity in coming years to 3.8 million tonnes per year.

Major U.S. suppliers are also expanding. U.S. Silica Holdings Inc. expects to expand its sand flows into several prolific shale basins by 68 per cent in 2017, while Emerge Energy Services LP, a Texas- based company, continues to expand its sand division by building out its rail infrastructure and loading facilities.

“The entire objective is to get volumes into the basin in a location that minimizes your trucking distances,” he says.

Without exception everybody is going through a phase of growth

Analysts are now wondering whether Canada’s rail infrastructure can absorb the addition demand as capacity is running near its peak. “This doesn’t yet appear to be a critical issue, but with every 1-2 wells effectively drawing a unit train of sand, it seems reasonable to question whether there is the logistical network to properly facilitate all of this,” Raymond James analysts wrote in a recent research note.

More worryingly, low commodity prices have gutted the stock valuations of some companies in recent months. Source Energy completed an initial public offering in April at $10.50 per share, well below the $17 to $20 range it had floated earlier in the year.

“Financial markets have been soft,” Thomson says. In early June its stock was trading around the $8.50 range.

U.S. sand suppliers have also seen their market valuations shrink. U.S. Silica’s stock price is down roughly 36 per cent from its February levels, while Emerge Energy Services LP’s stock price has been halved over the same period.

Meanwhile, several would-be Canadian suppliers have proposed building sand mines in Western Canada as a way to undercut Wisconsin-based shippers.

Julia Schmalz/Bloomberg

Edmonton-based Athabasca Minerals Inc. and Saskatoon-based Hanson Lake Sands Corp. both aim to secure a hold in the frac sand market from their gravel and nickel mines, respectively. Vancouver-based Stikine Energy Corp. had proposed two sand mines in B.C., but the company wasn’t able to raise the necessary capital and currently appears to be nearing insolvency. Calgary’s LaPrairie Group operates a sand mine near Grande Prairie, Alta.

Often times, domestic mines are not well connected to rail infrastructure, and depend on high-cost trucking services to deliver their product. Others have grains that are angular rather than spherical, which can cause the sand to bond with water molecules and plug a well.

“Everybody thinks they’ve got frac sand,” says Ray Newton, a co-founder of Canadian Sandtech Inc., a private company with a sizeable stake in an upstart sand mine near Saskatoon.

Proving the quality of sand is crucial. Canadian Sandtech recently sent several five-gallon pails of sand to a laboratory in Langley, B.C. to test the mettle of its sand particles. It also completed in-house tests, Newton says.

Newton, like other domestic suppliers, disputes whether silica sand is necessary to boost well returns. His local mix of “Bradley Brown” is equal in quality, he argues.

For now, however, producers seem willing to pay a premium for Ottawa White, even as they face pressure to continuously reduce well costs.

Producers in the northern reaches of B.C., for example, might pay $150 per tonne for frac sand, while companies in the southern Montney might pay $75. Domestic supplies cost a fraction of that price.

For now, Thomson is confident firms in Western Canada will continue to transport their sand over thousands of kilometres rather than risk using inferior grains of sand.

“There’s certainly a bit of a quality trade-off.”

MORE

How a ‘meteoric rise in demand’ has triggered a frack sand race

The Permian Basin: An existential threat to Canadian oil as war on cost heats up

Public fracking: Source Energy said to seek C$250 million in Toronto IPO