It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Europe’s arms imports nearly double, France overtakes Russia as world’s second-largest exporter

By Euronews

Much of the growth in arms imports by European countries between 2019 and 2023 is due to the massive transfers of weapons to Ukraine in 2022 and 2023, according to a recent study.

European countries have nearly doubled their arms imports between 2014-2018 and 2019-2023, boosting their purchases by 94% in the period observed, according to a new study by the Stockholm International Peace Research Institute (SIPRI).

Much of this increase was due to the transfers of arms to Ukraine, which is still fighting off the Russian invasion and which, between 2022 and 2023, received 23% of the region’s arms import in 2019-2023.

Two European countries - France and Italy - have also significantly stepped up their exports in the same period, finding willing buyers in Europe, Asia and the Middle East.

Perhaps surprisingly seeing the current situation in Europe and the rest of the world, with the conflicts in Ukraine and Gaza, the global volume of international arms transfers fell slightly by 3.3% between 2014-2018 and 2019-2023.

Who’s Europe buying arms from?

The largest importer in Europe was by far Ukraine, which accounted for 23% of all Europe’s imports between 2019 and 2023. The next biggest importers were the UK (11% of all European imports) and the Netherlands (9.0%).

A majority of 55% of the arms imports by European countries between 2019-2023 came from the US, whose exports to Europe were up 35% compared to the previous timeframe analysed, 2014-2018. Other major arms imported to Europe between 2019 and 2023 came from Asia, Oceania and the Middle East.

“Many factors shape European NATO states’ decisions to import from the USA, including the goal of maintaining trans-Atlantic relations alongside the more technical, military and cost-related issues,” SIPRI Director Dan Smith explained in a press release. “If trans-Atlantic relations change in the coming years, European states’ arms procurement policies may also be modified.”

The next largest supporters after the U.S. were Germany (6.4%) and France (4.6%).

The rise of France’s arms exports

The US and France currently dominate global arms exports, with Washington having grown its exports by 17% between 2014-2018 and 2019-2023 and Paris by 47% in the same period.

The US alone was responsible for 42% of the total global arms exports, delivering arms to 107 states between 2019 and 2023, more than any other major exporters. The rise in French arms exports, on the other hand, was mainly due to the delivery of combat aircraft to India, Qatar and Egypt.

For the very first time, France was ahead of Russia in the list of largest arms exporters in the world, ranking second where Russia ranked third. That’s because while France’s exports climbed, Russia’s exports halved (-53%) in the same period. While Russia exported to 31 states in 2019, the number dropped to only 12 in 2023.

The largest share of France’s arms exports (42%) went to countries in Asia and Oceania, while another 34% went to Middle Eastern states.

The largest recipient of French arms exports was India, with nearly 30% of all exports. The country was the world’s top arms importer between 2019-2023 - though its main supplier remains Russia, which accounted for 36% of all its imports.

“France is using the opportunity of strong global demand to boost its arms industry through exports,” said Katarina Djokic, a researcher at SIPRI. “France has been particularly successful in selling its combat aircraft outside Europe.”

Other countries - including another European one - saw their arms exports increase in the past three years. In Italy, arms exports grew by 86%, while in South Korea they climbed by 12%.

China saw arms exports slide down by 5.3%, Germany and the UK by 14%, Spain by 2.2% and Israel by 25%.

Who’s Europe selling arms to?

Together with the US, Western Europe accounted for 72% of all arms exports in 2019-2023, while alone Europe was responsible for about a third of global arms exports, including large volumes going outside the region.

A total of five European countries, excluding Russia, were among the top 10 largest exporters in the world, including France (2nd place), Germany (5th place), Italy (6th place), UK (7th place) and Spain (8th place). The Netherlands were in 12th place, followed by Sweden (13th), Poland (14th), Switzerland (17th), Ukraine (18th), Norway (19th) Belgium (22nd) and Belarus (23rd).

Some 30% of international arms transfers went to the Middle East in 2019-2023, with the top three buyers in the region being Saudi Arabia, Qatar and Egypt. The majority of arms imports by Middle Eastern states were supplied by the US (52%), followed by France (12%), Italy (10%) and Germany (7.1%).

The biggest importers in 2019-2023 were India, Saudi Arabia and Qatar, followed by Ukraine, which has received major transfers of arms from over 30 countries between 2022 and 2023.

The US and Germany accounted respectively for 69% and 30% of arms imports by Israel, which is currently fighting a deadly war against Hamas in Gaza which killed over 30,000 people, most of whom were civilians.

countries. Yet, new details show that arms supply is just as much the bloc’s area of specialisation, to eastern African countries.

The Brics arms race, it turns out, is already playing out in eastern Africa as new data indicates that in 2021 and 2022, Uganda and Rwanda were the biggest importers of Russian arms, while Ethiopia and Tanzania sourced their military firepower from China.

This is according to the Stockholm International Peace Research Institute (Sipri) arms transfer database.

In its August update — dated just before the August 22-24 Brics Summit in South Africa — Sipri, showed that Russia and China dominate supplies while India is the bloc’s and the world’s biggest arms importer. Sipri often research and maps conflicts, arms control and purchases.

The update studied arms transfers for the period 2008 — 2022, to see whether the trend of trading between Brazil, Russia, India, China and South Africa — which until the formal admission of six new members constituted the Brics group — is also reflected in arms trade between themselves.

According to Sipri, the Brics is an important economic bloc and trade between its members is growing. Data shows that Russia has remained the top supplier of arms to India in the last 14 years, while the Asian nation was also the number one export market for Russian arms exports.

“However, Russia’s share fell from 78 percent in 2008-12 to 45 percent in 2018-22, while France, Israel and USA all gained ground,” the think tank explains.

According to Sipri, China receives most of its major arms imports from Russia and was ranked the number two market for Russian arms exports in 2008-2022, but the Asian giant is becoming less reliant on arms imports, including from Russia as its domestic arms industry grows rapidly.

While India was the world’s number one importer of major arms from 2008 – 2022, China ranked third while other Brics members imported much smaller volumes, ranking 36th, 55th and 63rd for Brazil, South Africa and Russia respectively, according to Sipri.

In terms of exports, Russia, ranked number two globally after the US, while China was number five, with India, Brazil and South Africa having relatively small domestic arms industries but keen to increase their exports.

In East Africa, Uganda was ranked Russia’s biggest market in 2022, importing weapons worth $48 million out of a total import bill of $55 million, according to Sipri’s trend indicator values. Its other sources were Czechia ($4 million), Israel ($2 million), China ($1 million) and South Africa ($1 million).

In 2021, Rwanda imported arms worth $46 million from Russia, $10 million from turkey and $2 million from the US.

In 2022, Ethiopia imported weapons valued at $35 million from China, while the previous year, its arms were sourced from Turkey ($5 million) and $6 million worth of weapons from unknown sources.

In 2021, Tanzania imported arms worth $29 million from China and also sourced weapons worth $24 million from France.

Somalia and the Democratic Republic of Congo sourced their arms from South Africa; Kenya and South Sudan are the only countries from region whose military supplies are not sourced from a Brics member during this period.

In 2009, Brazil, Russia, India, China and South Africa formed the bloc to counter western dominance in geopolitics, and to promote peace, security, development and cooperation; the inclusion of new members Argentina, Egypt, Ethiopia, Iran, Saudi Arabia and the United Arab Emirates is meant to share these goals wider.

Scholars view the Brics emergence as critical to establishing a new world order to bridge the widening gap between the actual role of emerging markets in the global system and their ability to participate in the decision-making process of global institutions.

Our global culture of war means guaranteed profits for the arms industry

For the arms industry to flourish, it needs wars, preferably protracted, destructive stalemates in far-off places

Paul Rogers 23 June 2023, 5.19pm A missile on display at a DefExpo 2022, a defence industry trade fair in India | T. Narayan/Bloomberg via Getty Images

While most would agree there is no such thing as a ‘good war’, those taking a calculated view might argue that such a thing would mean a quick victory with minimal losses on your own side, with the other side so defeated as to present few problems in the future. A ‘perfect war’, then, might be one where there is capitulation and complete surrender without a shot being fired.

The world’s arms dealers will take a devastatingly different view. Their primary function, like that of any other industrial endeavour in a shareholder capitalist system, is to make money for shareholders while ensuring decent salaries and even more decent bonuses for the CEO and senior colleagues.

To them, a ‘perfect war’ is one that degenerates into a violent stalemate that creates an insatiable demand for arms and the replacement of worn-out equipment, while at the same time, each side constantly tries to improve its weaponry and tactics. Profit is placed over lives, though it is arguably better if the war has relatively low casualties so that public support remains high and the war – and the money it generates – can continue.

An even ‘better’ scenario for an arms dealer is selling arms to another country that’s engulfed in an everlasting war that their own country is not fighting, and better still if they are selling to both sides at the same time.

Now carry over this line of argument to the real world of the early 21st century, and we come up with some unusual and appalling results. The US-led coalition’s war in Afghanistan was long, and the 20 years of conflict certainly helped the armourers in many countries make plenty of money, as did the shorter eight-year war in Iraq.

Neither war, though, proved particularly popular back home and both came to a catastrophic end, with hundreds of thousands of people dead and two countries wrecked – but there were still plenty of profits for the armourers.

Iraq actually turned out to be a more complicated war, with ISIS emerging rapidly from the chaos left by Western forces. By 2014 it had taken control of much of northern Iraq and Syria. A US-led coalition was rapidly put together to organise an intensive air war across the two countries, with thousands of airstrikes and cruise missile attacks over a four-year period until ISIS was crippled.

According to AirWars, some 30,000 targets were attacked using more than 100,000 missiles and guided bombs, and at least 60,000 people were killed. Some of these will have been ISIS paramilitaries, but thousands will have been civilians of all ages. However, hardly any Western military personnel were killed apart from occasional accidents, there was little media coverage except when cities such as Mosul and Raqqa were taken, so there was little public attention paid to what appeared – from a Western perspective – to be a successful war.

Even its ‘success’ is debatable, though, as around a thousand US troops are still in northern Syria, many more are in Iraq, coalition forces still carry out air strikes in both countries, and ISIS is expanding its links with like-minded Islamist paramilitaries across the Sahel and on to the DRC, Uganda and even Mozambique. That war is still not over, so the profits still roll in.

For arms dealers, a ‘perfect war’ is one that degenerates into a violent stalemate that creates an insatiable demand for arms

Returning to today, there are many conflicts around the world that arms firms are looking at and seeing dollar-signs. Let’s start with the Indo-Pacific region, where there are plenty of new opportunities for arms marketing. Chinese manoeuvres towards Taiwan are combining with greater US military activity, stimulating a veritable arms sales bonanza across southeast Asia. Malaysia, Indonesia and the Philippines are all investing heavily, especially in new naval forces.

Further south, Australia is integrating its military posture closely with the United States and Britain in the AUKUS programme of new nuclear-powered attack submarines, while further west, a mini-arms race is developing between India and Pakistan as each invests in new generations of air-defence missiles. According to Jane’s Defence Weekly, Pakistan’s new weapons are centred on the advanced S-400 long-range ground-launched missile from Russia.

India, meanwhile, sees issues with China but is also concerned with what it views as rather too-close links between China and Pakistan. It, too, has bought into the S-400 system but is also buying Barak-8 medium-range anti-aircraft missiles from Israel.

As for China itself, people from its own version of a military-industrial complex have had little role in the national leadership until now, but that has changed in the wake of President Xi’s re-election for a record third term: five new members of the politburo are from the military sector. China may be a hybrid state-capitalist economy but individual corporations still look to business success and their own well-being.

Then there is Russia’s war in Ukraine, which is turning out to be both long and brutal, with many catastrophes and much loss of life. Three weeks into Ukraine’s offensive in the Donbas region, casualties on both sides are high and there are already signs that the offensive is unlikely to succeed in forcing Russia to agree terms.

The Russian military sector has proved more than able to continue producing large quantities of artillery and ammunition, and the leadership has learned from some of its early errors. Putin remains in firm control and though his position could change overnight, there is little sign of this happening.

Ukraine, meanwhile, is still receiving plenty of weapons, ammunition and materiel from NATO, though much of it is very slow in coming, especially the much-desired F-16 interceptors. The war may yet last years, not months – offering ideal conditions for arms’ companies to profit.

Many such arms industry leaders may choose to view themselves as patriotic guardians of their country. But the system in which they operate raises real ethical questions, which few seem to want to answer.

Meanwhile, as the conflict in Ukraine moves slowly towards a ‘perfect war’, more people will die, more towns and villages will be levelled – all of which will simply be seen as collateral damage in our global culture of war.

PERMANENT ARMS ECONOMY German arms sale approvals jump slightly in first quarter of 2020

The first-quarter increase comes on the heels of a record annual German arms sales in 2019. Sales to third world countries nearly tripled, including to countries involved in the Yemeni Civil War.

German arms sale approvals increased slightly in the first quarter of 2020 compared to the same period last year, the nation's Economy Ministry said on Thursday.

The ministry, responding to a formal question by the Left Party (die Linke), said the government approved arms exports worth €1.16 billion ($1.27 billion) in the first three months of 2020, a €43.5 million increase from the same period in 2019.

Government-approved arms sales hit a record high in 2019, totaling €7.95 billion. Sales had declined the previous three years after a previous record of €7.86 billion in exports in 2015. The Left Party, probably the most critical of Germany's arms export policies, condemned the increase in arms sales amid the coronavirus pandemic.

"While the UN is calling for a global ceasefire to fight the coronavirus pandemic, the German government continues to pour oil on the fire with its war weapons in crisis areas," die Linke's disarmament specialist Sevim Dagdelen said in response to the figures. "We need an immediate halt to arms exports and convert the defense industry to make civilian goods such as medical equipment. It is time to produce for life instead of death."

This Chinese armored medical evacuation vehicle arrived by ship at the port in Hamburg, before being shipped to southern Germany and the Bavarian town of Feldkirchen. A total of 92 Chinese and 120 German soldiers are taking part in the Combined Aid 2019 exercise, along with 120 men and women in supporting roles. Controversial sale to Egypt

Though sales to EU and NATO countries declined slightly, sales to non-NATO and non-EU members nearly tripled from €134 million in the first quarter of 2019 to €360 million in the first three months of 2020.

The Economy Ministry said the increase was due to a deal struck with Egypt involving a frigate and a submarine. At €290 million in sales, Egypt's nominally civilian government led by the former head of the army was by far the largest arms buyer from Germany in the first quarter of this year.

The deal with the African nation was finalized despite Germany affirming in 2018 that it would not sell weapons to parties involved in the conflict in Yemen, a conflict that has killed over 100,000 people. This resolution followed sharp criticism of a series of high-profile sales to Saudi Arabia, which is leading the international coalition attacking Yemen's Houthi rebels.

Egypt recently dispatched warships to assist with a Saudi-led naval blockade of Yemen.

Since early 2019, German arms manufacturers have sold over €1 billion worth of weapons to Egypt, the United Arab Emirates (UAE) and other countries part of the Saudi-backed coalition in Yemen.

"The UAE and Saudi Arabia are to blame for the biggest humanitarian catastrophe of our times," she said. She has called for Germany to halt exports to the UAE immediately.

Thursday, February 10, 2022

The ‘Wild Card Entry’ of China has Accelerated the Global Arms Race

In post Second World War era the Arms Race was identified by advances and innovations in conventional and nuclear weapons, with US and USSR leading the trend. After acquiring sufficient destructive force for ‘Mutually Assured Destruction’ (MAD), some common sense prevailed in the face of WMD, and treaties such as the NPT,CTBT, INF, and START, to mention a few, were signed by world powers. In the meantime, China continued to develop its comprehensive national power (CNP), which included, among other things, significant advances in military modernization and technology using every possible means. China’s recent developments in hypersonic weapons, combined with AI, cyber, and biological warfare instruments, have alerted the world to some previously unknown vulnerabilities, triggering a new Arm race with its wild, but loud announcement of the multidimensional threat it poses to its potential adversaries. Drivers of Global Arms Race

There are many drivers in global arms race. In today’s world every country aims to win, preferably without fighting, for which it needs to posture strong military power to deter the adversary with state-of-the-art arsenal, which triggers arms race. Chinese political aim is to displace US as lone superpower, whereas US would like to maintain its edge. Russia also wants to be counted as world power with all levers of power intact, except poor economy. China, on the other hand, has increased its CNP by improving its economy and defining its military objectives, such as modernising the PLA by 2035 and developing a world-class military capable of winning wars by 2049.

The threat to the country is the other driver in muti-domain warfare of today, which has elements of kinetic and non kinetic, contact and non-Contact warfare elements, often exercised in the ambit of Grey Zone Warfare. China finds its large coastline, other navies in its backyard near Eastern Sea board as threat, with its greatest vulnerability being long sea lines of communication (SLOC). It explains the logic of rapid expansion of PLA Navy. Russian threat is economy and western expansion; hence, as countermeasures nearness to China, strong posturing in Ukraine, annexation of Crimea is the outcome. US has limited conventional threat except from missiles, space assets and non- contact warfare elements like cyberwarfare.

Geography of a country is a constant in its CNP, where China has a disadvantage. It is grossly short of energy, water, agriculture land, needs to defend large borders and coastline, with Eastern seaboard hemmed in two island chains, from where maximum invasions took place in past. Lack of warm water access to western China is also a handicap. US on the other hand has enough security in energy, water, food, and faces no land border threat. Therefore, to checkmate US, China has to develop its arsenal to pose aerial threat including space and threaten it by non-contact warfare elements like cyber, info warfare, economy etc.Russia is self-sufficient in energy, industry, technology, military, nuclear and space, but can be targeted economically.

China recognises that the US’ defence budget has been three to four times higher for decades, and it has vast superiority in conventional, nuclear, ballistic missiles, heavier naval craft, and aircraft that is difficult to match; as a result, it has attempted to gain supremacy in areas that could make the USA vulnerable, such as hypersonic glide vehicles, space, Cyber, AI, robotics, and 6G networking, as well as the arsenal related to these technologies.

Arms race is a process with no permanent winner, because for every offensive innovation, new countermeasures are invented by adversary. Arm Race is also a vehicle on which many economies ride and it suits the arms dealers. Latest Trends in Arms Race Triggered by China

Hypersonic Weapons China has taken a quantum jump in Hypersonic technology by mounting DF-ZF hypersonic glide vehicle on DF17 MRBM, making it difficult to detect, thus exposing a vulnerability of global air defence systems. The test involving Hypersonic glide vehicle Space Re-entry Fractional orbital bombardment systems (FOBS) flying in low orbit, before accelerating towards a target, has put US and other world power on notice to start working on the counter technology, before it’s too late. China made use of provisions of UN Treaties and Principles of Outer Space, wherein WMD deployment in space is prohibited but is silent on hypersonic re-entry. It has also put Russia on notice which has such weapon systems, but is apprehensive that its technology might have been proliferated. The race is to bring the detection point as close to the target as possible, to minimise reaction time. The countermeasures will also see innovations through laser shield, enhanced detection capabilities in space or other technologies. It may not be a game changer, but it certainly threatens certain targets like aircraft carriers crucial to US striking power.

Nuclear Arsenal China is mindful of vast gap it has in nuclear arsenal in comparison to US and Russia.It developed comprehensive missile programme, remaining out of some of the arms control treaties. China has set a target of having at least 700 nuclear warheads by 2027 and 1,000 warheads by 2030. It has also miniaturised nukes for tactical use in localised conflicts. Although it’s a signatory of NPT but the suspicion of proliferating nuclear and missile technology to Pakistan and North Korea remains. US and Russia may not be keen to pursue nuclear arms race, but China is certainly accelerating it.

PLA Navy China in a short span of time has considerably increased the numbers of combat assets of its Navy to become largest Navy in the world with 348 combat ships surpassing 296 of US. Qualitatively US continues to have an upper edge in terms of 11 aircraft carriers, more nuclear submarines, cruisers, destroyers or large ships. China is expected to be increasing its Navy by 40 percent in future, as it finds it grossly inadequate to protect its SLOC and global investments.

Technological Leap China has also made rapid strides in unmanned vehicles and robotics. Drone warfare will see a major arms race in innovations, as it has been a major game changer in recent Armenia-Azerbaijanconflict. The West is also developingArea denial or Anti Access Anti Area weapon systems (A2AD), Laser shields, Direct Energy Weapons to name a few innovations. Non-Kinetic, Non-Contact Warfare

Biological Warfare For various reasons there is no evidence in open domain that coronavirus was a biological weapon unleashed by China, but there is no evidence to the contrary as well. The involvement of Wuhan Institute of virology, its alleged connection with PLA, combined with circumstantial evidences point the needle of suspicion that it could well be a biological weapon, causing devastation never seen before. If apprehensions are true, China could have violated ‘Biological Weapon Convention’.

Artificial Intelligence China is using state of the art artificial intelligence incorporated in variety of military arsenal like robotics, missile guidance systems, and unmanned aerial vehicles including naval vessels.

Cyber Warfare Many countries have been accusing China of launching large-scale cyber-attacks like UK, US and EU. China has put in place an exhaustive cyber as well as information warfare machinery, which others need to catch up, to defend not only their military and civil systems, but also some of their essential services. Needless to say the race will see similar capabilities being generated by others. China is thus looking to utilise disruptive technology to accelerate arms race. China as Arms Exporter

In last decade China has made significant strides in Arms industry to emerge as third largest exporter of military equipment in the world. However, its equipment is still untested in war and most of its purchasers are by countries highly indebted to it or having some compulsions other than quality and reliability, to buy its hardware. It’s estimated that 60 percent of Pakistani hardware is of Chinese origin and 35 percent of hardware produced by China is purchased by its captive buyer, Pakistan.

China triggers Regional Arms Race

Regionally China wants a ‘China-centric Asia,’ and has expedited the capacity-building of neighbours like India, which sees China as a threat because of its irresponsible aggressiveness in Ladakh and other areas along the LAC. Its overdrive to boost Pakistan’s military capacity, in order to strengthen the hybrid war against India, including the deployment of naval combat assets in the Arabian Sea, the transfer of technology to manufacture aircraft, and the suspected/alleged proliferation of nuclear and missile technology, are just a few examples to accelerate the arms race in South Asia. Should its plans of ‘winning without fighting’ fail, China appears to be considering posing a two-and-a-half front threat in coordination with Pakistan, as well as an ‘Informatised local conflict’ if necessary.

Gen. Shashi Asthana The author is a veteran Infantry General with 40 years experience in international fields and UN. A globally acknowledged strategic & military writer/analyst; he is currently the Chief Instructor of USI of India, the oldest Indian Think-tank in India.

Qatar ranks as top arms importer despite surge in weapons going to Ukraine

Russia's arms exports decreased, while France picked up new customers in the Middle East, according to a new arms report Attendees stand by a model of a Qatar Emiri Air Force (French-made) Rafale fighter jet during the Doha International Maritime Defence Exhibition in Qatar's capital Doha, on 21 March 2022 (AFP)

Middle East and North African countries remained among the world’s largest global arms importers in 2022, despite global attention on arms shipments to Ukraine amid Russia’s invasion, according to a report published on Monday by the Stockholm International Peace Research Institute (Sipri).

“Even as arms transfers have declined globally, those to Europe have risen sharply due to the tensions between Russia and most other European states,” said Pieter D Wezeman, senior researcher with the Sipri arms transfers programme, according to a Sipri press statement.

“Arms imports to East Asia have increased and those to the Middle East remain at a high level,” Wezeman said.

Russia-Ukraine war: Moscow's quest for Middle East arms deals upended by fighting

Arms from the US and European countries poured into Ukraine, following Russia’s February 2022 invasion of the country. The US alone has provided Ukraine with approximately $27.5 bn in military assistance since the beginning of the Biden administration. Kyiv was the third largest importer of arms globally in 2022.

Qatar, a gas-rich country of just three million people, holds the top spot as the world’s biggest arms importer as of last year. Shipments of weapons to the country increased by 311 percent between 2013-17 and 2018-22.

Doha is one of the world’s largest producers of natural gas. Along with neighbouring Gulf states, its global heft has swelled amid an energy crunch exacerbated by Russia’s Ukraine invasion.

In January, Qatar was designated a major non-Nato ally by US President Joe Biden, opening the path for more arms purchases from the US. In November, the US State Department approved the potential sale of a $1bn anti-drone system to Qatar.

Other Middle Eastern states have not been left out. Saudi Arabia was the world’s second-largest arms importer in 2018–22, receiving 9.6 percent of all global arms imports. Egypt, which is facing a debilitating economic crisis that has prevented the import of basic goods, ranked sixth globally for arms imports during that same period. Middle East buys big

Sipri also noted that while western states have been reluctant to provide Ukraine with major arms for fear of widening its conflict with Russia, they have shown little of the same reservation in the Middle East.

Middle Eastern states imported more than 260 advanced combat aircraft, 516 new tanks and 13 frigates between 2018-2022. Gulf powers alone have an outstanding order for more than 180 combat aircraft. The Biden administration has ruled out sending fighter jets like the F-16 to Ukraine for fear it could lead to an escalation in the war.

“Due to concerns about how the supply of combat aircraft and long-range missiles could further escalate the war in Ukraine, Nato states declined Ukraine’s requests for them in 2022. At the same time, they supplied such arms to other states involved in conflict, particularly in the Middle East,” Wezeman said. Russia-Ukraine war: How the conflict altered defence ties in the Middle East

Sipri also noted a drop in Russia’s arms exports, with decreases to eight of its 10 biggest recipients between 2013–17 and 2018–22. Russia’s arms exports fell by 31 percent in the same period and its share of global arms exports decreased from 22 percent to 16 percent.

The drop in Russian exports has coincided with an increase from the US by 14 percent between 2013-17 and 2018-22. The US accounted for 40 percent of global arms exports in 2018-22.

Sipri, however, noted that France was perhaps the biggest winner from Russia’s declining sales, with exports increasing by 44 percent between 2013-17 and 2018-22, mostly to states in Asia and the Middle East.

France scoops up market share

Middle East Eye previously reported that Russia was facing supply shortages as a result of the war and had to delay servicing clients. Analysts and diplomats have told MEE that Moscow’s poor military performance in Ukraine has hit its ability to pick up new clients in the Gulf region.

"The lack of quality of Russian weapons systems has been exposed to GCC capitals. There is a clear decline in interest among GCC countries for Russian military gear. They are doubling down on Nato weaponry," Cinzia Bianco, a visiting fellow at the European Council on Foreign Relations, previously told MEE.

Kirsten Fontenrose, a former senior director for Gulf affairs in the Trump administration’s National Security Council, previously told MEE that France’s arms industry could be the big winner from the war in Ukraine.

Turkey exploring massive UK arms deal involving planes, ships and tank engines

Fontenrose said buying from France could be a way for rulers in Riyadh and Abu Dhabi to beef up their arsenals “while not rewarding the US for what they see as mistreatment”.

Russia’s arms exports to Egypt increased 44 percent between 2013-17 and 2018-22. However, Cairo has more recently suggested it is looking to Washington for arms.

Last year, Egypt backed out of its planned purchase of Russia’s Su-35 fighter jet and decided to buy the US F-15.

The Sipri data also highlights the impact of Turkey’s rocky relationship with the US. In 2020, the US sanctioned Turkey's defence industry under the Countering America's Adversaries Through Sanctions Act (Caatsa) for its purchase of Russia’s S-400 anti-missile system.

Arms exports from Washington to Ankara decreased dramatically between 2013-17 and 2018-22, with Turkey falling from seventh to 27th place as the largest recipient of US arms.

More recently, Turkey has lobbied the US to purchase new F-16 fighter jets.

Governments help arms firms avoid Covid slump: report

Marc PRÉEL Sun, December 5, 2021,

The world's biggest weapons manufacturers largely avoided the economic downturn caused by Covid-19 and recorded a growth in profits last year for the sixth year in a row, according to a report published on Monday.

Governments around the world have continued to buy arms during the pandemic and some also passed measures to help their big weapons firms, according to the Stockholm International Peace Research Institute (SIPRI).

Overall, the 100 top weapons firms saw their profits rise by 1.3 percent on 2019 to a record $531 billion, despite the global economy contracting by more than three percent.

"Military manufacturers were largely shielded by sustained government demand for military goods and services," said SIPRI researcher Alexandra Marksteiner in the institute's annual assessment of arms companies.

"In much of the world, military spending grew and some governments even accelerated payments to the arms industry in order to mitigate the impact of the Covid-19 crisis."

The top five arms firms were all from the United States, Lockheed-Martin -- which counts F-35 fighter jets and various types of missiles among its bestsellers -- consolidating its first place with sales of $58.2 billion.

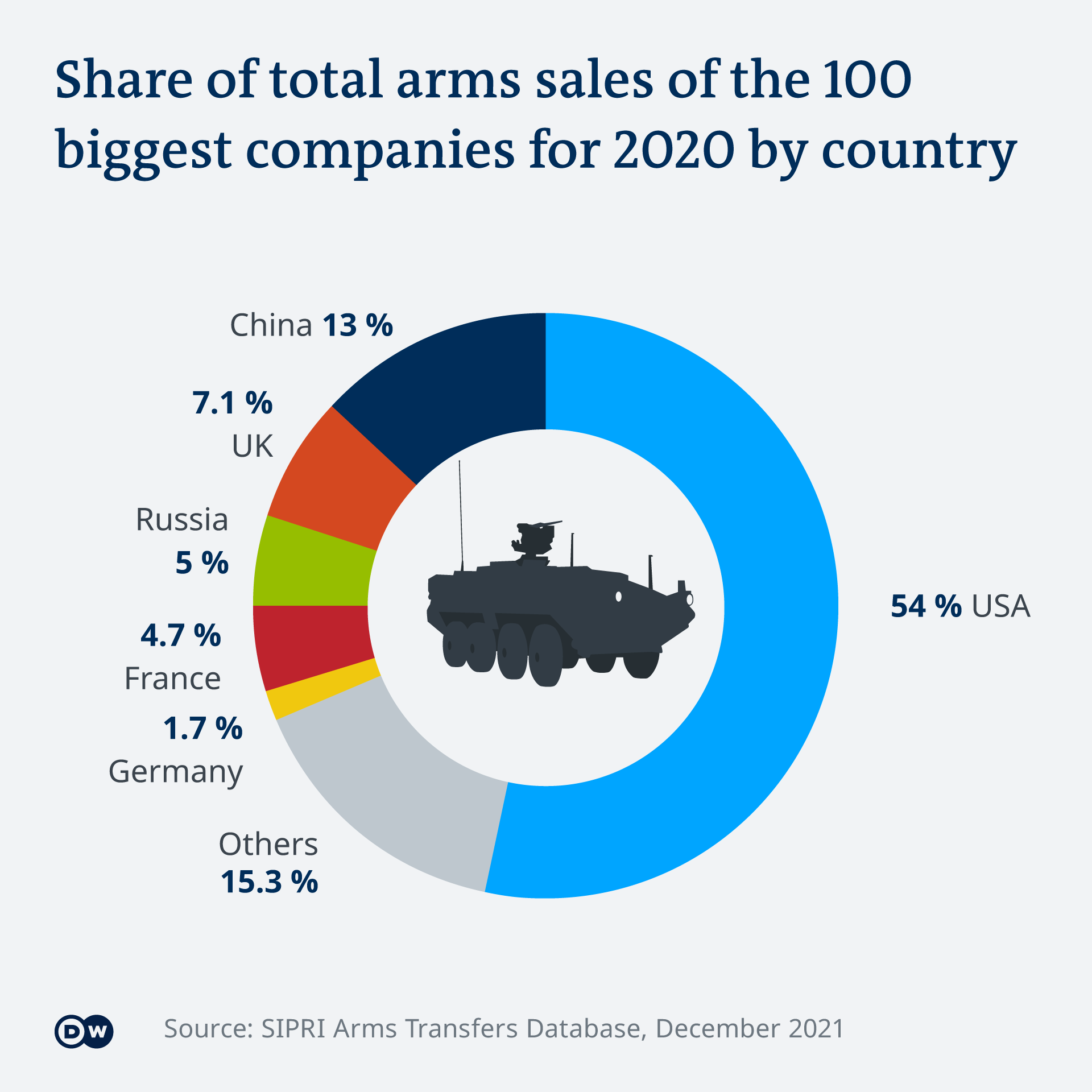

Britain's BAE Systems, in sixth position, was the highest-placed European firm, just ahead of three Chinese groups. - Rise of China -

"The rise of China as a major arms producer has been driven by its aim to become more self-reliant in weapons production and by the implementation of ambitious modernisation programmes," the report said.

While China's arms sales have expanded, they still lag US and British firms, accounting for a total of 13 percent of the top 100 arms sales in 2020.

Sales by the five Chinese firms in the top 100 totalled an estimated $66.8 billion in 2020, up 1.5 percent on the previous year.

"In recent years, Chinese arms companies have benefited from the country's military modernisation programmes and focus on military–civil fusion," SIPRI senior researcher Nan Tian said.

"They have become some of the most advanced military technology producers in the world."

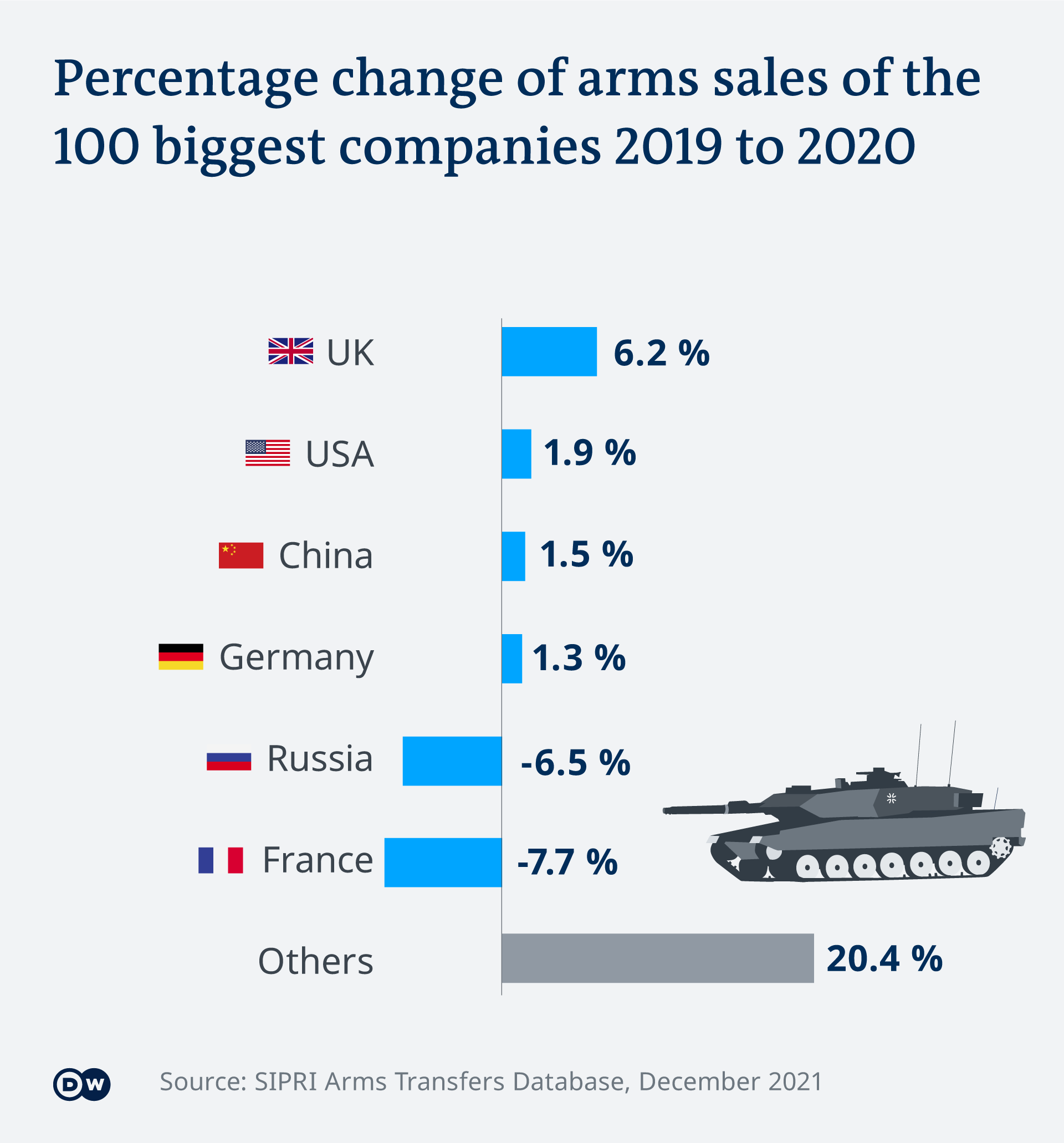

Of the top-producing countries, only France and Russia saw their firms' sales decline last year.

The institute said the firms had benefited from the broad injection of cash into economies, as well as specific measures designed to help arms companies such as accelerated payments or order schedules.

And as military contracts usually span several years, firms were able to make gains before the health crisis took hold.

"However, despite these and other factors, global arms production was not fully immune to the impact of the pandemic," the report said, pointing to France's Thales which blamed a 5.8 percent fall in arms sales on lockdown disruptions.

The report highlighted that the rate of increase in profits had slowed substantially between 2019 and 2020, and noted that measures taken to halt the spread of the virus had disrupted supply chains in the weapons industry just as they had across the wider economy.

SIPRI: Global arms industry flourishing despite COVID

A $531-billion business: The new SIPRI report shows that the world's top 100 arms producers have continued to increase sales — even in the pandemic year of 2020 and despite the global economy contracting.

Arms sales by German companies went up 1.3% in 2020, says SIPRI

Lockdowns, crumbling supply chains, jittery consumers: The COVID-19 pandemic has brought about massive economic slumps around the world. One sector, however, has proved immune to the virus: the arms industry. This is confirmed by the latest report on the world's 100 largest arms manufacturers by the Stockholm International Peace Research Institute (SIPRI).

SIPRI researcher Alexandra Marksteiner told DW that she was especially surprised by the data from 2020, the first year of the pandemic: "Even though the IMF put global economic contraction at 3.1%, we saw that the arms sales of these top 100 companies increased nonetheless — we saw an overall increase of 1.3%."

The sales of the top 100 arms manufacturers totalled $531 billion (€469 billion) in 2020, more than the economic output of Belgium. Some 54% of this was accounted for by the 41 US companies in SIPRI's top 100. The main companies in the industry are US-based: Lockheed Martin alone sold more than $58 billion worth of weapons systems last year — a sum bigger than the GDP of Lithuania.

Effective lobbying

Companies that big also wield political power. Markus Bayer, a political scientist at the Bonn International Centre for Conflict Studies (BICC), says arms companies are deliberately exerting influence. He quotes a report by the US NGO Open Secrets: "Defense companies spend millions every year lobbying politicians and donating to their campaigns. In the past two decades, their extensive network of lobbyists and donors have directed $285 million in campaign contributions and $2.5 billion in lobbying spending to influence defense policy."

And for the arms manufacturing giants, the spending appears to pay off. Alexandra Marksteiner explains that the US Department of Defense provided targeted support for the arms industry during the pandemic. "For example, they made sure that employees of defense companies were largely exempted from stay-at-home orders. On the other hand, there were some orders that were set up so that funds could be transferred to the companies a bit earlier, ahead of schedule, so that they would have a bit of a buffer."

Big Asian players

Simone Wisotzki has also examined SIPRI's new figures. An arms control expert at the Peace Research Institute Frankfurt (PRIF), she was especially struck by "the fact that arms companies from the Global South are becoming increasingly important." Wisotzki mentions India in particular: It has three companies in the top 100, whose combined sales total 1.2% — on a par with South Korea.

However, there are far more weapons leaving the factories of India's northern neighbor, China. SIPRI has been including Chinese companies in its studies since 2015, despite the many problems with transparency. China's five companies on the list are benefiting from the Chinese military's modernization program, and their shipments now account for 13% of the top 100's sales.

Wisotzki says India has not signed up to the international

arms agreement

Looking at the Chinese entries, Marksteiner notes that "these companies are capitalizing on what is called military-civilian fusion," citing the largest Chinese arms conglomerate as an example: "There was a satellite system that NORINCO co-developed, and it makes quite a bit of revenue from that, and it's used both for military and civilian purposes."

China has been modernizing its military

Militarized information technology

Simone Wisotzki also notes that the boundary between civil and military technologies is becoming increasingly blurred. "Information technology can no longer be separated from weapons technology," she says. In its new report, SIPRI specifically looks at the growing role tech companies play in the arms business.

Marksteiner emphasizes that, if you want a clear picture of the arms industry, "you can't just talk about traditional players like Lockheed Martin." SIPRI says that, in recent years, some Silicon Valley giants like Google, Microsoft and Oracle have sought to deepen their involvement in the arms business and have been rewarded with lucrative contracts.

SIPRI gives the example of a deal between Microsoft and the US Department of Defense worth $22 billion. The company has been contracted to supply the US Army with a type of super-glasses, called the Integrated Visual Augmentation System, which will provide soldiers with real-time strategic information about the battlefield.

The US military's interest in Silicon Valley is easy to explain. "They realize that, in these new enabling technologies, be it artificial intelligence or machine learning or cloud computing, these Silicon Valley companies' expertise is far beyond what you would see from traditional arms industry players," says Marksteiner. "There is a chance that some of these companies will actually end up entering the [SIPRI] top 100."

The line between technology for civilian use and miltary use is becoming increasingly blurred

Russia is falling behind

Along with France, the biggest drop in arms sales was recorded by Russia. The nine Russian companies on the list sold 6.5% fewer weapons last year than in 2019. The BICC's Markus Bayer believes this drop, to just 5% of the top 100's total sales, is directly related to India and China having developed arms factories of their own. Both countries were previously big buyers of Russian armaments.

Bayer cites the example of aircraft carriers. The first Chinese carrier was based on a Soviet-built ship purchased by Beijing in 1998. The Chinese carrier, named Liaoning, came into service in 2012.

A lot has happened since then, says Bayer. "In the last 20 years, China has not just caught up with Russia in terms of aircraft carrier production capabilities, it's overtaken it. Russia hasn't put a single aircraft carrier into service in that time. And now India has developed its own carrier as well, based on what was originally Soviet technology."

The Soviet aircraft carrier Warjag turned into the Chinese vessel Liaoning

Where does Europe stand?

The European arms industry has a combined 21% of the top 100's sales on its books. In 2020, the 26 European companies listed sold $109 billion worth of weapons. The four wholly German arms companies accounted for just under $9 billion of this total.

There are also trans-European companies like Airbus, which handled arms deals worth almost €12 billion — 5% more than in 2019. Europe is increasingly relying on joint ventures like these. Markus Bayer explains: "Europe is now trying, by political means, to expedite such cooperative ventures for the development of a 'Next Generation Weapon System,' the 'Future Combat Air System,' or the 'Main Ground Combat System,' so it can bear the high development costs for new systems like these."

These joint productions certainly make sense from a cost point of view. But as far as arms export control is concerned, they can often be problematic, says Simone Wisotzki. Referring to the Eurofighter Typhoon, a fighter jet developed by Germany, Britain, Italy and Spain, the PRIF analyst comments that "it is also specifically supplied to problematic third countries, such as Saudi Arabia, which is still waging war in Yemen." National export regulations are often not applied to joint productions — and it seems that Europe is still a long way from implementing effective joint controls on arms exports.

The global arms trade has long been a subject of scrutiny and debate, with its impacts reverberating across geopolitical landscapes. In recent years, significant shifts have occurred within this sphere, notably with France’s ascension as a major arms exporter on the world stage. This transformation raises pertinent questions regarding the underlying causes driving France’s newfound position and the implications it carries for international security dynamics. Examining the factors behind France’s rise in arms exports and the potential ramifications of this development is crucial for understanding contemporary geopolitical trends.

Between the periods of 2014–18 and 2019–23, arms exports from the United States, the leading arms provider globally, experienced a notable increase of 17 percent. Conversely, during the same timeframe, arms exports from Russia saw a substantial decline, plummeting by over half at 53 percent. Meanwhile, France’s arms exports witnessed a significant surge, growing by 47 percent, consequently propelling it ahead of Russia to claim the position of the world’s second-largest arms supplier.

In the period of 2019–23, as mentioned earlier France surpassed Russia to claim the position of the world’s second-largest exporter of major arms. French arms exports constituted 11 percent of all arms transfers during this timeframe, marking a notable increase of 47 percent compared to the period of 2014–18. In 2019–23, France supplied major arms to 64 countries, with India emerging as the largest recipient, accounting for 29 percent of French arms exports. The majority of France’s arms exports during this period were directed towards countries in Asia and Oceania (42 percent) and the Middle East (34 percent). Despite ongoing efforts to expand arms sales to other European nations, France’s exports to European states accounted for only 9.1 percent of its total arms exports in 2019–23. Notably, over half of its European arms exports (53 percent) were directed to Greece, primarily comprising transfers of 17 Rafale combat aircraft.

The Surge in France’s Arms Exports: Why?

France’s proactive export policies, including government support, technological advancements, and strategic targeting of regions like the Middle East, fueled a rise in arms exports during the period. This positioned them to capitalize on Russia’s decline as a major exporter following the Ukraine war, allowing France to secure the number two spot with advanced weaponry like the Rafale fighter jet.

It’s noteworthy that India stands as the largest arms importer globally, with France and Russia supplying 33 percent and 36 percent of its imports, respectively. In July 2023, New Delhi granted preliminary approval for the acquisition of six Scorpène submarines and 26 Rafale jets for the Indian Navy. Shortly thereafter, on July 25, reports from France’s La Tribune newspaper indicated Qatar’s contemplation of adding an additional 24 Rafales to its arsenal. According to the Stockholm International Peace Research Institute (SIPRI) report released in March 2023, France’s share of the global arms trade surged to 11 percent between 2018 and 2022, compared to 7.1 percent in the preceding four-year period. Conversely, Russia’s share of the international arms trade dwindled from 22 to 16 percent during the same period. So, this can be one of the indicators.

Figure 1: The 25 largest exporters of major arms and their main recipients, 2019–23

The imposition of multiple rounds of international sanctions on Russia may have hindered its ability to access the necessary materials for arms production, thereby hampering its export capabilities. Reports from Ukraine have cast doubt on the efficacy of Russia-built armaments, tarnishing their reputation on the global stage. Some importers have expressed dissatisfaction with Russian products in recent years. India, a longstanding importer of Russian arms suppliers, has raised concerns about the technical performance of Russian weaponry. As noted by Pieter Wezeman, the author of the SIPRI report 2023, India’s discontent has prompted a shift towards sourcing arms from France.

Furthermore, the United States wields significant influence over countries procuring weapons from Russia, a trend that predates the Ukraine conflict, according to Wezeman. For instance, Indonesia opted to abandon a planned purchase of Russian aircraft in 2021 in favor of options from the US and France.

A significant surge in the delivery of Rafale combat aircraft played a pivotal role in driving the growth of French arms exports during the period of 2019–23. In the preceding period of 2014–18, France exported 23 Rafales, a number that skyrocketed to 94 in the subsequent period of 2019–23. Remarkably, these exports accounted for nearly one third (31 percent) of French arms exports during this timeframe. Furthermore, the pipeline for Rafale exports remained robust, with an additional 193 Rafales on order for export by the end of 2023. However, it is noteworthy that the majority of the Rafale aircraft already delivered (96 out of 117) and those on order (178 out of 193) are destined for states outside Europe, including Egypt, India, Indonesia, Qatar, and the United Arab Emirates. This underscores the persistent challenge France encounters in selling its major arms to European states, particularly amidst fierce competition from the United States. Notably, out of the 10 European states that preselected or ordered combat aircraft in the period of 2019–23, eight opted for US F-16s or F-35s, with only Croatia and Greece opting for the Rafale.

In addition to bolstering its sales of combat aircraft, France also witnessed a 14 percent increase in exports of military ships, along with the weaponry required to equip them, between the periods of 2014–18 and 2019–23.

Figure 2: Global share of exports of major arms by the 10 largest exporters, 2019–23

Therefore the Rafale fighter jet, manufactured by Dassault Aviation, has emerged as a cornerstone of France’s recent achievements in the realm of defense exports, according to Olivier Gras, the general secretary of EuroDéfense-France, an association based in Paris comprising civil and military officials. Despite entering service as early as 2002, it wasn’t until 2015 that the Rafale made its inaugural foray into the international market. Since then, these twin-engine jets have found homes in Greece, Qatar, India, and Egypt, with impending deployments to Croatia, Indonesia, and the United Arab Emirates, which placed an order for 80 Standard F4 Rafales in 2021. The global tally of Rafale deliveries and orders now stands at nearly 500, representing approximately half the volume of its primary American counterpart, Lockheed Martin’s F-35. Moreover, potential orders from additional countries are on the horizon, with Colombia nearing a deal for 16 aircraft while Serbia, historically aligned with Russia’s arms industry, contemplates acquiring 12 planes.

Global military expenditure experienced a significant increase of 9 percent from the previous year, reaching a historic high of $2.2 trillion in 2023. This surge was attributed to heightened insecurity worldwide, fueled by numerous conflicts, as indicated by a recent report from the International Institute for Strategic Studies. Meanwhile, NATO’s budget hike can influence other actors in two ways. First, it sets a precedent. By collectively investing more, NATO strengthens the message of shared security concerns. This can pressure members who haven’t met spending targets to step up. Second, a larger NATO budget allows for more joint exercises and capabilities, potentially making individual militaries seem less essential. This might nudge some countries towards increasing their own budgets to maintain their national defense posture. And here France was an option to spend on.

Figure 3: Changes in volume of exports of major arms since 2014–18 by the 10 largest exporters in 2019–23

Who are the Importers?

In the period spanning 2019–23, the primary suppliers of major arms to Africa included Russia, constituting 24 percent of African imports, followed by the USA at 16 percent, China at 13 percent, and France at 10 percent. France emerged as the third-largest supplier to sub-Saharan Africa during this period, capturing an 11 percent share of subregional arms imports. Turning to South America, France assumed a prominent position as the leading supplier, contributing 23 percent of subregional imports. Meanwhile, in the Middle East, the United States dominated arms imports, commanding a significant share of 52 percent. Following the USA, France emerged as the next significant supplier, accounting for 12 percent of Middle Eastern arms imports, alongside Italy at 10 percent and Germany at 7.1 percent.

Qatar’s arms imports during the same period predominantly came from the United States, representing 45 percent of Qatari arms imports, followed by France at 25 percent and Italy at 15 percent. Notably, Qatar’s acquisitions included 36 combat aircraft from France, 36 from the USA, and 25 from the UK, in addition to 4 frigates procured from Italy.

Implications of Rising Arms Exports

The surge in arms exports across the globe is poised to have far-reaching implications, reshaping geopolitical dynamics and fostering a climate of heightened tension and competition. As importing countries bolster their military capabilities, several key implications emerge.

Firstly, heightened arms imports are likely to exacerbate existing tensions in importing countries and their surrounding regions. The influx of sophisticated weaponry may fuel regional rivalries and increase the likelihood of conflict, raising concerns about stability and security.

Secondly, importing countries are expected to allocate a larger portion of their budgets towards defense expenditures, reflecting a shift in their strategic priorities. The growing defense budgets signal a commitment to enhancing military capabilities and preparedness in response to perceived threats and geopolitical uncertainties.

Thirdly, the influx of arms into different regions, driven by increased exports from major suppliers, is poised to contribute to a proliferation of armaments. This proliferation not only amplifies the potential for conflict but also complicates efforts towards disarmament and non-proliferation initiatives.

Fourthly, Eastern Europe, already a region marked by geopolitical tensions and historical rivalries, is likely to experience further strain as arms imports increase. The influx of weaponry, coupled with ongoing political disputes, could exacerbate existing conflicts and raise the risk of escalation.

Fifthly, the surge in arms exports is expected to intensify competition among major exporters, particularly China, France, and Russia. As these countries vie for market share and influence, competition in the global arms trade is set to escalate, potentially leading to new marketing strategies and geopolitical maneuvering.

Sixthly, the rise in arms exports is likely to contribute to heightened polarization among nations, as countries align themselves with different suppliers based on strategic interests and geopolitical considerations. This polarization may further exacerbate regional tensions and complicate efforts towards diplomatic resolution of conflicts.

Finally, India’s increased arms imports from France, despite its longstanding relationship with Russia, signal a significant shift in procurement patterns. This shift underscores India’s strategic diversification efforts and reflects evolving geopolitical dynamics in the region.

The surge in arms exports has profound implications for global security and stability, with tensions likely to rise in importing countries and their respective regions. The growing competition among arms exporters, coupled with increased defense budgets and regional rivalries, underscores the need for concerted efforts towards arms control, disarmament, and diplomatic dialogue to mitigate the risk of conflict and promote peace and security on a global scale.

The elevation of France as a major arms exporter in the world marks a significant juncture in the evolving dynamics of the global arms trade. While driven by various factors such as strategic partnerships, technological advancements, and evolving defense policies, France’s newfound position underscores its growing influence in international security affairs. However, amidst the shifting landscape of arms proliferation, it becomes imperative for policymakers and stakeholders to carefully assess the implications of this trend on regional stability, conflict dynamics, and the broader geopolitical landscape. Through informed analysis and proactive engagement, efforts can be directed towards fostering a more secure and stable global environment.

Syed Raiyan Amir Research Associate The Center for Bangladesh and Global Affairs (CBGA)