China’s aluminum factories are changing to escape a crushing price war

For Liang Zhu, who runs an aluminum factory about 100 kilometers north of Hong Kong, there is only one way out of China’s vicious spiral of excessive competition: shift away from inexpensive metal for window frames and door handles, and toward the specialized alternatives needed for iPads and airplanes.

Guangdong province has long been a powerhouse of light manufacturing. Today, though, many companies like Liang’s are battling to survive in the era of “involution”, a term commonly used to describe the country’s intense, self-harming industrial race. China’s property boom is over, and has left behind small to medium-sized manufacturers saddled with overcapacity, evaporating margins and a relentless struggle for customers.

“Without sufficient profits, there will be no funds to invest in innovation, research or in finding solutions for society,” said Liang, general manager at Guangdong Mingzhu Metal Material Technology Co., a company he founded after returning from a spell working in Australia. “That’s a dilemma for us, so we look for ways to get out of this so-called involution.”

Producers of aluminum to be used in railings or furniture thrived in Guangdong from the early reform years of the 1980s up until the country’s real estate crisis began in earnest five years ago. Since then, the region has seen a wave of consolidation.

In July, Mingzhu Metal started up its first production line making items with “7-series” aluminum, a more complex product that’s harder to rework and weld, more resistant to heat and easier to crack when cooling. Most importantly, it has lucrative buyers in China’s emerging higher-value industries — from aerospace to electric vehicles and consumer goods.

Aluminum is arguably the world’s most versatile metal because it’s lightweight, durable and doesn’t rust. Extruders, as companies like Liang’s outfit are known, take thick bars of semi-finished metal and work it through several phases to form different shapes and profiles, from car frames to supports for solar panels.

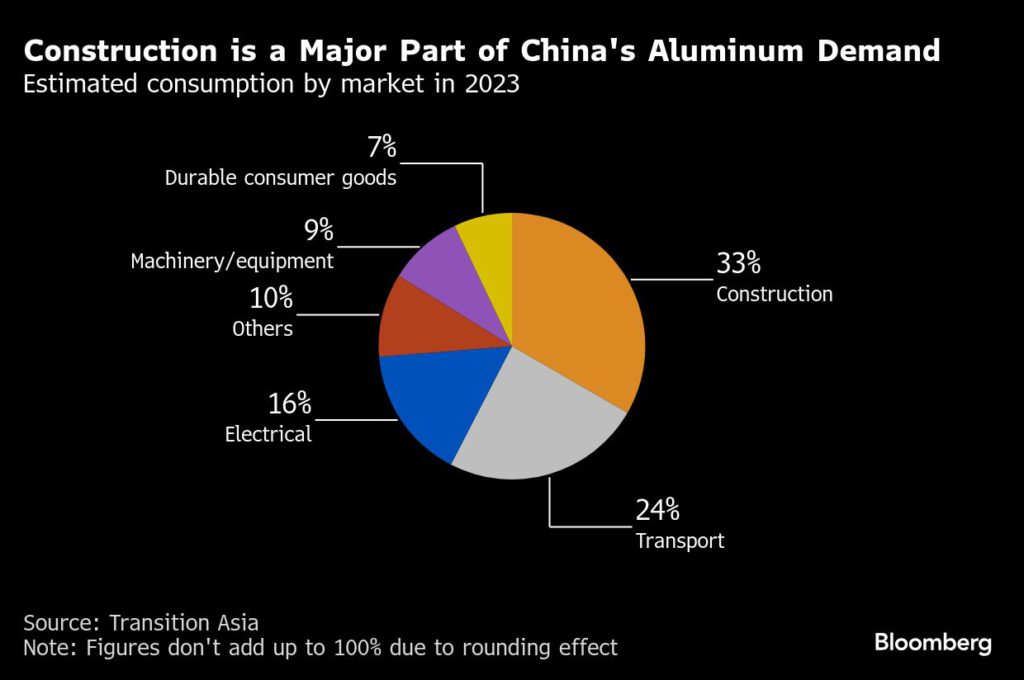

This corner of the sector has long relied on real estate and infrastructure, so the collapse of construction activity since the start of the pandemic has been devastating. Operating rates for aluminum processors are at about 60% to 70% for the best-performing companies, and at only 40% to 50% for the weaker ones, according to researcher Shanghai Metals Market, or SMM. Both are below the 80% level deemed a healthy minimum.

Midstream aluminum producers are “facing complex situations such as weak domestic demand, increased uncertainty in foreign trade, and intensified internal competition in the industry,” the China Nonferrous Metals Industry Association said in July. “The price competition situation is quite severe, and overall processing fees have reached an historic low.”

Shandong Nanshan Aluminum Co., a major producer of extrusions in eastern China, is a case in point. The firm said last week it’ll close 120,000 tons of its total 320,000 tons of capacity after recording utilization rates of just 59%. It plans to shift its focus to higher-end products for industry and autos.

President Xi Jinping has said he wants to “break involution,” which means reducing the excessive competition and capacity levels blamed both for a cycle of domestic deflation and raising tensions with trade partners.

The campaign is taking different forms across industries. Nationwide coal output declined in July from a year ago, after government inspectors targeted mines that produce too much. Oil refining and petrochemicals are set for a sweeping overhaul. And bosses from electric vehicle companies and some tech giants have been called before regulators and warned about over-competition.

An hour’s drive from Mingzhu Metal is China’s “aluminum capital” of Foshan, known for its panoply of extruders, fabricators and wholesale markets. Here, Foshan Golden Source Precision Manufacturing Co. has passed through several phases of specialization and technological upgrades since it was founded in the early 1990s.

Its showroom exhibits include trailer ramps and bathroom fittings to hard disk components and parts for the Harmony trains that pioneered China’s high-speed rail. The firm has hewn closely to the technological path prescribed by Xi’s Made in China 2025 plan that was launched a decade ago.

Most recently, Golden Source has developed components for EV charging points and lightweight fittings for airplane trolleys. When General Manager Rain Tam took over the business from her father, its founder, she raised spending on technological research in order to cut costs and to improve product quality.

Even then, there is intense competition.

“Technological innovation helps profit margins for some products, but overall our margins will be a lot worse this year than last,” said Wang Shunli, deputy general manager. “Right now, when it comes to pricing, I feel the pressure is extremely high.”

China’s last round of industrial supply reforms after 2015 heralded changes across the sector, from the smelters that produce aluminum to the factories that handle the metal. For extruders, strict new controls on carbon emissions and energy consumption put the squeeze on smaller, less efficient firms.

That’s left an environment that is complex, but also modestly positive. Chinese demand for the metal is set to grow 3.4% this year, according to Bloomberg Intelligence. China Hongqiao Group Co., the biggest primary aluminum producer, gave an upbeat outlook after it reported a rise in first-half earnings.

“Overall aluminum consumption is trending upward, but the main issues are rapid capacity expansion and severe product homogenization,” said SMM analyst Liu Xiaolei. “The aluminum industry is shifting toward new energy sectors, but these are also experiencing clear overcapacity.”

In Guangdong, managers and factory workers are settling in for a long battle. Unlike Xi’s last round of supply-side reforms, there’s little prospect of massive stimulus or a renewed construction boom to restore the growth rates of the past.

“The whole industry is experiencing a test,” said Golden Precision’s Wang. “For now, we need to survive first, so that we can advance more in five, seven, eight years.”

The U.S. and China Are Battling for Control of the World’s Bauxite Supply

- The global alumina and bauxite market is projected to grow from $84.5 billion in 2025 to $125.9 billion by 2033 at a 5.11% CAGR.

- The U.S. and China are vying for global bauxite supply, with China consuming over 60% of traded bauxite and the U.S. importing 75% of its needs.

- Guinea’s concession revocation, Rio Tinto’s $180M expansion, and stable Q2 2025 prices highlight both opportunities and risks for the sector.

Despite a few hiccups and occasional worries of oversupply, the global bauxite market has been growing steadily. Much of this expansion has been fueled by rising demand in the aluminum market, especially from automotive, aerospace and renewable energy sectors.

About 60% of EV manufacturers and over 70% of aerospace materials use aluminum in one form or another. Moreover, about 85% of bauxite is used for alumina production. Because of these facts, the global alumina and bauxite market is projected to grow from US $84.51 billion in 2025 to US $125.91 billion by 2033, at a CAGR of 5.11%. This means opportunity, but also the potential for volatility. Steps to manage the downstream volatility which can occur as a result of these supply chain disruptions are covered in MetalMiner’s Weekly Newsletter.

The U.S. and China Now Vying for Global Supply

Sector analysts believe the bauxite market, and by extension the aluminum market, is undergoing a strategic transformation. This hinges on the fact that the U.S. is expanding in domestic mining capacity, while the other major player, China, is vying for control over global bauxite resources.

The latter is the world’s largest aluminum producer, consuming over 60% of globally traded bauxite, much of it sourced from Guinea and Australia. On the other hand, the U.S. largely imports its bauxite, to the tune of about 75%. As aluminum market demand heads up, the United States wants to reduce this reliance on foreign supply.

The U.S. and the rest of North America have long relied on the Asia-Pacific region for bauxite. That area currently dominates the global market, with a 45% share of reserves. However, Africa and the Middle East follow closely. Guinea, for example, has about 24% of global reserves. And while Australia leads in exports, China is still numero uno in refining, followed by Saudi Arabia and the UAE.

Guinea’s Recent Moves

In a decisive move to assert control over its mineral resources, Guinea recently revoked a major bauxite concession from the UAE’s Guinea Alumina Corporation (GAC), citing failure to build a promised alumina refinery. The decree transferred the Boké concession from Emirates Global Aluminium (EGA) to a new state-owned entity, Nimba Mining Company, for a duration of 25 years.

GAC, which exported 18 million tons in 2024, plans to challenge the decision through international arbitration, calling it a wrongful termination. Some experts believe this could also change some of the dynamics where the U.S. is concerned, since the country relies on Guinea for at least some part of its bauxite supply.

More Investments

Even as the U.S. goes about expanding mining capacity, major aluminum market players like Rio Tinto are making moves to add to the overall bauxite supply. That company recently invested a significant amount of resources into its Australian operations, committing US $180 million to expand bauxite access at the Amrun mine in Queensland. Initial production is expected in 2027, with a full ramp-up by 2028.

Price Range

The sturdiness of the bauxite and aluminum market is reflected in global bauxite prices, which have remained relatively stable in Q2 2025. This is mainly the result of a complex interplay of supply chain disruptions, environmental regulations, and robust demand from the aluminum sector.

In the U.S., Q2 prices held at $82/MT thanks to consistent demand from aluminum smelters and refractory industries. Meanwhile, import reliance and freight delays pushed up landed costs, while environmental rules and labor shortages strained mining logistics. In China, Q2 prices rose to $99/MT amid strong industrial demand and domestic supply disruptions. Simultaneously, tight import availability and shipping delays from Southeast Asia and West Africa further constrained sourcing.

With aluminum demand accelerating and countries like the U.S. and Australia investing in strategic supply chains, the bauxite market seems poised for long-term expansion. But certain challenges do lie in its path. These include environmental constraints like red mud disposal, which adds up to 50% in operational costs, as well as certain geopolitical risks and the resulting price volatility.

By Metal Miner

No comments:

Post a Comment