It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Saturday, July 11, 2026

Foreship Develops Energy-Efficient Ferry Design for Greek Domestic Market

Foreship, the naval architecture and marine engineering company of RINA, has developed a new ferry concept tailored to the specific operational and economic requirements of the Greek domestic market, with a focus on efficiency, simplicity and cost control.

Greece’s ferry network is one of the most extensive in Europe, connecting more than 200 inhabited islands and transporting around 50 million passengers annually. At the same time, operators are working within a highly constrained environment, shaped by strong seasonality, regulated pricing and increasing pressure on operating costs, alongside the need to renew an ageing fleet.

Ari Huttunen, Marine Design & Engineering Projects Principal Consultant at Foreship, said, “This new vessel concept has been developed in response to the specific challenges of the Greek market, with a focus on optimising both capital and operating expenditure. The design integrates all essential functionalities for safe and reliable operations, while avoiding unnecessary complexity, resulting in a robust and economically sustainable vessel.”

A central element of the concept is the operating profile. While speed has traditionally been a defining factor in the Greek ferry sector, the new design is optimised for more moderate speeds, enabling a significant improvement in fuel efficiency and overall operating economics.

The vessel has also been conceived in line with the latest regulatory developments, including updated stability requirements that are reshaping ferry design across Europe and influencing aspects such as dimensions and passenger capacity. These changes have been taken into account from the early design stages, ensuring the concept remains aligned with the evolving framework.

By shaping design choices in the realities of the Greek ferry sector, including cost sensitivity, operational intensity during peak periods and the need for reliable, straightforward vessels, the concept provides a practical reference point for future fleet renewal.

The products and services herein described in this press release are not endorsed by The Maritime Executiv

GTT New Order from Samsung Heavy Industries for Tank Design of FLNG Unit

GTT announces that it has received, in the second quarter of 2026, an order from Samsung Heavy Industries shipyard for the tank design of Delfin FLNG 1, a floating liquefied natural gas unit (FLNG) to be built for the Delfin LNG project.

Delfin FLNG 1 will be the first floating liquefied natural gas unit to enter service in the United States, as well as the world’s largest in terms of expected production capacity (4.4 million tonnes of LNG1 per year).

As part of this order, GTT will design the cryogenic tanks of the unit, which will offer a total LNG storage capacity of 180,000 m³. The eight tanks will be arranged in two rows and will incorporate GTT’s Mark III Flex membrane containment system, suitable for demanding maritime and offshore applications, including operations in a region exposed to hurricane conditions.

Delfin FLNG 1, which will be operated off the coast of Louisiana, is scheduled for delivery in mid-2030.

François Michel, CEO of GTT, declared: “With Delfin FLNG 1, offshore LNG is entering a new phase in the United States. This project, unprecedented in scale, will contribute to the development of new LNG production capacity to meet global energy demand. It also illustrates the ability of GTT’s membrane technologies to support complex offshore projects facing demanding operational constraints, while meeting the highest standards of performance, reliability and safety."

The products and services herein described in this press release are not endorsed by The Maritime Executive.

Steel Cut for Carnival Cruise Line’s Next Mega Ship, Carnival Destiny

At approximately 230,000 gross tons the new Carnival Destiny will be among the largest cruise ships in the world (Carnival Cruise Line)

Fincantieri and Carnival Cruise Line celebrated the first steel cut for the line’s new cruise ship, which will be the largest built by Fincantieri and the largest built in Italy as the line becomes the next to jump the 200,000 gross tons milestone. Expected to be approximately 25 percent larger than Carnival’s current largest cruise ship, the line is harkening back to another revolutionary ship, announcing the new ship will be named Carnival Destiny.

Scheduled for delivery in the summer of 2029, the new Carnival Destiny will be approximately 230,000 gross tons. The ship will feature more than 3,000 passenger cabins and will accommodate over 8,000 passengers at full capacity. It is the first of three ships on order in Carnival’s new Ace Class, with sisters scheduled for delivery in 2031 and 2033.

"Carnival Destiny builds on a legacy that changed cruising once before, reimagining what guests can experience at sea," said Christine Duffy, president of Carnival Cruise Line. "With this ship, we're elevating the guest experience again creating a ship that feels more expansive, while helping guests feel more connected and ultimately have more fun."

According to the company, the ship will introduce a new way of experiencing the ocean. It incorporates Fincantieri’s concepts connecting passengers to the sea, with Carnival saying the new ship will “become the most outward-facing megaship at sea. The line points to more than 4.5 acres of glass, which it says will open up sightlines across the vessel. The ship will “create ocean views from more places on board.”

Carnival is also saying the ship will be evolutionary in how passengers engage on board. More than 70 percent of the venues and attractions will be new concepts for Carnival. It promises reimagined dining, bars and lounges, immersive entertainment, and vibrant outdoor spaces.

The first Carnival Destiny, launched 30 years ago, was the industry's first 100,000 gross ton cruise ship (Carnival)

The name Carnival Destiny was chosen to highlight the company’s heritage in pioneering and the long relationship with Fincantieri. The Italian shipyard delivered the first Carnival Destiny 30 years ago. The ship was the first passenger ship to exceed 100,000 gross tons. Carnival says it changed the industry, including expanding the availability of balcony cabins and new venues. Renamed Carnival Sunshine in 2013, the ship continues as part of the fleet.

The ceremony took place at the shipbuilder’s main production site in Monfalcone, Italy. It highlights that it has built 76 cruise ships for the brands of Carnival Corporation, including 15 cruise ships for Carnival Cruise Line. They highlight that the ship, which will be powered by LNG, will be equipped with advanced technologies aimed at improving energy efficiency, waste management, and emissions reduction.

Carnival Cruise Line will become the fourth cruise line after Royal Caribbean International, MSC Cruises, and Disney Cruise Line to surpass the 200,000 gross ton mark. Fincantieri will also build mega cruise ships over 200,000 gross tons for Norwegian Cruise Line. It is part of a trend among the mainstream contemporary brands that continue to upsize their vessels to add new amenities and realize economic efficiencies in their operations.

Delfin LNG Clears Legal Hurdle as Court Dismisses Environmental Claims

Rendering of the Delfin project which will be the first FLNG in the United States (Delfin)

The U.S. Court of Appeals for the Fifth Circuit yesterday denied a petition for review in a legal challenge to the Maritime Administration’s issuance of a deepwater port license to Delfin LNG. The environmental groups had challenged the approval, which was granted in March 2025 for the deepwater port facility to be located approximately 40 miles off the Louisiana coast for the export of LNG to the global market.

In denying the petition, the court held that three environmental groups failed to establish standing. The court did not rule on the merits of the case because the petitioners did not show any injury that might be traced to the challenged project.

“The Fifth Circuit’s ruling will make it harder for environmental groups — who have no stake in important energy projects — to challenge projects that will bring jobs and prosperity to Americans,” said Principal Deputy Assistant Attorney General Adam Gustafson of the Justice Department’s Energy and Natural Resources Division (ENRD).

The Maritime Administration first authorized the port in 2017 and issued the final licenses for the project in March 2025. Delfin Midstream and its investor group last month announced they had reached a financial investment decision to proceed with Delfin FLNG 1, which will become the first floating LNG project in the United States and the largest FLNG project globally.

To be positioned off the coast of Louisiana, the project is expected to have an initial export capacity of 4.4 million tonnes of LNG per year. It is the first stage of a proposed project that would have a total capacity of 13.2 MTPA based entirely on FLNGs. The investors for the project are being led by Global Infrastructure Partners, part of BlackRock. Mitsui O.S.K. has been an investor since 2023 and looks to contribute its expertise in LNG transport. Vitol, an energy and commodities trader, and Diameter Capital Partners have also agreed to invest in the first phase of the project.

“This commonsense ruling ensures that this vital energy infrastructure project won't be derailed,” said Maritime Administrator Stephen Carmel. The U.S. Department of Transportation’s Maritime Administration (MARAD) reports it will move forward with issuing a Deepwater port license to Delfin LNG following a decision by the U.S. Court of Appeals for the Fifth Circuit

Delfin FLNG 1 has already secured commitments for long-term LNG sales agreements with leading global energy companies, including Vitol, Expand Energy, Centrica, and Gunvor. They expect the first vessel to be operational by 2030.

EU Parliament Votes to Block Irish Alumina Plant's Sales to Russia

The European Parliament has expressed its displeasure with an ongoing, militarily-relevant trade route between Ireland and Russia. The EU's largest alumina plant is in County Limerick, Ireland, and it ships the majority of its output to Russia. After years of controversy, the European Parliament has passed a non-binding motion requesting the European Commission to put a blanket ban on all sales of alumina to Russian buyers, which would shut down the route and undermine the plant's business.

The dust-up involves Aughinish Alumina, a Russian-owned plant on Ireland's western coast. In March, the investigative outlet OCCRP and the Irish Times published a detailed report on Aughinish's role in the Russian defense supply chain. The plant is the largest bauxite-to-alumina refinery in Europe, and is part of a vertically integrated supply chain for Russian metals conglomerate Rusal. OCCRP's data shows that most of its bauxite feedstock comes from Rusal-owned mines in Africa and South America, and more than half of the plant's alumina output goes to Rusal smelters in Russia, which turn the commodity into aluminum. Rusal then sells the aluminum to an intermediary that supplies Russan defense manufacturers - many of which are sanctioned by the EU. Given how these end products are used, OCCRP concludes that some of that aluminum ends up in Ukraine in the airframes and components of Russian weapons systems.

The EU bans imports of aluminum metal from Russia, but has no restrictions on exports of alumina to Russia. Though the sales may be controversial, Aughinish is fully compliant with all existing regulations, and the firm emphasized this in comments to OCCRP.

Four years into the war, the EC has not yet put sanctions on this niche EU trade with Russia, which is essentially coterminous with the Aughinish plant's export operations. The plant's managers have previously said that without exports to Russia, only a government buyout would prevent large-scale layoffs - something that Ireland has sought to avoid.

After OCCRP's coverage, the outlook may change. The European Parliament voted Wednesday to pass a resolution in support of sanctions to prohibit the sale of European alumina to Russia. The petition supports action by the European Commission which has the sole power to propose sanctions. Any single EU member state can block an EC-proposed sanctions measure.

Most Irish MEPs supported the resolution, despite the effects on the local economy in Limerick.

"It is highly likely alumina exported from Ireland is being used in the Russian military and that these exports have increased since 2022. It is also now clearer that the beneficial owner of the company is still a pro-Putin oligarch," MEP Barry Andrews told The Irish Times. "If this is confirmed, the Irish Government must urgently work with our EU partners to close off these exports."

The United Kingdom is teaming up with the Netherlands to produce a fleet of new amphibious landing ships. The plan ties British Royal Marines and Dutch Korps Mariniers even closer together after decades of pre-existing close cooperation. The Maritime Executive reported last week on the pending announcement, and a formal announcement about the shipbuilding plan was made at the NATO summit in Ankara, Turkey, on July 7.

The plan appears to be more ambitious than previously thought. Both the UK and the Netherlands will each get four ships, to be operated as national assets, but frequently deployed together, whether in the High North or in the Caribbean, where both countries retain a sovereign footprint.

The ships are to be based on the pre-existing Damen Enforcer 15628 design, and revive a concept developed under the Anglo-Dutch Project Catherina, which the Dutch kept alive after the British withdrew in 2024. The new ships, 160 meters long (525 feet) and 15,000 tonnes, are larger than existing designs floated by Damen, but clearly take advantage of Damen’s previous experience.

The ships, it seems, will have a well deck from which to launch two landing craft and side hoists to launch raiding craft. The flight deck will have two helicopter spots, and a hangar able to accommodate four medium-sized helicopters. Whether from the flight or well deck, or using the davits, a variety of both sea and air autonomous vehicles can be sent on their way.

It is not clear how up-to-date the plans are for the defense of these platforms from both sea and aerial drones. The Enforcer 15628 design has a 76mm forward and two 30mm guns, a Phalanx for close-in protection, and a decoy system, but apparently no vertical missile launch system. Whether, as currently configured, this would be sufficient for such a ship to make a transit alone, for example, through the Bab el Mandeb, is no doubt a point of contention being pondered as the design of the class is finalized. Vulnerability to drones is already a global constant, not restricted any longer to narrows or choke points.

The configuration of the ships will make them both unique but also highly suited to the launch of autonomous systems, and one can well envisage that in times to come there will be a tussle for priority use of these platforms between those wanting to thicken up the capability of task forces conducting conventional operations, and their use as amphibious launch platforms for marines. They would, for example, be ideally suited for mounting the mine clearance force with its autonomous equipment, which is currently deployed on the RFA Lyme Bay (L3007). Each ship can accommodate about 500 marines, depending on the duration of the deployment.

One suspects that an order for four ships will be insufficient to meet the various demands from naval operational planners, but at least in the interim, the cooperation agreement between the UK and the Netherlands may be able to alleviate some of the pressure at times of stress.

The British announcement indicated that the UK’s ships would be built in the UK. This would be a good follow-on order for Navantia’s Harland & Wolf yard in Belfast, once the fleet solid support ships are completed, but there may be competition for the work from shipyards not too far distant from Manchester, such as a rejuvenated Balaena Cammel Laird operation.

Leveraging Damen’s experience in the area reduces risk, design and development time, and budgets permitting, will speed getting these ships into service. This will be particularly appreciated by the Royal Marines, who in effect have lost much of their amphibious lift capacity with the early retirement of HMS Albion (L14) and HMS Bulwark (L15), with the Bay Class landing ships operated by the RFA likely to be soon following in their wake.

Pakistan Begins Construction on its First Containership Since the 1980s

Karachi Shipyard, the only domestic shipbuilder, has begun assembly of containership (KS&EW)

As part of a broader government initiative to leverage the country’s blue economy, Pakistan has begun the construction of its first large commercial ship, a containership, since the industry largely stalled in the 1980s. Assembly of the vessel has begun at the country’s only shipyard, and it is expected to contribute to the economy and save the country vital foreign exchange costs.

The Karachi Shipyard & Engineering Works is building the vessel, which will have a capacity of 1,100 TEU, for the state-run Pakistan National Shipping Corporation. The project was first announced in 2024, with a contract signing in February 2024, but it had stalled due to financial challenges in Pakistan. The government stepped in to help revive the project, and steel cutting began in January 2026.

Steel cutting for the vessel has now been completed, and assembly has begun. Reports indicate that the last commercial ship was built more than 40 years ago, with the yard mostly working on frigates, corvettes, fleet tankers, and logistics ships for the Pakistan Navy. However, it highlights that it has the capacity to build vessels up to 26,000 dwt, including bulkers, tankers, dredgers, ferries, fishing boats, and tugs.

The government launched a task force in 2024 to examine the opportunities to expand Pakistan’s maritime economy. Reports indicate that it identified 99 bottlenecks and so far has been able to implement solutions for 84 of the challenges.

The government recognized that there were large financial barriers, and it agreed to abolish a 22 percent sales tax on vessel purchases and shipbuilding materials. It highlights that neighboring countries, including India, subsidize shipbuilding by up to 30 percent. By reforming its financial policies, it hopes to make Pakistan more attractive to shipowners. It notes that the country’s largest owners have in the past registered ships in Panama and Liberia.

In addition to reviving commercial shipbuilding, the government reports it is working to modernize the country’s port operations. It has reduced the customs clearance times, deployed advanced container scanners, and introduced 24-hour port operations.

Another portion of the plan seeks to revive the sagging shipbreaking sector. The business, which was among the largest in the world, collapsed due to financial pressures and new environmental mandates. Pakistan has become a signatory to the Hong Kong Convention and reports that five of the breaker yards have achieved full compliance.

Domestic shipbuilding, it reports, will save foreign exchange, and it believes it has the potential to become an exporter of new ships. It also notes that revitalizing the broader sector will also create new jobs.

Chinese Shipyards Double Their New Order Volume in First Half of 2026

A boxship for a large European container line appears behind China's latest aircraft carrier at CSSC Jiangnan Shipyard (Chinese social media)

In the first half, China's shipyards took on twice as many new orders as they did during the same period in 2025, according to the latest numbers from Clarksons.

Out of a total of 1,481 vessels ordered worldwide during the period, China took in 1,131 orders totaling 31 million compensated gross tonnes - about 72 percent of total market share, roughly equivalent to its dominant position in the industry in 2025. China has secured the majority of global shipbuilding orders for the last four years running, and continues to solidify its wide lead over its nearest competitor, South Korea.

The large Korean shipyards brought in 195 vessel orders totaling about eight million CGT - 60 percent more than they won during the same period last year, but far behind China, with just a fifth of global market share for the first half of this year. China's market share lead over Korea is expected to widen to 53 percentage points for the full year in 2026.

However, Korean yards are optimizing for profit rather than volume, and have been selective in picking orders. The Korean Big Three have secured a much higher proportion of the more profitable vessel classes - like LNG carriers, a longtime Korean specialty. Korea holds about two-thirds of the global orderbook for LNGCs, according to Wood Mac.

China has picked up far more of the high-volume, low-complexity, low-margin classes like small boxships and bulkers, but it is also winning some of the world's biggest accounts. MSC, the world's leading container line, now has a 100% Chinese orderbook for its gigantic and growing fleet. Already in possession of more than 1,000 container ships, MSC has another 128 on order - all in Chinese yards, according to Clarksons data.

US Navy Issued RFIs to Korean Shipbuilders for Destroyers and Oilers

US Admiral Steve Koehle visited the South Korean shipyards in 2025 to learn about their capabilities (Hanwha Ocean)

The United States Navy has formally requested information from South Korea’s leading shipbuilders regarding their capabilities to quickly build destroyers and oilers, according to media reports in Korea. The Korean news agency Yonhap revealed that the U.S. Navy had issued requests for information last month, marking the first formal requests since South Korea launched its “Make American Shipbuilding Great Again” commitments.

The RFIs reportedly came as Donald Trump asked South Korea’s President Lee Jae Myung, “Can you quickly build 10 U.S. warships?” The question was posed on the sidelines of the G7 summit in France in June. Media reports indicate that Trump and Lee met on the sidelines of the current NATO summit and agreed to launch a working-level consultation to explore the U.S. request for shipbuilding.

The RFIs were reportedly seeking details on the design capabilities and shipbuilding capacity of Korea’s leading shipbuilders. The U.S. government was gathering pricing information as well as delivery terms and other market information.

HD Hyundai Heavy Industries and Hanwha Ocean were asked to submit information for eight proposed destroyers. In a separate request, Samsung Heavy Industries, along with the two other yards, also responded with details for medium-sized naval tankers.

Yonhap quotes an industry source as saying, "We responded to the US RFIs by providing a comprehensive overview of the shipyards' capabilities, including their shipbuilding track record, design workforce and expertise, and annual shipbuilding capacity."

By Korea’s estimates, the U.S. Navy needs to add, on average, 12 ships a year to reach the Trump administration’s expansion plans. They report the U.S. Navy seeks to grow from its level of around 300 ships to 381 vessels by 2054. They estimate the U.S. will need to build 364 vessels over the next 30 years.

During the trade negotiations, Korea committed to a $150 billion investment into U.S. shipbuilding as part of a larger $350 billion investment in the United States. South Korea's government-backed policy banks moved forward last month with steps toward formalizing the financing plan for the initiative.

Reports indicate the Trump administration may be seeking ways to skirt around U.S. law, which currently prevents the building of navy ships overseas. The Byrnes-Tollefson Act from the 1960s says the U.S. Navy must build its ships in U.S. yards. The U.S. House Armed Services Committee took up the issue recently during its debate on the Defense Authorization Act and also reiterated that the Navy must use U.S. yards.

One possible action would be to use the yards in South Korea to work on the design and project plans and then have the companies work with their U.S.-based capabilities. Hanwha Ocean has already been seeking U.S. approval for building destroyers at the yard it acquired in Philadelphia, and it has announced plans for a large expansion of the yard and its capacity. Both HD Hyundai and Samsung formed partnerships in the United States. HD Hyundai is working with Huntington Ingalls Industries, and Samsung partnered with General Dynamics NASSCO.

The Korean shipyards have already begun work with the U.S. government. The yards have been carrying out maintenance and overhauls of USMSC vessels.

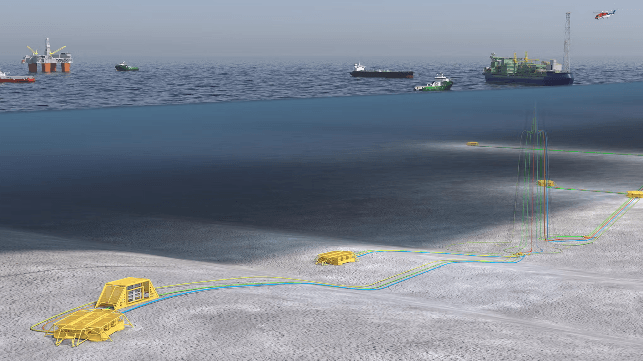

Equinor Buys Out BP's Stake in Bay du Nord Project off Newfoundland

Calm waters at the Bay du Nord project site (Illustration courtesy Equinor)

Equinor has bought out the interests of its partner BP in the Bay du Nord offshore field off the coast of Newfoundland and Labrador, making it full owner of a promising oil project in a famously difficult operating region.

"Over the past few years, we have strengthened Bay du Nord by improving the business case and reducing key risks. This transaction reflects our confidence in the project as we continue maturing it towards a final investment decision," said Equinor EVP Philippe Mathieu in a statement.

BP says that it is selling its 37 percent stake in 10 various Bay du Nord licenses in order to simplify its portfolio, maintain "strict capital discipline," and focus its attention on its highest-ROI projects. It will retain full ownership of two separate exploration licenses in the area, unrelated to its Equinor partnership.

Bay du Nord is a prospect in the Flemish Pass frontier basin, about 270 nautical miles to the east of St. John's. Statoil (now Equinor) took an interest in the basin in 1998, and drilled the Bay du Nord exploratory well C-78 in 2013. By 2017, it had drilled at five nearby sites in a cluster - Bay de Verde, Mizzen, Harpoon and Baccalieu.

Thirteen years later, the sites remain undeveloped, in part because the conditions are quite harsh. This region of the North Atlantic is known for severe storms and drifting icebergs, both hazardous for drilling and production operations. Icebergs can be managed by towing or nudging them away with anchor handling tugs, but this adds cost. In addition, the extra-long distance from shore means extra costs and extra time for transportation, both for goods and for personnel transfers.

Challenges notwithstanding, Equinor is progressing through the FEED process and looking for ways to make its FPSO-based development proposal less expensive. It plans to take a final investment decision on the $10 billion Bay du Nord project next year. The state-owned oil company believes that its experience on the Norwegian shelf has prepared it for the harsh North Atlantic conditions off Newfoundland. It also has relevant experience as a non-operating partner in the Hibernia and Hebron fields, both located next door to Flemish Pass.

China Begins to Return to the World Oil Market

Refinery at Ganjiaxiang, Nanjing (Vmenkov / CC BY SA 3.0)

China's withdrawal from the global oil market was one of the biggest surprises of the Strait of Hormuz shutdown. Shortly after Iran closed the strait in early March, China quietly banned exports of refined petroleum products and drastically cut its purchasing of foreign oil, taking the world's largest buyer off the market overnight - thereby offsetting the drop in Gulf supply and keeping a lid on crude prices. It has now lifted its prohibition on fuel exports, opening the door for privately-held refineries to resume purchasing foreign oil and exporting Chinese gas, diesel and jet fuel.

Market sources told Reuters that a division of Rongsheng Petrochemical, one of the largest independent refiners in China, has received an export permit to sell fuel to overseas buyers this month. Rongsheng has not confirmed the report, but if true, it would be the first private Chinese refiner known to receive such a permit in months. Taken together, licensed refineries will likely export about three million tonnes of fuels out of China this month - mostly jet fuel, according to Reuters' sources.

The profit potential behind these exports will likely drive refiners to resume importing oil, including the sanctioned Iranian oil used by some Chinese "teapot" private refineries. These companies buy the overwhelming majority of Iran's crude oil exports, using ship-to-ship transfers as a subterfuge to hide the crude's true origins.

China's buying of Mideastern oil grades has already ticked up, according to Argus. Chinese refiners recently picked up 26 million barrels for July or August delivery from suppliers in the GCC states, the commodity data firm reports. The sales are driven in part by deep discounts on Saudi grades for prompt loadings, and in part by China's need to refill stockpiles that were drawn down during the Hormuz shutdown.

Combined with renewed tightness if Hormuz hostilities spiral again - a possibility that both the U.S. and Iran have suggested, amidst a back-and-forth exchange of strikes - the return of China to the buy-side of the market would support higher global oil prices, especially after unsold Iranian floating inventory clears.

Increased Chinese diesel exports will also help offset Russia's decision to ban foreign sales of its own domestically-produced fuel, a response to the increasingly effective Ukrainian strikes on Russian refineries. Russian diesel exports were already down by half year-over-year in June, according to energy consultancy Sparta, as the country's abundant fuel surplus began to evaporate under Ukrainian attack.

On Thursday, a crowd of American mariners traveled to Garyville, Louisiana to meet a Chinese asphalt tanker at a refinery pier. That the vessel was Chinese-owned was not itself unusual - about 20 percent of all merchant ships are, and the owner of this one, China COSCO, is the world's largest shipping company. At issue was the vessel's route: since arriving in the United States, the foreign-crewed Jin Zhou Wan ("Jinzhou Bay," IMO 9802580) had called in Boston, Portland, Philadelphia and Baltimore to move U.S. cargoes, and arrived Thursday in Garyville to deliver a load of American-made asphalt. This would be unlawful in ordinary times due to the Jones Act, which reserves coastwise routes for U.S. tonnage and U.S. labor, but a White House waiver has authorized foreign labor in U.S. maritime transportation until mid-August.

Members of the Seafarers International Union (SIU) were on hand to protest the tanker's arrival. "Louisiana's mariners should not have to stand by on the dock while a Chinese state-owned shipping company takes over work that belongs on American vessels," said Chris Westbrook, SIU vice president for the Gulf Coast. "The Jones Act creates family-supporting jobs, strengthens our nation's maritime readiness, and helps ensure America has the merchant marine it needs when our country calls."

The initial 60-day waiver was signed when Iran shuttered the Strait of Hormuz and sent global oil prices soaring. The Trump administration enacted it in hopes that it would help keep down prices for gasoline, diesel and jet fuel; in the case of Jin Zhou Wan, the asphalt cargo is not fuel, but is still permitted by the broad waiver policy.

The Jones Act's supporters are hoping that the president will bring the waiver program to a close early, or at least by August 16, the current expiry date. All members of the House Republican leadership team - House Speaker Mike Johnson (R-LA), House Oversight chairman Rep. James Comer (R-KY), House Majority Leader Rep. Steve Scalise (R-LA), Transportation Committee Chairman Sam Graves (R-MS), and 48 others - have signed a petition asking the White House to sunset the waiver when it expires.

Administration officials have spoken positively about the waiver, and have yet to signal whether it could be renewed. The rationale for enacting it - high cost of energy - has largely passed. But pressure from the Jones Act's long-term opponents is stronger than ever.

Australian Dockers Push Back on Automation and AI on the Waterfront

Internal transfer vehicle (ITV) fleet trucks at DP World's Brisbane terminal (Press handout image courtesy DP World)

Docker jobs throughout the developed world are a natural target for automation, and longshore unions put the fight against automated cranes, RTGs and yard vehicles at the very top of the priority list for collective bargaining. They have legitimate cause for concern: newly-built box terminals like Shanghai Yangshan or Maasvlakte II have more robots and fewer people. Now one union is reframing that longtime threat in a new way, coupling the old fear of industrial automation to the new fear of AI, which could pose a threat to white-collar jobs.

"Foreign-owned ports operator DP World is planning to replace skilled Australian workers with AI and automation — without public consent, without proper rules, and without government oversight. If they get away with it here, your job is next," the Maritime Union of Australia (MUA) argues in a new public ad campaign.

The MUA, one of the world's most vocal dockers' unions, is fighting a long-running battle against plans to roll out automated trucks at DP World's four container facilities in the country. The union says that DP World is engaged in an "AI automation program that could threaten up to a thousand jobs," about 60 percent of the docker workforce.

In a report prepared with MUA, the pro-union tax justice group CICTAR lays out a case that more automation would be worse for Australia. CICTAR says that DP World's Australian revenues have gone up since 2019, driven by rising landside charges per container lift, but the wage share of that revenue has fallen: dockers used to earn about half of all dollars that came through the gate, but they now earn about one third.

The report argues that the same thing would happen with more automation in the terminal. In CICTAR's account, there would be fewer workers, but service charges would remain the same, leaving a larger profit margin for the operator. Depreciation on the cost of the automated equipment could also lower the company's tax bill over a period of years, the report argues.

The changes may not be limited to the yard. The MUA says that DP World Australia is also testing out a new AI software program to "revolutionize employee management," using an algorithm to make dockers' work scheduling decisions - a task normally performed by administrative staff.

The union is calling for a 28-hour workweek with no loss of pay for members who would see their jobs put at risk by automation. It has also launched an advertising campaign calling on all Australians to push their government for controls on how AI is used in the workplace. By law, it cannot go on strike until the expiration of its current contract in 2028 - but a change in the law could give it freedom of action.

"The Australian government must make urgent changes to the Fair Work Act to allow workers a genuine voice to effectively bargain how new technologies are introduced to Australian workplaces and introduce urgent safeguards on the use of AI. The government must also explicitly support workers seeking to share the productivity benefits from AI through bargaining," CICTAR concluded in its report for the MUA.

.jpg){kind=link}

{kind=link}