It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

(Article originally published in May/June 2026 edition.)

For years, ammonia has held a strange place in shipping's transition – promising, commercially uncertain, operationally uncomfortable. It carries no carbon atoms, can be made from renewable hydrogen and nitrogen, and may eventually serve deep-sea trade routes that batteries cannot reach.

But it's also toxic, corrosive, and unforgiving. "Ammonia slip," where unburned ammonia escapes through combustion or exhaust, is a real concern when injection timing and combustion pressure are poorly controlled.

The question is no longer whether ammonia can work. It's what evidence would prove it is becoming real.

CONFLICTING SIGNS

That question is sharper because the regulatory backdrop has weakened.

The IMO approved its draft Net-Zero Framework at MEPC 83 in April 2025, pairing a marine fuel standard with greenhouse gas pricing for large ships. But the extraordinary MEPC session in October 2025 adjourned for a year, pushing the earliest likely entry into force from 2027 to 2028. Long-lived assets still need ordering, but the compliance signal has moved backward.

The demand signal has not.

DNV estimates that by 2030 alternative-fueled ships could consume over 50 million tons of oil-equivalent, low-GHG fuels annually. The IEA is starker: Oil products still account for over 99 percent of international shipping energy, and biofuels supplied less than 0.5 percent in 2022. Under its net-zero pathway, low-emission fuels would need to reach almost 15 percent by 2030.

Price tells another part of the story. Very low sulfur fuel oil (VLSFO) remains the baseline, listed in Singapore at $781 per metric ton on May 29, 2026, against a global average of $893.50. Methanol looks cheaper by the ton, but on a VLSFO-equivalent energy basis, Singapore grey methanol translates to $1,345.50 per ton.

Biofuel premiums stay volatile with a recent Singapore B30 assessment carrying a $243 premium over VLSFO. LNG belongs here too with infrastructure and momentum that ammonia lacks: The dual-fuel LNG ships orderbook rises from 781 today to more than 1,400 by 2030.

By contrast, DNV reports 39 ammonia-capable ships, mainly carriers and bulkers, on order, with early deliveries expected around now. Ammonia enters a crowded contest where regulation, energy density, infrastructure, price, lifecycle emissions, safety confidence and willingness to pay all matter.

BUILDING THE VALUE CHAIN

ITOCHU Corporation sees ammonia moving from concept into first proof. Takeo Akamatsu, General Manager of the Green Innovation Business Unit in ITOCHU's Plant Project, Marine & Aerospace Division, says the conversation has changed materially.

"It's shifting from R&D to demonstration, especially after the NH3 (ammonia) engine is completed," he says. "Once the first ship with an NH3 engine is delivered, it may shift from demonstration to commercialization for early movers, but on a small scale."

ITOCHU does not frame the transition as a single vessel, fuel or port. Akamatsu describes an integrated project across the chain: downstream, ammonia-fueled ships; midstream, bunkering and supply; and upstream, clean ammonia production.

"As a first mover, our position is limited to a bunkering developer, but we will develop for both down and up," he explains. "ITOCHU's role is to support first movers who secure NH3-fueled ships as bunker suppliers in Singapore from the 2027 fourth quarter, once our bunkering ship is ready."

That vessel is central, and Akamatsu distinguishes it from a conventional carrier: "It's a purpose-built ship as an NH3 bunkering ship, not an NH3 carrier." The point is to demonstrate bunkering itself – a first-generation solution that will evolve through trials and new technology. It's where progress becomes less about engineering and more about permission to operate.

"We need society acceptance," Akamatsu says, which includes port workers and nearby communities. "We need to provide reassurance to those parties who are against ammonia bunkering in their society, which cannot be achieved through a one-time demonstration only."

Using it as fuel pulls bunkering crews, receiving vessels, regulators and responders into the safety case.

ITOCHU also sees adoption as demand-led. Dual-fuel vessels can still burn conventional fuel, so supply alone will not create the market. "Alternative fuel should be initiated by the demand side first," Akamatsu says. "Once the NH3 engine is ready, we believe a commercial decision by the end-user is key."

Ammonia doesn't scale because there's fuel. It scales when owners, charterers and cargo owners decide to use it.

FROM OPTIONALITY TO EVIDENCE

Jon Løken, Sales Director at CFARER - A DNV Company, formerly known as DNV Maritime Software, has long been cautious on ammonia. His view has shifted, but not into cheerleading.

The industry, he argues, must separate evidence from optionality. The orderbook still matters, but the better metric may be whether fuel is actually being booked. He points to zero-carbon ammonia booked in China for delivery in 2027. "The moment I heard about that, I felt, okay, now we're talking reality here. It's no longer a theory."

Geopolitics may be accelerating that shift. Disruption around the Red Sea and the Strait of Hormuz has reminded operators and governments that the fuel transition is also a question of supply-chain resilience, and Løken sees China moving hard where energy security, industrial policy and shipping economics overlap.

Still, "ammonia-ready" does not mean ammonia will be used. He compares it to old "HD-ready" televisions, where readiness did not always mean capability. The sharper distinction is "ultra-ready."

"Ultra-ready means that you actually install the dual injection system," he explains. "You install all the parts, the pipes and everything, and also test it so that you can technically go straight into using ammonia."

The conversion burden is not trivial. Activating an ammonia-ready vessel may currently require around 50 days in drydock. "There are ships in the yards who were supposed to be ammonia ready that are being taken out early from the yards because they don't have time to stay and finish the ammonia part of the engine," Løken says.

In a strong charter market, owners choose revenue today. "Converting the ammonia-ready ships is going to be a less likely scenario," he adds. "We're probably going to see more actual ammonia ships being ordered for the future."

EARLY USERS

Early use will be selective. "You're probably looking at something like 10 percent of your annual fuel consumption being ammonia," Løken says, assuming access to near-zero-carbon supply.

Ammonia may first appear on specific routes, compliance windows or cargo ecosystems, not as a full replacement. Stricter emission control areas could become a demand trigger near ports and sensitive coasts with China and parts of Africa worth watching.

The segments may surprise the market. "There are a surprising amount of bulk carriers being prepared for ammonia," Løken says. "Bulk is becoming kind of technological forerunner." That aligns with ITOCHU's view that Capesize bulkers, Aframax tankers and car carriers could make Singapore a natural demonstration port.

Geography matters too. Singapore has scale and policy momentum, but clean ammonia may be easier to implement where renewable energy is near major routes. Løken points to Egypt and the Suez Canal. "You have space, you have sun [solar power], and you have ships going through that canal," he says, calling it "a holy trinity of future fuels in maritime."

He raises a more speculative case: If Indonesia develops reliable clean energy and ammonia production, the Sunda Strait could gain strategic importance for Asia-Europe trade, offering an alternative to routing all traffic through Singapore and the Strait of Malacca.

DECISION TIME

The evidence is no longer only in the orderbook. It's in booked fuel, tested injection systems and the slow work of earning a community's permission to bunker a toxic fuel at the quay. That is where ammonia's future will actually be decided.

The opinions expressed herein are the author's and not necessarily those of The Maritime Executive.

Monday, July 13, 2026

Canada’s microbial fuel factories: How university researchers are turning microorganisms into the next generation of biofuels

As governments and industries search for alternatives to fossil fuels, biofuels remain one of the most promising routes toward decarbonising transportation, aviation and industrial processes. Yet traditional biofuels, produced from crops such as corn, wheat and sugarcane, have long attracted criticism due to land-use requirements, competition with food production, and variable environmental performance. Increasingly, scientists are looking elsewhere, to microorganisms.

Across Canada, university researchers are investigating algae, cyanobacteria, bacteria and engineered yeasts capable of converting carbon dioxide, waste streams and renewable biomass into fuels and fuel precursors. While commercial-scale deployment remains some distance away, the science suggests that microorganisms could become the basis of a new generation of sustainable fuel production systems.

Microorganisms offer several advantages over conventional energy crops. Many species grow rapidly, require little land, can be cultivated using wastewater or industrial emissions, and often produce oils, alcohols or hydrocarbons naturally. Microalgae, in particular, have attracted considerable attention because they are photosynthetic and can convert sunlight and carbon dioxide into energy-rich lipids. Researchers at Canada’s National Research Council have described algae as robust microorganisms capable of growth in photobioreactors, open ponds and wastewater systems without relying on agricultural land. The resulting biomass can then be converted into biodiesel, bio-oil, bioethanol and other renewable fuels.

Rather than extracting carbon from geological deposits formed millions of years ago, microbial systems recycle contemporary carbon already circulating in the atmosphere. Algae remain the leading candidates

Several species stand out including Chlorella vulgaris. This freshwater microalga is among the most extensively studied organisms for biodiesel production. Under nutrient-limited conditions, Chlorella accumulates large quantities of lipids, which can be extracted and converted into biodiesel through transesterification. Researchers view the species as attractive because of its rapid growth and relatively high oil content.

Another microalga receiving attention is Scenedesmus obliquus. University of Toronto research has examined engineered biofilms containing this species, exploring ways to increase biomass productivity while reducing harvesting costs—one of the major economic barriers to algal fuel production.

Although often referred to as blue-green algae, cyanobacteria are actually photosynthetic bacteria. These organisms are particularly interesting because they can be genetically modified to directly produce fuel molecules, including ethanol, hydrogen and hydrocarbon-like compounds. The CPCC maintains numerous cyanobacterial strains specifically for biotechnology research, carbon sequestration studies and environmental applications.

A river with cyanobacteria on the water. Image by Tim Sandle

Beyond naturally occurring algae, Canadian researchers are increasingly applying synthetic biology to microorganisms. At the University of Calgary, biotechnology research includes microbial metabolic engineering aimed at producing renewable energy products through modified biological pathways. Researchers are investigating how microbial systems can be redesigned to manufacture valuable compounds more efficiently, potentially creating industrial-scale microbial production platforms.

Rather than relying solely on lipid accumulation, synthetic biology enables scientists to reprogram microbes to produce specific chemicals that can serve as advanced biofuels. These include isobutanol, ethanol, and sustainable aviation fuel intermediates. Methane-eating bacteria: Another possibility

An intriguing area of Canadian research involves methanotrophs. These are bacteria that consume methane as their primary energy source. The University of Calgary’s microbial ecology research includes investigations into microorganisms involved in methane cycling. Methanotrophs possess enzymes capable of oxidizing methane into useful carbon compounds that can potentially be transformed into fuels, chemicals and biomaterials.

This approach has dual environmental value in terms of reducing methane emissions, a potent greenhouse gas and producing valuable fuel feedstocks from waste methane streams. This means landfills, wastewater treatment facilities and agricultural operations could eventually become sources of renewable carbon for microbial conversion systems.

Many microbial biofuel systems are attractive because they can utilize materials that would otherwise be discarded. Researchers at the University of Toronto have explored biological conversion processes involving wastewater, biosolids and industrial emissions. Coupling waste treatment with microbial cultivation creates the possibility of simultaneously reducing pollution while generating fuel feedstocks.

This “circular bioeconomy” concept is gaining increasing support among policymakers and researchers because it addresses multiple sustainability challenges simultaneously. Instead of viewing wastewater as a disposal problem, it becomes a nutrient source and instead of treating carbon dioxide as waste, it becomes feedstock.

Perhaps the most significant future market for microbial biofuels lies in aviation. While passenger vehicles are increasingly electrified, aircraft remain dependent on energy-dense liquid fuels. Algal oils are chemically similar to some petroleum-based fuel fractions and can be upgraded into sustainable aviation fuel (SAF). Researchers continue to investigate hydrothermal liquefaction and catalytic conversion technologies capable of transforming algal biomass into jet-fuel-compatible products. The challenges remain substantial

Despite the scientific promise, microbial fuels have experienced cycles of hype and disappointment. The primary challenge remains economics, since producing fuel from microorganisms still typically costs more than extracting and refining petroleum. Harvesting microalgae, extracting oils, maintaining cultivation systems and scaling photobioreactors all require substantial investment. Numerous studies have concluded that while technically feasible, large-scale algal fuel production remains commercially challenging. There is also a biological trade-off in that many microorganisms grow rapidly but produce relatively little fuel. Others accumulate large amounts of oil but grow slowly.

Researchers have wrestled with this problem for decades, prompting increasing interest in genetic engineering and synthetic biology approaches designed to optimize both productivity and fuel yield. Yet, if Canadian researchers can improve microbial productivity, lower harvesting costs and integrate fuel production with carbon capture and wastewater treatment, microbial biofuels could become one of the country’s most important bioeconomy sectors over the next two decades. But the economics suggest that success will come from combining fuel production with multiple revenue streams rather than relying on fuel sales alone.

Sunday, July 05, 2026

Asia Bets on Biofuels to Dodge Middle East Oil Shortages

Biofuel demand is reviving in 2026 as the Iran war and Strait of Hormuz closure sparked a wave of volatility that made buying difficult.

Vietnam is switching fully to ethanol-blended gasoline and Indonesia is raising its biodiesel mandate to 50%, while Europe holds back over food price and deforestation concerns.

Think tank Transport & Environment warns biofuel demand could rise up to 70% by 2030 if oil supply stays constrained, risking a food price crisis.

Interest in developing biofuels has fluctuated and has been strongly driven by global energy trends. In 2024, following the COVID-19 pandemic, the international call for a green transition, and the increased focus on developing cleaner fuels to decarbonise hard-to-abate industries, interest in biofuels grew. Biofuels were expected to play a major role in the global green transition by helping to decarbonise industries that could not simply shift to renewable electricity, such as aviation. However, this interest waned in 2025, as several companies backtracked on their green energy targets.

Biofuels are produced by heating biomass feedstocks (plant materials) rapidly at high temperatures (500°C-700°C) in an oxygen-free environment or by using gasification, hydrothermal liquefaction, or low-temperature deconstruction. Ethanol and biodiesel are the two most widely used biofuels, although other feedstocks can be used to produce alternative biofuels. Typical feedstocks include sugar cane, corn, and soybeans, most of which produce low-carbon fuels that can be used in existing engines.

In 2024, the International Energy Agency (IEA) said it expected the use of biofuels to increase significantly by 2030, with a much larger proportion of these fuels produced from waste, residues, and non-food crops, thereby making them more sustainable. The demand for biofuel rose to 4.3 exajoules (EJ) in 2022, thereby surpassing pre-pandemic levels. The IEA suggested that to meet net-zero emissions targets by 2050, global biofuel production would need to increase to 10 EJ by 2030.

By the end of 2024, there were 43 projects expected to be operational by 2030, according to Rystad Energy, with oil and gas firms such as ExxonMobil, Chevron, BP, Shell, TotalEnergies, and Shell all committing to biofuel production. Many of these projects focused on sustainable aviation fuel (SAF) production, as governments worldwide put increasing pressure on the aviation industry to decarbonise. However, by 2025, interest in biofuels had begun to wane.

In late 2025, the OECD said it expected global biofuel use to increase by 0.9 per cent per year over the coming decade, which was much lower than the 3.3 per cent annual growth seen in previous years. The OECD anticipated that biofuel growth would slow in high-income countries due to stagnating fuel demand resulting from electric vehicle adoption and weaker policy support, although continued demand growth in middle-income countries was expected to offset the slowdown.

In 2026, interest in biofuels is reviving, driven by the significant price volatility of fossil fuels. The U.S.-Israeli war on Iran and the resulting closure of the Strait of Hormuz, a key energy trade corridor, have led to energy shortages and driven oil prices sharply higher in recent months, prompting many governments and energy companies to consider investing in alternative fuel production to counter the shortages.

Between February and April, crude prices rose by around 30 per cent. Meanwhile, the price of corn increased by just 5 per cent over that period. Biofuels are typically blended into gasoline or used to replace diesel, making fuel more economical when crude prices are high. Several countries have addressed shortages and high prices by introducing measures such as fuel rationing and shorter workweeks, as well as by increasing their biofuel use.

Countries across Asia, which are heavily reliant on oil imports from the Middle East, have invested in increasing biofuel production since the beginning of the war. In late March, Vietnam announced plans to switch fully to ethanol-blended gasoline, produced using sugarcane, from April due to high crude prices. Meanwhile, Indonesia said it would increase the mandatory blending rate for biodiesel made from palm oil to 50 per cent from 40 per cent. Brazil and Thailand have also increased their biofuel use in recent months.

A biofuels analyst from data and analytics company Kpler, Beata Wojtkowska, explained, “In Asia, countries do look at biofuels that can be produced from locally sourced feedstocks, as they can reach two goals at once - limit energy imports and increase profitability for farmers.” However, while biofuel use has increased in Asia, Europe has been more reluctant to increase its biofuel production, citing concerns that excessive use could raise both food prices and deforestation rates.

The energy and climate director at the think tank Transport & Environment (T&E), Kädi Ristkok, warned that increasing reliance on biofuels could exacerbate geopolitical challenges. “Governments are playing a dangerous game by promoting food for fuel. Leaders are understandably trying to find solutions to the current oil crisis, but biofuels can never play more than a marginal role in our energy system without devastating consequences. The unintended impacts on food prices and the environment are enormous,” explained Ristkok. T&E estimates that the demand for biofuels could increase by up to 70 per cent by 2030 if the global oil supply remains constrained.

Investment in the expansion of the biofuel industry has fluctuated in line with global energy and environmental trends in recent years. However, limits to the world’s crude supply and higher fossil fuel prices have once again driven interest in alternative fuels. While this could help reduce reliance on the constrained oil supply, it could also lead to food shortages if not properly managed.

Italian oil company Eni SpA and commodity merchant Mercuria Energy Group Ltd. signed an agreement to join forces in trading, seeking growth in an area that has seen huge price swings and profit opportunities during the war in Iran.

The two firms will be combining their main trading books for various commodities including oil, liquefied natural gas and biofuels under a new entity headquartered in Geneva, according to statements on Wednesday.

It’s a big move for both companies — integrating Eni’s physical energy supply chains with Mercuria’s trading expertise could potentially allow them to compete more effectively with larger rivals such as Shell Plc or Vitol Group.

“This partnership brings together two highly complementary organizations,” Mercuria chief executive officer Marco Dunand said. The venture will combine “physical energy flows with world-class trading, logistics and risk management capabilities.”

For Eni, the tie-up could allow it to challenge its larger European rivals Shell, BP Plc and TotalEnergies SE, which are among the largest oil and gas traders in the world, buying and selling far more than what’s produced by their own assets.

For Mercuria, which long has trailed rivals like Vitol, Trafigura Group and Gunvor Group in its physical trading volumes, the deal offers an opportunity to supercharge an expansion push, especially in LNG. The fuel is seen by many in the industry as a key growth commodity, but it has faced setbacks, with Steve Hill, a former senior Shell executive whom it hired in 2024, leaving this year.

Eni and Mercuria expect the joint venture to be operational in 2027, with the two firms equally represented at the senior managerial level, according to a spokesperson for the Italian oil giant. Commodity traders won’t be made redundant, the spokesperson added.

Price volatility caused by the Iran war has created opportunities for companies that buy and sell energy in large volumes. Shell and BP posted first-quarter earnings that far exceeded expectations, thanks to a surge in profit from their extensive in-house trading operations.

Mercuria’s first-half profit jumped 88%, putting it on track for one of its best-ever annual results. For several months, the trading house has been doing deals to grow its access to physical commodities and processing assets, including $1.2 billion to help finance the buyout of a copper mining company in Kazakhstan and a deal to buy an oil refinery and petrol stations in Argentina.

Trading activities for both parties will be exclusive to the JV for the identified commodities, except cases that require joint approval, the spokesperson said, adding that Eni does not currently expect refinery assets to form part of the venture.

Talks between Eni and Mercuria to form a joint venture were first reported by Bloomberg in January.

(By Jack Wittels)

Mercuria signs first uranium financing deal with Malawi miner

Kayelekera uranium mine in Malawi. Credit: Lotus Resources.

Trading house Mercuria Energy Group Ltd. signed its first prepayment agreement with a uranium miner, striking a deal with the owner of an operation in Malawi.

Australia’s Lotus Resources Ltd. said last week it has signed a non-binding term sheet with the commodity trader for production from the its Kayelekera mine. If finalized, Mercuria will pay up to $30 million and be able to market 3 million pounds of uranium over 30 months.

The arrangement is Mercuria’s maiden foray into financing uranium miners in return for a portion of their output. The market for the nuclear fuel has recovered in recent years following a lengthy downturn after the 2011 Fukushima disaster, and demand is forecast to grow as multiple countries – led by China – expand their fleet of reactors.

Lotus acquired the Kayelekera asset in 2020, six years after it was shuttered due to weak uranium prices. The company restarted the mine last year and is targeting annual output of 2.4 million pounds of uranium oxide, although earlier this month it announced a temporary pause in production after the Iran war disrupted sulfuric acid supplies.

Mercuria’s funding – which won’t be available until September at the earliest – will provide “significant additional working capital flexibility to progress the project,” Lotus said. That involves repairing the mine’s acid plant.

Under the marketing agreement, Lotus will retain “full control” over who Kayelekera’s production is sold to, including to power utilities that have existing offtake contracts with the mine, the company said.

A spokesperson for Mercuria declined to comment.

(By William Clowes and Archie Hunter)

Monday, June 29, 2026

ANGOLA

The Billion-Dollar Debt Deals Exposing an Oil Giant

Sonangol has raised billions of dollars in loans and bonds as it struggles with weak cash generation from its core oil business.

Much of the company's profitability comes from dividends and external investments rather than upstream and downstream operations.

Asset sales, corporate restructuring, and a planned 2027 IPO are central to Sonangol's strategy to restore financial health.

Last week, Angola's state oil company, Sociedade Nacional de Combustíveis de Angola (Sonangol), secured a $2.65-billion financing deal with a consortium of international banks to fund the company's operating expenses and capital investments. The financing was heavily backed by a syndicate of foreign lenders including Société Générale, First Abu Dhabi Bank, Standard Bank of South Africa and Absa, while local Angolan banks, including Banco Fomento de Angola (BFA), Banco Millennium Atlântico and Banco Angolano de Investimentos (BAI), chipped in with $105 million.

The deal is the latest in a series of financing deals completed by Sonangol since the beginning of the current year, with the company having secured a $1.75 billion facility from the African Export-Import Bank (Afreximbank) in January to support its working capital needs and crude trading operations, shortly before it raised $750 million in international markets through a five-year bond carrying a 10% coupon in the same week. Sonangol is still hunting for more capital, with the company currently seeking an additional $4.8 billion from Chinese and European lenders to cover a funding deficit for the planned $6.6-billion Lobito Refinery.

Unfortunately, a deeper dive into Sonangol's flurry of financing deals uncovers major weaknesses in the Angolan oil model.

While the massive capital raise from international banks appears like a big seal of approval of Sonagnol’s operations, it actually underscores how a lack of core profitability, diversification into unrelated business and declining production are choking the country's energy champion.

First off, Sonangol’s core Oil & Gas operations are barely profitable. The company reported a respectable net profit of 862.4 billion Kwanza ($940 million) for its 2025 financial results; however, Sonangol’s upstream exploration and production(E&P) operations generated a miniscule Kz97.1 billion ($105 million) in actual profit despite generating generated a massive Kz4 trillion ($4.36 billion) thanks to to astronomical costs, asset depreciation and taxes. The company’s downstream refining and distribution segment fared even worse after posting a Kz820.3 billion ($895 million) loss in a single year.

Fully 53% of Sonangol’s profits in 2025 did not come from its core business, but rather from dividends paid by external corporate stakes in Portugal’s Galp Energia (OTCPK:GLPEF), Millennium BCP bank and the Angola LNG project. Sonagol owns a 22.8% stake in the Angola LNG project alongside Chevron Corp. (NYSE:CVX), with a 36.4% stake, while BP Plc (NYSE:BP), TotalEnergies (NYSE:TTE), and Eni S.p.A. (NYSE:E) each own a 13.6% stake apiece. Designed to process up to 1.1 billion cubic feet of natural gas per day and deliver 5.2 million metric tons of liquefied natural gas (LNG) per year, the $12-billion facility is supplied with associated natural gas from various offshore fields--including those operated by Chevron--and processes it into liquefied natural gas for the global market. The project plays a crucial role in eliminating the flaring of associated gas from offshore oil production fields, redirecting it instead into a commercialized clean energy export.

But Sonangol's problems do not end there.

The company’s statutory audit board recently warned that Sonangol’s internal cash reserves can cover only 18% of its immediate financial needs, with the cash crunch highlighted by the Kz8.2 trillion ($8.96 billion) owed to Sonangol by third parties and by the Angolan state itself.

That said, much of Sonangol’s woes can be traced back to the systemic corruption by Angola’s government. For years, the Angolan government used Sonangol as a de facto sovereign wealth fund, forcing the state oil company to accumulate stakes in roughly 65 non-core businesses.

The company was burdened with stakes in everything from aviation (Sonair) to medical clinics (e.g., Girassol clinic). These non-strategic holdings have proven to be a severe financial drain, costing the company billions in losses over a long stretch. Poor cash flows have forced Sonangol’s oil production to steadily decline due to the natural depletion of mature offshore fields and delayed upstream investments, with national crude output falling to just 1.1 million barrels per day (bpd) from its 2 million bpd peak in 2008. Much of the remaining prospective acreage is located in ultra-deepwaters, requiring high capital expenditures.

Thankfully, there’s still hope for Angola’s largest company. To refocus on its energy operations, Sonangol is lining up the sale of more than 70 non-core subsidiary shareholdings spanning real estate, aviation, banking, and telecommunications.

The company is restructuring its massive debt burden to ensure liquidity and is actively pursuing partnerships with international majors (such as Chevron) to develop new deep-water assets.

Further, the Angolan government is giving Sonagol more free rein to compete with its international peers. Until recently, Sonangol acted as both an oil operator and the state's concessionaire; however, the transfer of regulatory and licensing powers to the National Oil, Gas and Biofuels Agency (ANPG) has freed up Sonangol to bid on and manage oil blocks on an equal footing with international operators.

The ultimate goal of the restructuring drive is to float up to 30% of Sonangol on the stock market, with an IPO planned for 2027. Management is targeting a phased public listing, initially on the Luanda Stock Exchange with plans for subsequent listings on major international markets like the U.S and the U.K.

By Alex Kimani for Oilprice.com

Wednesday, June 24, 2026

U.S Northwest Could Potentially Be In For ‘One Of The Strongest El Niños We’ve Had’

(Oregon Capital Chronicle) — Warming temperatures at the equator could paradoxically bring the Northwest a wet fall and high winter snowpack, according to climatologists.

The West could be in for “one of the strongest El Niños we’ve had,” Larry O’Neill, Oregon’s state climatologist, said Monday. The ocean and atmospheric weather pattern that occurs every few years and touches all parts of the West typically brings with it warmer and drier temperatures from August through winter, but during a super El Niño — of which there have been only three since 1980 — it does the opposite, bringing greater rain and mountain snowpack.

“The very strong ones don’t follow the typical rule of thumb,” O’Neill said following an online drought and climate outlook meeting hosted by the National Oceanic and Atmospheric Administration.

That could be great for many drought-stricken parts of Oregon and the region, where heat, record low snowpack, depleted reservoirs and low stream levels have caused Gov. Tina Kotek to declare a drought emergency in nearly half the state’s counties. In April, Washington Gov. Bob Ferguson declared a statewide drought emergency for the fourth year in a row, and that same month Idaho Gov. Brad Little declared a statewide drought emergency for the first time in 25 years.

The National Oceanic and Atmospheric Administration earlier this month said El Niño conditions had formed in the Pacific, with a 63% chance of a “very strong” El Niño peaking by the end of the year.

But, O’Neill also cautioned, recent El Niño events and its counterpart La Niña — typically associated with colder temperatures and snow — have become far more unpredictable under rising global temperatures.

“In the last couple years, the La Niñas haven’t really been acting like they usually did. This past year, for instance, we had a weak La Niña, which is supposed to give us a good snow pack, and yet we ended up with our worst snow pack in our recorded history,” he said. “So where exactly this El Niño goes is pretty uncertain.”

If it’s weaker than expected, drought could continue through the winter and spring, exacerbating already low snowpack and water levels. If it is a “very strong” El Niño, depleted reservoirs and mountain snow banks could be refilled and formed, O’Neill said.

Another byproduct of a strong El Niño worth tracking over what’s predicted to be a tough wildfire year: more lightning. O’Neill and his colleagues have been studying decades of lightning patterns in Oregon during El Niño and La Niña events and found that in eastern Oregon there’s a slightly higher prevalence of lightning during an El Niño period.

Record heat

Taken together, August through November of 2025 was the record warmest on average across the Northwest in more than 130 years of recordkeeping. NASA scientists, using NOAA records of global average temperatures dating back to 1880, found that November was the third-warmest on Earth, behind only 2023 and 2024.

This October to May was the second warmest on record for Oregon and Idaho, and the third warmest for Washington. May temperatures across the region were about 4.5 degrees Fahrenheit above normal, and nearly 5 degrees above normal in Oregon. And in the last 60 days, Washington experienced its third warmest June and July on record, Oregon its fifth and Idaho its 15th warmest start to summer.

There’s a 50% to 70% chance that the region will continue to see above normal temperatures from July to September, scientists at the NOAA meeting said.

Low flow

“So not only did we start with below normal snow pack overall, but that snow pack has melted faster than normal as well,” said Karin Bumbaco, Washington’s deputy state climatologist.

Snow in Idaho, western Montana, the Washington Cascades and Snake River Basin melted two to five weeks earlier than normal, and in parts of the Oregon Cascades, mountain snowpack melted two months earlier than normal, Bumbaco said.

In Oregon, this means water reservoirs in Prineville and the Crooked River Basin and Crescent Lake in the Deschutes River Basin are expected to be low or very low by autumn. Crescent Lake is on track to end the season at its lowest level since the drought of the early ’90s, Bumbaco said.

In southern Oregon, some irrigation districts have curtailed junior water rights. In the Klamath Basin, the Klamath Project Drought Response Agency will pay farmers to stop irrigating and leave fields idle to reduce the risk of water shortages.

Oregon is breaking the most records for low streamflow in the region, and it’s expected to get worse in eastern Oregon and southern Idaho during the next four months, according to Bumbaco.

Low power

That’s a problem for the region’s hydropower system, according to Vince Tidwell and Natalie Voisin of the Pacific Northwest National Laboratory. Between 2003 and 2020, the region lost about 300 million megawatt hours of electricity generation from drought alone, Tidwell said, costing the sector about $28 billion.

And despite peak demand for electricity in the region growing by 4.6% since last summer, energy availability has increased by only 1.5%, Voisin said.

“If there was a perfect storm of extreme events, then there is an elevated risk that there could be an energy shortfall,” she said.

About Oregon Capital Chronicle The Oregon Capital Chronicle, founded in 2021, is a professional, nonprofit news organization. We focus on deep and useful reporting on Oregon state government, politics and policy. Staffed by experienced journalists, the Capital Chronicle helps readers understand how those in government are using — or abusing — their power, what’s happening to taxpayer dollars, and how citizens can stake a bigger role in big decisions. View all posts by Oregon Capital Chronicle →

‘El Niño is a distraction’: Why Europe’s deadly heatwave isn’t down to a natural weather phenomenon

Copyright Copyright 2026 The Associated Press. All rights reserved.

Europeans are sweltering under the latest heatwave, which experts say is being “amplified by long-term warming” – not El Niño.

Western Europe continues to swelter under its third heatwave of the year, as blistering temperatures show no sign of falling until the weekend.

On Monday (22 June) France placed more than half of its 96 mainland departments under red alert, urging citizens to exercise “absolute vigilance” and stay out of the direct sun during the hot spell.

It comes as huge swathes of the country grapple with temperatures exceeding 40℃ as well as a string of tropical nights – where the temperature never falls below 20℃ during a 24-hour period.

Two children, aged four and two, were found dead in their family’s car in south-eastern France on Monday, with officials confirming that intense heat is the “leading line of inquiry”. The tragic deaths follow those of three elderly people who died near Bordeaux over the weekend due to health problems caused by extreme temperatures.

Across the channel, the UK Met Office has issued a red extreme heat warning for today and tomorrow across parts of central and southern England, as well as Wales. Temperatures are expected to rise to 39℃ in the coming days, while overnight temperatures will also be “very high”.

“Humidity is also a factor, making this heatwave even more impactful with heat stress a danger to all,” the Met Office says.

In Germany, rising temperatures have increased the chances of forest fires, particularly in the south and east of the country. Regions including Bonn, Stuttgart and Frankfurt are bracing for temperatures nearing 40℃ over the weekend.

Is El Niño behind Europe’s sizzling heatwave?

Earlier this month, the US National Oceanic and Atmospheric Administration (NOAA) declared that El Niño conditions are officially underway in the tropical Pacific, following months of monitoring.

Many forecasters warn that El Niño conditions could be the strongest event in decades, leading to media coverage of a so-called ‘Super El Niño’. However, this isn’t an official scientific category and isn’t used by NOAA.

El Niño (Spanish for ‘the boy) is a naturally occurring phenomenon that happens when sea temperatures in the Eastern Pacific Ocean become unusually warm. This can push up global temperatures, paving the way for more extreme weather.

Previous El Niño events, such as the one during May 2023 through March 2024, contributed towards record-breaking heat which fuelled a series of deadly heatwaves, wildfires and floods across the globe.

Related

Experts at the IHE Delft Institute for Water Education in the Netherlands have warned that El Niño can have a series of knock-on effects beyond hotter temperatures, including drought, food insecurity and even electricity shortages.

Many media outlets are pinning the current heatwave in Europe on El Niño, but Ioanna Vergini, founder of global weather forecasting platform WYF24, tells Euronews Earth that this is “meteorologically off”.

“The Pacific isn't in a strong El Niño state now, and even when it is, its direct influence on European summer heat is weak and poorly constrained,” she explains.

“This is a classic jet-stream blocking event acting on a record-warm background. The dome is the mechanism; long-term warming is the amplifier; El Niño is a distraction.”

When and where does El Niño’s impact hit?

While El Niño’s impact can be severe, disruption is mainly felt in the tropics. Flooding is a common risk in South America, such as in northern Peru, and can reach parts of East Africa, Central Asia and the southern US.

Droughts and wildfire risks rise during El Niño, particularly across much of Australia, northern parts of South America and in Asian countries like Indonesia.

In Europe and the UK, El Niño’s impacts are much more indirect – but can still increase the likelihood of more unsettled conditions later in the year – such as a milder, wetter and windier weather during autumn and early winter.

“El Niño can also be associated with colder and calmer late winter periods in the UK,” says the British Met Office. “However, any potential impacts will be assessed in more detail later in the year as forecasts evolve.”

Climate experts predict that at the end of this year, and into 2027, the world will likely see very high temperatures – but this isn’t contributing to the intense heat already gripping much of Western Europe.

El Niño ‘comes and goes’ – climate change doesn’t

Most El Niño events have temporarily increased global average temperatures by around 0.2℃.

This is not as significant as human-made climate change, which has pushed the global surface temperature up by approximately 1.3 - 1.5℃ compared to pre-industrial levels.

El Niño’s impacts are therefore compounded by an already warming world. It’s why 2025 was the third warmest year on record – hotter than the El Niño year of 2016 – despite the naturally forming cool drag of a La Niña event.

La Niña (Spanish for the girl) typically cools global temperatures by strengthening trade winds and pulling colder water from the ocean depths to the surface across the equatorial Pacific. La Niña occurs irregularly too, but tends to last longer than El Niño.

"El Niño is a natural phenomenon," climate scientist Friederike Otto from Imperial College London said back in May, before El Niño conditions had officially started. "It comes and goes."

Climate change on the contrary gets worse as long as we do not stop burning fossil fuels. So climate change is the reason to freak out."

Dr Friederike Otto

Professor in Climate Science at Imperial College London and co-founder of the World Weather Attribution

Europe is warming more than twice as fast as the global average, with temperatures up by around 2.5°C compared to pre-industrial levels.

Parts of Europe extend into the Arctic, the fastest-warming region on Earth, where temperatures are rising at three-to-four times the global rate. As snow and ice melt, less sunlight is reflected by the Earth's surface, while the darker surfaces that are exposed absorb more heat, amplifying the melting.

Emissions controls have helped Europe to reduce air pollution, which has brought wide-reaching benefits for human health and the environment. But it has also reduced the low-level clouds produced by aerosols, which acted as a cooling barrier.

Europe's heat map is turning red due to annual heatwaves - IPCC

A set of projections buried in the Sixth Assessment Report shows how southern and eastern Europe shift from scattered amber risk today to near-total dark red exposure by mid-century under the bloc's higher-emissions pathways / bne IntelliNewsFacebook

Villages in northern France have been sweltering this week as temperatures broke through the 40°C in what is already clearly going to be the fourth hottest year in recorded history.

At least 18 people reportedly died in France in the last week, including two children left in a hot car, after temperatures records were smashed.

The annual disaster season of extreme weather is underway and Europe is already suffering from another heatwave that has sent the mercury rising. In its latest climate report, the United Nations’ Intergovernmental Panel on Climate Change (IPCC) warns that heatwaves are going to be a permanent fixture on the calendar from now on and the death toll in Europe is already climbing.

The Climate Crisis is accelerating. The IPCC says that the Paris Agreement goal of keeping temperature increases to less than 1.5°C-2°C above the pre-industrial benchmark has already been missed and temperature increases are on course to reach a catastrophic 2.7C-3.1C by 2050 when large parts of the world will become uninhabitable.

Europe is going to be hit hard, says the IPCC as it is warming faster than the rest of the plant. The most urbanised continent by some distance, some 547mn people — 74% of the European population — live in towns and cities, and the EU's metropolitan regions, home to 39% of the bloc's population, generate nearly half its GDP. The IPCC's Sixth Assessment Report, in its chapter on European cities, shows clearly how fast the process is going.

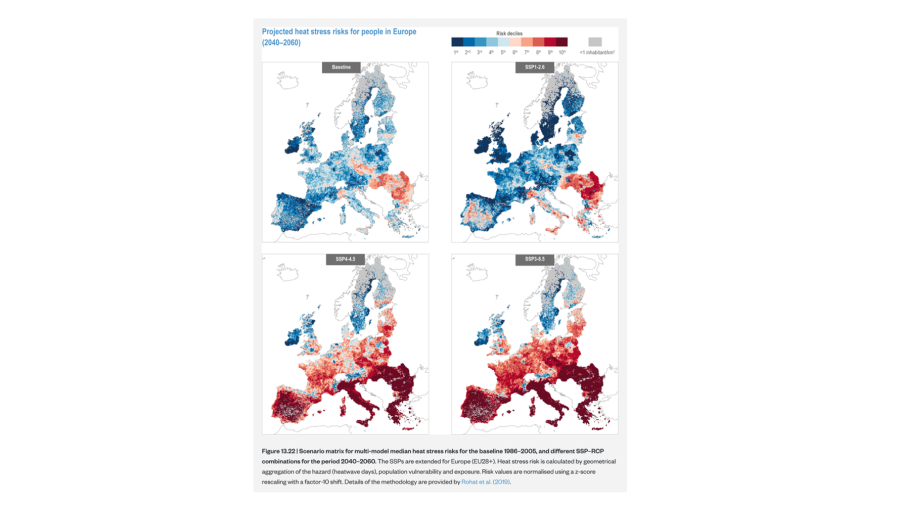

The IPCC plots projected heat stress risk across Europe for the 2040-2060 period under four scenarios, ranked by decile from the lowest-risk dark blue through to the highest-risk dark red in a heat map of the Continent. The baseline panel — reflecting the 1986-2005 reference period — already shows the familiar north-south gradient: Britain, Ireland, France, Germany and Scandinavia sit predominantly in the cooler blue deciles, while a band of amber and light red risk runs through the Balkans, Greece and parts of southeastern Europe.

What changes across the subsequent three panels is the speed and scale of the shift southward and eastward into deep red. Under SSP1-2.6 — the IPCC's low-emissions, high-cooperation pathway model — northern and western Europe largely retains or even improves on its current risk profile, but the Balkans and parts of southeastern Europe darken into the highest decile.

Under SSP4-4.5 — a middle pathway model marked by high inequality — risk darkens across virtually the entire southern half of the continent, with the Iberian Peninsula, southern France, Italy and the Balkans all turning deep red.

By SSP3-8.5 — the high-emissions, low-cooperation model that has historically been used as a worst-case benchmark — the red zone has expanded further still, swallowing almost the entirety of southern and central-eastern Europe in the two highest risk deciles, leaving only Scandinavia, the British Isles and pockets of Western Europe in cooler categories.

The rising heat is going to kill more people each year. At 1.5°C of global warming, the IPCC projects approximately 30,000 annual deaths across Europe attributable to extreme heat — a figure that could nearly triple under 3°C of warming. The 2010 heatwave across eastern Europe, by comparison, killed an estimated 55,000 people in a single event, illustrating the scale of mortality a single extreme summer can already produce at current warming levels.

Southern Europe carries the heaviest burden in every scenario the report models. Heat-related mortality and morbidity are expected to be highest there, and to grow fastest, with the region's vulnerability compounding under the higher-inequality SSP3 and SSP4 pathways relative to the more cooperative SSP1. Heat-related respiratory hospital admissions across Europe are projected to rise from roughly 11,000 annually in the 1981-2010 reference period to 26,000 a year between 2021 and 2050 — a more than doubling driven chiefly by the rising frequency of extremely hot days in the south.

Cities compound the underlying climate signal rather than simply inheriting it. Three-quarters of Europeans live in urban areas, where the urban heat island effect, building density and air pollution interact to intensify the physiological impact of any given heatwave beyond what the raw temperature data alone would suggest.

The report's modelling finds that holding warming to the Paris Agreement's 1.5°C target rather than 2°C would, on its own, reduce summer premature deaths in large European cities by 15 to 22% — a single half-degree of difference translating into tens of thousands of lives across the continent's urban population over time.

The report does flag a genuine source of uncertainty that cuts against the starkest readings of the map: human acclimatisation. Evidence is emerging across most European regions of rising heat tolerance over time, and some projections that assume full physiological and behavioural adaptation suggest mortality rates could remain flat or even fall despite continued warming. The penetration of air conditioners will play an increasingly important role in European demographics as the crisis plays out; ubiquitous in America, air conditioner penetration in Europe is far lower, but that is starting to change as cooling becomes an existential question.

But the uncertainty around humanity's capacity to adapt to genuinely unprecedented heat extremes that fall outside the historical range entirely, remains large. The IPCC explicitly does not treat acclimatisation as a reason to discount the risk captured in the maps.

El Niño, War, and Fertilizer Costs Create a Dangerous Inflation Cocktail

A super El Niño is expected to increase the risk of droughts, floods, crop losses, and higher food prices, adding to inflationary pressures already amplified by elevated energy and fertilizer costs.

India appears most vulnerable, with concerns over a weak monsoon, rising food prices, slower growth, and pressure on the Reserve Bank of India.

Brazil and Mexico could face higher electricity and agricultural costs, while weather-related disruptions may complicate monetary policy and economic planning across emerging markets.

Rory Green, TS Lombard's chief China economist, is the latest Wall Street strategist to warn of the mounting macro and food inflation risks that a super El Niño could release on certain regions of the world.

In a note titled "Super El Niño: Famine Follows War?" Green warns that war-related disruptions to energy and fertilizer markets, compounded by adverse weather conditions, could create a perfect storm for global food prices.

Green said, "In general, El Niño raises temperatures and significantly exacerbates both drought and heavy rainfall. For global macro, it is an inflationary shock via the food price channel – a shock that will likely be compounded by existing war-related high fertilizer costs."

He said within his coverage, "India is the most exposed to both growth and inflation risks, supporting our underweight Indian assets. Brazil and Mexico, too, will receive an inflation impulse."

In recent weeks, the Japanese Meteorological Agency became the first major weather body to formally declare the onset of a super El Niño in the tropical Pacific.

If that forecast is correct, adverse climatic disruption could persist for 2 or more years, raising the risk of drought, flooding, lower crop yields, and higher food prices across key agricultural regions.

Green noted that El Niño has typically been associated with "hotter and drier conditions in India, parts of South and Southeast Asia, and Central America. But at the same time, it brings higher rainfall to parts of southern South America, the United States and Central Asia."

Chart 1: GDP impact of past El Niño

Chart 2: CPI impact of past El Niño

El Niño Impact Watch:

If it proves "strong" or "very strong", the 2026 El Niño is likely to have a historically large impact on global food prices, given already elevated underlying inflation, existing supply-chain disruption and the current high cost of farm inputs. China, Korea and Taiwan are relatively well insulated from the shock. As are most DMs, with the exception of Australia, as the maps below and the charts above show. In our coverage, it is India and LatAm that are most exposed.

India Impact:

El Niño to hit prices, employment and potentially equities

India's Met Department recently warned that El Niño conditions will strengthen during the crucial monsoon season that accounts for ~75% of the annual rainfall the country receives. The Met Department (IMD) has forecast rainfall in the June-September monsoon to be 90% of the long-period average (LPA); if that projection bears out, India will face its worst monsoon since 2015. That year, the IMD had initially predicted below normal rainfall of 93% of the LPA, but the actual rainfall recorded was 86%, leading to drought-like conditions across many parts of India. Even though it is early days yet in this year's season with the rains just about setting in over south peninsular India, indications are that the monsoon is off to a weak start. Rainfall in the first 15 days of June has already been far below normal, as Chart 1 below shows, and the progress of the monsoon across the subcontinent has stalled.

A weak monsoon will exacerbate headwinds to growth that India's heavily energy import- dependent economy has been facing due to the surge in global oil prices. Damage to the summer-sown crop output is a risk to agricultural incomes and rural demand, as well as a potential inflation trigger. Rising food and fuel costs pushed headline CPI higher to 3.9% yoy in May, up from 3.5% yoy in April; May’s food price inflation rose at a faster pace to 4.8% yoy. We expect high commodity prices to spill over into broader inflation, and for headline CPI to breach the upper threshold of the Reserve Bank of India's (RBI) 2-6% flexible target by 3Q/FY27. At its early June policy, the RBI revised up its inflation forecast for FY27 to 5.1% vs 4.6% previously, cautioning against upside risks to its projection. It cited further downside risks to its GDP growth forecast for FY27 that is cut to 6.6% (vs 6.9% previously) owing to supply shocks from both energy and weather-related factors.

The government has been taking proactive measures to combat the El Niño impact, including increasing stocks of rice and wheat in state-run warehouses. How the El Niño impacts the monsoon will be clearer by end-July, when the IMD issues its updated monsoon forecast. July is the key month for crop sowing as the rains typically cover the entire country by the start of the month. Last week, Agriculture Minister Shivraj Singh Chouhan said almost 200 districts (a quarter of India's total) are "most vulnerable" to the impact of El Niño. The monsoon season's impact on crops is determined not just by the quantity of rainfall but also its geographical distribution. The accumulation of water in reservoirs – critical for the winter-sown crop – is also important to track: as of early June, the level was a little lower vs a year ago but higher vs the LPA.

For now, the markets are rebounding after tensions in the Middle East eased, but the Indian economy's resilience will be tested again soon if the monsoon fails: since 1951, 12 of 17 El Niño years have witnessed deficient rains. Foreigners remain net sellers in the equity market, although tax exemptions announced for overseas bond investors are pulling flows into local debt. Equities have been supported by local investors, but returns have been capped as momentum of domestic flows has been flagging recently

Brazil Impact

El Niño could weigh on power, food prices

A 'Super El Niño' could push up inflation, but Brazil is more prepared for extreme weather than in the past. As a country that spans across the South American continent, El Niño has an uneven impact on regional weather patterns. In southern Brazil, overall precipitation, the number of heavy downpours and the severity of storms tends to increase, particularly in the spring. Northern Brazil, including parts of the Amazon basin, tend to have drier weather, as does the country's northeast. While parts of the country's populous southeastern region see a limited impact, key states – including Minas Gerais, tend to be drier than normal. Across the countries, average temperatures tend to rise, and the number of heatwaves tends to increase. These factors, coupled with the greater frequency of extreme weather already effecting the country because of climate change, mean that Brazil runs an even greater risk of severe events this year, similar to the record floods in Rio Grande do Sul state in 2024.

The El Niño adds another layer of uncertainty regarding the economic outlook. Although we do not expect the El Niño to play a decisive role in the direction of the economy in H1/26, it could exacerbate existing issues in the economy, including inflation. Electricity prices, which typically tick up during the dry season (April to October) could rise even more if dry weather has a significant impact on hydroelectric reservoir levels in south-central Brazil, which holds the lion's share of the country's generation capacity. This would force the National Systems Operator (ONS) to continue to maximize the use of high-cost thermoelectric plants to offset the reduction in hydroelectric generation. This would mean that electricity costs would increase in the coming months through the so-called tariff flag systems, which is imposed to cover the costs of thermoelectric generation. Likewise, energy consumption – and spot market prices – tends to increase during heatwaves, as more households use air conditioning. The positive news is that Brazil is entering the dry season, Brazil's hydroelectric reservoirs are in a slightly more comfortable situation than in previous El Niño years, which could limit the impact of the weather phenomenon on power prices.

The El Niño could have an impact on food prices, but not in the short term. When temperatures exceed 40°C for prolonged periods, it generally takes three to four months for the hot, dry conditions to affect fruit and vegetable harvests. The effect on grain and oilseed crops takes even longer. Brazil has already harvested its summer soybean crop and the winter corn crop is in the ground and scheduled for harvest in August and September. At that point, farmers begin planting their summer crops. Even without the El Niño, there are already doubts regarding whether Brazil will manage to expand its soybean and corn crops in the upcoming 2026/27 season. This is because of unfavourable global prices, as well as higher input costs, which could force Brazilian farmers to reduce fertilizer use. While a modest decline in fertilizer application is unlikely to significantly affect yields in a single season, production costs for soybeans and corn will be higher for the 2026/27 season. This increase could influence the cost of meat and biofuels in the following year. In short, pressures from weather and fertilizer prices are present, but their impact on food prices is unlikely to be felt until early next year.

Mexico Impact

The most immediate impact is likely to come through agricultural prices. Adverse weather conditions have historically reduce agricultural output and, with a lag, feed into livestock prices as poorer pasture conditions and water scarcity raise production costs. Agricultural inflation hit 14.33% y/y during the 2023-24 El Niño, nearly three times the headline rate, with fruits and vegetables peaking at 25.69%. The 2026 starting point is no less uncomfortable. Fruits and vegetables spiked to 21.77% in March and, despite easing to 14.38% in May, remain well above headline, leaving the most weather-sensitive part of the CPI basket exposed to a renewed supply shocks. It's worth highlighting that El Niño affects Mexico in distinct ways, with northern states tend to see higher precipitation in winter, which tends to benefit export crops. But the weather phenomenon also boosts the risk of unseasonal frosts and floods that damage, with potential implications for the tomato, wheat, and maize harvests. In the centre-south, El Niño reduces rainfall and coffee, sugarcane, maize, beans, and avocados are the most exposed crops.

Bad timing for Banxico. The central bank cut rates to 6.5% in May and signalled that the easing cycle had likely come to an end, citing weak activity and a resilient peso. We continue to view growth risks as outweighing inflation concerns and believe additional easing in Q3/26 remains possible. However, a moderate-to-strong El Niño would complicate that assessment by pushing up agricultural inflation through supply-side shocks that monetary policy cannot easily offset. This would make any further easing harder to deliver, even as growth concerns continue to mount.

El Niño also exposes structural vulnerabilities to more extreme weather. Along the Pacific coast, warmer sea surface temperatures fuel a more active hurricane season, raising the risk of storm damage to coastal infrastructure and export agriculture. At the same time, the phenomenon puts urban water supply under pressure. Cutzamala, which provides roughly a quarter of Mexico City's water, fell to just 27% capacity during the El Niño. An exceptionally wet 2025 reversed much of that damage, bringing the system back to 67.7% by early June 202 – the highest level in the seasonal cycle in seven years. That buffer offers some protection, but a strong El Niño would still test it.

Green's note builds on a UBS report published earlier this month, which warned that El Niño risks could send food inflation higher across Asia.

The U.S. is not out of the woods just yet. Bank of America analysts warn that the energy shock of the last several months could ultimately feed into food inflation later this year, with a lag (read the report).

Now there has been what Daryna Kovalska, a commodity strategist at BofA, described as an "aggressive positioning washout" in the agriculture trade. However, she believes that the selloff in soft commodities such as corn is well overdone.

.jpeg)