Bank of Canada announces key interest rate hike of one full percentage point

FULL PRESS CONFERENCE

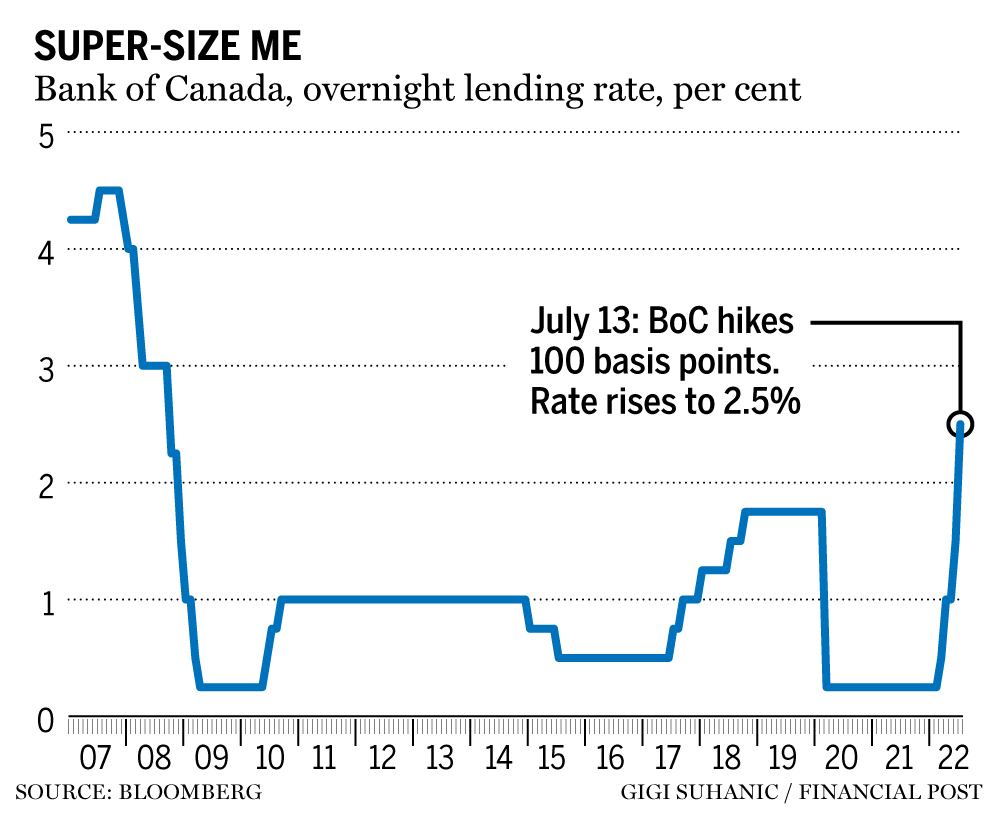

Bank of Canada surprises with

massive 100 basis point hike

Alicja Siekierska

Wed, July 13, 2022

The Bank of Canada raised its benchmark rate by 100 basis points on Wednesday, a surprise move that exceeded economist expectations, as the central bank attempts to set a firehose against scorching inflation.

The unexpected and supersized increase comes after two consecutive 50 basis point hikes, bringing the policy interest rate to 2.5 per cent, the highest level since 2008. It marks the first time the central bank has hiked its benchmark rate by a full percentage point since 1998, and was more aggressive than the 75 basis point increase most economists had widely predicted.

"With the economy clearly in excess demand, inflation high and broadening, and more businesses and consumers expecting high inflation to persist for longer, the Governing Council decided to front-load the path to higher interest rates by raising the policy rate by 100 basis points today," the Bank of Canada said in a statement.

The central bank also continued to warn on Wednesday of more hikes to come, saying that "interest rates will need to rise further, and the pace of increases will be guided by the Bank’s ongoing assessment of the economy and inflation."

But Bank of Canada Governor Tiff Macklem said at a press conference Wednesday that the surprise move – an increase he called "very unusual" – was necessary to combat inflation, which has reached levels not seen in nearly 40 years. Inflation hit 7.7 per cent in May, marking the biggest year-over-year increase since January 1983. Macklem says the bank expects the Consumer Price Index (CPI) to remain at around 8 per cent for "a few months."

"Inflation is too high, and more people are getting more worried that high inflation is here to stay. We cannot let that happen. Restoring price stability—low, stable and predictable inflation—is paramount," Macklem said.

"Our goal is to get inflation back to its two per cent target with a soft landing for the economy. To accomplish that, we are increasing our policy interest rate quickly to prevent high inflation from becoming entrenched. If it does, it will be more painful for the economy—and for Canadians—to get inflation back down."

The Bank of Canada is one of many central banks around the world on an aggressive path to tighten monetary policy in the wake of skyrocketing inflation. Wednesday's decision makes the Canadian central bank's policy rate the highest among G7 countries.

The central bank has estimated that the neutral range, where the interest rate is no longer stimulative, is within two and three per cent. Macklem says the bank is front-loading interest rate increases now to avoid higher rates down the road, which will bring the policy rate "quickly to the top end or slightly above the neutral range."

"The Bank seems determined to get to the finish line as quickly as possible," CIBC Capital Markets economist Karyne Charbonneau wrote in a research note.

"They are likely considering a move of 75 basis points in September, and it will take some downside data surprises to hold them to 50."

Alicja Siekierska is a senior reporter at Yahoo Finance Canada. Follow her on Twitter @alicjawithaj.

What economists are saying about Bank of Canada's steep rate increase

Bianca Bharti Wed,

July 13, 2022

The Bank of Canada delivered a steep hike of the overnight interest rate on July 13 as it wrestles to get decades-high inflation under control.

Governor Tiff Macklem and his deputies raised the policy rate by a full percentage point, bringing the interest rate up from 1.5 per cent to 2.5 per cent. It’s an aggressive move by the central bank, and the largest since 1998, but the governing council likely felt assured in their decision after the United States Federal Reserve Bank made a similarly vigorous hike of 75 basis points last month.

Inflation has hit records not seen in four decades, climbing to 7.7 per cent in May, thanks to higher prices in almost every category Statistics Canada tracks. Many economists predicted price pressures could be peaking, however the central bank’s rate increase landed just after the U.S. released inflation data for June, showing its consumer price index surged 9.1 per cent over the year.

Prices in Canada tend to follow what happens south of the border, and with inflation showing few signs of cooling, more hikes are likely to come.

Read on for expert reaction to what this outsized increase means.

Derek Holt, head of capital markets economics at Bank of Nova Scotia

“What I’d emphasize in this regard is that I just can’t accept their depiction of today’s move as being about how ‘the Governing Council decided to front-load the path to higher interest rates by raising the policy rate by 100 basis points today.’ That implies they think they are getting ahead of inflation risk when in reality they are far behind in the fight against inflation. All they have done today is to tiptoe into the neutral policy setting when what Canada needs to counter inflation is something more deeply into restrictive territory. Front-loading would have been like the (Reserve Bank of New Zealand) and (Bank of Korea) did when they began hiking last summer.

“We’re so past any relevant point at which today’s actions can be described as front-loading the response, when a more accurate depiction portrays the BoC in perpetual catch-up mode to inflationary pressures. As a consequence to having misread inflationary impulses last year, Canadians now face heightened economic anxiety because rates are going up by leaps and bounds when earlier and more gradual rate hikes could have nipped some of the inflation risk in the bud and avoided today’s big changes.”

Royce Mendes, managing director and head of macro strategy at Desjardins

“The Bank of Canada is committing to further rate hikes. Despite the fact that there are some signs that the economy is slowing and certain components of inflation are cooling, central bankers are again tying their hands with forward guidance. There’s not a lot of data between now and the September meeting. So expect further policy tightening is on a pre-set course.”

Stephen Brown, senior economist at Capital Economics

“The statement noted that the decision to hike the policy rate by 100 bp 2.5 per cent — the first 100 bp move since August 1998 — was intended to ‘front-load the path to higher interest rates,’ rather than to reach a higher final destination. While the Bank said that it ‘continues to judge that interest rates will need to rise further,’ it provided no update on where it expects the policy rate to end up, having hinted last month that it intends to raise it to either the top end of its neutral rate estimate — of between two per cent and three per cent — or a bit further.”

Simon Harvey, head of analysis at Monex Canada

“With the Fed expected to conduct two further 75 bp hikes at their next two meetings, it is likely the BoC will follow up today’s decision with a 75 bp hike in September. From thereon in, with rates considered to be above neutral, adjustments are likely to take a more fine-tuning approach.”

James Orlando, senior economist at TD

“This big step up in rates is uncommon, so too is the economic backdrop. With the unemployment rate at 4.9 per cent, wages running at 5.2 per cent, and inflation at 7.7 per cent, the pressure on the BoC has not let up. …The hit to consumers from high inflation and rising rates will weigh on growth over the remainder of this year and into 2023. Though this raises the risk that the economy tips into recession…. the Bank has to accept this risk (and possible outcomes) in order to prevent high inflation expectations from becoming even more entrenched.”

Karl Schamotta, chief market strategist at Cambridge Mercantile Corp

“Fear of an unmooring in inflation expectations was evident throughout the release, with officials noting ‘surveys indicate more consumers and businesses are expecting inflation to be higher for longer, raising the risk that elevated inflation becomes entrenched in price- and wage-setting,’ implying that ‘the economic cost of restoring price stability will be higher.'”

Tu Nguyen, economist at RSM Canada

“As unsettling as this news is for consumers and businesses alike, an economy-wide recession is still unlikely in 2022. Certain industries, such as the housing market which has already slowed, will likely go into decline, but overall, the economic indicators of the job market, businesses, and consumers point to a still rather healthy economy. However, a slowdown is certain and a necessary tradeoff to restore price stability.”

Bank of Canada delivers jolt with 100 basis point interest rate hike to crush inflation

What the Bank of Canada’s full percentage point hike means for the housing market and your mortgage

Bank of Canada raises interest rate: Read the official statement

Josh Nye, senior economist at Royal Bank of Canada

“The BoC revised its GDP growth forecasts significantly lower, trimming 0.75 percentage ppts from its 2022 projection and 1.5 ppts from 2023. It attributed the downward revisions to higher inflation, tighter financial conditions, ongoing supply chain disruptions and weaker foreign demand (global GDP growth seen slowing to 2 per cent next year with the U.S. at 1.1 per cent). …

“The BoC thinks the easing of temporary supply disruptions (assumed to be worth 2.5 per cent of GDP currently) will support growth over the next two years, allowing for decent GDP gains while still absorbing excess demand (currently thought to be around one per cent of GDP). That allows inflation to ease from eight per cent in the near-term to three per cent by the end of next year and two per cent in 2024. But the BoC admitted the path to such a soft landing has narrowed. Indeed, we think the BoC’s forecasts are optimistic, with growth likely needing to slow more materially next year if domestic inflationary pressure is to be brought under control in any reasonable timeframe.

“In our view, a soft landing will be difficult to achieve and our forecast now assumes a mild recession next year.”

Charles St-Arnaud, chief economist at Alberta Central

“The key message in today’s decision is that the central bank is fully committed to controlling inflation. The decision to front-load the increase in policy rate is an effort to nip in the bud any upside pressure on inflation expectations and prevent the high inflation rate from becoming entrenched. It also suggests that when deciding between bringing down inflation or avoiding a recession, the BoC will prioritize inflation. This means that the BoC will likely remain unfazed by the current pullback in the housing market unless it threatens financial stability.”

“It is important to stress that the BoC has little control over global inflationary pressures coming from higher commodity prices or global supply chain disruptions. As such, increasing interest rates will not lower food or gasoline prices or make the computer chip shortage disappear. The only way for the BoC to lower inflation is by slowing the domestic economy, creating excess capacity and reducing domestic inflationary pressures. This is a balancing act that will lead to a period of economic underperformance, notably in the labour market and consumer spending. Whether it will be a soft-landing or a recession remains to be determined.”

Omar Allam, managing director of global trade and investment at Deloitte

“For small- and medium-sized Canadian exporters, this translates into more purchasing power, but it can also hurt accounts receivables. As the Canadian dollar appreciates, it makes Canadian goods and services more expensive in comparison to global competitors who are being more strategic in terms of market diversification. It also has the effect of reducing the value of Canadian-owned corporate profits from global operations. This makes for a more challenging environment for Canadian companies and may ultimately end up negatively affecting their profit margins.”

How the Bank of Canada's rate hike will impact mortgages, loans and spending

Wed, July 13, 2022

TORONTO — The Bank of Canada increased its key interest rate by one percentage point Wednesday in the largest hike the country has seen in 24 years.

The move indicates the central bank will take a more aggressive approach to tackling inflation, which sits at a 39-year high of 7.7 per cent and has made groceries, vacations and other purchases more pricey.

The hike to 2.5 per cent will also impact mortgages, loans and spending habits.

Mortgages

Commercial banks and other financial institutions usually raise or lower their mortgage rates in tandem with the Bank of Canada's interest rate hikes.

The rate hike means consumers should expect most variable rates to hit a range between 3.35 and four per cent, said mortgage agent Sung Lee, in a Ratesdotca release.

Leah Zlatkin, a licensed mortgage broker with Lowestrates.ca, said in a release that every $100,000 someone holds in a variable rate mortgage will result in about $55 more in costs per month.

Based on the Canadian Real Estate Association's average home price of $711,000 in May, a variable rate of 2.7 per cent will result in monthly mortgage payments of roughly $2,845. At 3.7 per cent, which she considers the best mortgage rate, those payments will total $3,168, an increase of $323 per month.

While people with variable mortgages will be affected, anyone whose mortgage rate is up for renewal will likely have "sticker shock" too, said Laurie Campbell, director of client financial wellness at advisement firm Bromwich + Smith.

"It's going to be a situation where a lot of people are going to be rethinking whether they can continue to afford that home," she said.

"We've seen 10 years leading up to this of continued housing increases and the housing market going astronomically insane. Now, it will level off no doubt with these interest increases."

During the COVID-19 pandemic, Campbell saw people tap into their home equity, so some have a traditional mortgage and second mortgage on their property. If there is a correction in the housing market, she fears they could end up owing more on their homes than the property is even worth.

Loans

People with variable rate lines of credit, personal loans or car loans are all impacted by interest rate hikes.

"A lot more of their money is going to be going to interest and they probably want to up their payment, if they can, to cover that and make sure they get out of that debt quickly," Campbell said.

That won't be an easy feat for some Canadians. Campbell said she has seen studies saying Canadians have more debt than ever before and for every dollar someone in the country makes they owe an average $1.86.

"Individuals are really going to have to buckle down and figure out how to manage all of this debt," Campbell said.

If you can't pay off your debt and your financial situation isn't set to improve, she recommends seeking help from a licensed insolvency trustee.

Spending

Between inflation, supply chain snags, shortages and rising rates, most goods and services are becoming more expensive.

However, as pandemic-related restrictions ease, people are eager to venture out of their homes, gather and partake in favourite past times again.

"My guess is in the short term people will continue to spend because it is summer, people love to be outside and enjoy this time of year," Campbell said.

"However, I say that with caution. I think we're going to see increased debt levels and there will be a reckoning where people have to curb their spending because inflation is really killing us and really making it hard for us to make ends meet."

This report by The Canadian Press was first published July 13, 2022.

Tara Deschamps, The Canadian Press

Bank of Canada's jumbo rate hike set to slow lenders' earnings growth

Housing construction in Ontario

Wed, July 13, 2022

By Saeed Azhar and Sinéad Carew

NEW YORK (Reuters) -Bank of Canada's surprise full percentage point interest rate hike on Wednesday could put the brakes on the country's once-frothy housing market and weigh on banks' profits after strong mortgage growth emerged as the main growth engine during the pandemic.

The Canadian housing market was on fire earlier this year, fueled by ultra-low borrowing costs and pandemic-related demand shifts, with prices surging more than 50% over two years.

But sales have dropped dramatically in recent months and May's average selling price was down 12.9% from February's peak.

"Higher mortgage rates are definitely going to be headwinds for real estate and for the banks," said Paul Gardner, portfolio manager and partner at Avenue Investment Management.

Mortgages accounted for about 50% of Canadian banks' loans book, analysts estimate.

But Gardner said unemployment is low in Canada, which means people can still pay their mortgages even though there's going to be less discretionary spending for them.

"You're most vulnerable when unemployment goes through 10% and we're facing the other side, so it's kind of things that there are extreme events that are neutralizing each other," Gardner said.

He said bond markets are already pricing in a recession with an inverted yield curve, which is generally not great for the banks.

The Canadian central bank raised its policy rate to 2.5% from 1.5%, its biggest rate increase in 24 years, and said more hikes would be needed. Economists and money markets had been expecting a 75-basis point increase.

The gap between the 2- and 10-year Canadian bond yields widened by 11 basis points to about 15 basis points in favor of the shorter-dated bond.

Shares of the Royal Bank of Canada fell as much as 2.3% to a session low of C$124.71 ($96.29) on the Toronto Stock Exchange after the rate decision. Toronto-Dominion Bank shares dropped as much as 2.8% to C$78.55 but were last trading down 1.7% at C$79.50, while Bank of Nova Scotia shares dropped as much as 2.1% to C$73.40, but last traded down 1.2%.

The benchmark Canadian stock index fell to its lowest since March 2021 after the rate decision, but recovered to trade flat by late afternoon.

Sohrab Movahedi, banking analyst at BMO Capital markets, said the housing market has held up and part of this is how the product works: banks pre-approve or provide a commitment to consumers on housing loans.

They have an assumption of what would translate into real loans and banks hedge themselves, he said.

"In all likelihood with the rates moving higher, the proportion of those commitments that ends up in a loan will be lower than usual. More people will choose to either buy smaller houses or defer the purchase," Movahedi said.

"If the economy is going to slow down from here, then earnings growth prospects for the banks will also slow."

(Reporting by Saeed Azhar and Sinead Carew; additional reporting by Julie Gordon and Fergal Smith in Ottawa; editing by Jonathan Oatis)

No comments:

Post a Comment