It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

The global copper market enjoyed one of its best years in 2025. The threat of US tariffs on the industrial metal and its elevated status as a critical mineral, together with major supply disruptions globally, all played a part to help to lift prices 40% last year.

That run extended into 2026, as expectations of surging AI-driven demand and persistent supply constraints drove prices to a record of $14,500 a tonne in January. This week, copper is nearing another record.

The prospect of higher mining costs due to rising energy prices and a shortage of sulfuric acid, which is used in a fifth of the global copper production, is considered the next big catalyst for copper prices, a Sprott analyst recently said.

Goldman Sachs is also optimistic of copper surging higher again, due to the supply-side disruptions. The International Copper Study Group recently outright abandoned its previous surplus projections, now forecasting a 150,000-tonne deficit for 2026.

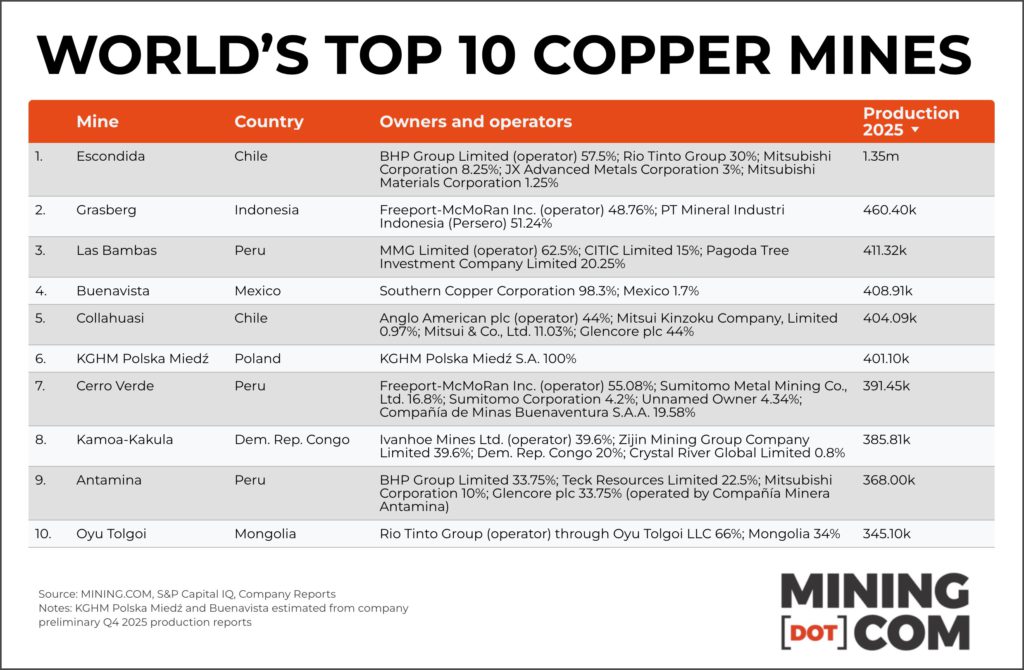

The top 10 mines, many of which have been in production for decades (some even trace roots back to the late 1800s) are responsible for more than a fifth of total global mined production – producing 4.9 million tonnes in 2025.

And surprisingly, after only recently being surpassed by BHP as the world’s number one copper producer on an attributable basis, Chile’s state owned Codelco does not have any of its operations qualify for the top 10.

As last year amply showed disruption at these giant operations (like the Grasberg and Kamoa-Kakula accidents that saw 100s of thousands of tonnes taken off the market,) can have a big impact on copper prices.

1. Escondida

Escondida in Chile, a joint venture between BHP, Rio Tinto, Mitsubishi, and JX Advanced Metals holds the top spot, producing 1,347.6 kts of copper metal in 2025. Escondida has long ranked the world’s biggest copper mine, but BHP’s operational review for the nine months to March 31 pointed to record material mined and concentrator throughput.

Las Bambas mine in Peru, owned jointly by China’s MMG, CITIC and Pagoda Tree Investment Company, churned out 411.3 kts in 2025. The mine was plagued by protests in 2024, but protesters agreed to lift a road blockade on a key Peruvian transport route, and operations resumed in April 2025.

4. Buenavista

Southern Copper’s Buenavista mine in Mexico moves up in this year’s ranking to fourth place with 409.4 kts produced. Copper has been mined at the historic site, 22 miles south of the US border, since 1899.

5. Collahuasi

Chile’s Collahuasi mine, a joint venture between Glencore, Anglo American and Mitsui produced produced 404.1 kts. In April this year, contractors finished building a system that will carry water from the coastal town of Punta Patache to the Ujina deposit, more than 4,400 meters above sea level, as part of a $1 billion infrastructure improvement project.

Cerro Verde in Peru, a joint venture between Freeport-McMohRan, Sumitomo and Buenaventura takes seventh place, producing 391.5 kts. The Peruvian government first mined Cerro Verde’s oxide ores and built one of the world’s first SX/EW facilities in 1972.

8. Kamoa-Kakula

The Kamoa-Kakula complex in the Democratic Republic of Congo, owned jointly by Ivanhoe Mines, Zijin Mining, Crystal River and the DRC government drops from third place last year to seventh — it produced 385.8 kts. Ivanhoe halted operations for three weeks in 2025 after seismic activity severely flooded the underground mine. In April, Ivanhoe slashed near-term production guidance, citing a shift toward underground development, rehabilitation and access work that will constrain ore delivery over the next 18 to 24 months.

9. Antamina

Antamina in Peru, co-owned by BHP, Glencore, Teck and Mitsubishi, moves up to ninth from 10th place, producing 368 kts. Last year, Antamina’s operators forecasted an almost 20% boost in cooper output.

10. Oyu Tolgoi

Oyu Tolgoi, a joint venture between Rio Tinto and the Mongolian government, churned out 345.1 kts. The government, which holds a 34% stake through state-owned Erdenes Mongol LLC., this year demanded earlier profit payments and a larger share of revenue, reopening negotiations over the $18-billion project’s commercial terms.

Honorable mentions: Morenci in Arizona, USA (313,100 tonnes), Quellaveco in Peru (309,900 tonnes), Los Pelambres in Chile (295,400 tonnes)

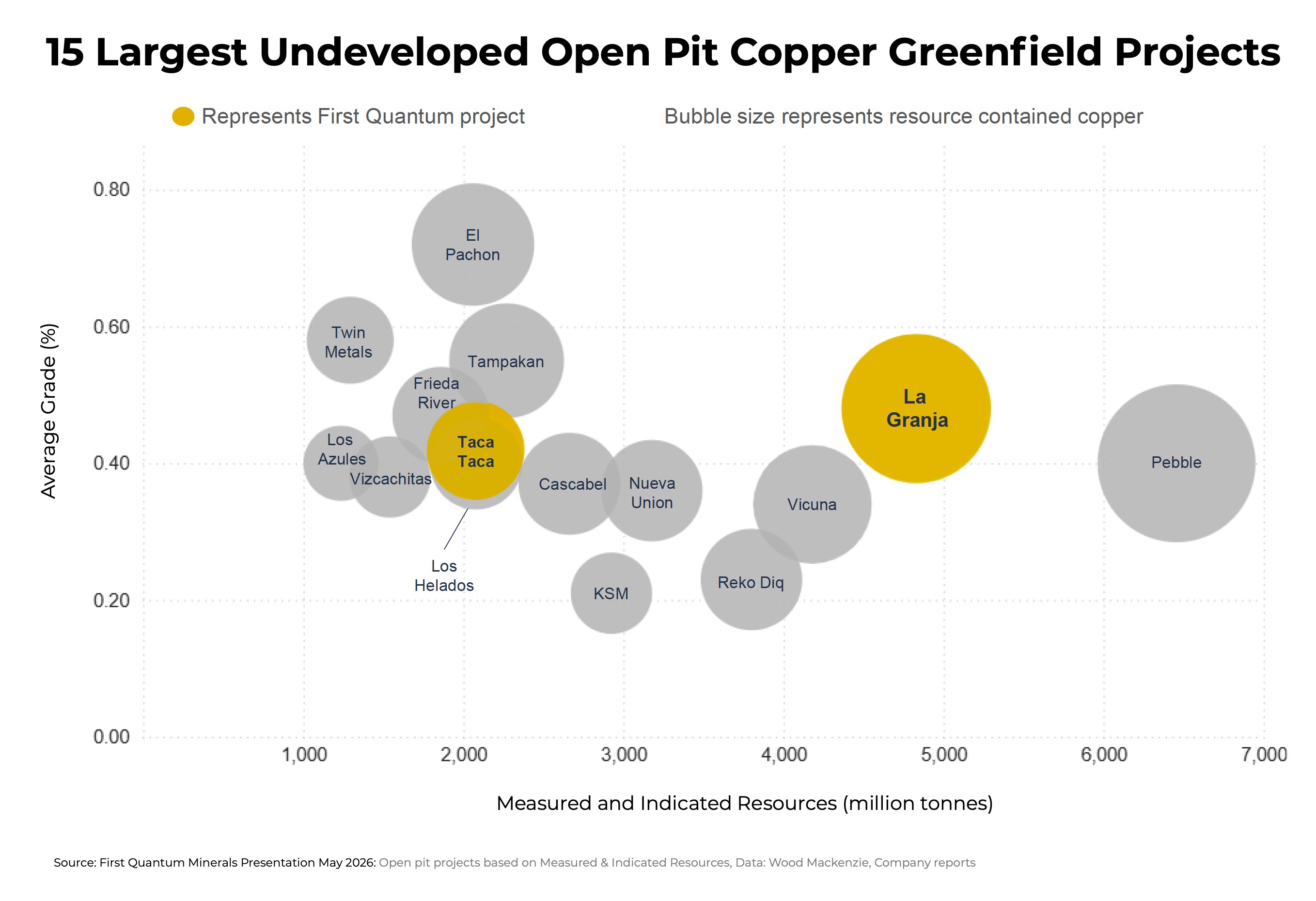

CHART: First Quantum’s Peru project joins ranks of copper giants

First Quantum has completed 370,000 metres of drilling at La Granja. Image: First Quantum Minerals.

First Quantum Minerals (TSX: FM) has filed a new NI 43-101 technical report for its La Granja project in the Cajamarca region of northern Peru it holds with Rio Tinto, outlining one of the copper sector’s largest undeveloped deposits.

First Quantum, said according to La Granja’s (meaning “the farm”) updated mineral resource, the orebody contains 4.8 billion tonnes of measured and indicated resources grading 0.48% copper, equal to 23.0 million tonnes of contained copper.

A further 5.2 billion tonnes grading 0.40% copper sits in the inferred category, containing another 20.7 million tonnes of copper, setting La Granja up as a tier-1, multigenerational asset, in the words of the company.

That places La Granja second among undeveloped copper projects in terms of measured and indicated resources behind only Northern Dynasty’s Pebble in Alaska and when including operating assets, also behind Kamoa-Kakula, the Ivanhoe Mines complex in the Democratic Republic of Congo.

First Quantum acquired the majority stake for only $105 million and has since spent $70 million out of a committed $546 million to advance the project.

Engineering challenges

In an interview conducted last year, First Quantum CEO Tristan Pascall said while the La Granja deal “wasn’t up there in the deals in terms of dollars, in terms of copper in the ground is one of the largest deals done in the last 10, 20 years.”

“Rio Tinto saw in First Quantum a partner that could want a challenging project, because it’s challenging from an engineering perspective, and particularly around deleterious elements like arsenic,” Pascall said. “We had a development hypothesis that we went to Rio with, and really that revolved around dealing with the orebody in a different manner.”

First Quantum says the drillhole database for La Granja now consists of a whopping 832 diamond holes totalling a whopping 370,000 metres, with more planned. The deposit remains open at depth with further exploration targets, according to the company.

Last month, ahead of the latest mineral resource estimate, Pascal told a group of reporters during a tour of its Zambian mines the company has spent the last three years of drilling validating this hypothesis:

“Our view was that it [the arsenic] wasn’t disseminated, that it was discreet and we could package it. That means you have assayable concentrate through a conventional flow sheet, and you don’t need any exotics in order to deal with arsenic.”

La Granja in Peru. Image: First Quantum Minerals

Water and tailings

La Granja’s pit optimization was based on a copper-only cut-off using a $4.00 a pound copper price (versus today’s price of $6.65 per pound, or $14,450 a tonne). Silver, gold and molybdenum should provide by-product upside, which may well lure streaming companies.

Other challenges at La Granja (and most sites in the South American copper belt) include water and tailings management. Unlike many copper projects in the Andean belt, La Granja sits at a moderate elevation between 2,000m and 2,800m above sea level.

First Quantum plans to carry out comminution near the pit, then move material by pipeline through a 7 km access tunnel to a flatter, arid Pacific coastal plain about 100 km from the mine where processing and tailings management would be located.

First Quantum said primary water supply would come from desalinated seawater, with site contact water captured and reused in processing to reduce impacts on local environmental flows.

Next up for La Granja is permitting, and progressing baseline environmental and social studies and continuing community engagement – a process that would take several years under Peru’s strict Environmental and Social Impact Assessment (ESIA) regulations.

A prior Peruvian government estimate put La Granja’s required investment at more than $2.4 billion. First Quantum is also advancing its Haquira project in the Apurímac region of southern Peru.

Annual output over the first 10 years at Taca Taca, which has qualified under Argentina’s fast-tracking program, is pegged at 291,000 tonnes of copper and 133,000 oz. of gold at cash costs of 97¢ per pound. Production over the mine’s life is projected at 209,000 tonnes of copper and 96,000 oz. gold at cash costs of $1.26 per pound.

Appian deepens Namibia push with $400M copper mine buy

Appian Capital Advisory has acquired Omico Copper in a deal giving the mining-focused private equity firm a 95% stake in Namibia’s Omitiomire copper project as it expands its exposure to a metal expected to face surging demand growth.

The mining-focused private equity firm plans to spend more than $400 million to develop Omitiomire into a mine producing about 30,000 tonnes of copper annually over a 15-year mine life, with first production targeted within three years.

The project, about 140 km northeast of Windhoek in Namibia’s Otjozondjupa Region, is considered one of the country’s most advanced undeveloped copper assets. Appian did not disclose the acquisition price for the asset, which was sold by Guernsey-based private equity fund Greenstone Resources LP and Australian mining company International Base Metals Ltd.

“Omico Copper is a technically robust development opportunity that aligns with Appian’s investment philosophy,” CEO Michael Scherb said in a statement. “The project complements our portfolio, offering near-term production alongside long-term growth potential.”

Scherb told Bloomberg News the firm could announce two more copper acquisitions before year-end involving projects at similar stages of development in South America, North Africa and southeastern Europe.

Mining investors are increasingly targeting copper assets amid expectations supply will struggle to meet rising demand from electric vehicles, renewable energy systems, power grids and AI infrastructure. S&P Global forecasts copper demand will climb 50% to more than 42 million tonnes by 2040 from 28 million tonnes last year.

The metal, crucial to electrification, is once again trading near a record high above $14,000 a tonne as a squeeze on Middle Eastern sulfur supplies threatens some operations, compounding disruptions at major mines elsewhere around the world.

Building a copper pipeline

Appian’s latest acquisition also builds on a broader strategy to expand its mining portfolio across Africa and Latin America. In October 2025, the firm established a $1 billion partnership with the International Finance Corp., the World Bank’s private-sector arm, to support mining investments in the regions.

The fund has already backed the development of an underground operation at the Santa Rita nickel mine in Brazil and the expansion of Asante Gold Corp.’s mines in Ghana, Scherb said. Namibia remains one of several “tier-one jurisdictions” where Appian is actively seeking investments alongside Morocco, Ivory Coast, Botswana and Zambia

The firm’s current portfolio includes operations producing about 480,000 ounces of gold annually, along with 55,000 tonnes of zinc and 19,000 tonnes of nickel.

Monday, March 09, 2026

China Splits Port Investments Between High- and Low-Income Countries

The operator of the port of Piraeus is majority-owned by China COSCO (Apaleutos25 / CC BY SA 4.0)

The protracted port dispute in Panama involving the Chinese operator CK Hutchison has revealed how strategic harbors could act as a flashpoint in global power competition. In a world where geopolitical tensions continue to rise, control over critical ports is being seen as a means to assert sea power - particularly when it comes to Chinese control.

Last week, AidData, a research lab at the College of William and Mary, released a new dataset capturing the unprecedented rise of Chinese influence in foreign ports. The report traces Beijing’s global ports footprint spanning over two decades between 2000 and 2025. Over the course of that period, Chinese entities and state-owned enterprises provided loans and grants worth nearly $24 billion for 168 ports across 90 countries.

While AidData has previously investigated Beijing’s financing of ports around the world, the 2026 update provides new data on Chinese-funded shoreside equipment, including cranes and scanners. It also includes proposed port investments which are yet to be funded, including Lobito port in Angola, Sandino port in Nicaragua and Mubarak Al-Kabeer port in Kuwait.

Notably, AidData noted that its research rarely found evidence to support the ‘debt trap’ narrative, popularly used to describe Chinese overseas ports financing.

If anything, this new report strengthens the argument that China does not seek sovereign control of overseas territory as much as it does strategic security,” said Alexander Wooley, AidData’s Director of Partnerships and Communications.

Wooley added that China’s overseas port network provide an anchor for its global maritime supply chains. The network provides a geopolitical benefit: a parallel logistics system that offers Beijing strategic independence, free from interference from rivals, and permits it to contemplate a military counter to potential blockades that could be attempted by an enemy in any future conflict.

Indeed, the report found that Chinese state-owned creditors are increasingly co-locating port financing with other investments vital for China’s national security, such as critical minerals mining. The report identified 22 Chinese-financed mines within a 500-kilometer radius of Chinese-funded seaports. Leading examples include the Port of Chancay in Peru and its proximity to the Las Bambas copper mine, as well as the Port of Morébaya in Guinea, developed by Chinese investors together with the Simandou Iron mining project.

Most importantly, the report clarifies a common misconception that Chinese port investments are focused on developing economies.

"Chinese financing for global seaports is almost evenly split between high-income and low- and middle-income countries,” said Rory Fedorochko, the report’s co-author and Program Manager at AidData. “Some $10.8 billion supports 29 port locations across 20 high-income countries including Greece, Spain, Australia, New Zealand and Singapore- for projects where the intent is generally commercial, rather than geopolitical.”

Some of the ports heavily financed by China include Hambantota in Sri Lanka ($1.97 billion), Port of Newcastle in Australia ($1.32 billion), the Autonomous Port of Kribi in Cameroon ($1.17 billion), the Port of Melbourne in Australia ($1.14 billion) and Haifa Port in Israel ($1.13 billion).

CK Hutchison and its Panama-based subsidiary, the Panama Ports Company, have taken a series of additional legal steps in the ongoing dispute over the concession to operate terminals in the ports of Balboa and Cristobal. As part of the action, the Panama Ports Company (PPC) clarified that under the already filed international arbitration, it is seeking at least $2 billion in damages, a figure it says Panama has been misrepresenting.

Before the Supreme Court decision was published finalizing the ruling that the contracts were unconstitutional, Hutchison had already said it would begin an arbitration under the rules of the International Chamber of Commerce. The ruling was finalized, and Panama seized the two ports on February 23 and immediately entered into temporary contracts with divisions of Maersk and MSC to operate the ports.

Both PPC and its parent company, CK Hutchison, report they have increased the legal actions, saying they will “not relent and they are not coming for some token relief.” They are calling the actions of Panama “radical breaches” while continuing to assert the actions were inconsistent with applicable law, contract, and treaty rights.

CK Hutchison, in today’s statement (March 6), continues to say Panama has a pattern of disregarding communications and discontinuing consultations. They assert it was part of a “state campaign” that had been carried out over the past year. It also accuses the state of “various inaccurate remarks,” which it says have “further aggravated the circumstances.”

The company has filed an administrative petition seeking reconsideration of the decree that empowered what Hutchison calls the “occupation” of the ports and the taking of its property and personnel.

PPC says it is seeking recourse related to the decree based on its extreme scope mandating the taking of all its property. It is also challenging the “radical implementation” of the decree, and the seizure and misuse of property, it says, is unrelated to port operations.

They are asserting that Panama entered a private storage facility and unlawfully seized documents. They are demanding immediate access to and return of property and legally protected documents and information. Investigators for Panama had confirmed they searched the company’s offices, saying it was related to new information about possible crimes.

Panama said when it took over the operations of the port terminals that it was also taking control of all the equipment and information. It, however, was careful not to claim ownership but instead said it was controlling the equipment needed to continue the operation of the terminals.

The Panama Maritime Authority reported that as of February 28, terminal operations were back to 100 percent in Balboa under the management of APM Terminals. It said that operations had been open at Cristobal under the management of Terminal Investment Limited (TiL), a division of MSC, since February 27. The authority has said the country’s intent is to hold new tenders within 18 months and that companies would be limited to operating the terminals in one port to further increase competition.

Tuesday, February 03, 2026

FEATURE

The world is facing a global copper shortage

LONG READ

Thanks to the growing combined demand from AI, EVs and the green energy revolution, global demand is going to outstrip supply and copper prices are already soaring in anticipation. / bne IntelliNews

The world is on track to run short of copper that could pose a “systemic risk” to global economic growth, driven by the energy transition and the booming artificial intelligence sector’s demand for the red metal, S&P Global said in a report on January 8

The looming deficit is forecast to reach 10mn tonnes — equivalent to almost one-third of current global demand — by 2040, in the absence of a “meaningful expansion of supply”, according to S&P Global .

“The shortage would be 23.8% shy of the projected demand of 42mn tonnes by 2040, even as recycled copper scrap more than doubles to 10mn tonnes,” according to the "Copper in the Age of AI: The Challenges of Electrification" study.

“The supply gap threatens to constrain technological advancement and economic growth as copper becomes increasingly essential for AI data centres, electric vehicles, renewable energy infrastructure and defence systems,’ the report said.

Production shortfall

Without significant changes to supply, global copper production is projected to peak at 33mn tonnes in 2030 before declining, while demand is expected to surge 50% from current levels.

“The widening disconnect highlights copper's dual role as both enabler and potential bottleneck for the energy transition and digital transformation,” S&P Global said.

Four key demand vectors are driving copper consumption higher. Core economic demand from construction, appliances and traditional industries is expected to reach 23mn tonnes by 2040, representing 53% of global demand. Energy transition demand from electric vehicles, battery storage and renewable power is projected to increase by more than 7.1mn tonnes to 15.6mn tonnes over the same period.

In addition, AI and data centre demand is expected to triple by 2040 as total installed capacity reaches 550 GW, more than five times 2022 levels, according to the study. The world’s biggest mining group BHP estimated in January that the amount of copper used in data centres worldwide will grow “sixfold by 2050”.

Another largely hidden demand factor is defence spending that could double to $6 trillion by 2040 amid rising international tensions.

Together just data centres and defence represent a combined 4mn tonnes of additional copper demand.

Demand for copper is being boosted by the construction of grid infrastructure for the green transition as well as data centres for artificial intelligence. These need between 27 and 33 tonnes of copper per megawatt of power, according to miner Grupo México, over twice the requirement of conventional data centres.

The study also identifies humanoid robots as a potential fifth demand vector; 1bn units in operation by 2040 would require about 1.6mn tonnes of copper annually, equivalent to 6% of current demand.

The study estimates that an additional 10mn tonnes of primary supply will be required by 2040 beyond increased recycling. However, without significant investment, global primary production could reach just 22mn tonnes by 2040, 1mn tonnes below current levels.

Supply side constraints

On the supply side, declining ore grades, rising energy and labour costs, complex extraction conditions and lengthy permitting processes combine to limit new mine development, the report said.

Supply chain concentration adds another layer of risk. Only six countries are responsible for roughly two-thirds of mining production, according to the study. The International Energy Agency said this year that by 2035, production from existing and planned mines was on track to meet only 70% of global demand.

Existing mines, some dating back more than a century, are getting older and less productive, while large untapped deposits are becoming harder to find. 20 mines produce about a third of the copper mined globally. Of the 239 copper deposits discovered between 1990 and 2023, only 14 were discovered in the past decade, according to the IEA.

China accounts for approximately 40% of global smelting capacity and 66% of copper concentrate imports, making the global supply vulnerable to policy shocks and trade barriers, the report said.

Analysts are expecting shortfalls as soon as this year, with consultancy Wood Mackenzie forecasting a 304,000-tonne shortfall of refined copper in 2025, a gap it says will widen in 2026. Prices have already risen to record levels in anticipation.

Prices rising

Copper is the “new gold” and has already made record gains as fears of a global shortfall mount, rising by the highest amount in over a decade

Copper soared to a record high of more than $13,000 per tonne on January 2 compared with around $8,500 two years ago, as concerns over supply disruption and tariffs extended a rally that has pushed up the price of the metal by almost a third since October, after disruptions at several large mines.

Analysts at BMI, part of Fitch Group, said they expected the price of copper to average $11,000 per tonne this year, while prices would reach $17,000 per tonne in 2034.

US President Donald Trump added to the uncertainty in December, adding copper to a list of critical minerals vital for the US economy. Fears that the Trump’s administration may impose additional import tariffs on the metal have also driven up demand The amount of copper in US Comex warehouses has jumped to a record high of more than 450,000 tonnes, compared with less than 100,000 tonnes a year ago and about 400,000 at the start of December, the Financial Times reports.

Chile is the world’s largest copper producer and holds the largest proven reserves globally. State-owned miner Codelco dominates domestic output, followed by major multinational operations, including BHP’s Escondida mine — the largest copper mine in the world. Despite resource abundance, the sector has faced recent challenges, including declining ore grades, water scarcity in arid regions, labour unrest, and regulatory uncertainty linked to environmental reforms and proposed tax changes. Nonetheless, Chile remains the cornerstone of global copper supply.

Peru

· Annual copper production (2022): 2.4mn tonnes

· Proven copper reserves: 92mn tonnes

· Major companies: Southern Copper Corporation, MMG, Glencore, Freeport-McMoRan, Anglo American

Peru is the second-largest global producer of copper and has rapidly expanded its mining capacity over the past decade. The Las Bambas, Antamina, and Cerro Verde mines are among the country’s most significant operations. Copper accounts for a substantial share of Peru’s export revenue. While the government has maintained a generally investment-friendly stance, mining projects often face delays due to community opposition and social conflicts, particularly in rural Andean regions. Infrastructure and political instability continue to impact investment flows.

Democratic Republic of Congo (DRC)

· Annual copper production (2022): 2.2mn tonnes

· Proven copper reserves: 25mn tonnes

· Major companies: China Molybdenum (CMOC), Glencore, Ivanhoe Mines, Gécamines (state-owned)

The DRC has emerged as a top-three copper producer, driven by heavy Chinese investment and joint ventures with state-owned Gécamines. The Tenke Fungurume and Kamoa-Kakula complexes are among the most productive and rapidly expanding copper sites globally. While rich in high-grade deposits, the sector is hindered by governance risks, poor infrastructure, and fluctuating mining policies. Nevertheless, output continues to rise, positioning the DRC as a key supplier for future green energy demand.

China

· Annual copper production (2022): 1.8mn tonnes

· Proven copper reserves: 26mn tonnes

· Major companies: Jiangxi Copper, Tongling Nonferrous Metals, Zijin Mining, China Nonferrous Mining Corp

China is the world’s largest consumer of copper accounting for around 58% of 2025 demand and among the top five producers, although it relies heavily on imports to meet domestic demand. Copper production is concentrated in several provinces, including Jiangxi and Yunnan. State-owned firms dominate the sector, and the government continues to invest heavily in both domestic mining and overseas copper assets. Environmental regulations have tightened in recent years, leading to modernisation and consolidation in the domestic industry.

China itself only produces around 9% of the world’s mined copper, but that figure rises to around 20% after taking into account overseas projects it has ownership stakes in, according to Benchmark Mineral Intelligence. China now controls around half of copper smelting capacity worldwide. The US, by contrast, has just two operational copper smelters.

In China, the domestic build-out of smelters has been so dramatic in recent years that there is not enough copper ore to feed all the facilities globally. Miners used to pay smelters to process their ore; now it is the other way around. The prospect of new copper smelters opening outside China in the short term — something western policymakers want, in order to reduce their reliance on Beijing — is unlikely. They are expensive to build, energy-intensive to operate and run on thin profit margins.

United States

· Annual copper production (2022): 1.2mn tonnes

· Proven copper reserves: 48mn tonnes

· Major companies: Freeport-McMoRan, Rio Tinto, Grupo México (via Asarco), Capstone Copper

The US copper sector is led by Freeport-McMoRan, which operates the Morenci and Bagdad mines in Arizona. Domestic production has been relatively stable but is challenged by permitting delays, environmental opposition, and aging infrastructure. Projects such as Rio Tinto’s Resolution Copper remain stalled due to legal and community opposition. Nevertheless, the US retains significant untapped reserves and has seen renewed policy interest in critical minerals, including copper, amid supply chain and energy transition concerns.

Australia

· Annual copper production (2022): 900,000 tonnes

· Proven copper reserves: 87mn tonnes

· Major companies: BHP, Glencore, OZ Minerals (acquired by BHP), Sandfire Resources

Australia is a leading copper reserve holder, with large-scale operations such as BHP’s Olympic Dam and Glencore’s Mount Isa complex. The country benefits from a stable regulatory environment, advanced infrastructure, and strong ESG standards. In 2023, BHP completed its acquisition of OZ Minerals, consolidating control over several copper and nickel assets critical to the energy transition. While not among the top three in annual output, Australia is well-positioned for long-term supply growth.

Russia

· Annual copper production (2022): 900,000 tonnes

· Proven copper reserves: 62mn tonnes

· Major companies: Norilsk Nickel, Ural Mining and Metallurgical Company (UMMC), Russian Copper Company

Russia holds large copper reserves and maintains significant domestic production, largely consumed by its own industrial base or exported to Asia. The sector is dominated by vertically integrated giants like Norilsk Nickel, which also produces palladium and nickel. Since the onset of Western sanctions in 2022, Russia has faced reduced access to equipment and capital markets, which may hinder future development and investment in the copper sector.

After more than a decade in the making, strip-mining operations began in the depths of Siberia at Udokan, one of the largest copper deposits in the world, in August 2020. As bne IntelliNewsreported, the mine belongs to Alisher Usmanov, one of the richest men in Russia and contains an estimate 26.7mn tonnes of copper ore that was discovered in Soviet times, but proved technically difficult to develop thanks to its remote location in the region near Lake Baikal. Usmanov have invested some $3bn into developing the mine,

Mongolia

· Annual copper production (2022): 350,000 tonnes

· Proven copper reserves: 30mn tonnes (estimated)

· Major companies: Rio Tinto (via Turquoise Hill Resources), Erdenes Oyu Tolgoi (state-owned), Mongolyn Alt (MAK)

Mongolia is a rising copper producer with significant long-term potential, driven primarily by the massive Oyu Tolgoi mine — one of the largest known copper and gold deposits in the world. Located in the South Gobi Desert, Oyu Tolgoi is operated by Rio Tinto and co-owned with the Mongolian government through Erdenes Oyu Tolgoi. Underground development of the mine began commercial production in 2023, substantially boosting national output. Mongolia’s copper sector is strategically important due to its proximity to China, which receives the bulk of its exports. However, the country faces logistical challenges, regulatory uncertainties, and the need to balance foreign investment with national resource sovereignty. Additional deposits such as Tsagaan Suvarga and projects under MAK may further expand production in the coming decade.

Kazakhstan

· Annual copper production (2022): ~600,000 tonnes

· Proven copper reserves: ~20mn tonnes

· Major companies: Kaz Minerals, KAZ Minerals Group (formerly part of ENRC), Glencore (via Kazzinc), East Copper Company (ERG)

Kazakhstan is a significant copper producer in Central Asia, with a well-established mining sector and extensive undeveloped mineral potential. The industry is led by Kaz Minerals, which operates several large-scale open-pit mines, including Bozshakol, Aktogay, and Artemyevsky. These assets have undergone major expansion since 2015, boosting national output and positioning the company as a key supplier to China. Glencore, through its subsidiary Kazzinc, is also active in the sector, operating polymetallic mines with copper by-products.

The country’s copper sector is supported by substantial reserves and improving infrastructure, including rail and energy links to China and Europe. State-backed industrial policy has prioritised mining investment, though challenges persist around environmental regulation, water availability, and fluctuating export demand. The sector is also home to East Copper Company, part of the Eurasian Resources Group (ERG), which operates copper concentrate facilities as part of its diversified mining portfolio. Kazakhstan is considered strategically important for the global copper supply chain due to its location, resource base, and growing trade ties with China and the Eurasian Economic Union.

First Quantum has completed 370,000 metres of drilling at La Granja. Image: First Quantum Minerals.

First Quantum has completed 370,000 metres of drilling at La Granja. Image: First Quantum Minerals.

{kind=link}