Notes on the Latest US Jobs Report

Photo by Hennie Stander

Last year the major anomaly in the labor market seemed to be that we were seeing very weak job growth and only a limited rise in the unemployment rate. The most plausible explanation was that the Trump administration’s immigration policies had sharply curtailed the pace of labor force growth, with the number of jobs needed to keep the unemployment rate stable now in the range of 20K to 60K.

In the last three months we seem to be seeing the opposite story. The economy added 172,000 jobs in May, after adding 214,000 jobs in March and 179,000 in April, for an average of 188,000 jobs a month — yet the unemployment rate has remained unchanged at 4.3 percent. The household survey actually shows a modest loss in employment of 141,000 over these three months.

The establishment survey is much larger and less erratic, so it is likely giving us a better picture of the state of the labor market. Nonetheless, the disparity in the surveys is striking.

Health Care, Local Government, and Leisure and Hospitality are Big Job Gainers

The health care and social services sector continued to be a big job gainer, adding 47,200 jobs. Local governments had a surge of 55,000 new jobs, the largest gain since March of 2024. Most of these jobs — 43,500 — were not in education, which lessens concern over seasonal adjustment issues. The leisure and hospitality sector added 70,000 jobs, with 48,000 of these coming in restaurants. These three sectors together accounted for all the job growth in May.

Job Growth in the Goods Sector Remains Weak

There was some limited growth in all three components of the goods sector. The logging and mining sector added 4,000 jobs, 3,100 of which were the support activities for mining, which is primarily the oil and gas industry. Employment in the sector is still down by 5K from the year-ago level. The surge in oil and gas prices is an inducement to increased drilling, but the gains will be limited if the industry does not believe prices will remain high.

Construction added 17,000 jobs, somewhat better than its average of just 6,000 per month over the last year. Manufacturing added 7,000 jobs, its fourth gain in the last five months, after losing jobs all through 2025. Employment in the sector is still 46K below the year ago level.

Air Travel and Insurance Shed Jobs

The airline industry lost 8,700 jobs in May, 1.5 percent of total employment. This is fallout from the war-related jump in fuel prices. The insurance industry was also a job loser, shedding 10,700 jobs, after losing 7,800 jobs in April. Employment is down 72,900 (2.4 percent) from its year-ago level. This could plausibly be the impact of AI.

The professional and business services category added just 6,000 jobs, despite the big jump in job openings in the sector reported in the April JOLTS. Retail lost 1,100 jobs after adding 23,500 in April. Employment is up just 17,900 over the last year.

The motion picture industry lost another 2,700 jobs. Employment is down 127,900 (28.0 percent) from its peak in November of 2022.

Wage Growth Slows to 3.4 Percent

Despite the uptick in employment, the growth in the hourly wage slowed further to just 3.4 percent. This is down from a rate of just over 4.0 percent in 2023-2024. With inflation now running at close to a 4.0 percent rate, wages are no longer keeping pace with inflation.

Wages for lower paid workers seem to be doing slightly better. Wages for non-supervisory workers rose 3.6 percent over the last year and in the low-paid restaurant sector they rose 4.4 percent.

Household Survey Shows a Mixed Story

In addition to the stable unemployment rate, the employment-to-population ratio (EPOP) edged up to just 59.2 percent, still 0.1 percentage point (p.p.) below its February level and 0.5 p.p. below its year-ago level. With baby boomers retiring in large numbers, some fall in the EPOP might be expected, but 0.5 percent is larger than can be explained this way.

There is a better story for prime-aged workers (ages 25 to 54). Their EPOP edged up 80.8 percent, 0.3 p.p. above the year-ago level and just 0.1 p.p. below the peak for the recovery hit in several months in 2023 and 2024.

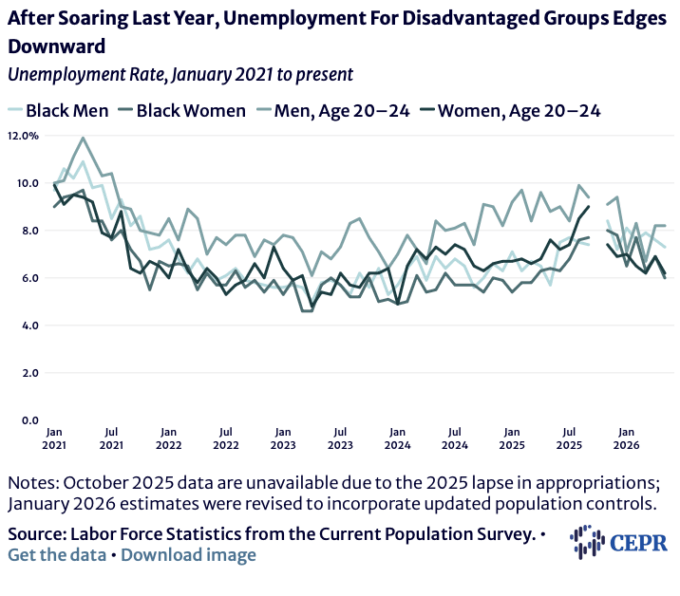

Unemployment Rate for Black Workers Falls to 6.6 Percent

The unemployment rate for Black workers had increased sharply in 2025, peaking at 8.2 percent in November. It has fallen back substantially in the last half year, with the 6.6 percent rate just 0.4 p.p. above the January 2025 level. Still, this is a 1.8 p.p. rise from the low hit in April of 2023. The EPOP for Black workers, at 57.9 percent, is down 0.8 p.p. from the January level and 2.8 p.p. from the peak in March of 2023.

Duration Measures of Unemployment All Rise

Perhaps the most negative item in the household survey was the rise in the duration of unemployment spells. The average duration rose by 1.6 weeks to 26.0 weeks, up from 21.9 weeks a year ago. The median duration rose by 0.6 weeks to 11.6 weeks, compared to 9.5 weeks a year ago. The share of long-term unemployed (more than 26 weeks) rose to 27.5 percent, up from 20.4 percent a year ago. Clearly people who lose a job are finding it harder to get a new one.

Going the other way, the share of unemployment due to quits rose to 12.5 percent, up from 11.3 percent in April. But given the 4.3 percent unemployment rate we would expect the share due to quits to be over 14.0 percent.

Mostly Positive Report with Some Serious Anomalies

It’s hard to complain about a jobs report showing a gain of 172K jobs following two previous months of strong gains. Still there are some serious items that provide serious grounds for concern. The most important is the gap with the household survey. This does happen, so it is not especially alarming, but still it is striking to see three months of job growth that is surely far above the breakeven rate and no decline in the unemployment rate.

The other major anomaly is the weakness of wage growth. We should be seeing a tightening of the labor market, and the higher inflation should mean that workers expect larger wage increases. But wage growth is slowing. It’s not clear what this is saying about the labor market, but it clearly means many workers are falling behind.

The concentration of job growth in three sectors is also a bit concerning. Health care is likely to continue to show strong growth given the aging of the population, but that is not likely to be the case with local governments. And the growth in restaurant employment seems inconsistent with the recent retail data.

Nonetheless, the overall picture still looks positive, but that could change if the war continues and oil prices stay high.

This first appeared on Dean Baker’s Beat the Press blog.

.png)