After a decade of flooding the market with cheap fossil fuels, investors have cut back on production.

(Illustration by Peter and Maria Hoey)

BY LEE HARRIS

FEBRUARY 10, 2022

This article appears in The American Prospect magazine’s February 2022 special issue, “How We Broke the Supply Chain.” Subscribe here.

Following two decades of steeply rising corporate returns, Wall Street profits soared to extraordinary highs last year, despite inflation and the increased costs of securing and transporting goods. The stock market is thundering along, with S&P 500 earnings rising 45 percent in 2021, according to FactSet.

As the economy has staggered back from the pandemic, investors have ridden rising prices to higher returns. (Higher public investment during the past two years also explains some of the extraordinary profits.) “What we really want to find are companies with pricing power,” Giorgio Caputo, one portfolio manager, told Bloomberg. “In an inflationary environment, that’s the gift that keeps on giving.”

Stock buybacks helped retailers remit profits to shareholders. Best Buy CFO Matt Bilunas told investors on a November earnings call that the consumer electronics chain would spend more than $2.5 billion on buybacks in 2021 while hiking prices on appliances. “In most cases, we’ve flowed those prices on to the consumer,” he explained.

More from Lee Harris

Brokers who string together strained supply chains have also seen swollen profits. The meat industry, which has shown some of the most dramatic inflation in the economy, is patrolled by a concentrated group of meat processing middlemen who buy low from ranchers and sell high to consumers at the grocery store.

Many bottlenecks in this special issue stem from domestic underinvestment, offshoring, or oligopolies’ multiyear strategy to roll up an industry. By contrast, the saga of the shale boom—underwritten by banker ebullience, cheap credit, and public support—is a story of homegrown misinvestment. After years of struggling to cartelize, collapsing demand in 2020 finally shocked the industry into a wave of mergers. By the following summer, the investors who bailed out distressed frackers saw their demands for lower production and higher profits (and prices) finally realized.

Commodity traders, who arbitraged across pandemic-induced dislocations and benefited from the volatility of fossil fuel commodities, are poised to further exploit bottlenecks in fossil fuels.

Vitol, the world’s biggest oil trader, distributed $2.9 billion to partners in just the first half of last year, averaging a $7 million bonus per partner. That’s on top of $2 billion in payouts in 2020—the same year oil prices went negative. The pandemic-time profits weren’t a one-off. The private trading houses are gearing up for years of sustained higher profits, anticipating that the same chronic underinvestment facilitated by the fracking pullback will now deliver a “commodities supercycle.”

AS LOCKDOWNS LIFTED AND LIFE RESUMED last year, oil supply lagged surging demand. OPEC Plus, the expanded consortium of oil-exporting nations, ramped up quotas to meet a growing appetite, but inventories were low and production had idled. Prices nearly doubled over the year. Entering 2022, key OPEC producers like Nigeria and Russia are still underperforming relative to their allotments, though rising production from the United States, Canada, and Brazil—all of which expect to pump at their highest-ever levels this year—could lift supply.

The rise in energy prices has an outsize impact on inflation. Rising prices at the pump are a bigger attention-grabber than aggregate figures like the Consumer Price Index, though that measure also gives energy a heavy weighting. While lagging energy production may seem understandable following the pandemic, OPEC producers’ slow ramp-up is only part of the story.

Investors in American shale oil—in the past, the most flexible barrel available to global markets, playing a pivotal role as swing producer—have exacerbated the price spike by holding down production, compared with past run-ups, as demand resumed.

Energy, like the tech sector, had been a growth industry for the 2010s.

From 2010 to 2019, a whopping 80 percent of the addition to global oil and gas demand was met by U.S. production growth, according to Kevin Book, the head oil and gas analyst at ClearView Energy Partners.

That growth kept a lid on prices—and on profits, as many smaller players entered the sector. But as demand picked back up last year, shale oil producers postponed new expenditures, wringing out yield for their long-suffering investors. That delay, energy analysts say, drove most or all of the energy price increase last year.

That the shale boom contracted sharply in 2021, leaving consumers in the lurch, has been shrugged off by analysts as an overdue market correction. Gas output has dropped, “but with good reason.” Frackers are finally “learning to live within their means.” The shock concluded years of shoveling good money after bad. And anyway, others rightly point out, fracking must end due to its climate-heating emissions and toxic air pollution.

This indifference to fracking’s demise—reports of which may be exaggerated—ignores years of malinvestment in shale, driven by animal spirits and the kind of governmental support that renewable investors can only dream of.

“WE PRODUCE MORE NATURAL GAS than ever before—and nearly everyone’s energy bill is lower because of it,” President Obama bragged in his 2013 State of the Union.

Hydraulic fracturing—breaking up shale to suck out oil and gas—roared to life under the Obama administration, which enthusiastically backed the natural gas boom in its tender years. Claiming energy independence as a victory for Democrats helped cement the industry as a bipartisan priority. While Obama also emphasized the transition to renewables in speeches, and with anemic federal grants under his recovery act (ARRA), his unequivocal backing of shale sent a strong signal to markets, helping launch a decade-long boom. Responding to that regulatory signal, Wall Street banks joined pension funds and regional banks around the U.S. shale patch in betting hard on new drillers.

Other unconventional fuels that developed over the decade require longer-term undertakings. Deepwater rigs and Canadian tar sands mines take years to open, but then produce steadily. Shale, however, is more capital-intensive, like a treadmill. Drilling sites are quick to open, but output can fall off, meaning one site can require continuous cash infusions to hold production steady.

The firm landscape that emerged—including new heavyweights like Anadarko, Marathon, Pioneer, and Chesapeake—was diverse compared to the long-standing dominant oil companies, with the low barriers to entry leading to many small and midsize participants. The romance of the wildcatter striking out alone wasn’t entirely a myth.

All were eager, at the first sign of higher prices, to ramp up investment. OPEC would try to cut production, prices would rise. Frackers would then ramp up capital spending and production, turn on the spigots, and prices would fall. The supply glut—and efficiency gains in the developing technology—left oil prices to plunge, as they did in the 2014–2016 collapse in oil prices.

BY LEE HARRIS

FEBRUARY 10, 2022

This article appears in The American Prospect magazine’s February 2022 special issue, “How We Broke the Supply Chain.” Subscribe here.

Following two decades of steeply rising corporate returns, Wall Street profits soared to extraordinary highs last year, despite inflation and the increased costs of securing and transporting goods. The stock market is thundering along, with S&P 500 earnings rising 45 percent in 2021, according to FactSet.

As the economy has staggered back from the pandemic, investors have ridden rising prices to higher returns. (Higher public investment during the past two years also explains some of the extraordinary profits.) “What we really want to find are companies with pricing power,” Giorgio Caputo, one portfolio manager, told Bloomberg. “In an inflationary environment, that’s the gift that keeps on giving.”

Stock buybacks helped retailers remit profits to shareholders. Best Buy CFO Matt Bilunas told investors on a November earnings call that the consumer electronics chain would spend more than $2.5 billion on buybacks in 2021 while hiking prices on appliances. “In most cases, we’ve flowed those prices on to the consumer,” he explained.

More from Lee Harris

Brokers who string together strained supply chains have also seen swollen profits. The meat industry, which has shown some of the most dramatic inflation in the economy, is patrolled by a concentrated group of meat processing middlemen who buy low from ranchers and sell high to consumers at the grocery store.

Many bottlenecks in this special issue stem from domestic underinvestment, offshoring, or oligopolies’ multiyear strategy to roll up an industry. By contrast, the saga of the shale boom—underwritten by banker ebullience, cheap credit, and public support—is a story of homegrown misinvestment. After years of struggling to cartelize, collapsing demand in 2020 finally shocked the industry into a wave of mergers. By the following summer, the investors who bailed out distressed frackers saw their demands for lower production and higher profits (and prices) finally realized.

Commodity traders, who arbitraged across pandemic-induced dislocations and benefited from the volatility of fossil fuel commodities, are poised to further exploit bottlenecks in fossil fuels.

Vitol, the world’s biggest oil trader, distributed $2.9 billion to partners in just the first half of last year, averaging a $7 million bonus per partner. That’s on top of $2 billion in payouts in 2020—the same year oil prices went negative. The pandemic-time profits weren’t a one-off. The private trading houses are gearing up for years of sustained higher profits, anticipating that the same chronic underinvestment facilitated by the fracking pullback will now deliver a “commodities supercycle.”

AS LOCKDOWNS LIFTED AND LIFE RESUMED last year, oil supply lagged surging demand. OPEC Plus, the expanded consortium of oil-exporting nations, ramped up quotas to meet a growing appetite, but inventories were low and production had idled. Prices nearly doubled over the year. Entering 2022, key OPEC producers like Nigeria and Russia are still underperforming relative to their allotments, though rising production from the United States, Canada, and Brazil—all of which expect to pump at their highest-ever levels this year—could lift supply.

The rise in energy prices has an outsize impact on inflation. Rising prices at the pump are a bigger attention-grabber than aggregate figures like the Consumer Price Index, though that measure also gives energy a heavy weighting. While lagging energy production may seem understandable following the pandemic, OPEC producers’ slow ramp-up is only part of the story.

Investors in American shale oil—in the past, the most flexible barrel available to global markets, playing a pivotal role as swing producer—have exacerbated the price spike by holding down production, compared with past run-ups, as demand resumed.

Energy, like the tech sector, had been a growth industry for the 2010s.

From 2010 to 2019, a whopping 80 percent of the addition to global oil and gas demand was met by U.S. production growth, according to Kevin Book, the head oil and gas analyst at ClearView Energy Partners.

That growth kept a lid on prices—and on profits, as many smaller players entered the sector. But as demand picked back up last year, shale oil producers postponed new expenditures, wringing out yield for their long-suffering investors. That delay, energy analysts say, drove most or all of the energy price increase last year.

That the shale boom contracted sharply in 2021, leaving consumers in the lurch, has been shrugged off by analysts as an overdue market correction. Gas output has dropped, “but with good reason.” Frackers are finally “learning to live within their means.” The shock concluded years of shoveling good money after bad. And anyway, others rightly point out, fracking must end due to its climate-heating emissions and toxic air pollution.

This indifference to fracking’s demise—reports of which may be exaggerated—ignores years of malinvestment in shale, driven by animal spirits and the kind of governmental support that renewable investors can only dream of.

“WE PRODUCE MORE NATURAL GAS than ever before—and nearly everyone’s energy bill is lower because of it,” President Obama bragged in his 2013 State of the Union.

Hydraulic fracturing—breaking up shale to suck out oil and gas—roared to life under the Obama administration, which enthusiastically backed the natural gas boom in its tender years. Claiming energy independence as a victory for Democrats helped cement the industry as a bipartisan priority. While Obama also emphasized the transition to renewables in speeches, and with anemic federal grants under his recovery act (ARRA), his unequivocal backing of shale sent a strong signal to markets, helping launch a decade-long boom. Responding to that regulatory signal, Wall Street banks joined pension funds and regional banks around the U.S. shale patch in betting hard on new drillers.

Other unconventional fuels that developed over the decade require longer-term undertakings. Deepwater rigs and Canadian tar sands mines take years to open, but then produce steadily. Shale, however, is more capital-intensive, like a treadmill. Drilling sites are quick to open, but output can fall off, meaning one site can require continuous cash infusions to hold production steady.

The firm landscape that emerged—including new heavyweights like Anadarko, Marathon, Pioneer, and Chesapeake—was diverse compared to the long-standing dominant oil companies, with the low barriers to entry leading to many small and midsize participants. The romance of the wildcatter striking out alone wasn’t entirely a myth.

All were eager, at the first sign of higher prices, to ramp up investment. OPEC would try to cut production, prices would rise. Frackers would then ramp up capital spending and production, turn on the spigots, and prices would fall. The supply glut—and efficiency gains in the developing technology—left oil prices to plunge, as they did in the 2014–2016 collapse in oil prices.

JAE C. HONG/AP PHOTO

Hydraulic fracturing, as seen in this oil field in California, boomed under the Obama administration.

For years, oil production fluctuated within the so-called “shale band”—between around $40 a barrel and $65 a barrel, the price above which shale producers aggressively ramped up production.

Frackers seemed to defy gravity. Even as profits failed to materialize, investor enthusiasm persisted. The logic was self-reinforcing: High debt burdens fueled the boom, as frackers would roll over their debts repeatedly, paying off old loans with new ones. Low interest rates helped, too. Investors were searching for yield wherever they could find it. A decade of quantitative easing made more investors willing to take risks on producers who were drilling with less regard to the profitability of their own internal balance sheets.

But low interest rates and public investment don’t explain the full story of shale’s multiple leases on life.

“One of the only reasons they got away with it was that the independence story moved hearts,” Book said. “The idea that America was winning its energy independence was just as persuasive in the 2010s as the idea that solar stocks, a decade before, were saving the world.”

The energy independence story was persuasive because it was true—even if unsustainable, both ecologically and economically. And the failure of frackers to stanch the supply glut was hardly a problem for end users of gas, who benefited from years of depressed prices.

But there was growing unrest among investors. “Half a trillion dollars was more or less set on fire, as producers chased more production, and in the process depressed the global price of oil. They never really made much money out of it,” said Rory Johnston, a commodities economist at the investment firm Price Street. “Any profits you could get out of shale producers were filed back into more investment, which is ultimately kind of self-defeating.”

ALREADY IN 2018, MARKETS WERE SOURING on shale for overpromising and underdelivering. Mergers increased, with executives, private equity investors, and corporate raiders like Carl Icahn citing disappointing profits as the impetus.

Energy, like the tech sector, had been a growth industry for the 2010s, said Andrew McConn, an oil and gas analyst at industry consultancy Enverus. As it matured, shale companies began looking to attract yield-oriented investors as opposed to the growth-oriented ones who’d been more tolerant of lower returns.

“At the beginning of an industry, if you treat shale like an independent industry, it’s good to have lots of firms that innovate and compete and grow,” McConn said. But that sentiment has changed as investors have become impatient with low returns and have sought economies of scale. “It’s just very simply a desire for profitability, a desire to pivot from the growth phase in the industry to distributions.”

That assessment triggered a spate of shale tie-ups during the pandemic. Three of the four quarters with the highest deal value for corporate mergers and acquisitions since 2012 occurred after mid-2020, an Enverus analysis found. In the second quarter of 2021, the sector saw more than 40 deals valued at $33 billion.

Expand

By last summer, shale strategy had flipped on its head: Rather than reinvesting more than 100 percent of new investments into drilling, frackers were holding oil fields idle while raking in cash, sending payments back to investors in the form of buybacks or special dividends.

As prices marched upward into the fall, the industry’s newfound restraint held. Public shale companies clocked $4.1 billion in free cash flow—a measure of liquidity—in the first quarter of 2021. By the third quarter, consultancy Rystad found, they underspent by around $7 billion.

Only now are those companies bringing production back, and more cautiously than they used to. Rig counts are rising about one-third as fast as they did in the last few run-ups, according to Book. (The numbers aren’t perfect comparisons, because rig productivity also increased over that interval, but it’s a good proxy for level of investment.) Of course, rising prices tempt investors and individual firms to drill harder. But collectively, they’re showing more restraint.

Some observers have asked how the industry achieved this newfound capital discipline. Fewer competitors and stricter restrictive covenants on production may have helped. Public information is scant, but some analysts have speculated that it was the oil majors that may have bailed out frackers—who in previous binges have driven down prices—at the bottom of the market, and mandated lower production levels.

Asked about speculation that majors might have funded smaller operators, Book said, “It wouldn’t surprise me.” If you’re trying to raise alternative capital, he said, it would have to come from nations’ sovereign investment funds, private equity, or corporate investment. “Sovereigns probably weren’t interested. Private equity was probably more interested, although some of them got burned, and were also going to probably demand some pretty hard terms. But yeah—why not oil companies? Of course.” (If big oil companies lent to distressed shale firms, some argue that move could raise antitrust concerns, since oil majors would have an interest in holding down production as oil prices rose.)

FRACKING ALSO RECEIVED GENEROUS federal support during the pandemic. The Federal Reserve launched a Main Street Lending Program to provide emergency support to small and midsize businesses. Initially, that program wouldn’t have supported businesses as heavily indebted as shale companies. But after Trump energy secretary and former energy lobbyist Dan Brouillette pushed on behalf of the industry, the Fed changed the program’s terms to let more heavily indebted companies get loans, and allow them to use the loan funds to refinance existing debt. Researchers have found that the Fed’s secondary market bond-buying program, meant to be sector-neutral, is disproportionately tilted toward energy bonds.

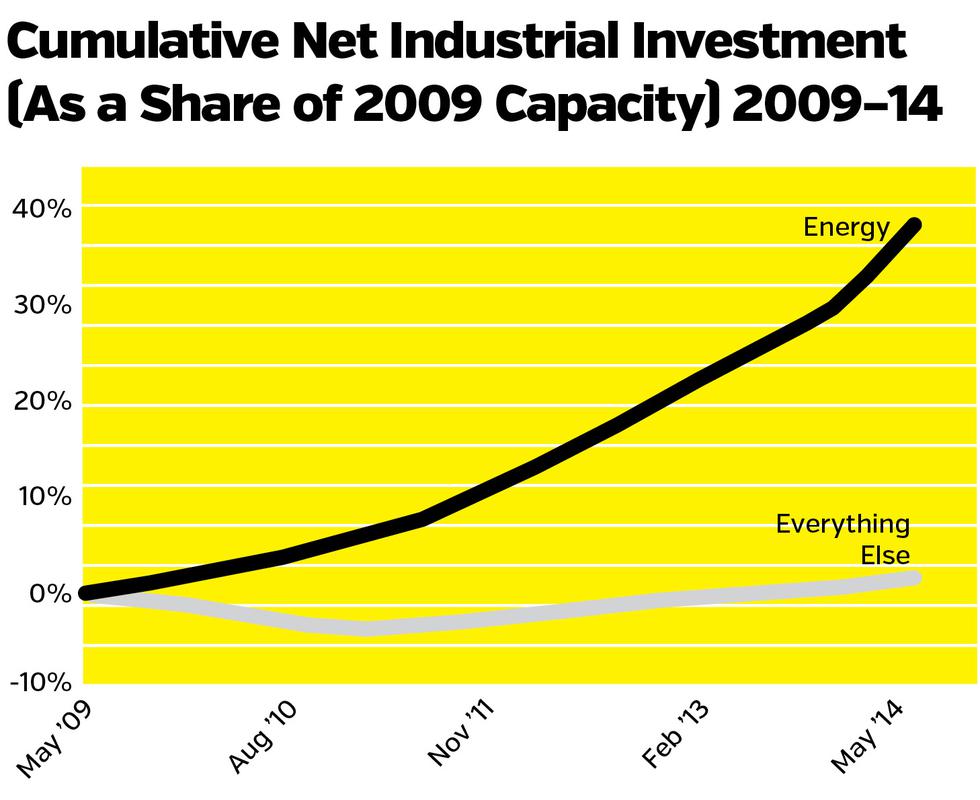

As markets appear to turn on shale, it’s a good time to look back at the limitations of the boom. Between 2009 and 2014, investment in equipment for oil and gas field exploration accounted for a major share of all industrial investment.

Sleepy towns in Texas and Oklahoma and deindustrialized Pennsylvania were suddenly poster children for fracking. Cheap natural gas was said to be giving new hope to the Rust Belt. Many of those jobs, however, which never unionized, have evaporated as quickly as they appeared. Even more striking is how little America was able to capture knock-on economic gains from cheap oil, which did surprisingly little to lift growth. On the contrary: Along with slowing growth in China, the shale energy boom and resulting oil glut helped set off a commodity price shock in 2014–2015. A global slowdown ensued.

THE PAST YEAR ALSO SAW commodity traders expand their ability to influence energy prices, despite earlier efforts to limit their sway. During the tumult of 2008, the growth of ETFs and mutual funds helped push up commodity prices.

Gary Gensler, who was then chairman of the Commodity Futures Trading Commission (CFTC), decided to impose position limits to curb that speculation, with a particular focus on energy commodities like oil and natural gas. Those rules only went into effect over a decade later, however, under a Trump-appointed CFTC, at which point they had been seriously watered down by industry.

While the new position limits improve a trading environment that had previously lacked any guardrails, said Tyson Slocum, an advocate with Public Citizen and member of the CFTC’s Energy and Environmental Markets Advisory Committee, they will not achieve their goal of controlling excess speculation, since they actually expand the ability of commodity exchanges to grant exemptions to traders. For-profit exchanges make money based on trading volume, so position limits, which would reduce trading volume, could lower their fees.

“The exchanges are for-profit companies. They are financially conflicted, here, and should not be in charge of calling balls and strikes, because they’re not a neutral umpire,” Slocum told the Prospect. CFTC Commissioner Dan Berkovitz echoed those objections in a dissenting statement on the flawed rule.

Political backlash to banks’ lucrative oil trading in 2008 also changed market structure. As Congress was negotiating a TARP bailout for top Wall Street banks, news emerged that a top trader at Citigroup’s Phibro trading desk had made so much money for Citi in 2008 that he was due a $100 million cash bonus. Under pressure, Citi sold Phibro to the shale firm Occidental.

As Wall Street’s turbulent romance with fracking was kicking off, foreign commodity trading houses—Swiss-based Mercuria and Glencore, Dutch Vitol, Singapore’s Trafigura—also saw a chance to step in.

By last summer, rather than reinvesting into drilling, frackers were holding oil fields idle while raking in cash.

Private commodity traders also took advantage of pandemic-driven supply chain dislocations, snapping up barrels of crude when prices went negative and orchestrating deals as shipping lines seized up. Trafigura’s profits—its highest ever—increased by 57 percent last year as the company hauled in $231.3 billion in revenue.

The pandemic wasn’t a one-off. Trading firms do best in conditions of market turmoil, so they’ve also done well in price slumps like 2015’s. Now they are preparing for a “commodities supercycle”: sustained high prices in materials. Even as they anticipate a renewables push into metals and minerals like lithium (for batteries), energy traders expect the surge will be greased by greater investments in oil and gas.

Trafigura is well placed to continue capitalizing on market dislocations due to “chronic under-investment,” the company says in its 2021 annual report. The co-heads of oil trading add in a note that the firm is especially well positioned given its vertical integration. “Trafigura is one of the few crude oil trading houses positioned to operate an integrated supply chain from wellhead to refinery, based on close cooperation between the crude desk and the in-house shipping team and the use of Trafigura-owned vessels or long-term charters.”

While real-world disruptions furnished huge opportunities for commodity traders, a handful of the biggest houses disproportionately nabbed those deals. For most trading shops, The Wall Street Journal reported, the sector’s bumper year ironically encouraged market concentration. For smaller commodities firms, “funding has rarely been harder to come by.”

LOOKING AHEAD, PRIVATE TRADERS and commodity bulls like Goldman Sachs are predicting years of elevated prices to correct for protracted underinvestment. Some of that profitable uncertainty will come from a politically erratic push into clean energy, where a new metals-based economy will need to be fed by heavy mining of minerals like copper and lithium.

Bulls are counting on a global shift toward green industrial policy, in fits and starts, to fuel the supercycle. Top trading analysts also cheerfully predict a broader end of austerity and a shift toward more public investment.

“When you stimulate low-income groups, you create the type of demand growth that’s behind commodity supercycles,” Jeff Currie, Goldman’s global head of commodities research, recently argued on a podcast about the commodity sector.

Currie is betting that these two trends—the clean-energy transition and redistributionist fiscal policy—will drive a structural rise in demand, as people spend more on everything from gas to green appliances.

Although investors are re-entering shale more cautiously, traders are not treating the energy transition as a zero-sum pivot away from fossil fuels. On the contrary, they are especially bullish on rising oil prices, which Trafigura predicts will continue into 2022, “underpinned by general under-investment in new crude oil production.”

It’s not inevitable that commodity traders will make out like bandits in the coming investment bonanza. Their revenues depend on market fluctuations under volatile conditions. In theory, then, maximalist industrial policy that sends an unambiguous signal on clean-energy investment could decrease political whipsawing and put a damper on traders’ profits.

For now, however, the major commodity houses are still betting on a supercycle that repeats Obama’s climate-smoking energy strategy: “all of the above.”

LEE HARRIS is a writing fellow at The American Prospect.

No comments:

Post a Comment