RENT INCREASES = INFLATION

Toronto apartment rents soar 20% to record with market tightening

, Bloomberg News

Toronto tenants are saying goodbye to the era of COVID-19 discounts, with rents fully recovering pandemic losses and reaching record levels, according to new data.

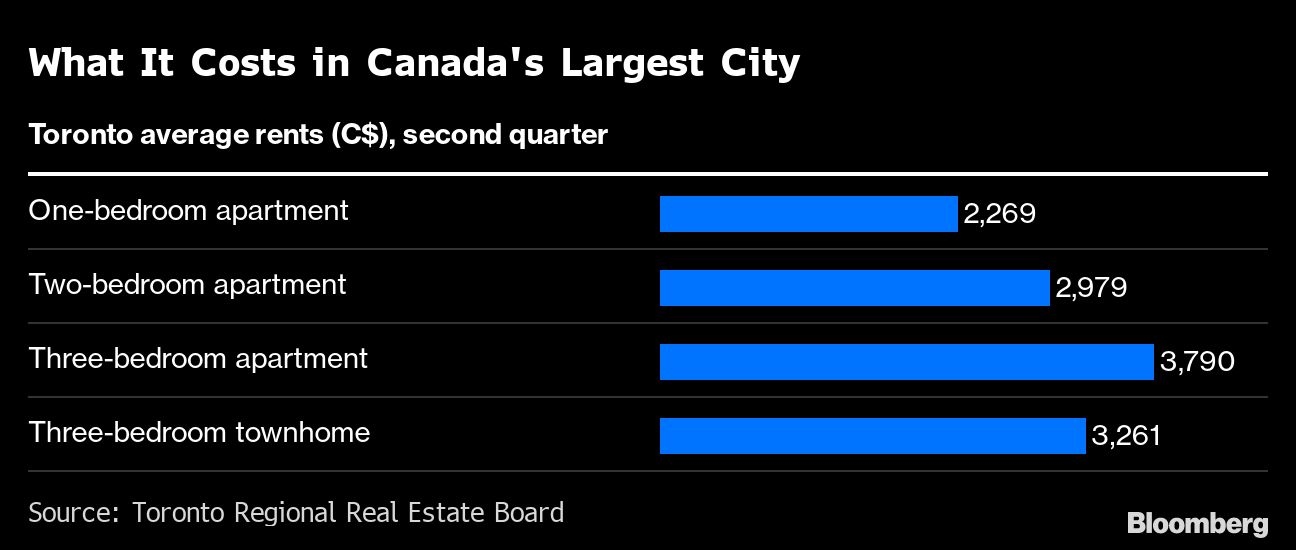

Average monthly rents on newly-leased one-bedroom apartments in Canada’s largest city rose to $2,269 in the second quarter, up 20 per cent from a year earlier, the Toronto Regional Real Estate Board said Thursday.

Rents on two-bedroom homes, at $2,979, were up 15 per cent from year-ago levels. The cost of three-bedroom apartments rose 13 per cent.

The double-digit price gains reflect a decline in the number of leased listings, which are down 11 per cent from a year ago, according to the report.

The pandemic led to a sharp increase last year in apartments listed as people left city centers. Now, as the COVID crisis eases, some of them are returning. Rising interest rates, meanwhile, will price many potential homebuyers out of the market and keep demand elevated for rental units.

“Expect rental market conditions to tighten further in the coming months,” Kevin Crigger, president of the real estate board, said in the statement.

Rents hit four-year lows last year as demand dried up and listings surged. The previous record for one-bedroom rents was $2,262, reached in the third quarter of 2019.

Justin Wu, a realtor in Toronto, said that it’s been challenging to find apartments for even the most qualified tenants, and that some landlords have been closing offers with down-payments of four months to one year worth of rent.

“We had one client that was very qualified, had excellent credit and income but we couldn’t find her anything,” Wu said by telephone. “Everything we tried to put an offer on had nine to ten offers. We had some where the competing offers were offering 12 months of rent up front.”

Homebuilding delays and cancellations -- the result of rising construction costs, higher rates and labor shortages -- are putting further upward pressure on rents.

Out of the 30,000 condo units that were supposed to be built this year, approximately 10,000 have been canceled or paused, according to a note by Benjamin Tal, deputy chief economist at CIBC Capital Markets.

GTA condo rents climb at fastest pace on record: Urbanation

, BNN Bloomberg

Jul 19, 2022

Condo rental prices climbed at a record pace in the Greater Toronto Area during the second quarter of this year following a sharp drop in available homes to rent, according to industry tracker Urbanation Inc.

Urbanation found that the average rental price per square foot rose 5.9 per cent quarter-over-quarter to a new high of $2,533. As well, annual rental growth prices rose by a record pace of 16.7 per cent in the second quarter, the data showed.

The decline in condo inventory comes at a time when some buyers are being priced out of the housing market because of the rising interest rates. Urbanation also pointed toward strong population growth and near record-low unemployment in the GTA have contributed to the growing rental demand.

“The GTA rental market was as strong as ever heading into the peak summer months, which is sure to place further downward pressure vacancies and upward pressure on rents,” according to Shaun Hildebrand, president of Urbanation, in a statement.

Urbanation said tenants sought smaller and more affordable condo units to rent, a segment that reported stronger rental growth than larger spaces. That demand caused the overall vacancy rate in the GTA to fall to 1.4 per cent from 5.1 per cent a year earlier.

Rental supply is expected to remain tight as new rental construction almost completely stopped in the second quarter of 2022 with only 87 rental starts, compared to the average of 1,916 starts during the preceding four-quarter period.

YOU NEED AN INCOME OF OVER $220K TO

BUY A HOME IN TORONTO, VANCOUVER,

NEW DATA SHOWS

, The Canadian Press

Jul 21, 2022

You'll need to be making more than $220,000 to buy a home in Toronto and Vancouver with a 20 per cent down payment, according to new data from Ratehub.ca.

Even though home prices have been going down in hot markets like Toronto and Vancouver, the income required to purchase a home in these markets still remains elevated due to higher stress test rates caused by rising mortgage rates.

Ratehub.ca says it used March 2022 and June 2022 real estate data to make the calculations.

Homebuyers in Toronto need to earn $15,750 or seven per cent more compared with March, with those in Vancouver needing to make $31,730 or 16 per cent more.

Across all Canadian cities, the annual income needed to buy a home has jumped by $18,000 on average in just the last four months.

Victoria, B.C. saw the biggest increase in June compared to March, with $35,760 or 23 per cent in additional income required.

"Home prices will need to drop significantly in order to neutralize the effects that higher mortgage rates have on the stress test," Ratehub.ca co-CEO James Laird said in a statement. "Unless this happens, home affordability will continue to be impacted significantly by the current rising rate environment."

Rapidly rising interest rates have pushed Canadian home prices down in recent months, with the average price of a home falling 1.9 per cent in June compared to May, according to the Canadian Real Estate Association (CREA).

June was the third consecutive month of declining prices, and the biggest monthly drop since 2005.

BMO Capital Markets senior economist Robert Kavcic said in a July 15 note that the Bank of Canada's recent move to boost its key interest rate by a full percentage point is setting the stage for an even deeper housing market correction in 2023.

Kavcic said the hike which prompted the commercial banks to increase their prime rates has made it more difficult to qualify for a mortgage under Canada's stress test rules.

The stress test sets the qualifying rate for uninsured mortgages at either two percentage points above the contract rate or 5.25 per cent, whichever is greater.

Bank of Montreal, CIBC, RBC, Scotiabank, TD Bank and National Bank raised their prime rates by a full percentage point to 4.70 per cent from 3.70 per cent last week in response to the central bank's hike.

Five-year fixed rates continue to hover around or slightly above five per cent.

"A lot of potential buyers are sitting on the sidelines at the moment waiting to see how this rate environment shakes out, which is why you've seen transaction volume down so significantly in those major markets. But the demand is still there," Ratehub.ca's Laird said in an interview.

Rental rates are increasing so that would provide support for the market from an investor perspective, first-time buyers still desire to enter the market and many new Canadians prioritize owning a home when they get here, he explained.

"If rates moderate at this level or hold at this level, I expect to see a reasonable fall home buying cycle. If rates keep going up then I think we'll keep seeing people waiting on the sidelines."

No comments:

Post a Comment