Aerial view of Merdeka square in Jakarta. Stock image.

He’s the biggest trader in the world’s top producer of nickel, a metal that’s powering the shift to batteries and electric cars. His firms handle billions of dollars worth of ore and own stakes in mines covering an area around the size of New York City. Yet even in the metals industry, few know the name Arif Kurniawan.

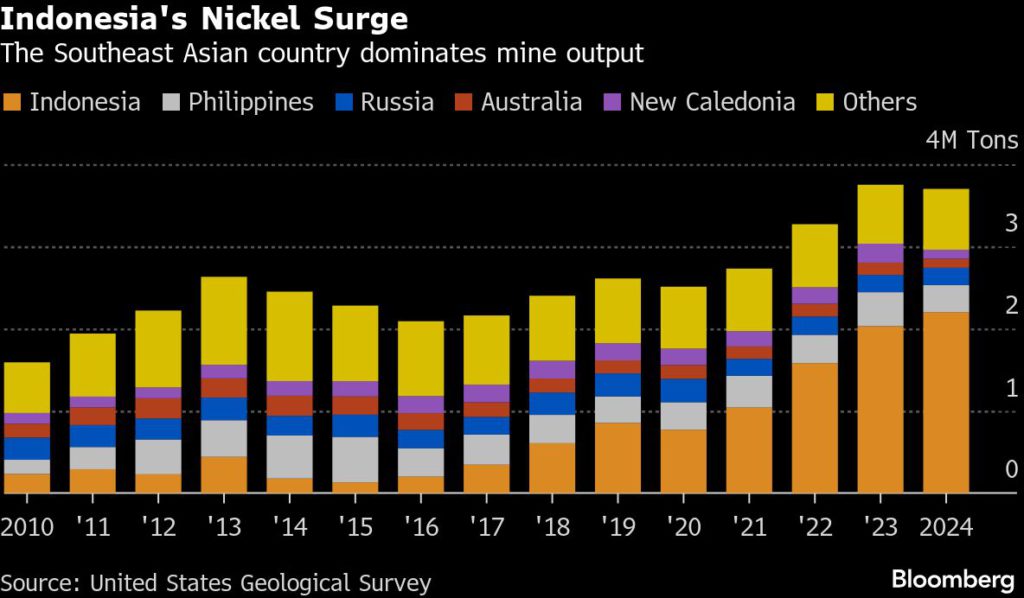

Indonesia’s nickel sector has seen a dramatic rise in recent years, as technological innovation turned vast, low-grade deposits into mining dominance and industrial clout. Kurniawan’s fortunes have tracked that ascent. In under a decade, he has gone from earning paychecks at Glencore Plc to controlling approximately a third of his country’s domestic trade in nickel ore.

“Indonesia has been a complete disruptor of the nickel market over the last 10 years,” said Angela Durrant, principal analyst of base metals at consultancy CRU Group based in Sydney. “These local guys are the power brokers.”

Much has been written about the Chinese tycoons who poured billions into processing nickel in the Southeast Asian nation, flipping the global market and wrongfooting rivals. Less has been said about the Indonesians who control the mines that are the ultimate source of the metal, and about the influence they wield.

This first account of Kurniawan’s rise is based on interviews with more than 19 miners, traders and smelters familiar with his operations, who did business with or worked alongside him, as well as dozens of filings from Indonesia’s company registry. Most of the people asked not to be identified so they could discuss private matters.

When contacted through two business associates, Kurniawan declined to comment for this story.

The route to prominence and wealth in Indonesia often passes through a family business. Kurniawan’s solo rise speaks instead to his alliances, skills and the speed of the country’s industrial transformation over the last decade. It also underscores the precarious nature of the achievement, as President Prabowo Subianto shakes up the mining industry and ignites a new battle for control of the country’s resources.

Kurniawan and his main business partner, Edi Liu Amas, between them have stakes in at least 20 mining concessions across the country’s major nickel centers, according to a Bloomberg analysis of corporate filings. These span more than 71,000 hectares (175,000 acres), an area roughly as large as New York City and far bigger than Weda Bay Nickel, the world’s largest mine in eastern Indonesia.

There’s no recent public data on Indonesia’s nickel ore trade, but according to the average estimate of a dozen fellow traders, miners and smelters, Kurniawan traded about a third of the ore market last year, excluding a small amount of supply consumed by integrated conglomerates. Based on last year’s production of 220 million tons, according to figures cited by Macquarie Group, and current government benchmark prices, a rough estimate would put his annual volumes at around $3 billion.

This is a remarkable slice of the flows that underpin Indonesia’s nearly 70% of global nickel production, a level of control that has made the country critical for the world’s battery industry — all at a time when China is using its own stranglehold on parts of the wider supply chain to fight back against punitive tariffs.

“It’s unsurprising that the Indonesian market for nickel ore provides lucrative opportunities for savvy traders like Arif Kurniawan,” said Ian Hiscock, Singapore-based director at MMC, a critical minerals consultancy.

“An environment of constantly changing regulations, ore export bans and short-term mining licenses provides no incentive for nickel miners to make long-term plans. The sector is highly fragmented with more than a hundred small operations,” Hiscock said. “Since smelters and refineries require a steady supply of ore at a consistent quality to operate efficiently, a large gap is created for a trader to absorb — and profit from — the volatility.”

A slight man who is believed to be in his 40s, Kurniawan is part of Indonesia’s ethnic Chinese minority, a community long prominent in local commerce and particularly associated with powerful conglomerates during Suharto’s New Order era. Other than that, little is known about his background.

The trader keeps a low public profile and avoids social media. He dresses casually and eschews displays of wealth, maintaining the unassuming manner of his early days, according to people who know him — only the cluster of mobile phones next to him during meetings hints at his clout.

In the early 2000s, he was working at Glencore’s office in Jakarta, initially in the much larger coal division before transferring to the commodity giant’s nickel business, according to the three former colleagues who asked to remain anonymous discussing private information about his past. At the time, Indonesia’s nickel industry was less than a 10th of its current size, and the London-listed firm was largely focused on exporting ore from its mine in the country.

The sector was about to be transformed. A first key development was a ban on ore exports that took effect in 2014, as Indonesia’s government sought to shift from being an exporter of raw ore to a center for processing and manufacturing. That led to the expansion of Chinese firms, including the giant conglomerate Tsingshan Holding Group Co., which set up big smelting operations in the country. They brought with them technologies including furnace methods that allowed for low-cost production of nickel pig iron, a material used to make stainless steel.

Then came a technique called high-pressure acid leaching, or HPAL, that made it possible to produce battery-grade nickel from Indonesia’s plentiful, lower-grade ore — and upended the global industry.

Glencore sold its mining stake in 2013 as Indonesia prepared to introduce the ban. Shortly after, Kurniawan left the company to start a quarrying business. The new venture didn’t work out, so he rejoined Glencore, according to two of his former colleagues.

When he returned, Kurniawan wanted to expand Glencore’s ore trading business in the country, but the firm was reluctant to deal with the small miners who even now account for about half of production, according to a person familiar with the company who asked not to be identified as the discussions were private. Many nickel producers in Indonesia have opaque ownership, unreliable accounts and poor records of their mineral resources, which presented an unacceptable level of risk for the Switzerland-based trader, Kurniawan’s three former colleagues said. Glencore declined to comment.

Kurniawan set off alone once again, the three people said. His flagship PT Dua Delapan Resources — meaning 28 Resources in Indonesian, a nod to nickel’s atomic number — had been founded in 2015, according to a filing from Indonesia’s Ministry of Law. His trading unit was founded in 2018, according to another filing. Some of his former colleagues joined the new company, the people said.

The timing could hardly have been better for the man who became “Mr 28.” Indonesia’s government, which had eased ore export restrictions that year, was flagging plans to ban exports again, and the Chinese firms were rapidly building smelters.

Kurniawan, who speaks Mandarin, Indonesian and English according to multiple people who have met him, became a crucial intermediary between the Chinese businesses and the patchwork of small mines dotted across the nation of more than 17,000 islands. He had a ready network of local contacts, and the trading instincts developed at his former employer.

He started with small volumes and quickly built his business, according to competitors. Mirroring Glencore’s approach, Kurniawan constantly reinvested his profits in the supply chain to gain influence, buying a portfolio of mines whose production he could trade. He snapped up many of them before 2021, when nickel prices were low, according to corporate filings and three people familiar with the matter.

His path has not always run smoothly. Tsingshan, the incumbent heavyweight, was reluctant to work with a trader who was consolidating supply and could undermine its buying power with smaller miners, five people familiar with the matter said.

So Kurniawan turned to the second-biggest player, Jiangsu Delong Nickel Industry Co., another conglomerate whose operations were rapidly expanding and needed ore. He frequently visited the Chinese firm’s Jakarta offices, and was a key supplier to its three smelting operations on the island of Sulawesi, according to people who were involved in the dealings at the time. The two groups even co-invested in mines, according to data from Indonesia’s Energy and Mineral Resources Ministry.

Eventually, even Tsingshan started to work with Kurniawan. It was expanding two huge smelting parks in the country, and needed more ore. The two set up a joint venture for trading in 2021, according to the Energy and Mineral Resources Ministry website.

In response to Bloomberg queries, representatives of Delong and Tsingshan declined to comment.

Since 2022, ore market conditions have become more favorable to miners, as government restrictions on production led to shortages. Those with supply can demand near-record prices from smelters, whose survival increasingly depends on the favor of locals like Kurniawan.

At least four Chinese firms with plants in Indonesia have slashed output or idled plants, with the ore shortage driving up costs and prices for their products near record lows. Some have even defaulted on payments to creditors and suppliers.

“There is obscene demand for ore,” CRU’s Durrant said. “That tightness has just translated into elevated ore prices.”

Indonesian miners’ grip over the wider nickel market has also only strengthened. With rivals in Australia and New Caledonia squeezed out by its low-cost production, the Southeast Asian country is now in a position to manage the supply of the metal needed to make everything from electric vehicle batteries to aircraft. Jakarta has also tightened quotas issued by the government to the largely locally owned mining sector, another factor keeping ore supply from catching up with demand.

“The country is transitioning from being a marginal cost-setter to being a deliberate price floor architect,” Industrial & Commercial Bank of China Ltd. analyst Dongchen Zhao wrote in a note earlier this month.

That should shift yet more influence and profit to those who control ore supply — at the expense of the country’s largely Chinese-owned smelters.

That’s potentially a small win for Beijing’s geopolitical rivals, who have lagged behind in the race for critical metals, but not necessarily for Kurniawan. Competition for lucrative concessions has intensified just as the country undergoes a major political shift, with Prabowo taking over as president in October last year, ending Joko Widodo’s decade in power.

Jokowi, as the former leader is better known, oversaw the vast expansion of nickel mining and processing as part of an effort to boost the value of Indonesia’s natural resource exports and build a manufacturing sector. In that boom period for nickel, Kurniawan cultivated allies in the former president’s political party through partner Liu, according to people familiar with the matter. Liu did not respond to Bloomberg queries.

Prabowo has taken a different approach. He has increased the royalties demanded of miners to fund expensive projects, and has cracked down on illegal mining, which he claims costs the country billions of dollars in lost revenue every year.

His government is also seeking to punish companies at a massive smelting park owned by Tsingshan for environmental violations. A task force led by Defense Minister Sjafrie Sjamsoeddin has also seized tracts of land and is threatening punitive fines against mines alleged to have breached their forestry permits, among them one of Kurniawan’s concessions on the island of Kabaena.

“Prabowo is trying to signal that he really wants to improve the governance in Indonesia,” said Siwage Negara, a research fellow at the ISEAS-Yusof Ishak Institute in Singapore. The president’s methods, though, are not always transparent, he added. “He doesn’t really use the existing institutions and bureaucracy. He uses his own people.”

The Indonesian president’s office referred queries to the Energy Ministry, which did not respond to requests for comment.

Kurniawan has been out of Indonesia for much of this year, according to people in contact with him. The exact reason is unclear. His business has been in the hands of one of his subordinates, according to two of his clients.

Prabowo’s efforts to consolidate control under the presidency have not always favored the businessmen who flourished under Jokowi and earlier administrations. They’ve been asked to buy so-called patriot bonds, for example — debt instruments yielding lower than market rates that are issued by Danantara, the sovereign wealth fund started by the current president this year.

Kurniawan has built strong relationships over years, even without the name recognition of other tycoons. Maintaining his grip on the ore trade, though, will require the forging of new political alliances, according to people familiar with the matter, at a time when favor has rarely been more valuable — or more contested.

Lower nickel prices have not helped extend the sector’s influence, especially at a time of personnel change at the top, said political analyst Kevin O’Rourke at Reformasi Information Services, a Jakarta-based consultancy. “It’s a rearranging of the patronage networks,” he added. “It’s a new administration and a new set of supporters and allies. There’s an impetus to reward friends and punish enemies.”

(By Eddie Spence, Alfred Cang and Annie Lee)