It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

The global oil and gas industry is facing a severe downturn with widespread job losses and investment cuts.

Falling crude prices, exacerbated by OPEC+ output increases, are making it difficult for western majors to fund projects and shareholder payouts.

The downturn is significantly impacting the US shale industry and raising concerns about the future of domestic oil production.

Oil and gas producers worldwide are bracing for a prolonged downturn, with job losses and investment cuts spreading through the industry, according to a new report from Financial Times. ConocoPhillips, Chevron, and BP have all announced large-scale layoffs, while others are shelving or selling projects to conserve cash. “This isn’t just a Conoco problem,” said Kirk Edwards of Latigo Petroleum. “It’s a flashing red warning light for the entire US oil and gas industry.”

FT writes that the sector is under pressure as crude prices, which spiked after Russia’s invasion of Ukraine, have since dropped by half. Opec+ has shifted strategy, increasing output to regain market share, a move that adds further price strain. Analysts at Wood Mackenzie predict Brent could slide under $60 a barrel by early 2026 and stay there “up to a few years.” Below that level, western majors struggle to fund both shareholder payouts and new projects.

The cuts are hitting hardest in the US, where shale drilling requires around $65 a barrel to stay profitable, according to the Dallas Federal Reserve. ConocoPhillips has warned that as many as 3,250 staff may lose their jobs by Christmas, while Chevron has been working through 8,000 cuts since February. BP has already trimmed 4,700 positions. “The way we protect the most jobs for the most people is by remaining competitive,” said Chevron’s Mike Wirth.

State-owned producers are also retrenching: Saudi Aramco raised $10bn by selling part of its pipeline network, and Malaysia’s Petronas shed 5,000 jobs. Capital spending worldwide is forecast to fall 4.3% this year to $341.9bn — the first decline since 2020 — and US output is expected to contract for the first time since 2021.

Some companies are leaning on outsourcing and digital tools to offset the downturn. “AI is giving operators new ways to optimise in a challenging market,” said Andrew Gillick of Enverus. But industry veterans warn that shrinking investment may have long-term consequences. “Domestic oil producers are finding it hard… which is costing jobs,” said Roe Patterson of Marauder Capital. “The problem is that our domestic oil production may not be there when the country needs it in the future.”

Carbon markets are increasingly vital for companies and countries to reduce emissions and mobilize private capital, especially in developing nations, as public funding is insufficient to meet climate commitments.

The carbon market is progressing towards global standardization and higher integrity through initiatives like the ICVCM's Core Carbon Principles, despite ongoing fragmentation and slow implementation of regulatory reforms.

Demand for carbon credits remains resilient, with growing interest in tech-based removals, and the market's success hinges on reforms delivering transparency and durability to achieve climate targets.

Carbon markets have become increasingly important as a cost-effective pathway for companies and countries to reduce emissions in a world struggling to meet its climate goals. They can mobilize private capital, particularly in developing countries where clean technology financing remains scarce, and provide hard-to-abate sectors with access to solutions that would otherwise be out of reach. Climate finance pledges are materializing – the $100 billion goal was finally met and the Loss and Damage Fund launched, both in 2022 – but public funding alone remains too limited and slow. Moreover, around 1,400 of the world’s largest companies have set climate commitments with both interim and long-term targets. Near-term milestones are approaching, and direct cuts can be insufficient or costly, so more organizations are turning to carbon credits to help meet goals and stay on track towards net zero.

Today, most trading occurs across fragmented initiatives: some under regional, national or sectoral compliance schemes or globally through voluntary action – most of which operate with diverging standards and eligibilities. Progress at last year’s COP29 conference on operationalizing Article 6 of the Paris Agreement on climate change marked a step towards a global, standardized market. However, implementation will be slow: methodologies must be developed, infrastructure built, and political compromises resolved. In the meantime, integrity risks persist, and the market’s credibility depends on non-governmental initiatives that are setting tougher standards. The Integrity Council for the Voluntary Carbon Market’s (ICVCM) Core Carbon Principles – already referenced by several jurisdictions – signal this shift. Developers are issuing credits under these new rules, though buyers remain slower to adapt, with most retirements still tied to older, weaker methodologies.

Meanwhile, demand remains resilient. Retirements have already reached 110 million credits so far this year, outpacing last year’s levels at the same point in time by 5%, spanning sectors from energy and utilities to aviation and logistics. Tech-based removals are expanding rapidly – about 24 million credits sold so far this year, up 166% on 2024 – though supply is constrained by high costs, limited project pipelines and long delivery timelines. Nature-based removals and high-quality reductions, therefore, will remain essential, even if not all credits can achieve perfect one-to-one equivalence with emissions. The critical question is whether the whole system delivers durable climate value, not whether each credit is flawless.

The trajectory is clear: carbon markets are moving from a credibility crisis towards higher integrity, though progress remains uneven. Success will depend on whether reforms – both regulatory and voluntary – can deliver the transparency and durability needed to satisfy climate goals and compliance demand. In a decarbonization landscape where many other pathways are stalling, carbon trading remains a vital – if imperfect – lever for mobilizing finance and accelerating climate action.

By Petter Atrchi Aspestrand, Product Manager of Carbon Markets Research at Rystad Energy

U$ WAR ON THE ENVIRONMENT

U.S. Energy Chief Calls Net Zero a “Colossal Train Wreck”

U.S. Energy Secretary Chris Wright blasted net-zero targets as a “colossal train wreck” ahead of his trip to Europe for a gas summit and meetings with EU officials, warning the push for climate policies could weaken energy security and derail a U.S.–EU trade deal.

“Net zero 2050 is just a colossal train wreck,” Wright told the Financial Times in an interview.

“It’s just a monstrous human impoverishment program, and of course, there is no way it is going to happen,” said the Energy Secretary, whose remarks were also shared on X by the official account of the U.S. Department of Energy.

Secretary Wright, a former oil and gas executive, made his position on net zero known shortly after he was picked to lead the energy department earlier this year. Weeks earlier, the Trump Administration had given a loud and clear message on what it thinks of net zero on Day One—the day that President Donald Trump withdrew the United States from the Paris Agreement, again.

After years of aligning with Europe on the net-zero agenda under President Biden, the United States is now on a collision course with the EU and its climate regulations.

The EU’s Corporate Sustainability Due Diligence Directive and the Carbon Border Adjustment Mechanism (CBAM), commonly known as the “carbon border tax”, ultimately aim to impose levies on higher-emission products imported into the EU.

Many companies outside the EU, including those in the U.S., have signaled they would rather not sell in Europe than pay significant “border taxes”, levies, penalties, or whatever the language will be later this decade, when the mechanism will come into effect.

These rules and the EU’s “crusade” toward net zero are a threat to the U.S.-EU trade deal, Secretary Wright told FT.

“I think those regulations significantly threaten the ability to implement the trade deal that was agreed to,” he added.

The U.S.-EU trade deal for European energy purchases of American products already looks unrealistic, analysts say, even without accounting for all EU climate-related levies.

U.S. giant ExxonMobil hopes the ongoing U.S.-EU dialogue on trade would address the “bone-crushing penalties” in the EU’s climate regulations, the supermajor’s CEO Darren Woods told analysts on the Q2 earnings call last month.

Wright’s remarks from this week aren’t the first time the U.S. Energy Secretary has slammed the net zero agenda.

Europe’s goal to pursue a net-zero agenda is depriving citizens of reliable and affordable energy in a choice made by politicians, Wright said at a forum in Poland in April.

“This top-down imposition of enforced “climate policies” is justified as necessary to save the world from climate change,” Wright said.

“But I can say that climate alarmism has clearly reduced energy freedom, and, hence, prosperity and national security across Western Europe.”

Wright noted that affordability is more important than sustainability.

“Today, folks struggling to pay their bills while aspiring to live highly energized lifestyles like you and I is a far bigger global challenge than climate change. Energy access is far too important to get wrong,” Wright said.

The U.S. pushback against net zero has led to Secretary Wright saying that the United States could abandon the IEA if the organization, created in the aftermath of the 1970s Arab oil embargo, doesn’t return to forecasting energy demand without strongly promoting green energy.

“We will do one of two things: we will reform the way the IEA operates or we will withdraw,” Wright told Bloomberg in an interview in the middle of July.

“My strong preference is to reform it,” Secretary Wright added.

The official echoed voices in the U.S. Republican party that the agency has become an advocate of the energy transition and is not objective in forecasting energy demand trends.

From ensuring security of supply after the 1970s embargo, the agency has shifted from this purpose in recent years to endorsing the net-zero by 2050 goal and is advocating for a major change in the global energy system to include more electric vehicles (EVs), renewable power supply, hydrogen, and all other low-carbon energy sources.

The IEA’s forecast that oil demand will peak this decade is “just total nonsense,” Secretary Wright said.

By Tsvetana Paraskova for Oilprice.com

Teck-Anglo deal could boost Canadian critical mineral output: experts

Teck's zinc and lead smelting and refining complex, left, is pictured in Trail, B.C.

THE CANADIAN PRESS/Darryl Dyck

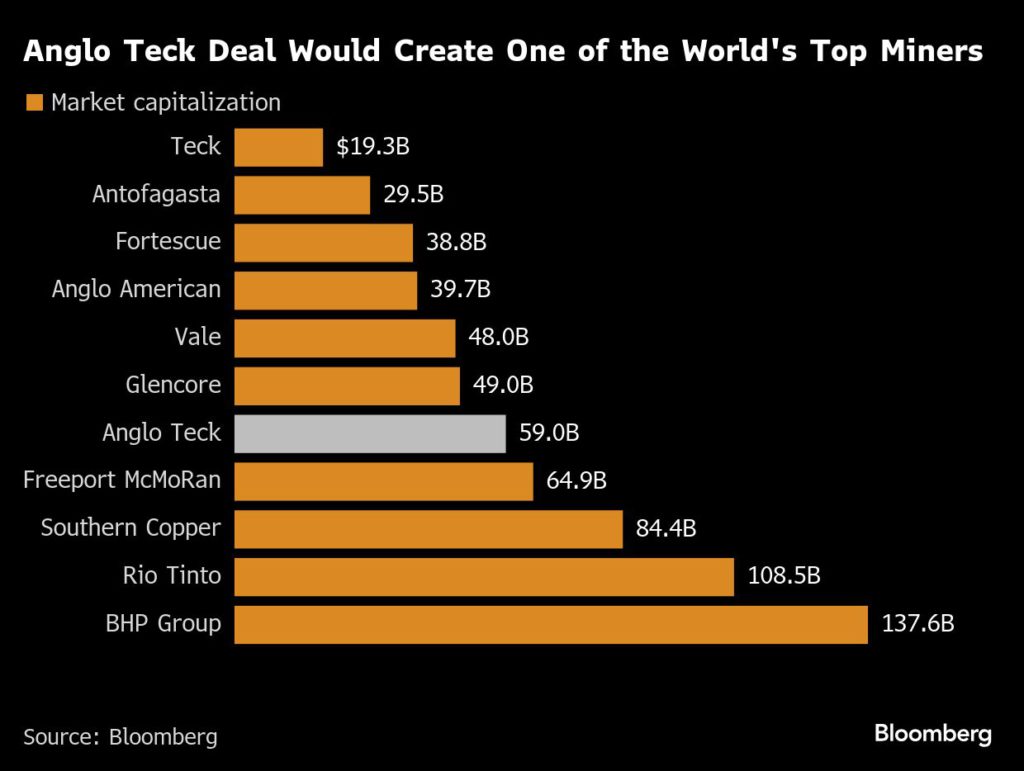

TORONTO — Experts say the proposed merger between Teck Resources Ltd. and Anglo American PLC to create a $70 billion, critical minerals-focused giant could help Canada’s efforts to boost production of the metals that are key to the energy transition.

John Steen, director of the Bradshaw Research Institute for Minerals and Mining at UBC, says the size of the combined company could help it move faster to develop mines than Teck could alone.

Teck and U.K.-based Anglo American have also committed to spend $4.5 billion in Canada over five years as part of its pitch to regulators for the deal, with a focus on the critical minerals space that the federal government has made a priority.

A good chunk of that spending is already committed by Teck, including upwards of $2.4 billion to extend the life of its Highland Valley Copper mine, but the companies say they will also spend on exploration as well as development in areas like B.C.’s Golden Triangle.

Steen says having what would be the world’s fifth-biggest copper producer be based in Vancouver would especially help efforts to produce more of the metal that will “make or break” the energy transition.

He says the potential for the combined company to add to copper processing capacity at Teck’s smelter in Trail, B.C., is notable as Canada has a shortage of critical minerals processing capacity, but that the company’s talk of supporting new processing facilities seems like a longer-term prospect given the difficulty of building them.

This report by The Canadian Press was first published Sept. 11, 2025.

Anglo’s go-to banker drives Teck deal after seeing off BHP

Centerview Partners LLC banker James Hartop has his own badge to get into Anglo American Plc’s headquarters near London’s diamond district. Rival advisers wait to be called in. It’s a symbol of the dealmaker’s bond with the century-old miner, and his crucial role in protecting it – most recently just last year when BHP Group made a $49 billion bid for its smaller rival.

That relationship meant that Hartop took the lead for Anglo as it negotiated with the Canadian miner Teck Resources Ltd., according to people with knowledge of the negotiations. The deal, which would create a $50 billion copper giant, is one of the largest in the sector in years.

Over three decades, the 51-year-old has become Anglo’s go-to banker for advice in an industry with a constant backbeat of mergers, takeovers and restructurings. This kind of connection has become rare, as the business of advising on large M&A has become increasingly commoditized. But Hartop’s long-term association with the miner has given him, and Centerview, access to a mandate that several bankers with knowledge of the situation say is one of the most lucrative jobs in the mining industry.

This story is based on conversations with current and former employees of Anglo American, and other advisers and bankers who asked not to be identified in order to discuss sensitive information.

Centerview, Hartop and Anglo American declined to comment.

Hartop’s association with Anglo American started when he joined SG Warburg — which subsequently became part of UBS Group AG — as an M&A banker in 1995, following an internship at the firm. An Oxford theology graduate, he quickly moved up the ranks as a young banker who showed enthusiasm and a level of maturity beyond his age, according to one person who worked with him during that period.

Anglo American was one of UBS’s key clients at the time, and Hartop was brought into work on the firm’s sprawling global business, which spanned multiple geographies and had copper, gold, platinum and nickel assets, among others. In 1998, he lived in Johannesburg for six months as he worked to get a deal to consolidate eight gold mining companies into AngloGold over the line.

In 2009, Hartop helped ensure that a £41 billion ($66.7 billion) merger proposal from Xstrata Plc was left – according to the company — “dead and buried.”

He advised Anglo on the spinoff of packaging business Mondi Plc in 2007, the purchase of a controlling stake in De Beers Plc in 2012, and the sale of a minority stake in Anglo American Sur SA to a consortium led by Mitsui & Co Ltd. in the same year.

One mining banker at a rival firm said the ties between Hartop and Anglo were so strong that if he saw Anglo run a sell-side process without Hartop’s involvement, he thought the company wasn’t serious about a sale.

These deals propelled Hartop’s near two-decade career at UBS. He went on to become the co-head of European investment banking at the Swiss lender and was named the head of its coverage and advisory business for Europe, Middle East and Africa before leaving to join Centerview. The boutique advisory firm was cofounded by a former UBS colleague, Blair Effron, in 2006.

UBS’s advisory work with Anglo American dropped off after Hartop’s departure, according to data compiled by Bloomberg. In 2024, The bank worked as an adviser to BHP in its approach to Anglo, along with Barclays Plc.

When that bid was made, one of the first people Anglo called in was Hartop.

Anglo had suffered a series of major setbacks. Prices for some key products had plunged and operational difficulties had forced it to cut production targets, driving down its valuation and leaving the company vulnerable to potential bidders. BHP planned to break it up.

Along with counterparts at Goldman Sachs Group Inc. and Morgan Stanley, Hartop helped devise a turnaround at Anglo, which included exiting coal, diamonds and platinum and slowing down spending on a massive UK fertilizer mine. BHP eventually walked away last May after a five-week battle.

Since then, Hartop has been heavily involved in the simplification of Anglo, working on the demerger of its platinum business and an attempt to sell its steelmaking coal business to Peabody Energy, which was scrapped in August.

Discussions between Anglo and Teck started around a year ago, according to people familiar with the matter, and gained momentum a few months ago. On Anglo’s side of the table, Hartop was ever-present, the people said.

Outside of his mining work, Hartop has worked on some of the world’s largest M&A deals globally since joining Centerview — including Anheuser-Busch InBev’s purchase of SAB Miller for about $104 billion in 2016 and AstraZeneca Plc’s acquisition of Alexion Pharmaceuticals Inc. for $39 billion. Among his key clients is DSM-Firmenich.

Centerview ranks eighth among advisers on M&A deals announced this year with an 8% market share, ahead of rival boutiques, including Lazard Ltd. and Rothschild & Co., according to data compiled by Bloomberg. They have had a role on $226 billion of transactions, the data show. Centerview were the main adviser on the recent breakup of Kraft Heinz, and Sycamore Partners’ acquisition of Walgreen Boots Alliance in March.

People who have worked with Hartop describe him as unassuming, easy to deal with and straight to the point. He’s developed a strong rapport with the current Anglo CEO Duncan Wanblad, just as he did with previous leaders of the firm.

New CEOs often bring with them existing relationships with key advisers, but Hartop appears to have proved himself too valuable to Anglo. He’s been a constant even as five CEOs – Julien Ogilvie Thomson, Tony Trahar, Cynthia Carroll, Mark Cutifani and now Wanblad – have gone through the top office since he started working with Anglo.

The agreement with Teck doesn’t mean that Hartop’s job is done. There is still a chance that another bidder could attempt to derail the deal by coming in with an offer for Teck. And BHP, or another large miner, could still come back to make a bid for Anglo, meaning once again it will need someone to head up its defense.

(By Dinesh Nair and Thomas Biesheuvel)

Anglo-Teck Vancouver headquarters is a ‘perpetual’ commitment

Downtown Vancouver, British Columbia. Stock image.

Anglo American Plc and Teck Resources Ltd.’s plan to headquarter their merged company in Canada is “a perpetual commitment,” according to Teck chief executive officer Jonathan Price.

“The commitment that we are making to Canada and the presence of the global headquarters of Anglo Tech in Canada is an enduring commitment,” Price told BNN Bloomberg Television on Wednesday.

An agreement by UK-based Anglo to acquire Canada’s Teck in one of the biggest mining deals in over a decade will need regulatory approval in countries including Canada. Last year, Canada said it would only approve foreign takeovers of large mining companies involved in critical minerals production “in the most exceptional of circumstances.”

Establishing the global headquarters in Vancouver, with the presence of most senior executives, “is a great thing for the country,” Price said.

Asked if a string of setbacks at Teck’s copper mine in Chile was a driver for the transaction, Price said “we’re fully confident that we’ll overcome those challenges.”

“The reason for doing this transaction now is that these opportunities don’t come along very often,” he said. “When you see them, you have to seize them.”

If approved by regulators, the acquisition is expected to close in 12 to 18 months.

The two companies are speaking to investors all over the world, explaining the “incredible upside” and gathering feedback, Price said. While those conversations are very preliminary, “there is real recognition here for the industrial logic of this and the quality of the business we are creating.”

(By James Attwood)

Anglo American’s £36 Billion Merger With Teck Marks Blow to UK Business

Anglo American and Teck will merge in a $50bn deal, forming Anglo Teck with headquarters in Vancouver but retaining a London listing.

The merger will concentrate around 70% of the company’s portfolio in copper, alongside iron ore and zinc, while issuing a $4.5bn dividend to Anglo shareholders.

The move drew sharp criticism from UK opposition figures as a blow to London’s global business standing, though executives touted growth in critical minerals.

Anglo American will merge with Canada’s Teck Resources in a $50bn (£36bn) deal, shifting its headquarters to Canada and reducing its London presence in a move criticised by shadow business secretary Andrew Griffith. The Tory MP said it represents a blow to UK business and confidence in London.

The new entity, to be called Anglo Teck, is expected to have roughly 70 per cent exposure to copper, as well as premium iron ore and zinc. Under the terms of the deal, Anglo will own 62.4 per cent of the combined group, with Teck shareholders owning the rest.

Anglo American’s share price rocketed up 7.75 per cent in early morning trading to £24.55, in response to the news.

HQ relocates to Canada

The company will be headquartered in Vancouver, but will retain its primary London listing with secondary listings in Johannesburg, Toronto and New York.

However, as a result, Anglo American’s London office, which employs up to 700 people, will be significantly downsized.

The merged company will be led by Anglo American chief executive Duncan Wanblad, while Teck chief executive Johnathan Price will move to the role of deputy CEO. However, the CEO, deputy CEO, CFO, and a “significant majority” of the executive management team will also be based in and reside in Canada.

Andrew Griffith told City AM, “If we want the UK to be the best place in the world to do business, Labour must wake up fast.”

He said: This is a clear signal that companies and investors are losing confidence in the UK and voting with their feet.”

“Taxing and regulating businesses into submission will not bring growth; it drives them away. What businesses need instead is a government that champions wealth creation and investment, not one that undermines our competitiveness.”

The fact that a historic British mining giant is moving its headquarters to Canada is yet another signal of decline under Labour,” the shadow business secretary added.

The deal, revealed to its shareholders on Tuesday, follows both companies rejecting takeover approaches from larger rivals, including BHP’s failed £39bn pursuit of Anglo in 2024.

Wanblad said: “Together, we are propelling Anglo Teck to the forefront of our industry in terms of value accretive growth in responsibly produced critical minerals.”

Price added: “This transaction will create significant economic opportunity in Canada, while positioning Anglo Teck to deliver sustainable, long-term value for shareholders.”

Shareholder decisions and dividends

The companies said the shareholder vote for the deal would take place in the coming months, and if approved, antitrust approval could take an additional 12 to 18 months.

Anglo will issue 1.33 shares to existing Teck investors for each share they hold in the company.

The London company is also set to issue a special $4.5bn dividend to its own shareholders ahead of the merger.

The merger is expected to generate annual cost savings and efficiency gains of $800m by the fourth year after completion.

Commenting on the deal, AJ Bell investment director Russ Mould said: ““It now remains to be seen whether it can complete the restructuring of its own business and then whether Anglo Teck delivers on its operational and financial targets, but at least the lowly valuation means there could be upside in the newly-formed company’s share price if it does so, all other things being equal and providing commodity prices do not nose dive in the meantime.”

Mike Henry, chief executive officer of BHP Group. (Image by the World Economic Forum, Flickr.)

Top global miner BHP’s focus on expanding its own copper assets while it undergoes leadership change means it is unlikely to gatecrash the planned $53 billion tie-up of Anglo American and Teck Resources, investors and bankers said on Wednesday.

London-listed Anglo American and Canada’s Teck Resources announced a merger on Tuesday, marking the sector’s second-biggest tie-up ever, to forge a new global copper-focused heavyweight.

The deal came just over a year after BHP scrapped a $49 billion bid for Anglo that in one mega acquisition would have beefed up the Australian miner’s holding in the metal seen as essential to the energy transition.

After being rebuffed by Anglo three times, BHP opted instead to double down on a series of smaller projects where it sees better value, a strategy that investors said has been consistent and suggests it is unlikely to make a move on Anglo or Teck.

“Given BHP’s message, ‘We have moved on,’ any move by BHP for either of the companies would come as a surprise,” said Andy Forster, a portfolio manager at Argo Investments in Sydney, which holds BHP shares.

In the past year, BHP instead spent $2 billion for a stake with Canada’s Lundin in two Argentinian copper projects, including the Josemaria mine whose life was last month extended by six years. It has also pushed hard to eke out production gains at top copper mine Escondida in Chile.

BHP declined to comment on whether it might spoil the Anglo-Teck deal but pointed Reuters to recent comments by its chief executive saying that M&A was just one lever of many for growth.

“Frankly in current markets, it’s hard to see the right combination of the commodities that we like, the asset quality that we like, at a price where we can still unlock attractive value for BHP shareholders,” CEO Mike Henry said on a results call in August.

Despite its recent failure to offload its Australian coal assets, Anglo has worked hard to improve its share price from a year ago, one M&A banker said.

“Both miners are in play now. Anglo’s share price is up, they could probably put in a good defence like they did last time,” he said. Shares in Anglo have jumped 20% since before BHP’s bid in late April while BHP shares have dropped 8%.

The deal was smart in that several factors were favourable to Canada in a way that would be difficult to replicate for other majors who might want to buy Teck, such as relocating the new company’s headquarters to Canada, two people said.

Among the conditions for approving BHP’s merger with South Africa’s Billiton in 2001, the Australian government mandated that the holding company be headquartered in Australia.

Succession may be another stumbling block. BHP chair Ross McEwan replaced Ken MacKenzie in March, after the latter’s decade at the wheel, while CEO Henry is more than five years into a typical six-year term, meaning that BHP may be focused for now on replacing him rather than on big ticket M&A.

But bankers aren’t ruling out the possibility of BHP swooping in down the track, especially if the deal doesn’t go to plan.

“You’d have to have a serious think about it – the two most obvious targets in a nil premium deal,” said an M&A banker not directly involved in the deal, which the parties expect to take 12 to 18 months to complete.

“They have got time … A deal doesn’t have to be done tomorrow.”