It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Wednesday, October 01, 2025

Bulgaria aims to become regional leader in small modular reactors, says energy minister

Bulgaria will leverage its favourable geographical location and diverse energy mix to become a leader in SMRs, Minister of Energy Zhecho Stankov said. / Bulgarian energy ministry

Bulgaria intends to position itself as a regional leader in small modular reactors (SMRs), leveraging its favourable geographical location and diverse energy mix, Minister of Energy Zhecho Stankov said at a round table on energy transition and sustainable development in Sofia, the Ministry of Energy reported on September 30.

Stankov said that Bulgaria has strong potential to become one of the first countries in Southeastern Europe to explore and deploy SMRs. He noted that while the technology was considered “exotic” in 2015, it is now central to the country’s long-term energy strategy.

The Ministry of Energy will initiate talks with developers of small nuclear reactors after signing a cooperation agreement with the United States to conduct preliminary studies on their deployment, the ministry statement said.

On September 16, Stankov signed a joint statement with United States Secretary of Energy Chris Wright, under which one of the 12 US Department of Energy laboratories will support Bulgaria in selecting a site for SMR deployment. Stankov highlighted that other European states, including the Czech Republic and Poland, have also declared interest in SMRs. He cited Canada as an example, noting his recent visit to Ontario, where four SMR projects are under construction.

Just north of Bulgaria, in Romania, Nuclearelectrica is already developing an SMR project under a similar civil nuclear cooperation agreement signed with the US.

Bulgaria has scrapped plans to build a second nuclear power plant at Belene, but is expanding the existing Kozloduy Nuclear Power Plant.

The Bulgarian minister stressed that continuous investment in new energy capacities is crucial for Bulgaria’s energy security. He identified the construction of Units 7 and 8 at the Kozloduy Nuclear Power Plant as the most important project for the national economy and a top government priority. According to Stankov, banks from the United States and South Korea have expressed willingness to finance the development, and a financial adviser has already been appointed.

Orano says 1,500tonnes of uranium stockpiled at seized Niger site

French nuclear group Orano has said 1,500 metric tons of uranium are stockpiled at its expropriated SOMAIR mine in northern Niger, and that it will seek compensation and pursue criminal charges if the material is seized or sold without authorization.

A source at the mine said Niger had not yet sold any uranium although “potential buyers include Iranians, Russians and Turkey”.

Orano launched arbitration at the World Bank’s International Center for the Settlement of International Disputes in January after Niger’s military government blocked operations at SOMAIR before moving to nationalize it.

International court bans Niger uranium transfers

Niger, the world’s seventh-largest producer of the nuclear fuel and cancer treatment material, accounted for 15% of Orano’s uranium supplies when its mines were in full operation.

Niger’s expropriation of Orano’s 63.4% stake mirrors a broader regional shift, with military-led governments in Mali, Burkina Faso and Guinea asserting more control over resources.

A World Bank tribunal on September 23 ordered Niger to halt the sale or transfer of uranium that Orano said had been mined before the military government suspended operations.

The company has no information about subsequent production at the mine, Orano said in an emailed response to questions from Reuters.

“To the best of our knowledge, the uranium is still stored at the SOMAIR site,” it added

With the uranium spot price at $82 a lb, Orano’s stockpile at the Somair mine is worth about $270 million. Prices have gained around 30% since mid-March but are still below a peak of $106 touched in February 2024.

Orano declined to comment on prospective buyers approaching Niger, citing its focus on the arbitration.

Niger’s government did not immediately respond to a request for comment.

Niger takes control of uranium production

The source in SOMAIR told Reuters about 1,570 tons of uranium is stored in the mine.

Production is now supervised by the state-owned SOPAMIN (Société du patrimoine des mines du Niger), they added.

“To my knowledge, there have been no official sales,” the source said, asking not to be named due to sensitivity of the issue. “There is a lot of demand for purchases.”

The Somair mine has produced over 70,000 tons of uranium near the city of Arlit since the 1970s.

The military government, which seized power in a coup in July 2023, has tightened control over Niger’s gold, oil and coal.

At the UN General Assembly, Prime Minister Ali Lamine Zeine accused foreign firms of decades of exploitation, saying uranium had brought “misery, pollution, rebellion, corruption and desolation” to Nigeriens while enriching France.

(By Maxwell Akalaare Adombila; Editing by Veronica Brown and Kevin Liffey)

Tribunal decision supports Orano in Somaïr dispute

An international tribunal has ruled in favour of Orano in its dispute over the sale of uranium produced from the Somaïr mine.

Samples of calcined and natural uranium oxides (Image: Orano/Eric Larrayadieu)

Somaïr, which operates the Arlit uranium mine, is 63.4% owned by Orano, with the Niger state-owned mining assets company SOPAMIN holding 36.6%, but has been under the operational control of the Nigerien authorities since December.

The French company has filed several international arbitration proceedings against Niger since events following a 2023 coup d'état in Niger, including the inability to resume sales of uranium production from Somaïr due to a lack of logistics solutions approved by the Niger authorities. Earlier this year, Niger's Council of Ministers announced plans to appropriate and nationalise the joint venture.

Orano said the International Centre for Settlement of Investment Disputes (ICSID) rendered a new decision relating to one of those filings, case number ARB/25/8, on 23 September.

"In its decision, the arbitral tribunal ordered the State of Niger not to sell, transfer, or even facilitate the transfer to third parties of the uranium produced by SOMAÏR that was withheld in violation of Orano’s rights, as requested by Orano," the company said.

"Orano continues to deplore the prolonged detention of its representative in Niger, Mr Ibrahim Courmo, who has been illegally held since May 2025, and welcomes that ICSID has also requested the State of Niger to proceed with his release in accordance with the decision of the Niamey Court of Appeal in July 2025," the company added, saying the decision "represents a new significant step in the proceedings and confirms the relevance of the arguments presented by the group".

"Orano will continue to defend its interests with determination and reserves the right to initiate any additional actions, including criminal ones, against third parties if there is any preemption of the matter in violation of its lifting rights. Orano also remains committed to ensuring the protection of its employees, partners, and clients."

The ICSID was established in 1966 by the multilateral Convention on the Settlement of Investment Disputes between States and Nationals of Other States (the ICSID Convention), and describes itself as an independent, depoliticised and effective dispute-settlement institution available to investors and States. It says it helps to promote international investment by providing confidence in the dispute resolution process. It provides for settlement of disputes by conciliation, mediation, arbitration or fact-finding.

Viewpoint: Key takeaways from World Nuclear Symposium 50

The 2025 World Nuclear Symposium marked a historic milestone: the 50th edition of the flagship gathering of the global nuclear industry. Held in London, the event brought together leaders from government, industry, finance, and technology under the theme Energizing the Future Now. World Nuclear Association Director General Sama Bilbao y León reflects on the main messages from the discussions.

(Image: World Nuclear Association)

Over three days, 1,122 registered delegates from 59 countries explored the evolving role of nuclear energy in a rapidly changing world, with a clear message: Global momentum is with nuclear, so the time is now for our sector to lead with a bold mindset and deliver what the world demands - a secure, sustainable energy future.

This year marked a significant high point. The World Nuclear Performance Report showed that 2024 was a record year, with nuclear reactors supplying more electricity than ever before - 2667 TWh - and avoiding 2.1 billion tonnes of carbon dioxide emissions (of coal equivalent generation).

While we were celebrating our 50th Symposium, many delegates were joining us for the first time. That in itself demonstrates how the industry has shifted its messaging and engagement, turning inside out, from speaking amongst ourselves to engaging influential external stakeholders. This Symposium wasn’t looking back, it was looking forward and outwards.

Listen to highlights from Symposium on the World Nuclear News podcast:

Finance and energy users signal demand for nuclear

Perhaps most striking was the significant engagement of the financial community. Banks, investors, and multilateral institutions were here in greater numbers than ever before (including the likes of the World Bank, UBS, Deutsche Bank, JP Morgan, and HSBC). At the Finance Summit they spoke of the unprecedented appetite for nuclear from investors and the opportunity ahead, but also of the need for standardisation and de-risked financial models. For the first time in decades, nuclear is being discussed in boardrooms and investment committees as a serious growth sector. That shift cannot be overstated.

On the demand side, the Energy Users Summit highlighted how diverse industries - from heavy industry to high-tech - are actively looking to nuclear. A landmark moment came when Microsoft became the first global technology company to join World Nuclear Association. This signals a powerful alignment between the digital economy and nuclear energy, and a partnership that can accelerate deployment and deliver on climate goals.

Fuel cycle: Investment decisions must be made now

At the same time, we cannot rapidly expand nuclear capacity without also investing in the resilience of the fuel cycle, supply chains, and workforce.

The launch of the World Nuclear Fuel Report 2025–2040, its 22nd edition, reinforced the urgency of action in the front end. In its reference scenario, nuclear capacity is projected to double to 746 GWe by 2040, with uranium requirements rising to 150,000 tU.

Primary uranium now meets 90% of requirements, and while resources in the ground are sufficient, new mines must be developed to bring this material into supply. Conversion and enrichment services face regional constraints shaped by geopolitics, and fuel fabrication capacity must expand - not only to meet growing demand, but also to support new reactor types. The choices made in the next few years will determine whether supply keeps pace with ambition.

Partnership and delivery

A recurring theme across the Symposium was the need for deeper, broader partnerships to turn ambition into reality. Delivery at scale cannot rest on isolated projects or single actors; it will depend on governments, industry, financiers, and energy users working together.

Delegates spoke of moving from projects to programmes, from prototypes to fleets. Whether through regional cooperation, supply chain integration, or joint financing models, partnership is the essential ingredient. The Symposium showed clearly that nuclear’s future will be written not by individual players, but by those willing to collaborate and deliver together.

Final thoughts

World Nuclear Symposium 50 was not just a celebration of history - it was a turning point. With mounting pressure to decarbonise, secure energy supplies, and meet growing electricity demand, nuclear energy is stepping into a new era of prominence.

The Summits and Symposium did not simply ask questions; they provided consistent, credible answers. They pointed beyond what nuclear does, to whom it serves, why it matters, and - most urgently - how and when it must be delivered.

The last 50 years proved the essential value of nuclear. The next 25 will decide its impact. The conversations in London made one thing clear: the world is asking for nuclear energy, and now is the time for the nuclear industry to answer.

Transatlantic partnership for SMR deployment

US advanced nuclear technology company Oklo Inc and Swedish lead-cooled small modular reactor technology developer Blykalla have announced a strategic partnership focused on technology collaboration, supply-chain coordination, and regulatory knowledge-sharing.

(Image: Blykalla)

Under a Joint Technology Development Agreement, Oklo and Blykalla will share insights on materials, components, non-nuclear supply chain sourcing, fuel fabrication, and licensing best practices across the USA and Sweden. Through increased cooperation and coordination, both developers aim to reduce costs and schedule risks.

Together the companies will examine shared suppliers for reactor-agnostic equipment to improve availability, schedules, and cost. Under the agreement, Oklo may also supply select components for Blykalla's direct use to strengthen a vertically integrated, potentially cross-border, supply chain. Oklo may also provide fuel fabrication services to Blykalla. In parallel, Oklo and Blykalla will pursue targeted R&D and regulatory analysis to boost reliability and lower lifecycle costs without requiring design changes.

The agreement includes Oklo co-leading Blykalla's next investment round through a commitment of about USD5 million.

The partners said the agreement demonstrates how advanced reactor developers can align on fuel, supply chains, and regulation to accelerate commercialisation globally. "The partnership reflects a shared commitment to making advanced reactors a cornerstone of the clean energy transition, delivering reliable power for industry, data centres, and future electrification needs," they said.

Blykalla is a spin-off from the KTH Royal Institute of Technology in Stockholm, where lead-cooled reactor systems have been under development since 1996. The company - founded in 2013 as a joint stock company - is developing the 55 MWe SEALER (Swedish Advanced Lead Reactor) lead-cooled SMR.

Oklo is developing its sodium-cooled fast-reactor Aurora powerhouses of up to 75 MWe, with a focus on deployment at US sites to serve industrial, defence, and data centre customers.

"This partnership strengthens the growing advanced reactor ecosystem in the face of unprecedented global demand for power," said Oklo co-founder and CEO Jacob DeWitte. "By teaming up on suppliers, materials data, and licensing insights, we can shorten critical paths to deployment and stay focused on delivering reliable, clean power to customers, while recognising that we have more to gain from cooperating than from competing."

Blykalla CEO Jacob Stedman added: "Oklo and Blykalla share a practical, industrial approach to bringing advanced fission to market. Coordinated component sourcing and targeted joint R&D can unlock efficiencies for both companies and help our suppliers plan for scale, regardless of which side of the Atlantic they are on."

Construction of new Dutch research reactor formally begins

Anita van den Ende, Secretary General of the Ministry of Health, Welfare and Sport, has officially launched the construction of the Pallas research reactor in Petten, the Netherlands.

(Image: NRG-Pallas)

The Pallas research reactor is to be built to replace the existing High Flux Reactor (HFR), which began operating in September 1960 and supplies about 60% of Europe's and 30% of the world's medical radioactive sources. Pallas will be of the "tank-in-pool" type, with a thermal power of around 55 MW, and able to deploy its neutron flux more efficiently and effectively than the HFR.

"Every day, many thousands of patients depend on medical isotopes produced in Petten for their diagnosis or treatment," said NRG-Pallas CEO Maurits Wolleswinkel. "By constructing the Pallas reactor to replace the High Flux Reactor, we are ensuring future security of supply. This will make the Netherlands and Europe less dependent on other countries. Developments in the field of therapeutic isotopes are very promising. By developing and producing new isotopes, we aim to contribute to better and more efficient patient care."

Peter Dijk, programme director of the Pallas Programme added: "The Pallas reactor is a major infrastructure project, and that requires careful preparation. We've gone through all the steps with the Ministry of Health, Welfare and Sport to become a state-owned company and secure the financing. Together with our construction partner FCC and design partner ICHOS, we've reached the point where construction of the reactor building can begin. We're proud of what we've achieved together and what we still have to do: actually erecting a reactor in the cofferdam."

Background

The Dutch government allocated funding for the coming years for the construction of the Pallas reactor, even before making a final decision on its construction. Last year the European Commission also approved, under EU state aid rules, the Dutch government's plan to invest EUR2 billion (USD2.2 billion) in the reactor, which received a construction licence in February 2023.

Preparatory work on the foundation began in May 2023 - then ministers instructed NRG-Pallas not to take any irreversible steps, but to continue with the preparations for the project to avoid unnecessary delays pending the construction getting the official go-ahead.

In May this year, NRG-Pallas announced that the building of the construction pit - a hole of about 50 metres by 50 metres and 17.5 metres deep - and the foundation for the Pallas reactor had been completed.

In July, the Netherlands' caretaker Minister of Health, Welfare and Sport Daniëlle Jansen informed the House of Representatives that the project to construct the Pallas research reactor was ready to enter the next phase of construction.

In its update on progress, NRG-Pallas said construction has already begun on the pit for the secondary cooling system building. It added that preparations are also progressing for the installation of the cooling water pipeline, which will extract water from the Noordhollandsch Kanaal and discharge it into the North Sea.

Point Beach units cleared for 80 years of operation

The US Nuclear Regulatory Commission has renewed for a second time the operating licences of Point Beach units 1 and 2, clearing the way for an 80-year operating life for the two pressurised water reactors.

Point Beach Nuclear Plant site vice president Thad Edmonds, NextEra Energy Resources nuclear fleet licensing manager Maribel Valdez, Point Beach Nuclear Plant engineering manager Scott Kahl (standing), and Greg Bowman, director of the NRC's Office of Nuclear Reactor Regulation. Photo credit: Britt Griffin for NextEra Energy Resources, mark the licence renewal (Image: Britt Griffin for NextEra Energy Resources)

Point Beach unit 1 entered commercial operation in 1970, with unit 2 following in 1973. The units, in Two Rivers, Wisconsin, were initially licensed by the Nuclear Regulatory Commission (NRC) for 40 years of operation, with both units receiving renewed operating licences in 2005 for a further 20 years, licensing them until May 2030 for unit 1 and August 2033 for unit 2.

NextEra Energy Point Beach, LLC - the owner and licensed operator of the two units - submitted its application for a subsequent licence renewal for the plant in November 2020, requesting authorisation to operate from 60 to 80 years.

The NRC has issued the renewed licences - which will now expire in October 2050 for unit 1 and March 2053 for unit 2 - following a review which saw it issue a final supplemental environmental impact statement, and a supplement to its May 2022 safety evaluation, in August 2025.

Point Beach (Image: NextEra Energy Resources/X)

"This approval ensures that Wisconsin's only nuclear plant will continue to provide safe, reliable, low-cost energy for generations to come," NextEra Energy Resources President and CEO Brian Bolster said. "We are proud that Point Beach will remain an integral part of Wisconsin's energy future and a vital contributor to the state and local economies."

Initial licences issued by the NRC for US commercial power reactors cover operation for up to 40 years; these can be renewed for an additional 20 years for an operating lifetime of 60 years. Subsequent licence renewals cover a further 20 years of operation beyond 60 years and focus on the management of plant ageing during the 60-80 year operating period.

The NRC has so far issued some 13 units with subsequent licence renewals, including two units at Turkey Point which are operated by NextEra Energy's sister company Florida Power & Light. A further ten units - including Florida Power & Light's two St Lucie units - are currently undergoing the process.

Atucha I life extension work '44% completed'

During its first year of shutdown for work to extend its life by 20 years, the Atucha I nuclear power unit in Argentina has seen 44% of the project completed, Nucleoeléctrica Argentina has said.

The Atucha nuclear power plant site (Nucleoeléctrica Argentina)

"Significant progress," the company said, had been made in "modernising essential systems and optimising key processes. This work will ensure that, once the refurbishment is complete, Atucha I continues to operate safely and efficiently, strengthening the contribution of nuclear energy as a base energy source for the country's development".

Atucha I, a 362 MWe pressurised heavy water reactor, entered commercial operation in 1974 and had a design life in its operating licence of 32 equivalent years of full power. The life extension project is seen as one of Argentina’s most significant infrastructure projects.

The first extension to its operating licence began in 2018 when the original 32-year mark was reached.

The duration of the amended operating licence was for the equivalent of 5 years operation at full power, or 10 years from 2014, which ended on 29 September 2024, which is when the current planned 30-month shutdown began.

Nucleoeléctrica Argentina put the refurbishment programme's cost at USD463 million in 2023 when it launched a fundraising round of bond sales to cover the LTO (long term operation) cost and construction of a dry storage facility for used fuel.

Background

Atucha I was designed and built by KWU, which was a joint venture of Germany's Siemens and AEG. Over time, KWU was fully owned by Siemens, before being sold to the reactor business of France's Areva which is now owned by EDF and trading as Framatome. However, Argentina now has an experienced supply chain of its own for pressurised heavy water reactors, having completed and brought into operation the similar Atucha II reactor in 2016.

It has become common for pressurised heavy water reactors like Atucha I to undergo refurbishment, which typically involves replacing pressure tubes and fuel channels, to enable another two decades of operation. Nucleoeléctrica Argentina said ahead of the shutdown that 2,000 jobs would be created as it modernised "all the processes and systems of the plant".

U.S. shale oil wells generate 27–45 million barrels of toxic wastewater every day, with shale gas adding billions more gallons annually.

Traditional underground disposal is polluting groundwater, reactivating old wells, and triggering earthquakes in Texas and Oklahoma.

Oil companies like ConocoPhillips and Chevron now warn that wastewater could flood oil reserves and choke production unless alternatives are developed.

There's an old saying that I won't spell out completely, but which most readers will certainly have heard at least once in their lives, to wit: "Don't sh-- where you eat." It is an all-purpose warning about not pursuing incompatible activities in the same place, particularly activities that produce either physical waste or emotional complications.

In this case, the waste part is wastewater emitted by oil wells drilled into shale deposits, which must undergo extensive hydraulic fracturing (often called fracking) before the oil can be freed. What most people do not know is that for every barrel of shale oil extracted, three to five barrels of water laden with fracking chemicals and salt, toxic minerals, and radioactivity (from the deep rock) also come up, most of it water originally injected under high pressure to fracture the shale and release the oil.

Groundwater used for human and animal consumption is being polluted by these shallower underground injections. So much pressure has built up underground that some old abandoned wells have sprung to life, spewing wastewater that comes to the surface through old well casings. The industry pretends to care about this, but generally fights landowners who complain and sue. But what the industry is really increasingly concerned about is that the wastewater is starting to break through to producing wells and compromise production. One major producer, ConocoPhillips, has warned that underground wastewater injections risk flooding out oil reserves. "Flooding out" means that water infiltrates into oil reservoirs from places where wastewater has been injected, complicating production or even making profitable production impossible as water comes to dominate extraction volumes.

The call for developing alternatives to underground disposal now has an unlikely champion, oil major Chevron, a company at the center of the controversy over fracking wastewater disposal. The industry will need a solution soon, as water use is expected to balloon as the industry moves on to less oil-rich reservoirs that will require more fluid to successfully fracture wells. This is projected to lead by 2035 to a 39 percent increase in wastewater from the Permian Basin, the largest producer of shale oil in the United States.

TotalEnergies completed the sale of a 50% stake in a 270 MW portfolio of wind and solar projects in France to Eiffel Investment Group, valuing the assets at €265 million.

The transaction fits TotalEnergies’ Integrated Power business model, under which the company retains a 50% stake and remains operator while monetizing part of its renewable assets once they reach commercial operation. This strategy enables the French major to derisk projects, recycle capital, and target 12% profitability in its power segment. TotalEnergies will continue to offtake and market most of the electricity generated by the projects.

Eiffel Investment Group, an asset manager with €7 billion under management, brings deep expertise in energy transition financing, backed by the Impala group of entrepreneur Jacques Veyrat. The firm has expanded its reach across Europe, the U.S., and the Middle East, with a strong focus on sustainable infrastructure investment.

For TotalEnergies, the deal supports its broader ambition to scale renewable capacity while maintaining capital discipline. The company had more than 30 GW of installed renewable capacity at mid-2025 and is targeting 35 GW by year-end. By 2030, it aims to deliver more than 100 TWh of net electricity production, positioning itself as a leading integrated power provider.

The transaction highlights a growing trend among oil majors to share ownership of renewable assets with financial investors, enabling balance sheet flexibility while meeting energy transition goals. Rivals such as bp, Shell, and Eni have pursued similar divestment models in Europe and beyond.

By Charles Kennedy for Oilprice.com

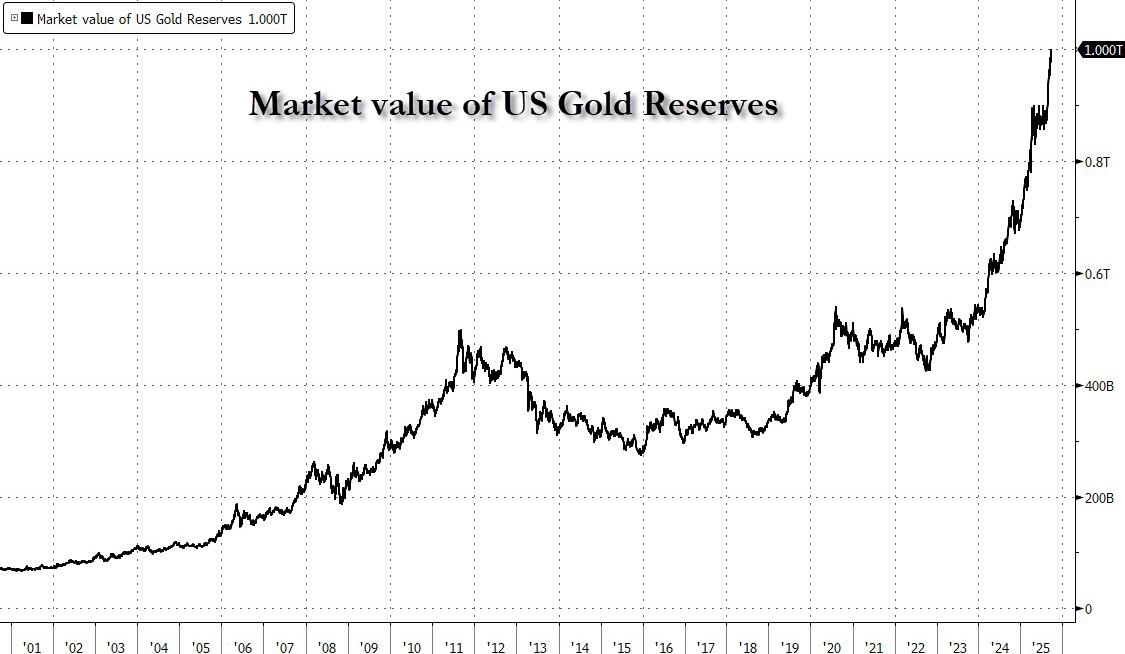

U.S. Treasury's Gold Stash Surpasses $1 Trillion

NOBODY HAS CHECKED FORT KNOX TO SEE IF IT'S STILL THERE; 'I TRUST IT'S THERE' SAYS CNBC COMMENTATOR

The U.S. Treasury's gold hoard has exceeded $1 trillion in value, significantly more than its stated balance sheet value, leading to speculation about a potential revaluation.

A revaluation of the gold reserves to today's market prices could release approximately $990 billion into the Treasury's funds, reducing the need for new bond issuance.

While considered unorthodox and potentially impacting fiscal and monetary independence, a gold re-marking would increase the size of both Treasury and Fed balance sheets and could lead to a surge in gold prices.

On the back of a 45% surge in the price of gold this year, the US Treasury's hoard of the barbarous relic has surpassed $1 trillion in value for the first time in history.

That is more than 90 times what's stated on the government's balance sheet and is reigniting speculation that Treasury Secretary Bessent could revalue (mark to market) the massive pile of precious metal.

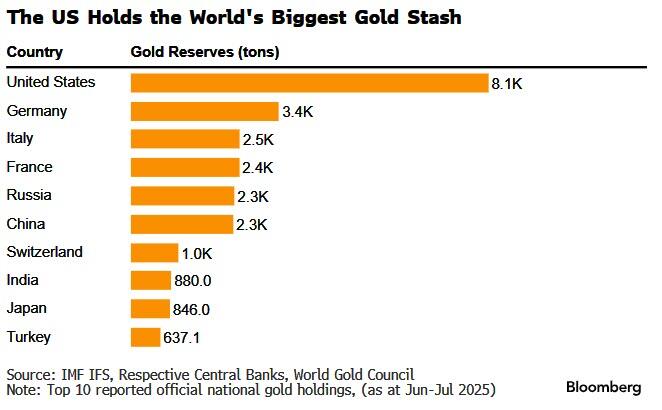

Unlike most countries, the US’s gold is held by the government directly, rather than the central bank.

The Fed instead holds gold certificates corresponding to the value of the Treasury’s holdings, and credits the government with dollars in return.

That means, as we detailed previously, that an update of the reserves' value in line with today's prices would unleash roughly $990 billion into the Treasury’s coffers, dramatically reducing the need to issue quite so many Treasury bonds this year.

While Treasury Secretary Bessent initially dismissed the suggestion, a trillion dollars here and a trillion dollars there adds up and it would be by no means unprecedented. As Bloomberg reports, Germany, Italy and South Africa all have taken the decision to revalue their reserves in recent decades, as an August note from an economist at the Federal Reserve discussed.

US gold re-marking would have implications for both the Treasury & Fed balance sheets.

US Treasury: assets would rise by the value of the gold re-marking & liabilities would rise by the size of gold certificates issued to the Fed.

Federal Reserve: assets would rise by value of gold certificates & liabilities would rise by a crediting of cash in the Treasury cash balance (Exhibit 4). And here is the punchline: the Fed balance sheet impact would look like QE though no open market purchases would be required & Fed liability growth would initially be in TGA.

In other words, the best of all words: a QE-like operation, one which see the Fed quietly funnel almost $700 billion in cash to the Treasury... but without actually doing a thing!

On net, a gold re-marking would increase the size of both Treasury & Fed balance sheets + allow for TGA to be used for Treasury priorities (i.e. SWF, pay down debt, fund deficit, etc). Meanwhile, the Fed and Treasury magically conjure some $990 billion out of thing air to be spent on whatever, all because the Treasury agrees that the fair value of gold is... the fair value of gold.

Needless to say, a gold re-marking would be seen by the market as unorthodox, if not completely unexpected. US gold has not been re-marked for decades likely to guard against (1) volatility of Treasury & Fed balance sheets (2) concerns over fiscal & monetary authority independence.

According to none other than BofA's heaviest of Fed plumbing hitters, former NY Fed staffer Mark Cabana, a gold re-marking could cause TGA to be paid down in ways that stoke macro activity, risk inflation, & add excess cash into the banking system (higher TGA would eventually move to higher Fed reserves or ON RRP balances). In essence, gold re-marking would ease both fiscal & monetary policy (all else equal).

The BofA strategist's conclusion is that gold re-marking is possible (and certainly likely after Bessent's earlier comments), but has legal questions, "may not be well received by the market since it would amount to an easing of fiscal & monetary policies + erosion of fiscal / monetary independence" (yup, QE under any other name...). And, not unironically, the revaluation of gold will also send the price of gold (not to mention bitcoin and anything else that may also be subsequently remonetized) soaring.

As such, BofA still places low odds of US asset monetization until Bessent provides more credible detail on how he will “monetize the asset side of the US balance sheet." We, however, having realized that Trump moves very fast and breaks everything in his path, are confident that the odds of a gold revaluation are surging, and are a big part of why gold is trading just shy of $4000.

The agency proposed scaling back Clean Air Act Section 111 and Mercury and Air Toxics Standards (MATS), undoing Biden-era 2024 rules and easing emissions limits for coal and gas plants.

While coal’s role is shrinking, the rollback signals minimal regulatory pressure on new natural gas plants.

By framing the rules in partisan terms, the EPA increases the chance of future reversals, leaving utilities exposed to insurance, litigation, and climate-related financial risks despite temporary relief.

This past June, the US EPA revised its views on power plant emissions, particularly of coal-fired plants. In short, EPA is now in favor of emissions. OK, we’re kidding, but not by much. The agency proposed to rollback: 1) the Clean Air and Water Act, section 111, and 2) MATS, the Mercury and Air Toxics Standards for power plants, back levels established in 2012. (Both rules, the Biden administration strengthened in 2024, to the dismay of coal-fired power plant owners.)

The proposed revisions to the CAA are based on two statements of regulatory purpose. First, since the regulated pollutants are a global problem, the EPA should not be obligated to regulate emissions unless there’s definitive proof that a specific power plant caused the alleged environmental harm. Second, greenhouse gas emissions from fossil-fired fuel plants do not result in harmful emissions under the meaning of the revised CAA statutes. These two regulatory revisions make clear that the government no longer has an interest in regulating greenhouse gas emissions from US power plants.

By contrast, the MATS revisions are specific. They canceled all new power plant pollution remediation requirements issued by the Biden administration in 2024: the particulate matter standard for coal-fired plants, the tighter mercury standard for lignite-fired plants, and they would eliminate the new requirement for particulate matter continuous emissions monitoring systems. The EPA stated that these revisions would alleviate “regulatory uncertainty” in twelve states with coal plants and save $120 million a year starting in 2028. (The total bill for coal fuel is less than $15 billion, so the new rules will lop less than 1% off the fuel bill for coal.)

Although coal accounts for about 15% of the nation’s overall power generating mix, the percentage of coal-fired generation in coal-producing states remains large: West Virginia (91%), Missouri (75%), Wyoming (74%), Kentucky (71%), Utah (62%), and Indiana (57%). And the nation’s coal fleet, however, is aging out. Power plants built in the 1970s and 1980s are approaching retirement (the average age of a retiring coal plant in 2024 was 54 years).

There is nothing unique about politicians providing regulatory relief for a legacy industry in decline like coal. But there is also a clear message here for the owners and builders of natural gas fired power plants—the EPA is not interested in regulating your emissions either. No utility has built a large coal-fired power-generating station in a long time. But there are about 19 gigawatts of new gas fired capacity expected to come on line between now and 2028, according to the EIA, and possible data center growth would only add to this number.

As utility investors, our initial conclusion is that these EPA proposals substantially mitigates the risk of environmental penalties for fossil fired power plants. Given coal’s declining role in the energy landscape, these rule changes may have little economic impact. However, EPA head Zeldin made two comments worth noting. First, he said that “affordable, reliable, electricity is the key to the American dream and a natural byproduct of national energy dominance.“ But in justifying the policy changes, he stated that “the primary purpose of the Biden-Harris administration regulations was to destroy industries that didn’t align with their narrow-minded climate change zealotry.“ And that’s the problem. The Democrats can simply rewrite that statement when they assume power (“The primary purpose of the Trump administration regulations….”). By politicizing this issue in strong partisan terms, this raises the possibility of a political reversal by a future administration, one with greater concerns over environmental issues. If so, do we now face the overhang of stranded asset risk for all new gas-fired power generation? We doubt this is being priced into stock prices at the moment.

The government is in effect telling power plant owners not to worry about particulate emissions and greenhouse gases. This is the same government that denies the efficacy of vaccines and freely attacks established expertise in science and medicine. So where’s the risk for utilities if our government chooses to ignore the adverse effects of greenhouse gas emissions? We’re not sure. It could be the insurance industry refusing to insure plants, like they bailed on nuclear plants ages ago. Or maybe it's pollution/climate harm lawsuits that gain traction in the courts, like the successful lawsuits against tobacco companies. All we can say is that this government's denial of big issues like climate change comes to resemble a game of whack-a-mole. The government has managed to somewhat suppress the business risk for coal and gas-fired power plants, at least in the near term, but we think the financial risks will keep reasserting themselves in new forms, which is neither helpful to planners trying to allocate billions for energy capex nor to the investors who will be asked to put up the money.

By Leonard Hyman and William Tilles for Oilprice.com

_55374.jpg)

_67794.jpg)

_72764.jpg)

_11072.jpg)