It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Wednesday, January 14, 2026

Azerbaijan and U.S. Weigh Cooperation on Peace Corridor and Energy Projects

U.S. and Azerbaijani officials discussed investment opportunities linked to the Trump-brokered Armenia-Azerbaijan transit corridor.

Talks covered rail infrastructure, telecommunications, data centers, and renewable energy cooperation.

The U.S. delegation planned to continue regional consultations with a follow-up visit to Armenia.

Azerbaijan rolled out the red carpet for a delegation led by Carl Kress, the regional director for Eurasia of the US Trade and Development Agency. Local media reports characterized Kress’ talks with a variety of top Azerbaijani government officials as “constructive” but no specific deals were announced.

“The two sides highlighted significant potential for collaboration across multiple sectors,” noted a commentary published by the government-connected website Caliber.az. Discussions focused on the development of the Trump Route for International Peace and Prosperity (TRIPP), the centerpiece of a provisional peace deal between Armenia and Azerbaijan, brokered by the US president last summer.

During a meeting at the Foreign Ministry, Kress discussed ways to connect Azerbaijani government agencies with US private-sector representatives to explore corporate investment in the development of TRIPP infrastructure, as well as participation in renewable energy ventures, according to Azerbaijani media accounts.

In separate discussions at the Ministry of Digital Development and Transport, the two sides explored joint projects to develop railroad infrastructure and telecommunications capacity, as well as the construction of data centers. The USTDA delegation was scheduled to travel to the Armenian capital, Yerevan, on January 13.

Mantoverde is an open-pit mine located in the Atacama region of Chile. Credit: Capstone Copper

Talks for a new collective agreement at Chile’s Mantoverde copper and gold mine remain frozen as the strike continues to affect production, the union said on Monday.

The workers’ union said in a statement the labor authority had notified it that the company will not have emergency personnel from the union to keep facilities operational “due to non-compliance with legal requirements and late submissions.”

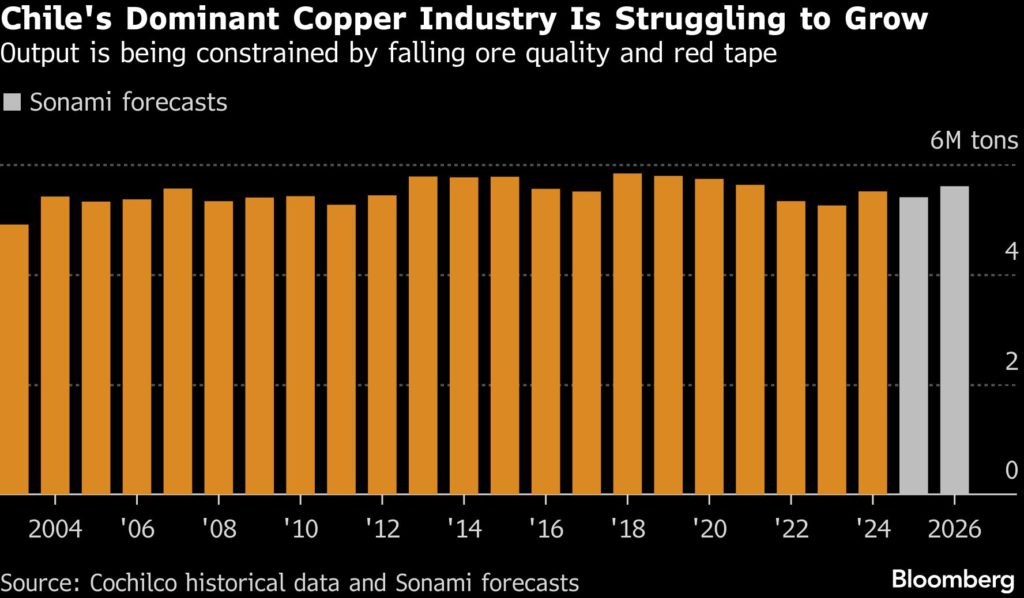

Chile’s copper industry eyes double-digit growth after reforms

Truck at Chuquicamata, world’s biggest open pit copper mine, Calama, Chile. Stock image.

Chile, the world’s top copper producer, could break out of two decades of stagnant output by cutting red tape and easing regulation under the incoming government, according to the country’s mining industry group.

Sonami president Jorge Riesco said Tuesday he agrees with recent comments from President-elect José Antonio Kast’s team that mining output could rise by 10% to 20% over the next year or two. Kast’s projections followed consultations with Sonami, Riesco said.

Removing restraints on investments as part of a pro-growth agenda could unlock billions of dollars in mine expansions that together would have a sizable impact on output, Riesco told reporters in Santiago on Tuesday. Annual production that slipped to 5.4 million metric tons last year is set to reach 5.5 million to 5.7 million this year, according to Sonami. High prices may also flush out more supply, the association said.

Getting Chilean production closer to 6 million tons a year would be welcomed by a tightening global market, where copper prices have surged to a record above $6 a pound. Analysts have warned of a looming supply squeeze as producers struggle to expand output just as demand rises from artificial intelligence and higher defense spending.

Chile’s experience mirrors challenges facing the global mining industry. The development of giant deposits such as Escondida cemented the country’s position as the world’s dominant producer. But output is now broadly in line with levels seen two decades ago as ore grades decline and projects become more complex and expensive.

Still, Sonami forecasts copper prices will average about $4.50 a pound this year — well down from current levels — as some of the disruptions that helped fuel the rally ease. Mining investment in Chile is projected to total $26.8 billion between 2025 and 2029, even as spending this year is expected to fall by about 20%.

(By James Attwood)

Codelco submits $1.3B plan to prolong Radomiro Tomic mine life to 2058

Chile’s state-run miner Codelco, the world’s largest copper producer, on Tuesday submitted a $1.3 billion continuity project to Chile’s environmental authority to request an extension of its leaching operations at its Radomiro Tomic mine until 2058.

The proposal aims to boost the mine’s capacity to an average of 725,000 tonnes per day, up from its current level of 675,000 daily tonnes, requiring pit expansion and new waste dumps and ore stockpile areas.

The plan seeks to extend the operation of the mine’s chlorinated leaching process at an average annual rate of 154,000 tons per day.

Leaching is a method of extracting metals and minerals from rock using liquid chemicals instead of melting or crushing.

The project also seeks to provide operational continuity to its waste treatment and dumping line, which uses chemical solutions to extract copper from ore rather than smelting.

Plans include expanding support facilities and installing a hydraulic barrier system with four wells to control water infiltration in the industrial area.

The project includes truck transport of 20,000 daily tons of ore or waste per year to Codelco’s Chuquicamata facility over the next 10 years.

Codelco’s Radomiro Tomic mine is one of the company’s three most prominent mines in Chile.

(By Fabian Cambero; Editing by Natalia Siniawski)

BHP is stuck on the sidelines of copper M&A frenzy it started

South Australia’s Olympic Dam copper, gold, uranium mine. (Image courtesy of BHP.)

BHP Group’s bold bid to buy rival Anglo American Plc in 2024 was supposed to set it up as the clear winner in a copper boom it had long predicted. Two years later, the copper market is indeed booming. And yet the world’s biggest miner is left sitting on the sidelines of an M&A frenzy it began.

People familiar with BHP’s thinking said the news that Rio Tinto Group and Glencore Plc are closer than ever to a deal that would leapfrog BHP to become the world’s most valuable mining company has caused consternation within the Australian mining giant. However, some of the people played down the likelihood that it would respond with a move for Glencore, and said it’s watching from the sidelines for now.

Instead of cementing its clear lead over Rio and others, the failed attempt to buy Anglo helped create the conditions for two big tie-ups among its major rivals. Anglo itself agreed last year to merge with Canada’s Teck Resources Ltd., and now Rio’s prospective deal for Glencore threatens to create an even more powerful competitor at a time when BHP is also contending with a mounting dispute over iron ore sales to its most important customer, China.

BHP surprised investors with a half-hearted last-minute bid to crash the Anglo-Teck deal late last year, fueling questions about its strategy after chief executive officer Mike Henry earlier said the company had moved on from Anglo.

And a response to the Rio-Glencore talks would be even more complicated: BHP and Glencore are two of the largest miners of metallurgical coal, meaning any merger would certainly run into antitrust issues — although BHP could theoretically make an offer for the whole of Glencore and then decide to sell or spin off the coal assets to get regulatory approval for a deal.

BHP’s CEO Mike Henry is also nearing the end of his tenure, potentially hindering the negotiation of a transformational deal.

The company is monitoring the Rio-Glencore talks and reviewing the situation and options with its advisers, the people said.

“If Rio combines with Glencore, and you’ve already got Anglo and Teck in play, BHP risks being left behind,” said Iain Pyle, senior investment director at Aberdeen Group Plc, which holds shares in Rio and BHP. “There aren’t many other ways to gain copper scale.”

BHP declined to comment.

Henry has long preached a mantra of M&A discipline, gradually warming investors back up to dealmaking after a series of disastrous deals at the top of the last cycle. He walked away from his bid for Anglo in 2024 after demanding that the smaller miner spin off its South African businesses as a condition of any deal.

Today, thanks to a restructuring along the lines that BHP had proposed, a copper boom much like the one it had been predicting, and the deal with Teck, Anglo is worth about $52 billion — more than the offer that BHP walked away from.

“I think they’ve got to look very closely and think about it,” George Cheveley, a portfolio manager at asset manager Ninety One and former analyst at BHP, said of the prospect of a BHP bid for Glencore. However, BHP “may find it difficult emotionally after their failure to close a deal with Anglo American,” he said.

The combination of Glencore and Rio would likely exceed BHP in copper mining scale and could surpass Chile’s Codelco to be the world’s largest copper miner. Anglo Teck would also become one of the world’s largest copper miners, though still somewhat smaller than BHP, according to the two companies’ presentation announcing the deal.

“There are many in the market who feel BHP cannot afford to sit and watch all the other consolidation that is going on,” Mark Kelly, who runs merger arbitrage specialist MKI Global Partners in London, said in a note to clients. “BHP has obviously said repeatedly it doesn’t need to acquire, but there was talk in mining circles all last year about Glencore beautifying itself to attract both BHP and Rio, thus hopefully extracting the best price in any sale.”

Glencore has a market capitalization of about $73 billion, compared with $158 billion for BHP, while Rio is valued at $138 billion.

A merger of Rio Tinto and Glencore would almost certainly put the combined company out of BHP’s reach for antitrust reasons. But Anglo-Teck could yet be an attractive target if and when the two companies’ merger is complete.

“It’s not obvious that this is the only thing they’ve got. There are other things that can happen,” said Cheveley. “To panic and pile in over the top of this one is not what you want to do.”

(By Thomas Biesheuvel, Dinesh Nair, Jack Farchy and Paul-Alain Hunt)

Kal Tire’s Mining Group, Decoda team up to develop KalPRO HaulSight

Kal Tire’s Mining Tire Group and Australian mining technology firm Decoda have announced a strategic alliance that the companies say will bring mines real-time, autonomous haul road hazard detection to increase truck productivity, tire life and fuel efficiency.

Kal Tire and Decoda have collaborated to develop KalPRO HaulSight, which builds on the momentum of KalPRO TireSight autonomous tire inspections.

“HaulSight’s ability to detect road hazards as they arise means mines can prevent the tire damage that TireSight detects,” Kal Tire’s technology services director Christian Erdelyi said in a news release.

“We’re excited about how this collaboration with Decoda will further our achievements in the autonomous space to bring customers even greater improvements to tire life, productivity and fuel efficiency.”

With Decoda’s LiDAR and camera sensors mounted to the front and rear of haul trucks, and an ‘edge’ computer processing live footage, HaulSight gives fleet teams instant alerts about hazards such as spillage, road undulations and high G-force events that can cause truck and tire damage and slow down operations, the company said.

Modeling TireSight, HaulSight’s scanning technology integrates with Kal Tire’s TOMS (Tire & Operations Managing System) and allows condition monitoring experts to assess flagged issues and automate priority-based work orders.

“HaulSight gives mine sites unprecedented visibility across the entire haul circuit and turns that insight into action. By making critical data easy to visualize and act on, operations see measurable improvements, like faster circuits and reduced downtime, from day one,” George Spink, Decoda’s executive general manager, stated.

“Leveraging Kal Tire’s longstanding relationships means we have the chance to bring these benefits to more mines.”

HaulSight enables road crews to react quickly and create optimal road conditions that maximize cycle speed and fuel use. When long-term planning opportunities arise, HaulSight calculates the cost to lost tire life, productivity and fuel against the cost of a road improvement.

“The responsiveness of the system means mine sites benefit right away with trucks spending more time hauling, but HaulSight also offers long-range planning insights that enable confident decision-making around tire maintenance and road upgrade investments,” Erdelyi added.

To ensure HaulSight is just as effective in sub-zero conditions, testing began on Canadian mine sites 18 months ago with strong results, the companies said, adding that since no two mines are alike, and no two roads even within a site are alike, HaulSight’s real-time feedback option can guide truck operators into loading or dumping spots to avoid impacts with road hazards.

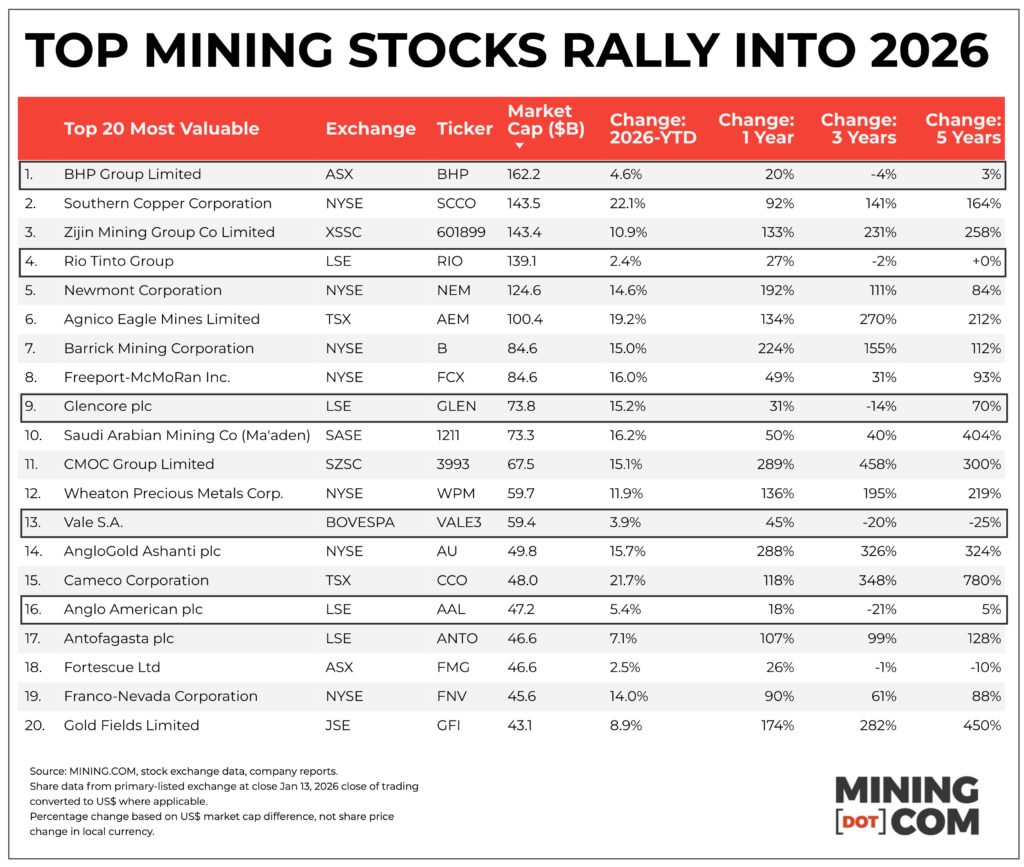

Rio Tinto kicked off number 2 perch, Agnico tops $100 billion for the first time

Global mining started 2026 the way it ended 2025 – with a huge rally.

Gold now looks to have $5,000 in sight, silver’s wild swings are getting wilder, and copper is hitting all time highs with regularity.

Mining stocks have duly responded, and after a blowout 2026, the Top 50 biggest mining stocks’ collective value now sits comfortably above the $2 trillion level reached at the end of last year.

You have to scour the corners of the mining world to find something that’s down and titanium and silicon are not exactly pillars of the industry.

While the metal and mineral price rally is broadbased and most mining stocks in the upper echelons already sport double digit percentage gains YTD, a few underperformers stand out. Stocks of the losers (or small gainers) appear to be driven by factors beyond buoyant metal prices.

Global mining is beefing up – and that’s before the mergers and acquisition currently being discussed.

Since inception, the MINING.COM TOP 50 was headed by two firms – BHP and Rio Tinto – the only miners with consistent market capitalizations above $100 billion (with a wobble here and there).

Now there are six firms with the distinction. The latest is Agnico Eagle, (TSX:AEM) which on Tuesday entered the ranks of the triple digit billion dollar miner. If only just.

The Toronto-based company joins Chinese champion Zijin Mining (SHA: 601899), Southern Copper (NYSE: SCCO), the mining arm of Grupo Mexico, and Denver’s Newmont Corporation (NYSE: NEM) which rode gold and copper prices all the way to the top towards the end of last year.

While the ascent of these counters is not surprising given gold’s glorious run and copper’s inexorable climb, the recent underperformance of BHP (ASX:BHP) and Rio Tinto (LSE:RIO), appears to have more to do with doubts over M&A.

While there is little separating them, it is striking that Rio Tinto is now in position number four, below Southern Copper and Zijin. Rio Tinto is up 2.2% on the LSE so far this year at $140.8 billion. Zijin has added 11% in Shanghai in USD terms while Southern Copper has surged by 22% in New York just eight trading days in.

In fact Rio Tinto and BHP (up 4.6% for $162 billion) are some of the only counters that have not seen double digit gains in 2026. Rio Tinto has received the sharp end of investor skepticism over a combination with Glencore.

Glencore in turn has gained 15.2% in value in London to $73.9 billion. The talks between Baar and Melbourne date back more than a year and investors have had ample time to digest its prospects.

The downsides of a deal for Rio Tinto, apart from what to do with coal, do not seem insurmountable while the upsides when it comes to copper are obvious. A merged entity would become the clear copper king with attributable production of roughly 1.6 million tonnes a year by 2028 – and when Glencore’s projects come on stream in the early 2030s it could hit 2m tonnes-plus (versus BHP and Codelco’s 1.3m tonnes).

Rio Tinto just this week appointed three investment banks to give advice so at least who needs who more may soon become apparent.

BHP’s lacklustre performance also appears to have an M&A angle, this time because the company has been relegated to the sidelines after more than one failed attempt over the years (including with Rio Tinto) while others partner up.

Today a RioCore would be worth not that much more than $200 billion (a number the likes of GOOG gains or gives up in an afternoon) and it’s easy to forget that BHP flirted with this level all the way back in April 2022 when it briefly displaced oil major Shell as the most valuable stock on the FTSE.

Trading in two other merger candidates has also been uninspiring. Anglo American (LSE:AAL) stock rose by 5.4% by Tuesday for a $46.7 billion valuation while Teck Resources (TSX:TECK.B) is 5.2% for the better at $24.3 billion in Toronto (well outside the top 20).

BHP’s odd last-minute intervention aside, AngloTeck is coming closer to reality with the EU poised to also clear the deal within weeks. At current prices a combined entity would only just make it into the top 10. That Anglogold Ashanti (NYSE:AU) is now worth more than its erstwhile parent must sting in the offices of 17 Charterhouse (slated for evacuation).

Apart from an operational level agreement with Glencore to explore in Canada’s Sudbury basin, absent from the conversation has been Vale (BOVESPA:VALE3).

Long the number three most valuable and for a day or two in 2022 also worth more $100 billion, the Brazilian miner continues to drift down the ranking. An IPO for the Rio de Janeiro-based company’s base metals unit would be in 2027 by the earliest.

Mining’s traditional big 5 diversified giants – BHP, Rio Tinto, Glencore, Vale and Anglo American – that trace their roots back many decades if not more than a century, not that long ago occupied the top five spots as a matter of course and constituted nearly a third of the overall value of the Top 50.

It is not just their recent performance that stands out, when looking at a three-year (or even five-year) chart it is hard not to conclude that the old guard has not kept up with the new world of mining.

Among spectacular gains for copper, gold and other commodity specialists with three/four or sometimes eight-fold gains in value since 2022, the geographically spread out, diversified mining model remains in the red.

And mergers and acquisitions and spinoffs and bolt-ons, it seems, do not provide solutions for this perennial disappointment.

Gold bars and coins. (Image by Zlaťáky.cz, Pexels.)

Gold vaulted above the historic $4,600 an ounce mark on Monday as a flare-up in geopolitical tensions and expectations of looser US monetary policy led bullion to hit its first record peak of 2026 after a string of all-time highs last year.

Here are some ways to invest in gold:

Spot market

Large buyers and institutional investors usually buy gold from big banks. Prices in the spot market are determined by real-time supply and demand dynamics.

London is the most influential hub for the spot gold market, with the London Bullion Market Association setting standards for gold trading and providing a framework for the over-the-counter market to facilitate trades among banks, dealers, and institutions.

China, India, the Middle East and the US are other major gold-trading centres.

Futures market

Investors can also get exposure to gold via futures exchanges, where people buy or sell a particular commodity at a fixed price on a particular date in the future.

COMEX, part of the New York Mercantile Exchange, is the largest gold futures market in terms of trading volumes.

The Shanghai Futures Exchange, China’s leading commodities exchange, also offers gold futures contracts. The Tokyo Commodity Exchange, popularly known as TOCOM, is another big player in the Asian gold market.

Exchange-traded products

Exchange-traded products or exchange-traded funds issue securities backed by physical metal, allowing people to gain exposure to gold prices without taking delivery of the metal itself.

Global gold ETFs witnessed the strongest year of inflows on record in 2025, led by North American funds, according to World Gold Council data. Annual inflows surged to $89 billion.

Bars and coins

Retail consumers can buy gold from metals traders selling bars and coins in shops or online. Gold bars and coins are both effective means of investing in physical gold.

What drives the market?

Investor interest and market sentiment

Rising interest from investment funds in recent years has been a major factor behind bullion’s price moves, with sentiment driven by market trends, news and global events fuelling speculative buying or selling of gold.

Foreign exchange rates

Gold is a popular hedge against currency market volatility. It has traditionally moved in the opposite direction to the US dollar, since weakness in the US currency makes dollar-priced gold cheaper for holders of other currencies and vice versa.

Monetary policy and geopolitical tensions

The precious metal is widely considered a safe haven during times of uncertainty.

US President Donald Trump’s trade tariffs have over the last year sparked a global trade war, rattling currency markets. Trump’s capture of Venezuelan leader Nicolas Maduro and aggressive statements on acquiring Greenland are adding to market volatility.

Global central banks’ policy decisions also influence gold’s trajectory. Lower interest rates reduce the opportunity cost of holding gold, since it pays no interest.

Central bank gold reserves

Central banks hold gold in their reserves, and demand from this sector has been robust in recent years because of macroeconomic and political uncertainty.

The World Gold Council said in its annual survey in June that more central banks plan to add to their gold reserves within a year despite high prices.

Net central bank purchases in November totalled 45 metric tons, World Gold Council data showed, pushing the figure for the first 11 months of 2025 to 297 tons as emerging market central banks continued their significant gold buying.

China kept adding gold to its reserves, with its holdings totalling 74.15 million troy ounces at the end of December from 74.12 million in the previous month as it extended its buying spree for the 14th month in a row.

(Compiled by Bangalore commodities and energy team; Editing by Peter Graff and Jan Harvey)

Caledonia plans to spend $132 million on Zimbabwe’s biggest gold mine this year

Caledonia Mining is weighing its options on how best to press the Bilboes gold mine in Zimbabwe back into service. Credit: Caledonia Mining

Caledonia Mining Corporation plans to spend $132 million this year to launch development of what, once operational, will be Zimbabwe’s largest gold mine, the company announced on Wednesday.

Miners are riding a wave of record bullion prices to expand output. Spot gold prices hit another record high of $4,639.48 an ounce early on Wednesday, fueled by escalating tensions in Iran, concern over the Federal Reserve’s autonomy and softer inflation readings that boosted rate cut bets.

Caledonia said in a production update that the planned spending, part of a $162.5 million total capital expenditure program for 2026, was subject to board approval and availability of funding.

Caledonia, which already operates the 80,000-ounce-per-year Blanket mine in Zimbabwe, plans to develop the Bilboes mine at a projected total capital cost of $584 million.

Production from the new mine is expected to begin in late 2028, with steady-state annual output of 200,000 ounces anticipated from 2029 for an initial period of 10 years.

The company has said it plans to fund the Bilboes project through a mix of non-recourse senior debt, contributions from existing operations as well as specialized financing methods such as streaming, where investors provide cash in return for future metal supply.

Caledonia’s expansion plans received a boost last month when Zimbabwe’s government reversed plans to double the gold royalty rate and change the tax treatment for capital expenditure.

(By Chris Takudzwa Muronzi; Editing by Nelson Banya and Joe Bavier)

Bharat Coking Coal draws $13 billion bids in India IPO

Bharat Coking Coal drew bids worth 1.17 trillion rupees ($12.97 billion) for its $118.7 million initial public offering on Tuesday, as prospects of strong demand for coking coal from steelmakers lifted appetite for the shares.

The company, which is India’s top coking coal miner, received bids for 50.93 billion shares, nearly 147 times the number of shares on offer, at the end of three days of bidding, as per exchange data.

The firm is a subsidiary of state-owned Coal India.

The strong response underscores continued investor interest in Indian primary market after two years of record fund-raising.

Bharat Coking Coal is the first mainboard IPO in India this year and consists entirely of a stake sale by its parent.

India ranked as the world’s second-largest primary market in 2025 after the United States, with 367 IPOs raising $21.8 billion, according to LSEG data.

Offerings from companies such as LG Electronics India and ecommerce platform Meesho drew strong demand during the year.

“Despite turbulence in the secondary market, this shows that primary market remains buoyant. The investor interest in Bharat Coking Coal is also driven by its strong parentage,” said Kranthi Bathini, director of equity strategy at WealthMills Securities.

“The Indian coking coal industry benefits from structural demand growth driven by government-led infrastructure development, capacity addition in steel manufacturing, and policy emphasis on import substitution,” said Ventura Securities.

Qualified institutional buyers bid for 24.61 billion shares of Bharat Coking Coal, about 311 times the number of shares on offer for them, leading the subscriptions.

Non-institutional investors and retail investors quota were subscribed 258 times and 49 times, respectively.

($1 = 90.1780 Indian rupees)

(By Vivek Kumar M; Editing by Nivedita Bhattacharjee)

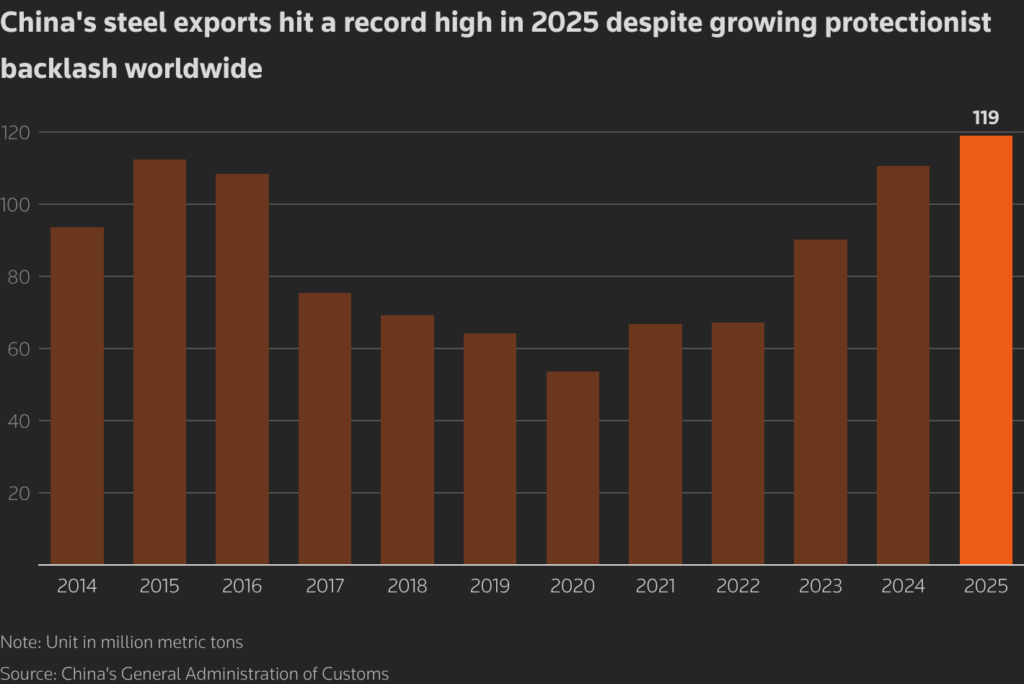

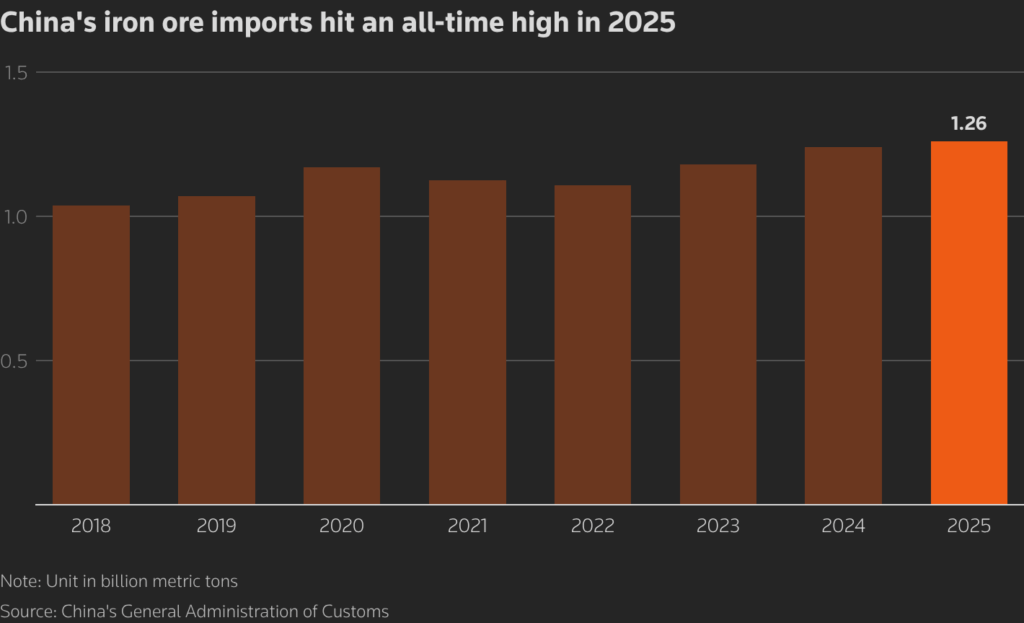

China’s steel exports, iron ore imports hit record highs

China’s steel exports hit a record monthly high in December, fueled by front-loading driven by Beijing’s announcement of an export licence requirement for shipments from 2026.

The world’s largest steel producer shipped 11.3 million metric tons of the metal used in construction and manufacturing last month, the highest for a single month, data from the country’s General Administration of Customs showed on Wednesday.

Beijing has plans to roll out a licence system from 2026 to regulate steel exports, as robust shipments have sparked a growing protectionist backlash worldwide.

Some exporters rushed to ramp up shipments before January on fears that the export licence requirement might impact shipments, analysts said.

Despite surprisingly high exports, China’s prolonged property market woes have remained a drag on steel consumption.

China’s steel demand is projected to slide by 1% this year after an annual fall of 5.4% in 2025, according to a forecast from a state-backed research agency.

Steel exports for the whole year rose by 7.5% from the year before to an all-time high of 119.02 million tons despite an increasing number of countries throwing up trade barriers on Chinese steel arguing that domestic manufacturing has been hurt.

Iron ore imports at record

Iron ore imports in the world’s largest consumer hit a record high last year as low in-plant inventories and improved steel margins encouraged mills to book more cargoes.

Chinese steelmakers have kept low inventories at plants since late 2022 as a demand slump caused by the crisis-hit property market strained their cash flow.

Moreover, robust steel exports underpinned resilient demand for the key steelmaking ingredient, analysts said.

Imports in December rose 8.2% from the month before to 119.65 million tons, the highest for a month, bringing the total in 2025 to a record high of 1.26 billion tons with a rise of 1.8% from 2024.

Global iron ore supply is forecast to grow by 2.5% in 2026, and shipments to China are expected to increase by between 36 million and 38 million tons, piling pressure on prices this year, said Bai Xin, an analyst at consultancy Horizon Insights.

(By Amy Lv and Lewis Jackson; Editing by Jacqueline Wong and Tomasz Janowski)

Congo pitches new $29 billion iron ore and logistics project

The Democratic Republic of Congo, one of the world’s biggest producers of copper and cobalt, wants to add a $29 billion iron ore project to its mineral portfolio.

The country’s government has created a project called Mines de Fer de la Grande Orientale, or MIFOR, to develop a particularly rich seam of ore in the remote north of the country, Mines Minister Louis Watum told the council of ministers Friday, according to minutes published on the website of the office of the prime minister. The deposit has an estimated 20 billion tons of resources at an average grade of 60%, he said.

The first phase of the project would require the construction of heavy rail and transport on the Congo River to the deep-water port of Banana on the Atlantic Ocean and cost $28.9 billion, Watum said. Initial production capacity would be approximately 50 million tons per year, expandable to 300 million tons, Watum told the council.

“After more than 100 years of mining primarily focused on copper and cobalt, the MIFOR project marks a major strategic shift in the Democratic Republic of Congo’s extractive model,” Watum said, according to the minutes.

The project has already attracted institutional investors, he told the council, which agreed to create an inter-ministerial commission dedicated to the project.

(By Michael J. Kavanagh)

Radiant unloads BHP iron ore in China as trader tests curbs

A bulk carrier laden with BHP Group’s Jimblebar iron ore has discharged in China after weeks idling offshore, in a rare case of a trader pressing ahead with restricted cargoes despite an ongoing pricing dispute.

The Berge Mawson unloaded its cargo, owned by trading firm Radiant World, at the northern port of Caofeidian in the first week of January and has now left the country, Bloomberg ship tracking data show. The vessel saw lengthy delays after port storage constraints led to a backlog of ships waiting to offload cargoes.

The Jimblebar Fines blend is one of the BHP products subject to curbs imposed by China’s state-run iron ore trader. The nation is the world’s largest buyer of the steelmaking staple and BHP one of its biggest suppliers. As such, the fate of the cargo has become a focal point for traders wanting to gauge whether restricted material can ultimately be sold in the country, according to people familiar with the matter.

Radiant World is a private trading company that has grown rapidly in recent years to become one of the largest players in the market. The Berge Mawson had been anchored off the coast since early December before finally docking on Dec. 31.

It isn’t clear whether Radiant has found a buyer, or whether the ore is stacked up at the port and yet to clear customs. Prolonged delays to shipments threaten to tie up vessels and raise demurrage and storage costs.

BHP is locked in a dispute with China Mineral Resources Group Co., the state-run firm set up in 2022 to consolidate iron ore purchases and wrest pricing power away from foreign miners. Although CMRG told steelmakers in September to stop purchasing Jimblebar, there may be mills that aren’t linked to the state-owned firm willing to take the product. Others might seek special approval from CMRG.

Radiant World and BHP both declined to comment. CMRG didn’t respond to a request for comment. Another vessel loaded with BHP ore that’s being closely watched by traders, the Ever Shine, has been idling off the port of Qingdao since early December

CMRG is also in talks with BHP’s Australian peers, Rio Tinto Group and Fortescue Ltd., for long-term supply deals in 2026. Meanwhile, Chinese customs has been stepping up checks to screen for cargoes of BHP ore, said two of the people, who declined to be named discussing a sensitive matter.

China’s customs administration didn’t immediately respond to a fax seeking comment.