Global integrated reporting is essential if the planet is to achieve net-zero emissions.

COMMENT

26 July 2022

A gas flare at an oil well in North Dakota. Credit: Andrew Burton/Getty

In March, the United Nations took its first meaningful step to hold investors, businesses, cities and regions accountable for reducing greenhouse-gas emissions, when UN secretary-general António Guterres asked an expert panel to develop standards for ‘net-zero’ pledges by these groups. A challenge now is how to count emissions coherently.

Nations, companies and scientists each use different, disjointed methods to tally greenhouse-gas emissions. These numbers cannot easily be compared or combined. The existing patchwork of greenhouse-gas inventories is woefully inadequate. From governments to businesses, information on these emissions is inconsistent, incomplete and unreliable.

To design effective carbon taxes, border tariffs and other zero-carbon policies or investments, the numbers need to be reconcilable across all levels, from product supply chains all the way up to planetary scale. The sum of national emissions should tally with growth in atmospheric carbon dioxide and estimates of carbon sinks.

We are researchers and practitioners from academia, industry and non-profit organizations who have developed a vision for an integrated global system of greenhouse-gas ‘ledgers’ that can balance the books of emissions and removals across the planet. Using interoperable accounting methods adapted from the financial sector, this system must create inventories of greenhouse gases emitted by nations and companies, catalogue emissions embodied in global supply chains and track fluxes of these gases in and out of ecosystems. Recent advances in remote sensing and digital technologies put this vision within reach. Here we outline a road map for doing so.

Global patchwork

Greenhouse-gas accounting is the measurement, analysis and reporting of data on emissions and removals of gases such as CO2 and methane that cause climate change. The atmospheric concentration of greenhouse gases is the bottom line. It holds humanity to account for how we use our remaining ‘carbon budget’ — the total amount of CO2 that can be emitted over a period of time while avoiding a dangerous rise in global temperatures above a certain threshold.

Climate simulations: recognize the ‘hot model’ problem

Scientists monitor global carbon sources and sinks. For example, the Global Carbon Project measures, analyses and reports flows of CO2, methane and nitrous oxide into and out of the atmosphere from human activities (such as transport, industry and land use) and natural environments (such as forests, soils and oceans)1.

At the national level, governments follow UN guidelines to self-report emissions from human activities in their territories. Most rely on tables of ‘emissions factors’ for these calculations. These factors give typical rates of greenhouse-gas emissions for various activities, such as using different energy sources or producing particular farm crops.

Businesses, cities and other non-state actors follow other standards adapted from UN guidelines (such as ghgprotocol.org). These also rely on emissions factors to count direct and indirect emissions from supply chains and the use of products. For example, when a company makes a pair of jeans, it must account for its own emissions from sewing and delivering the trousers to stores. It should also count emissions from growing the cotton and converting it to fabric, as well as laundering by the consumer and the ultimate disposal of the clothing. Often, more than 80% of a company’s emissions are indirect.

Inconsistent and incomplete ledgers, among both businesses and governments, prevent accurate assessments of decarbonization policies and investments. For example, adding ethanol produced from maize (corn) to petrol might not provide any carbon benefit when emissions from land-use change and other activities involved in its production are accurately counted2.

Reliability constraints

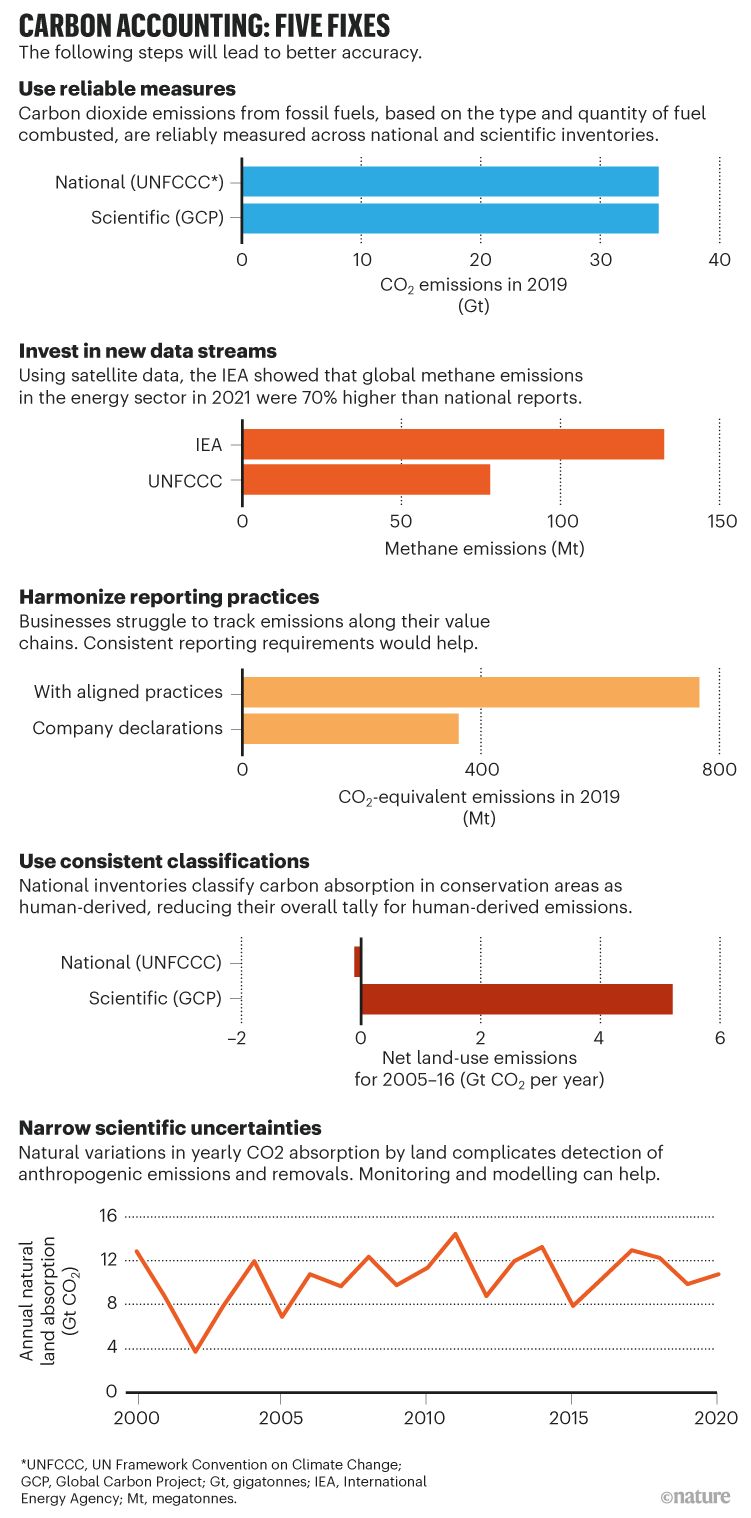

Emissions of CO2 from fossil fuels and industry can be tallied with relatively high confidence. But it is difficult to account reliably for non-CO2 gases and for emissions across the land sector and in supply chains and carbon offsets (see ‘Carbon accounting: five fixes’). Inventories are rife with measurement errors, inconsistent classification and gaps in accountability.

In March, the United Nations took its first meaningful step to hold investors, businesses, cities and regions accountable for reducing greenhouse-gas emissions, when UN secretary-general António Guterres asked an expert panel to develop standards for ‘net-zero’ pledges by these groups. A challenge now is how to count emissions coherently.

Nations, companies and scientists each use different, disjointed methods to tally greenhouse-gas emissions. These numbers cannot easily be compared or combined. The existing patchwork of greenhouse-gas inventories is woefully inadequate. From governments to businesses, information on these emissions is inconsistent, incomplete and unreliable.

To design effective carbon taxes, border tariffs and other zero-carbon policies or investments, the numbers need to be reconcilable across all levels, from product supply chains all the way up to planetary scale. The sum of national emissions should tally with growth in atmospheric carbon dioxide and estimates of carbon sinks.

We are researchers and practitioners from academia, industry and non-profit organizations who have developed a vision for an integrated global system of greenhouse-gas ‘ledgers’ that can balance the books of emissions and removals across the planet. Using interoperable accounting methods adapted from the financial sector, this system must create inventories of greenhouse gases emitted by nations and companies, catalogue emissions embodied in global supply chains and track fluxes of these gases in and out of ecosystems. Recent advances in remote sensing and digital technologies put this vision within reach. Here we outline a road map for doing so.

Global patchwork

Greenhouse-gas accounting is the measurement, analysis and reporting of data on emissions and removals of gases such as CO2 and methane that cause climate change. The atmospheric concentration of greenhouse gases is the bottom line. It holds humanity to account for how we use our remaining ‘carbon budget’ — the total amount of CO2 that can be emitted over a period of time while avoiding a dangerous rise in global temperatures above a certain threshold.

Climate simulations: recognize the ‘hot model’ problem

Scientists monitor global carbon sources and sinks. For example, the Global Carbon Project measures, analyses and reports flows of CO2, methane and nitrous oxide into and out of the atmosphere from human activities (such as transport, industry and land use) and natural environments (such as forests, soils and oceans)1.

At the national level, governments follow UN guidelines to self-report emissions from human activities in their territories. Most rely on tables of ‘emissions factors’ for these calculations. These factors give typical rates of greenhouse-gas emissions for various activities, such as using different energy sources or producing particular farm crops.

Businesses, cities and other non-state actors follow other standards adapted from UN guidelines (such as ghgprotocol.org). These also rely on emissions factors to count direct and indirect emissions from supply chains and the use of products. For example, when a company makes a pair of jeans, it must account for its own emissions from sewing and delivering the trousers to stores. It should also count emissions from growing the cotton and converting it to fabric, as well as laundering by the consumer and the ultimate disposal of the clothing. Often, more than 80% of a company’s emissions are indirect.

Inconsistent and incomplete ledgers, among both businesses and governments, prevent accurate assessments of decarbonization policies and investments. For example, adding ethanol produced from maize (corn) to petrol might not provide any carbon benefit when emissions from land-use change and other activities involved in its production are accurately counted2.

Reliability constraints

Emissions of CO2 from fossil fuels and industry can be tallied with relatively high confidence. But it is difficult to account reliably for non-CO2 gases and for emissions across the land sector and in supply chains and carbon offsets (see ‘Carbon accounting: five fixes’). Inventories are rife with measurement errors, inconsistent classification and gaps in accountability.

Sources: Reliable measures: The Washington Post (https://go.nature.com/3PHDQZW)/Global Carbon Project; Data streams: Ref. 3; Reporting practices: Ref. 4; Classifications: Ref. 5; Uncertainties: Ref. 1

Poor data can lead to inaccurate emission factors, such as when emissions are measured at only a few locations over brief time intervals. For example, one analysis in February used the latest satellite data to show that methane emissions from the energy sector were 70% higher than those reported by national accounts, which use emissions factors that are based on idealized conditions and don’t include leaks from fossil-fuel operations3.

Data gaps and inconsistent application of accounting standards lead to widespread undercounting of emissions. For example, only one-third of suppliers provide information on their indirect emissions to customers4, leading companies to report different levels of emissions for similar activities. In the technology sector, proper inclusion of indirect emissions from purchased goods and product usage can double emissions estimates4.

Inconsistent classifications make it hard to compare emissions. For example, following UN guidelines, many national inventories classify conservation areas as managed lands. The carbon absorbed there is then considered as human-derived removal, which can be used to offset fossil-fuel emissions. Scientists, by contrast, classify emissions and removals from conservation lands as natural5.

Ambiguity in human versus natural sources of some emissions leads to gaps in accountability. For example, wildfire emissions are typically classified as natural, and are thus not counted in national, provincial or corporate ledgers, even though they can be significant6. According to California’s Air Resources Board, the state’s emissions from wildfires in 2020 exceeded those generated from electricity. In Canada in 2018, British Columbia’s wildfires emissions were three times greater than all other emissions in the province combined (see go.nature.com/3zewvna).

The atmospheric impact of nature-based carbon removal is poorly quantified. For example, evaluations of steps to increase forest cover must account for the possibility that such changes might have occurred anyway, that they might be reversed by fire, or that they could cause more forest clearance elsewhere. These risks are captured inconsistently in current accounting practices7.

Insufficient transparency creates opportunities for misrepresentation, by making it difficult to use scientific observations to verify emissions reported by businesses. For instance, in 2021, the Oil and Gas Climate Initiative, which represents about 30% of oil and gas producers globally, reported that methane emissions by its members were 0.2% of gas production8. Without disclosure of the underlying data, this low value is difficult to reconcile with scientific assessments, which range from 3.7%9 to 9.4%10 of gas production in different regions.

Scientific uncertainties limit how observations can be used for verification. For example, the amount of carbon taken up by forests and soils can vary from year to year in ways that are difficult to predict, and can differ by more than annual increases in human-caused emissions11.

There is also little oversight. Under the Paris climate agreement, nations’ self-reported emissions are reviewed but rarely verified independently. For companies, nearly all greenhouse-gas reporting is voluntary and not externally reviewed.

Some progress

Things are getting better. At the UN’s COP26 climate meeting in November 2021, new rules were established to prevent double counting in international carbon-offset markets. The International Sustainability Standards Board (ISSB) was launched to support the financial sector in reporting sustainability metrics consistently. In 2023, the Greenhouse Gas Protocol will issue corporate-accounting guidance for land use and carbon removal.

Huge gaps in detection networks plague emissions monitoring

Some governments are stepping in. In March this year, the US Securities and Exchange Commission proposed a rule mandating that corporations disclose information on their emissions; the United Kingdom and European Union are advancing similar rules.

And scientific uncertainties are narrowing. Satellites can now provide measurements of atmospheric greenhouse-gas concentrations almost in real time. Remote sensing and advanced analytics help to track terrestrial emissions more accurately, with increasing global coverage12.

Digital tools that automate greenhouse-gas accounting are proliferating. Platforms are emerging from companies such as SAP, Salesforce and Microsoft (where A.L. and L.J. work) to allow businesses to combine data on their activities with emissions factors compiled from government, private and non-profit sources. These tools are reducing the time and expertise needed for such accounting.

But much work remains. Even with improved standards and mandatory reporting, many companies and nations might not have the resources to be able to comply. Digital platforms are at risk of facilitating inaccurate emissions accounting if underlying data are unreliable. National and corporate accounting systems often use outdated emissions factors and data. Scientific studies are often misaligned with national and corporate accounting needs. Data across corporate, national and planetary ledgers are difficult to compare, combine and share.

Global integration

We propose a more holistic approach, in which each greenhouse-gas ledger — whether for a company, city or nation — is one node of an interconnected global system. From consumers choosing low-carbon products to nations imposing regulations on trade, decisions require information drawn from multiple ledgers to reliably assess the consequences for the planetary carbon budget. For example, emissions data from thousands of products and companies would be needed to fully implement a carbon border adjustment mechanism. (This levies a carbon tariff on imports to protect domestic companies from competition by producers in countries with weaker climate policies.)

Smoke from wildfires plagued San Francisco in September 2020.

The effect on regional emissions tallies can be significant.

Credit: David Paul Morris/Bloomberg/Getty

Interoperability is key. The capacity to exchange data and process information from multiple sources is essential for integrated emissions accounting, just as it underpins the financial sector12. Most businesses worldwide use the eXtensible Business Reporting Language (XBRL) for digital financial reporting to regulators and investors. XBRL, which is free and managed by an international not-for-profit consortium, provides an open standard for defining terms, exchanging data between information systems and creating shared, searchable data repositories. With XBRL, financial information can be rapidly and accurately aggregated, transmitted and analysed. This facilitates transactions across borders, enables peer-to-peer transactions and extends access to the financial system to communities that are underserved by banks.

A similar system for greenhouse-gas accounting, with emissions data for products held in interoperable repositories, would make it easier to track emissions across value chains. Faster and more granular reporting would direct purchasing and investment towards low-carbon innovations more effectively. Interoperability would allow reporting platforms to access the most current and reliable data. Oversight and accountability would be improved. Greater transparency would build public confidence.

Scientists would gain access to larger, more compatible data sets at higher temporal and spatial resolution. Artificial intelligence (AI) and machine learning could be used, for example, to update and tailor emissions factors to changing conditions and local contexts. As a result, forecasting of the impacts of policies and climate change itself would improve.

Next steps

Four components are essential for this system to work.

Data. Researchers and practitioners need to assess the opportunities for and constraints on improving the quality of data and data products in greenhouse-gas accounting, especially concerning land, non-CO2 gases, offsets and indirect emissions. Those engaged in all aspects of greenhouse-gas measurement, accounting and reporting, from product to planetary scales, should first identify which data gaps most undermine the reliability of emissions accounting. They should ask: where should investments in research and development be targeted to close gaps? What are the best prospects for improvements using the latest technologies? How can new data streams and knowledge be most rapidly integrated into emissions-accounting infrastructure? And how can stubbornly poor data be worked around?

Interoperability. Protocols and principles for enabling the interoperability of a digital infrastructure for greenhouse-gas accounting need to be agreed. This should be done in an open and inclusive process overseen by an independent governing body, such as the ISSB in partnership with the UN.

Three sets of protocols will be needed. First, technical and syntactic rules are required that specify how information is to be read by humans and machines. Data must be formatted for seamless exchange between ledgers, platforms and data libraries. A starting point could be the Sustainability Accounting Standards Board’s proposed XBRL-based guidelines for corporate sustainability reporting.

G20’s US$14-trillion economic stimulus reneges on emissions pledges

Second, there need to be clearer definitions of the myriad metrics and terms used so that systems can unambiguously exchange information — known as semantic interoperability. Examples include how uncertainty is quantified, how offsets are classified and how emissions are parsed between managed or unmanaged lands. An ontology will be required to align the meanings of terms. A common set of metrics must be agreed, which will provide the greenhouse-gas record of any entity. This would mirror the US health sector’s Common Clinical Data Set for any patient.

Third, protocols and principles for institutional interoperability are needed. These include policies and regulations to facilitate data exchange across borders and between companies. Different frameworks need to be harmonized. Decisions need to be made on how to govern AI and distributed digital ledgers (such as blockchain) within the system.

Trust. Greenhouse-gas reports must be trusted by decision-makers, regulators and the public. Transparency is key. Data on emissions, removals and progress by nations and companies towards their commitments should be publicly available in an interoperable, machine-readable form. This could be achieved by collecting emissions reporting in one global registry, or in an interoperable network of national registries (through the UN Framework Convention on Climate Change) and sectoral ones (such as the disclosure system CDP). Open access to data would enable independent verification, for example by comparing reported emissions with satellite-based measurements, as the Verify project has done for countries in the EU from 2018 to 2022 (see https://verify.lsce.ipsl.fr).

Although companies have legitimate privacy concerns related to business operations, these could be overcome by standards for emissions audits that maintain confidentiality. Audits must go beyond confirming that the correct procedures were followed, and should encompass checks on the quality and completeness of the data. Transparency and independent verification are needed to assure the trustworthiness of emissions data, as well as the emissions factors and other data products used in accounting.

Finance. New funding models are needed to support the generation of emissions data and information products as digital public goods. Current models have limitations. For example, private satellite services delay the release or degrade the resolution of public versions to protect profits. And government research and philanthropic seed money are neither sufficient nor appropriate for operationalizing emissions data and accounting services.

Public–private partnerships could offer a solution. For example, the US National Weather Service uses application programming interfaces to make real-time data available to businesses that package and market data products to consumers. Philanthropists fund collaborations between academic, government and industry partners, such as MethaneSat, Carbon Monitor and Carbon Mapper, to track methane and CO2 emissions. Blended-finance models, which leverage public funds and loan guarantees to reduce risk and attract capital investment to sustainable development projects, could be adapted for greenhouse-gas information systems. Challenges to be overcome include intellectual-property rights and data sovereignty.

Such steps will make greenhouse-gas accounting more reliable. That alone won’t solve the climate crisis, but it is essential for implementing strategies that could.

Nature 607, 653-656 (2022)

doi: https://doi.org/10.1038/d41586-022-02033-y

References

Friedlingstein, P. et al. Earth Syst. Sci. Data 14, 1917–2005 (2022).

Article Google Scholar

Lark, T. J. et al. Proc. Natl Acad. Sci. USA 119, e2101084119 (2022).

PubMed Article Google Scholar

International Energy Agency. Global Methane Tracker 2022 (IEA, 2022).

Google Scholar

Klaaßen, L. & Stoll, C. Nature Commun. 12, 6149 (2021).

PubMed Article Google Scholar

Grassi, G. et al. Nature Clim. Change 11, 425–434 (2021).

Article Google Scholar

United Nations Environment Programme. Spreading Like Wildfire: The Rising Threat of Extraordinary Landscape Fires (UNEP, 2022).

Google Scholar

Joppa, L. et al. Nature 597, 629–632 (2021).

Article Google Scholar

Oil and Gas Climate Initiative. Accelerating Ambition & Action: A Progress Report from the Oil and Gas Climate Initiative (OGCI, 2021).

Google Scholar

Zhang, Y. et al. Sci. Adv. 6, eaaz5120 (2020).

PubMed Article Google Scholar

Chen, Y. et al. Environ. Sci. Technol. 56, 4317–4323 (2022).

PubMed Article Google Scholar

Peters, G. P. et al. Nature Clim. Change 7, 848–850 (2017).

Article Google Scholar

Seele, P. J. Clean. Prod. A 136, 65–77 (2016).

Article Google Scholar

Download references

Interoperability is key. The capacity to exchange data and process information from multiple sources is essential for integrated emissions accounting, just as it underpins the financial sector12. Most businesses worldwide use the eXtensible Business Reporting Language (XBRL) for digital financial reporting to regulators and investors. XBRL, which is free and managed by an international not-for-profit consortium, provides an open standard for defining terms, exchanging data between information systems and creating shared, searchable data repositories. With XBRL, financial information can be rapidly and accurately aggregated, transmitted and analysed. This facilitates transactions across borders, enables peer-to-peer transactions and extends access to the financial system to communities that are underserved by banks.

A similar system for greenhouse-gas accounting, with emissions data for products held in interoperable repositories, would make it easier to track emissions across value chains. Faster and more granular reporting would direct purchasing and investment towards low-carbon innovations more effectively. Interoperability would allow reporting platforms to access the most current and reliable data. Oversight and accountability would be improved. Greater transparency would build public confidence.

Scientists would gain access to larger, more compatible data sets at higher temporal and spatial resolution. Artificial intelligence (AI) and machine learning could be used, for example, to update and tailor emissions factors to changing conditions and local contexts. As a result, forecasting of the impacts of policies and climate change itself would improve.

Next steps

Four components are essential for this system to work.

Data. Researchers and practitioners need to assess the opportunities for and constraints on improving the quality of data and data products in greenhouse-gas accounting, especially concerning land, non-CO2 gases, offsets and indirect emissions. Those engaged in all aspects of greenhouse-gas measurement, accounting and reporting, from product to planetary scales, should first identify which data gaps most undermine the reliability of emissions accounting. They should ask: where should investments in research and development be targeted to close gaps? What are the best prospects for improvements using the latest technologies? How can new data streams and knowledge be most rapidly integrated into emissions-accounting infrastructure? And how can stubbornly poor data be worked around?

Interoperability. Protocols and principles for enabling the interoperability of a digital infrastructure for greenhouse-gas accounting need to be agreed. This should be done in an open and inclusive process overseen by an independent governing body, such as the ISSB in partnership with the UN.

Three sets of protocols will be needed. First, technical and syntactic rules are required that specify how information is to be read by humans and machines. Data must be formatted for seamless exchange between ledgers, platforms and data libraries. A starting point could be the Sustainability Accounting Standards Board’s proposed XBRL-based guidelines for corporate sustainability reporting.

G20’s US$14-trillion economic stimulus reneges on emissions pledges

Second, there need to be clearer definitions of the myriad metrics and terms used so that systems can unambiguously exchange information — known as semantic interoperability. Examples include how uncertainty is quantified, how offsets are classified and how emissions are parsed between managed or unmanaged lands. An ontology will be required to align the meanings of terms. A common set of metrics must be agreed, which will provide the greenhouse-gas record of any entity. This would mirror the US health sector’s Common Clinical Data Set for any patient.

Third, protocols and principles for institutional interoperability are needed. These include policies and regulations to facilitate data exchange across borders and between companies. Different frameworks need to be harmonized. Decisions need to be made on how to govern AI and distributed digital ledgers (such as blockchain) within the system.

Trust. Greenhouse-gas reports must be trusted by decision-makers, regulators and the public. Transparency is key. Data on emissions, removals and progress by nations and companies towards their commitments should be publicly available in an interoperable, machine-readable form. This could be achieved by collecting emissions reporting in one global registry, or in an interoperable network of national registries (through the UN Framework Convention on Climate Change) and sectoral ones (such as the disclosure system CDP). Open access to data would enable independent verification, for example by comparing reported emissions with satellite-based measurements, as the Verify project has done for countries in the EU from 2018 to 2022 (see https://verify.lsce.ipsl.fr).

Although companies have legitimate privacy concerns related to business operations, these could be overcome by standards for emissions audits that maintain confidentiality. Audits must go beyond confirming that the correct procedures were followed, and should encompass checks on the quality and completeness of the data. Transparency and independent verification are needed to assure the trustworthiness of emissions data, as well as the emissions factors and other data products used in accounting.

Finance. New funding models are needed to support the generation of emissions data and information products as digital public goods. Current models have limitations. For example, private satellite services delay the release or degrade the resolution of public versions to protect profits. And government research and philanthropic seed money are neither sufficient nor appropriate for operationalizing emissions data and accounting services.

Public–private partnerships could offer a solution. For example, the US National Weather Service uses application programming interfaces to make real-time data available to businesses that package and market data products to consumers. Philanthropists fund collaborations between academic, government and industry partners, such as MethaneSat, Carbon Monitor and Carbon Mapper, to track methane and CO2 emissions. Blended-finance models, which leverage public funds and loan guarantees to reduce risk and attract capital investment to sustainable development projects, could be adapted for greenhouse-gas information systems. Challenges to be overcome include intellectual-property rights and data sovereignty.

Such steps will make greenhouse-gas accounting more reliable. That alone won’t solve the climate crisis, but it is essential for implementing strategies that could.

Nature 607, 653-656 (2022)

doi: https://doi.org/10.1038/d41586-022-02033-y

References

Friedlingstein, P. et al. Earth Syst. Sci. Data 14, 1917–2005 (2022).

Article Google Scholar

Lark, T. J. et al. Proc. Natl Acad. Sci. USA 119, e2101084119 (2022).

PubMed Article Google Scholar

International Energy Agency. Global Methane Tracker 2022 (IEA, 2022).

Google Scholar

Klaaßen, L. & Stoll, C. Nature Commun. 12, 6149 (2021).

PubMed Article Google Scholar

Grassi, G. et al. Nature Clim. Change 11, 425–434 (2021).

Article Google Scholar

United Nations Environment Programme. Spreading Like Wildfire: The Rising Threat of Extraordinary Landscape Fires (UNEP, 2022).

Google Scholar

Joppa, L. et al. Nature 597, 629–632 (2021).

Article Google Scholar

Oil and Gas Climate Initiative. Accelerating Ambition & Action: A Progress Report from the Oil and Gas Climate Initiative (OGCI, 2021).

Google Scholar

Zhang, Y. et al. Sci. Adv. 6, eaaz5120 (2020).

PubMed Article Google Scholar

Chen, Y. et al. Environ. Sci. Technol. 56, 4317–4323 (2022).

PubMed Article Google Scholar

Peters, G. P. et al. Nature Clim. Change 7, 848–850 (2017).

Article Google Scholar

Seele, P. J. Clean. Prod. A 136, 65–77 (2016).

Article Google Scholar

Download references

AUTHORS

Amy Luers ,

Leehi Yona ,

Christopher B. Field ,

Robert B. Jackson ,

Katharine J. Mach ,

Benjamin W. Cashore ,

Cynthia Elliott ,

Lauren Gifford ,

Colleen Honigsberg ,

Lena Klaassen ,

H. Damon Matthews ,

Andi Peng ,

Christian Stoll ,

Marian Van Pelt ,

Ross A. Virginia &

Lucas Joppa

Leehi Yona ,

Christopher B. Field ,

Robert B. Jackson ,

Katharine J. Mach ,

Benjamin W. Cashore ,

Cynthia Elliott ,

Lauren Gifford ,

Colleen Honigsberg ,

Lena Klaassen ,

H. Damon Matthews ,

Andi Peng ,

Christian Stoll ,

Marian Van Pelt ,

Ross A. Virginia &

Lucas Joppa

No comments:

Post a Comment