It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Sunday, July 20, 2025

How Seawater Could Solve the Lithium Supply Crisis

Researchers developed a vermiculite membrane to efficiently extract lithium from seawater.

This technology could reduce environmental damage and geopolitical risks tied to traditional lithium mining.

It may also help diversify global supply chains and unlock new sources of critical minerals.

The world is going to need a whole lot of lithium to power a more sustainable future. The critical mineral is an essential ingredient in a wide range of clean energy technologies and is particularly essential in batteries for electric vehicles and energy storage–two rapidly expanding global sectors. But there are a lot of problems associated with extracting and sourcing lithium, from environmental degradation and public health hazards to market uncertainty and heightened geopolitical vulnerabilities. However, a brand new technological breakthrough might have provided a way to get around nearly all of those pitfalls.

A team of researchers from the U.S. Department of Energy’s (DOE) Argonne National Laboratory and the University of Chicago has found a way of “mining without a mine” by extracting lithium from one of the planet’s most infinitely renewable resources: seawater. The method uses a membrane made of vermiculite, an abundant, cost-effective, and naturally occurring form of clay. This membrane “filters lithium ions with remarkable efficiency, offering a potential domestic alternative to traditional mining,” according to Interesting Engineering.

While extracting lithium from brine is not a new idea, current technologies are inefficient and extremely water-intensive. Because of this, the sector has a high exposure to risks associated with climate change, as 50% of mines are located in very high and arid areas like South America’s Atacama Desert. But reports indicate that this new vermiculite membrane method is more refined. “Filtering by both ion size and charge, our membrane can pull lithium out of water with much greater efficiency,” said the study’s first author Yining Liu, a Ph.D. candidate at UChicago.

Avoiding traditional mining techniques solves a myriad of problems facing traditional lithium extraction. Any form of mining is associated with a heavy environmental cost, and lithium mining is no exception. Usually, richer countries outsource those environmental risks to poorer nations with rich lithium deposits. But with this new technology, any country with a coast can source lithium in a cost-effective and relatively environmentally friendly manner.

Demand for lithium has skyrocketed over the past few years, largely driven by the clean technology sector. Global lithium demand rose 63% between 2021 and 2023, from 101,000 tons to 165,000 tons, and is on track to increase another 222% to reach 531,000 tons by 2030. However, despite this runaway growth rate, lithium prices have remained volatile and even experienced paradoxical slumps thanks to gross overproduction from China.

China’s chokehold over global lithium supply chains is one of the primary challenges facing the sustainability and security of the critical mineral. Chinese companies control 25% of the world’s lithium mining capacity and 60% of the world’s refining capacity for EV-battery-grade lithium. By next year, China will overtake Australia to become the single largest lithium miner in the world.

The International Energy Agency ranks lithium’s geopolitical risk as a 3 out of 5, noting that 85% of global lithium production comes from just three countries – Australia, Chile, and China. And China has signalled that it is not afraid to flex its geopolitical might to disrupt global supply chains to further its own political interests. This weak spot in global lithium supply chains has only been exacerbated by Trump-era tariffs and a growing global trend toward nationalism and protectionism.

The ability to cost-effectively and safely extract lithium from seawater would reconfigure much more equitable and resilient global lithium supply chains. “Such a membrane could reduce our dependence on foreign suppliers and open the door to new lithium reserves in places we never considered,” said researcher Liu.

Furthermore, this method could have potential for extracting other critical minerals as well, including nickel, cobalt, rare earth elements. The membrane could even be utilized to remove harmful contaminants from drinking water, potentially counteracting the lithium sector’s long history of water contamination.

By Haley Zaremba for Oilprice.com

KoBold signs Congo deal to boost US mineral supply

Kobold, backed by investors including Bill Gates and Jeff Bezos

The Democratic Republic of Congo has struck a preliminary mineral exploration agreement with US‑based Kobold Metals, deepening American involvement in its critical minerals sector.

The deal opens the door to US investment in what is a major global supplier of cobalt and copper. The African nation also holds substantial reserves of lithium, tin and tungsten.

Kobold, backed by investors including Bill Gates and Jeff Bezos, agreed “in principle” to apply for exploration permits and digitize Congo’s geological data, according to a presidential announcement.

The deal signed in Kinshasa with President Félix Tshisekedi marks a strategic push for US to gain access to critical minerals such as cobalt, copper and lithium. It aligns with a broader US‑Congo initiative aimed at reducing China’s dominance in the minerals’ supply chain.

Kobold plans to deploy its AI‑powered exploration tools and begin a lithium project in the mining town of Manono, in the southeastern province of Tanganyika. The company said it will fund digital geological mapping, hire local staff and support infrastructure investments in host communities.

The exploration agreement complements Kobold’s earlier progress, including a $1 billion framework to acquire part of the Manono lithium deposit from Australia’s AVZ Minerals — a move supported by the US government. However, the final outcome remains contingent on resolving ongoing legal disputes and securing necessary permits.

(With files from Bloomberg)

Rare Earths Rally After the Pentagon Picks a Winner

The Pentagon’s landmark deal with MP Materials guarantees magnet prices and gives the U.S. government a direct equity stake.

Rare earth stocks worldwide soar as investors rotate into Western producers and juniors following the MP announcement.

Apple quickly follows with a $500M commitment to source recycled magnets from MP, boosting the reshoring momentum.

Shares of rare earths companies have exploded higher since MP Materials (NYSE:MP) unveiled a game-changing deal with the U.S. Department of Defense that marks the most aggressive federal intervention in the rare earths space in decades. The DoD-backed investment package will see the Nevada-based producer build out a fully domestic magnet supply chain and lock in long-term pricing support for neodymium-praseodymium, the critical alloy used in everything from fighter jets to iPhones. MP shares have doubled in just days, taking year-to-date gains north of 275% and re-rating the entire Western rare earths complex.

The deal isn’t just about cash; it’s about control. Under the agreement, the Pentagon will take a 15% equity stake in MP through a $400 million preferred share issuance and secure warrants for additional common stock down the road. The government is also extending a $150 million loan, while JPMorgan and Goldman Sachs are syndicating $1 billion in private financing to bring MP’s so-called “10X Facility” online. Construction is already underway, with commissioning slated for 2028.

The real deal sweetener is a $110/kg floor price guarantee for NdPr magnets, nearly double today’s spot price of $63. That pricing mechanism, backed by the full faith and credit of the U.S. government, creates a bulletproof margin environment for domestic producers and resets the cost basis for long-term buyers across defense, autos, and consumer electronics, according to Reuters.

Analysts say it's the rare earths equivalent of a strategic petroleum reserve, but for permanent magnets.

MP’s planned capacity of 10,000 metric tons per year will cover a significant chunk of U.S. magnet demand and more than double current domestic output. For defense planners, the numbers are even more compelling: that volume would be enough to secure magnet supply for the entire F-35 fleet, major missile systems, and naval sonar applications—all without touching Chinese exports.

The move immediately drew follow-on activity. Apple Inc. said it would invest $500 million to source NdFeB magnets from MP made entirely from recycled feedstock. The tech giant, which has faced mounting scrutiny over its reliance on Chinese rare earths, said production would begin in 2027 and ramp up to cover “hundreds of millions” of devices per year. Apple will source from MP’s upgraded facility in Mountain Pass, California, and its soon-to-be-operational Texas plant, using material pulled from discarded devices and scrap.

The Apple deal adds enormous commercial legitimacy to MP’s scale-up and underscores the trend toward localization at the OEM level. Recycled magnet manufacturing has long been viewed as a technical curiosity. Now it’s a $500 million line item on Apple’s strategic sourcing agenda.

Meanwhile, rare earth equities have gone vertical. Lynas Rare Earths (OTCPK:LYSDY) surged to a two-year high after Jefferies hiked its price target from A$6.40 to A$10, calling the company “the next logical beneficiary” of U.S.-led reshoring. Iluka Resources exploded 30% in a single session—its biggest one-day gain on record—as investors rotated into any name with near-term capacity outside China. Australian juniors like Liontown and Sayona also caught a bid.

MP added to the frenzy by announcing a $500 million common stock offering to fund continued expansion and working capital—triggering a minor pullback in the stock but doing little to dent the broader narrative. Capital is pouring into rare earths like it’s 2011.

Defense contractors were quick to endorse the move. Lockheed Martin, prime contractor for the F-35, said it welcomed efforts to “strengthen secure, resilient supply chains.” Analysts say the move will de-risk magnet inputs for THAAD batteries, Virginia-class submarines, and next-gen missile systems. At the industrial level, General Motors and Stellantis are evaluating new sourcing options for permanent magnet EV motors as they accelerate domestic platform rollouts.

What sets this deal apart is its structure. Rather than handing out tax credits or indirect subsidies, the U.S. government is writing equity checks, underwriting price floors, and letting commercial lenders come in behind. The structure resembles the CHIPS Act, but more serious. Analysts say this model could be replicated for battery anodes, graphite, and even gallium.

Still, execution risks loom. MP will need a reliable pipeline of rare earth oxide feedstock, and while it has upstream capability at Mountain Pass, questions remain about whether that will scale fast enough. Labor and permitting hurdles in both California and Texas could delay full ramp-up. And there's the broader question of how quickly defense and OEM contracts can be converted into long-term offtake agreements.

As of mid-July 2025, Beijing has remained quiet. No official response from the Chinese government or state media has been issued in response to the Pentagon-MP announcement. That silence is notable. In 2024, Chinese officials warned against “artificially constructing supply chains” without China. That language has not been repeated publicly this year.

But observers note that China's influence remains concentrated in refining, oxide conversion, and separation, areas where Western capacity still lags. Any serious U.S. effort to localize rare earths will inevitably collide with these structural realities, and Beijing may yet respond through informal levers like export permit delays or price manipulation.

By Alex Kimani for Oilprice.com

Billionaire turns Pentagon into Trump’s defense investment wing

The equity investment in MP Materials Corp. – the first in modern Pentagon history – was a priority for the Cerberus Capital Management co-founder

Steve Feinberg, the Defense Department’s 36th deputy defense secretary. Credit: US DoD

Just four months into his tenure at the Pentagon, private equity billionaire Steve Feinberg has landed his first big deal: a $400 million bet on the US’s only miner of rare earth elements, a key commodity in the rivalry with China.

The equity investment in MP Materials Corp. – the first in modern Pentagon history – was a priority for the Cerberus Capital Management co-founder, who took over as deputy secretary of defense in March, according to people familiar with the efforts. The deal, which comes alongside $1 billion in financing from JP Morgan Chase & Co. and Goldman Sachs Group Inc., is to be the first of several aimed at leveraging Pentagon support and Wall Street cash to jump-start efforts to break China’s lock on global supplies of rare earth minerals, the people said.

Feinberg, who has made few public comments since taking office, declined to respond to written questions for this article. In his confirmation hearing, he vowed to make unleashing US critical-minerals production a priority and highlighted the need to accelerate use of the Defense Production Act – a law dating back to the Korean War that was used for the MP deal.

US dependence on Chinese supplies of rare earth minerals – used for everything from cars to missiles to data centers – emerged as a key vulnerability for the administration when Beijing cut off supplies this spring in retaliation for President Donald Trump’s tariffs, driving the White House to the negotiating table.

Pentagon officials immediately began canvassing the industry for ways to ramp up production of permanent magnets, an especially critical product made from neodymium-praseodymium oxide.

Feinberg pushed the MP deal despite objections within the Pentagon about using DPA authority, which typically involves loans, to take a 15% equity stake that would make the Pentagon MP’s largest shareholder, according to people familiar with the matter. The company highlighted the “unconventional use” of the law, along with the fact the Pentagon will need to secure more funding from Congress for the deal, among the risk factors it disclosed to investors.

US administrations have for years sought to develop domestic supplies of the minerals to counter China’s grip on 85% of global processed supplies. But the domestic industry has struggled for decades with high costs and brutal competition from Beijing.

“DoD selected a unique approach to this agreement to account for the difficulties in establishing and sustaining production of critical rare earth magnets in a market environment in which China controls much of the supply chain,” a Pentagon spokesperson said.

The MP deal includes a 10-year agreement to establish a price floor that’s nearly double current market prices to ensure profitability, as well as a Pentagon commitment to make sure all the so-called permanent magnets the Las Vegas-based company will produce at a new factory find either defense or commercial customers.

The deal, followed days later by a $500 million pact with Apple, catapulted MP’s stock to a record. Hopes of similar agreements boosted share prices across the small US rare earth sector.

Feinberg is eager to build national champions across key sectors to boost US competitiveness, according to people familiar with his thinking. He’s personally making decisions on which companies will get Pentagon funding through the DPA, which allows the government to support strategic projects. He co-signed the MP deal with his boss, Defense Secretary Pete Hegseth.

“Taking a partial stake is something I have not seen,” said William Greenwalt, a former deputy undersecretary of defense for industrial policy. “It is much easier for DoD to own the factory or means of production and bring a contractor in to perform the work.”

Feinberg made his name in private equity and has deep experience dealing with defense contractors. He’s also known on Wall Street for keeping a tight circle of staff, a characteristic that’s carried over to his Defense Department post, according to people familiar with the situation. Secrecy around the MP deal was especially tight.

“Even though there’s significant government equity, they’re also moving a lot of capital,” said Gracelin Baskaran, director of the critical minerals security program at the Center for Strategic and International Studies. “That’s what you want out of federal dollars — you want federal dollars to mobilize a lot of private capital.”

The bet on MP is a potentially risky one. The last company that owned the deposit MP is now developing went bankrupt. Most of the expertise in refining the materials and turning them into magnets is in China.

“There’s a lot of good faith in this, but for the taxpayer I’m concerned,” said David Abraham, a critical minerals specialist at Boise State University. “We’ve chosen a company that’s never made magnets to rely on to make all the magnets.”

Israel’s only Red Sea port at Eilat is on the verge of a full commercial halt as municipal authorities freeze the operator’s accounts, citing unpaid taxes and concession fees totaling around NIS 10 million (~$3 million). The financial crisis reflects the sharp fallout from nearly 20 months of Houthi missile and drone attacks in the Red Sea, which have slashed port revenues by over 90%, according to the Times of Israel.

The closure, which is set to begin on July 20, has been confirmed by both Israel’s Ports Authority and National Emergency Authority, with additional reporting by Marine Insight. Regional sources, including Middle East Eye, highlight that municipal authorities froze the port’s accounts after months of deferred payments and repeated shortfalls, with throughput effectively collapsed since late 2023.

“The Eilat port has strategic national importance to Israel as the country’s southern gateway on the Red Sea for maritime trade with the Far East, India, and Australia, and constitutes a significant economic anchor for the city and its residents,” Eilat port CEO Gideon Golber told The Times of Israel. “The closure of a strategic seaport in Israel would be a huge international success for the Houthis that none of our enemies have ever achieved.”

From an energy-sector standpoint, the shutdown impairs not only general trade volumes but also strategic flows such as potash exports and potential crude oil movements via the Eilat-Ashkelon pipeline. Shipping firms now face costly rerouting either to Mediterranean terminals or via the Cape of Good Hope. However, that alternative adds over 6,000 nautical miles and days to transit times.

Analysts say the financial unraveling at Eilat reflects the wider vulnerability of Red Sea logistics infrastructure under massive and lasting pressure. With no clear resolution in sight, maritime risk premiums are rising, and Israeli authorities face a dilemma: absorb emergency losses to sustain operations or abandon the Red Sea corridor altogether. Either choice carries implications for regional energy supply chains and long-term port viability.

Despite objections from ExxonMobil, Chevron has completed its planned acquisition of privately-held rival Hess, including a 30 percent stake in Exxon's lucrative Stabroek Block developments off Guyana.

Exxon attempted to block the Hess acquisition by filing an arbitration case through the International Chamber of Commerce. Hess's contract for the ownership of the Stabroek Block lease included a clause providing right of first refusal to Exxon in the event of a sale of Hess' stake; Exxon insisted that this clause applied in the event of the sale of Hess itself. Chevron disagreed, and acrgued

On Friday morning, Exxon lost its arbitral case, and Chevron completed the process of closing on the acquisition of Hess within four hours of the arbitration panel's announcement. Chevron CEO Mike Wirth celebrated the win, thanking the arbitral panel for recognizing the "longstanding practice and understanding that asset-level rights of first refusal do not apply in parent company merger and acquisition transactions."

Exxon has accepted the reality that - despite its objections - Chevron is its new business partner in the Stabroek Block project. "We disagree with the ICC panel’s interpretation but respect the arbitration and dispute resolution process," Exxon said in a statement. "We welcome Chevron to the venture and look forward to continued industry-leading performance and value creation in Guyana."

The Stabroek Block is one of the world's most promising offshore finds, and is a powerhouse behind Exxon's profit margins. The IEA predicts that it will singlehandedly produce one percent of the world's oil in future years. Even with the high cost of offshore operations, the first four Stabroek FPSOs will produce oil at a breakeven cost of less than $35 per barrel, according to independent estimates - meaning that even in an era of low oil prices, the projects will still be profitable.

Chevron Completes Hess Megadeal After Winning Guyana Arbitration

Chevron Corporation said on Friday it had completed the $53-billion acquisition of Hess Corporation after winning an arbitration case against Exxon over the Guyana assets of Hess.

In 2023, Chevron proposed a $53-billion deal to buy Hess Corp and thus take Hess’s assets in the Bakken in North Dakota and the 30% stake in Guyana’s Stabroek offshore oil field—a top-performing asset with the potential to yield even more barrels and billions of U.S. dollars for the project’s partners.

Exxon is the operator of the Stabroek block with a 45% stake. Hess held 30%, and China’s state firm CNOOC has the remaining 25% stake.

Proceeds for the consortium, which is already pumping more than 660,000 barrels per day (bpd) from several projects in the block, are rising with growing production, even at relatively lower oil prices, because the Guyana block is estimated to have a breakeven oil price of about $30 per barrel.

Chevron’s bid to buy Hess’s stake in the Guyana projects was challenged by Exxon and CNOOC, who claim they have a right of first refusal for Hess’s stake under the terms of a joint operating agreement (JOA) for the Stabroek block. Hess and Chevron claimed the JOA doesn’t apply to a case of a proposed full corporate merger.

The dispute went to arbitration, which ruled in favor of Chevron, the company said today, announcing the completion of the Hess acquisition, “following the satisfaction of all necessary closing conditions, including a favorable arbitration outcome regarding Hess’ offshore Guyana asset.”

Chevron now owns a 30% position in the Guyana Stabroek Block, which has more than 11 billion barrels of oil equivalent discovered recoverable resource.

In addition, the Federal Trade Commission (FTC) on Friday lifted its earlier restriction, clearing the way for John Hess to join Chevron’s Board of Directors, subject to Board approval.

“The combination enhances and extends our growth profile well into the next decade, which we believe will drive greater long-term value to shareholders,” said Mike Wirth, Chevron chairman and CEO.

The article questions whether large M&A transactions in the E&P sector consistently translate into tangible shareholder value, despite initial promises of immediate accretion and synergies.

The ExxonMobil acquisition of Pioneer Natural Resources is examined as a case study, highlighting the industrial logic behind the deal but also pointing out the lack of immediate financial benefits for ExxonMobil shareholders, such as increased stock price or EPS accretion.

The author suggests that while M&A may offer long-term benefits in terms of scale and sustainability for companies, the short-term impact on shareholder returns often appears negligible or even negative, describing it as a "shell game" for investors.

I've been noodling around with an idea for a while now. The thing on my mind is when do investors actually gain from the big gobs of money E&P companies spend on M&A? A lot of promises are made in the early days. But as time wears on, I rarely see any effort made to reconcile results with these promises. So bear with me as I go through this little exercise.

Now I am not saying that M&A isn't necessary as strong companies buy out smaller, weaker companies to get their premium assets. That part of the transaction is easily understood, and I will review that thought in the ExxonMobil/Pioneer Natural Resources case as we go through this exercise. My point here is investors are still waiting for these results to show up in their mail box. In fairness, not a lot time has elapsed, but I think trends are instructive. Let's dive in.

Upstream M&A: Shell game?

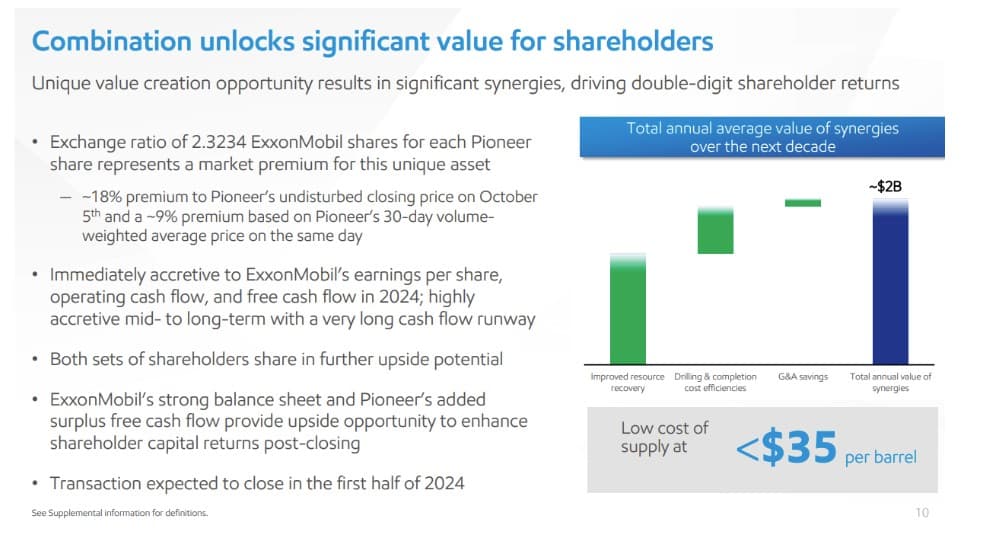

The upstream industry has been on a buying binge the last several years with hundreds of billions worth of transactions on the books. One of the most notable thus far has been ExxonMobil’s (NYSE:XOM) acquisition of Pioneer Natural Resources, for approximately $253 per share or a substantial $64.5 billion, including debt, in an all-stock transaction. As noted in the deal slide from the announcement, this was an 18% premium to recent pricing for Pioneer. In exchange for XOM diluting current holders of its stock by about 255 mm shares or ~6%, the company made some firm promises in regard to the future upside for the combined company. Among other things XOM holders were told the transaction would be “immediately accretive to EPS.” Hold that thought.

Some time has gone by since the deal closed in May of 2024 and it seemed appropriate to peek under the hood to see how the company was delivering on these commitments. It’s also worth reviewing just what drove Exxon’s interest in paying a premium to Pioneer to obtain their Midland acreage.

The Industrial Logic of ExxonMobil and Pioneer

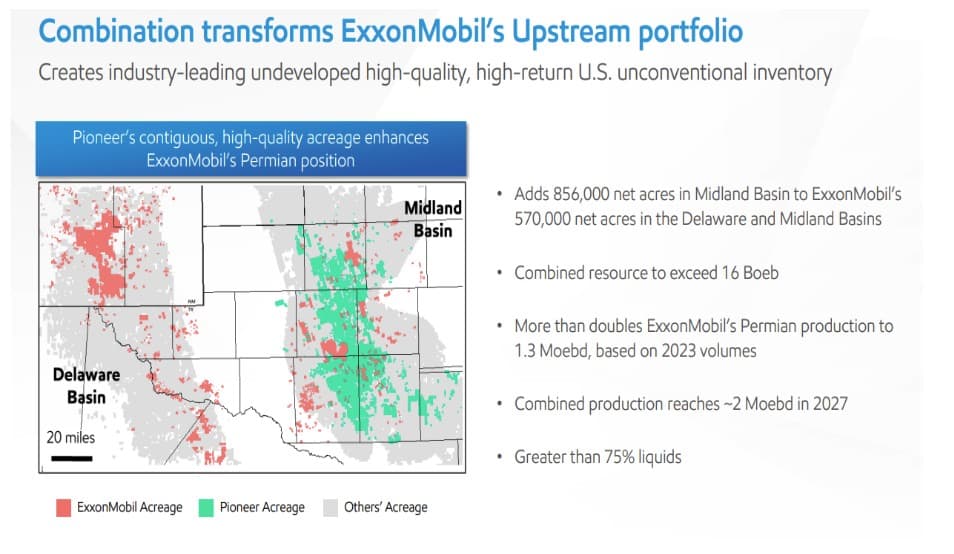

Industrial logic is the term applied to these mega deals. It’s one of the terms, along with synergy and accretive, that are bandied about on announcement day. As you can see below, Pioneer’s Midland basin acreage was like a missing puzzle piece to Exxon’s prior footprint in the play. Exxon is a technology company with a track record of pushing the envelope to drive down costs and increase production, but to fully deploy their technical expertise, they needed more room.

When you snap the two pieces together, you get a blocky, connected plot of land that runs for 50-75 miles east and west, and the better part of a couple of hundred miles north and south. 1.4 million acres is a sizeable chunk of dirt. That’s significant and opens the door to huge numbers of 4-5 mile laterals, with centralized logistics, sand, water, the stuff of fracking, and helping lock-in low cost of supply. The easy stuff put in place, XOM engineers are free to work their magic wringing maximum barrels out of each foot of completed interval. That’s all great for the company, but does this add to the value of the company in a way that benefits shareholders? Something real, and tangible that they can spend. Today. Like the stock price going up. Or special dividends. It seems like it should, and that’s where we will look next for any sign the company is about to embark on an enhanced shareholder rewards package.

Capitalization is one metric by which we might judge the impact of a transaction. Suppose company A, worth X, buys company Z, worth Y. In that case, logic suggests that company AZ should match the value of the two merger partners, or X + Y. Referring back to our ExxonMobil example, on May 2nd, the day before the merger closed the share price of XOM was $116.21 per share. With 3,998,000,000 shares outstanding that works out to a capitalization of $462 bn. At the agreed price of $253 per share for Pioneer their capitalization was $59.5 bn. The two together should have created an entity worth $521 bn, a point from which the merger driven success of the company should have been a value accretion launching pad. By the end of 2024 XOM stock was trading at $107.27. With 4,424 bn shares outstanding the company’s capitalization stood at $474 bn. In about six months, some $47 bn in capitalization had vanished into thin air.

Investors were promised the transaction would be immediately accretive to earnings per share. In June, 2024 reporting for the second quarter showed EPS to be $2.14 per share. For the fourth quarter EPS was $1.67 per share. So no immediate accretion. Perhaps patience will pay off. For the first quarter of 2025 EPS was $1.76 per share and the forecast for Q-2 is $1.55 share. One step forward and another back. What matters is that, thus far the combined company has not equaled its standalone performance. This is a sobering thought in light of the dilution visited upon shareholders, and the expense the company is going to repurchase shares.

I may be piling on a bit here as the time elapsed since the merger is minimal. ROCE or Return on Capital Employed, shows little sign of being moved significantly higher in the merger. For a Twelve-Trailing Month-TTM period, Exxon’s ROCE was 0.10882, a slight improvement from Full Year-2024’s 0.1082. Moving in the right direction, but after spending $64.5 bn in stock dilution, one might hope for a teensy bit more. Like I said, perhaps not enough time has gone by to attach much weight to the change in ROCE.

Summing up

So, where does that leave us as we eagerly anticipate another mega merger? I refer, of course, to the one that now hangs in the balance for Chevron (NYSE:CVX) and Hess (NYSE:HES), with an arbitrator set to rule on XOM’s claim of primacy in the pre-emptive right to buy HESS’ share in the Stabroek field, offshore Guyana. If we buy into CVX today it will cost us $150 per share. If the arbitrator rules in their favor and the assets of Hess are merged into CVX, will the price of CVX then become X+Y-dilution? Or the CVX price plus the Hess price of $171 per share, less the amount of stock CVX will print~$351 mm shares to meet the deal price of $60 bn? Will the combined company have a capitalization of $327 bn? If history is any guide this outcome is unlikely.

It is certainly food for thought as another serial acquirer comes to mind. I refer here to Occidental Petroleum, (NYSE: OXY), which after the Anadarko deal of 2019 for $57 bn, and then the CrownRock deal of 2024 for $12 bn- a combined cash and stock outlay of $69 bn for a company with a present day capitalization of $42 bn. Warren Buffett with a 26.92% stake in OXY, for which he’s paid an average of $51.92 per share, is down 21% on his investment. I wonder what his response would be today if the OXY plane landed in Omaha with a deal in management’s pocket. I have a pretty good idea actually.

I will reiterate-the Industrial logic of upstream M&A is abundantly clear. As an industry matures size and scale matter, and perhaps (likely) this is where value shows up for shareholders who remain long for an extended period. The company can continue to develop oil and gas deposits long after the standalone company would have drilled itself out of existence. But over the short run, it looks like a shell game to me.