Copper price jumps as China traders cheer prospect of lower US levies

Base metals gained as China’s markets reopened after the Lunar New Year break and traders cheered potentially lower US tariffs.

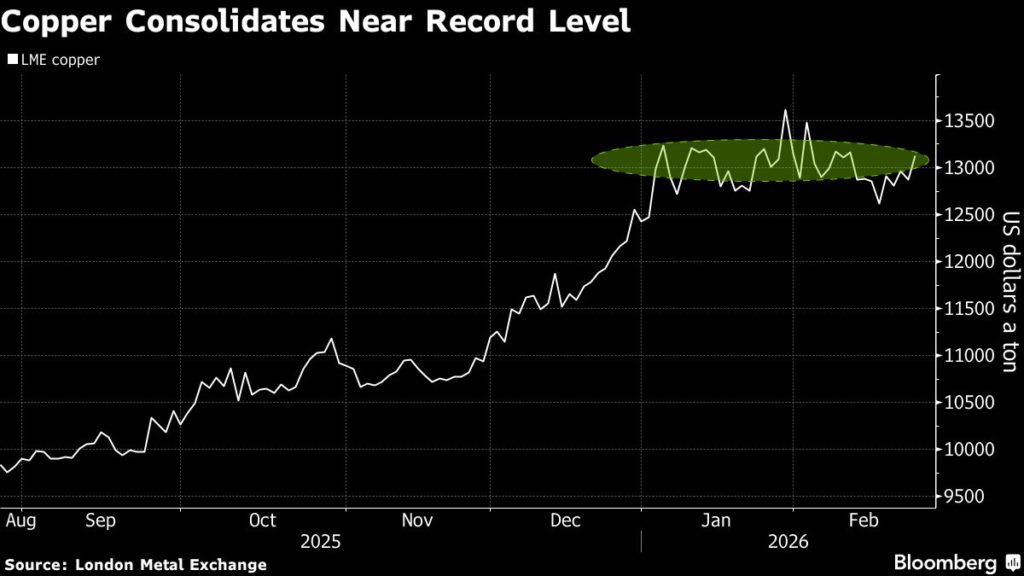

Copper rallied as much as 2.8% to reach $13,228 a ton in London and aluminum also inched higher. China faces less-punitive charges, a boost for the country’s metal-intensive exports, with the administration proposing a 15% levy after the Supreme Court ruled against President Donald Trump’s reciprocal duties.

“The US Supreme Court dismantled the most cost-effective tariff instrument, but not the new tariff regime overall,” Allianz SE analysts, including chief investment officer Ludovic Subran, wrote in a note. “Uncannily, the Global South and China now emerge as the biggest winners.”

The gains in metals were echoed by a positive tone in mainland equities, as the benchmark CSI 300 Index also advanced on Tuesday. Under the new trade framework — if it’s confirmed — Morgan Stanley estimated that the average US levy on goods from China will drop to 24% from 32%.

The US news is bullish for metals, said Jon Li, an analyst at Guangzhou Finance Holdings Futures Co. Demand from manufacturers will return, he added.

Copper has consolidated at a high level since hitting a record in January, with moves driven by frequent shifts in US policy, as well as mine snarls and forecasts for higher consumption from the energy transition. Higher prices have weighed on physical demand in China, causing exchange-tracked inventories to expand to the highest since 2024. Holdings of the red metal have been rising in the US, as well as in London Metal Exchange-tracked sheds.

Copper rose 2.3% to settle at $13,166.50 a ton on the LME. Aluminum was up 0.1%, as all base metals climbed.

Column: Copper drives BHP and Rio, but getting more is the trick

The latest corporate results from major miners BHP Group and Rio Tinto highlight copper’s starring role in driving profits, but they also underline how difficult it will be to get more exposure to the industrial metal.

BHP, the world’s largest listed miner, reported last week a stronger-than-expected half-year underlying attributable profit of $6.2 billion, up 22% from the same period a year earlier.

What was notable in the results was that for the first time the miner earned most of its operating earnings from copper, with a contribution of 51%, overtaking iron ore.

A similar dynamic was in evidence at Rio Tinto, with annual iron ore earnings dropping to around 60% of the miner’s total, down from 70% in the prior year, while those from copper doubled to about 30%.

The greater role of copper in the mining companies’ earnings is largely explained by price movements, with copper outperforming iron ore, which has struggled in line with softer Chinese steel production and rising supply.

London copper futures closed at $12,868.50 a metric ton on Monday, down slightly from the previous session and 11.4% below the all-time high of $14,527.50 hit on January 29.

However, copper has been in a sustained uptrend since April last year, and has risen 59% from a low of $8,105 a ton on April 25 to its close on Monday.

The rally has been driven by several factors including US stockpiling amid uncertainty over the tariff policy of President Donald Trump and supply disruptions at major mines.

But there is also a long-term fundamental driver for copper insofar as it is a vital component of the energy transition given its role in the electrification of power and transport systems.

Estimates vary as to how much more copper is going to be needed, but the more modest end of the scale is for a doubling of demand by 2050.

Finding long-term copper deposits is both challenging and costly, which explains why both BHP and Rio went looking to acquire existing mines.

Deals stymied

BHP proposed buying Anglo American in both 2024 and 2025, but eventually walked away from the projected $53 billion deal, largely because of differences in valuation of assets.

Anglo’s South American copper assets were what BHP wanted, and it was less interested in the iron ore, coal and diamonds also housed in the London-listed, former South African mining company.

Anglo instead found its own suitor in Canada’s Teck Resources in another $53 billion deal that will create the world’s fifth-largest copper producer when finalized.

Rio also tried to bulk up its copper production through a merger with Glencore, which would have created a $200 billion mining giant and the world’s largest copper producer.

Once again it was differences over valuations that scuppered the deal, with Glencore holding out for a greater share of the merged entity than Rio was prepared to offer.

With the benefit of hindsight and in view of the strong rally in copper, both Anglo and Glencore were probably correct in rejecting the overtures from BHP and Rio.

What the failure of these proposed mega-mergers shows is that any successful deal will require a much higher premium for the copper assets, one that reflects likely copper demand in 10 or 20 years, rather than what demand is currently.

It also makes it more likely that companies like BHP and Rio will be forced to either start gobbling up junior miners or start exploring and developing new mines, or a combination of both if they want to boost the share of copper in their portfolios.

And what of iron ore, the commodity that built both BHP and Rio into the companies they are today?

China’s steel output fell below 1 billion tons in 2025 for the first time since 2019, and it’s likely that it has now peaked and will slowly decline in coming years.

China buys about 75% of seaborne iron ore and it will remain the major market, but it is also going to get an increasing share from mines it controls in Guinea, where the Simandou project is ramping up over the coming years to an annual capacity of 120 million tons.

This has been reflected in prices, with Singapore Exchange iron ore contracts trading in a narrow range around $100 a ton for much of last year, but dipping below that level on February 13 and ending at $98.46 on Monday.

This is a double whammy for BHP and Rio, with lower prices meeting ebbing demand from China.

The question is whether the rising steel sectors in India and other Asian countries will be enough to compensate for what’s lost in China.

(The views expressed here are those of the author, Clyde Russell, a columnist for Reuters.)

(Editing by Muralikumar Anantharaman)

Disclosure: At the time of publication Clyde Russell owned shares in BHP Group and Rio Tinto as an investor in a fund.

No comments:

Post a Comment