Credit card holders out thousands after deal between company, bank goes bad

Story by Rosa Marchitelli • Yesterday

Constance McCall can't catch a break.

The Edmonton woman needed to fix her credit score after getting divorced, so she signed up for a secured credit card that promised to help her do that.

Instead, she's out thousands of dollars, and left with a credit score that's worse than when she started.

McCall, 59, is one of many cardholders stuck in the middle of a bitter legal battle between the credit card company and the bank it partnered with, Calgary-based Digital Commerce Bank, also called DC Bank.

She signed up for the Visa through Plastk Financial & Rewards after seeing it recommended on Credit Karma, a website she trusted.

Plastk promises cardholders the chance to improve their credit scores by reporting their transactions to the credit bureau Equifax.

As a secured card, the credit limit matches whatever customers prepay for a security deposit — between $300 and $10,000.

Plastk founder and CEO Motola Omobamiduro launched his company in October 2020, and partnered with Calgary-based Digital Commerce Bank. (Jenn Blair/CBC)© Provided by cbc.ca

Plastk says customers can cancel any time and get their deposit back after a two-month holding period if the account is in good standing.

After cancelling in December, McCall was expecting $4,500 to be returned in February. Without it, she's had to borrow from family and friends to pay for the basics.

"It was extremely humbling — $4,500 is not a little amount of money, especially for someone like myself. It's huge," she said.

"That was going to pay my next two months' rent, buy my food."

After Go Public brought McCall's case to the company's attention, Plastk refunded her entire deposit — four months after she was supposed to get it back.

Plastk has 7,000 customers across Canada. Go Public spoke to a dozen — hundreds more have posted complaints online — who say they too are out hundreds or thousands of dollars.

Gail Henderson, an expert in consumer finance, says consumers who use secured credit cards backed by non-bank lenders need to be better protected.

Credit cards backed by bank lenders are heavily regulated by the federal Financial Consumer Agency of Canada (FCAC), she says, but cards offered by organizations that are not banks — such as Plastk — have fewer regulations and are overseen by general provincial consumer protection branches.

The FCAC warns consumers to "be careful when applying for a secured card from an unknown financial institution," and recommends checking with the institution to make sure security deposits are insured.

The agency says, in a report published in June, that non-bank consumer complaints about financial products and services have a much lower rate of resolution than those about banks.

Gail Henderson, an associate professor in the Faculty of Law at Queen’s University, is an expert in consumer finance. (Alexis Raymon/CBC)© Provided by cbc.ca

The FCAC report also said most surveyed Canadians don't understand that financial products not backed by banks have less consumer protection.

It suggested that oversight of non-bank products and services ought to be brought up to the stricter level of federally regulated banks and credit unions.

Pedro Oliveira of Hamilton cancelled his Plastk card on Feb. 12 and is still waiting for his $1,000 deposit. After failing to get a resolution with Plastk after about 100 days he filed a complaint with the Better Business Bureau, then he turned to the government — and got sent in a circle.

"I reached out to Consumer Protection Ontario," he said, "and they told me to reach out to the Financial Consumer Agency of Canada who told me to reach out to Consumer Protection Ontario."

Brian Kline of Maple Ridge, B.C., never received hiscard from Plastk after he sent a $2,500 deposit. In late October he asked to cancel his card, and is still waiting for his refund.

He too reported to the Better Business Bureau, then DC Bank, which sent him back to Plastk. Then he tried the Ombudsman for Banking Services and Investments, which said the matter isn't under its jurisdiction. He says the Better Business Bureau closed his complaint as unresolved.

DC Bank says the problem with customer refunds is not its responsibility, since it's not part of the credit agreement between Plastk and its customers. (Google maps)© Provided by cbc.ca

"In all honesty, I'm not confident in ever having my hard-earned money lawfully returned to me," he said.

Plastk CEO and founder Motola Omobamiduro says he is trying to pay customers back, but their money is being held up by DC Bank.

Plastk and DC Bank partnered in April 2020. Court documents show their dispute started about two years later when DC Bank said Plastk owed unpaid fees and wasn't providing the required funds for the bank to pay Visa.

Plastk said the bank was unfairly imposing new rules and fees and that its technology didn't always work — limiting Plastk's ability to do business.

Plastk sued for $5 million in January, and DC Bank counter-sued for $3.8 million a few weeks later.

McCall says the real shock was finding out the businessman behind Plastk is a former used car salesman with a conviction for breaking a consumer protection law.

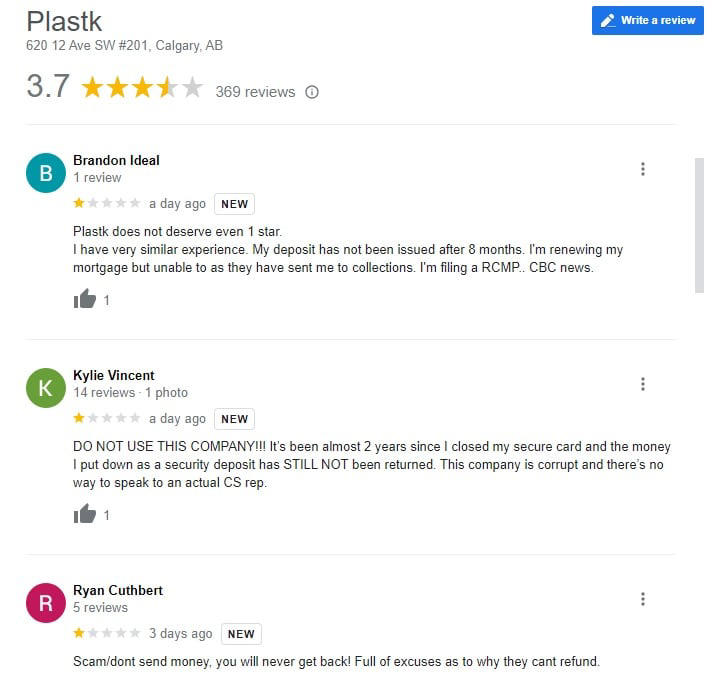

This screen grab of Google reviews, taken on June 7, shows a few of the many online complaints from Plastk customers who say they are waiting for refunds. (Google)© Provided by cbc.ca

On Nov 4, 2021, Omobamiduro pleaded guilty and was convicted under Alberta's Consumer Protection Act for not paying off liens on trade-in vehicle sales, leaving his customers with the debt.

Go Public spoke with two former customers, who say that ruined their credit scores.

Omobamiduro says he had nothing to do with failing to pay off the liens; that it was the fault of an employee in B.C.

"It was an employee that did the deal. The partner should have flagged it and stopped it. Unfortunately it went through and as a consequence, you know, I took responsibility," he said.

Omobamiduro was ordered to pay a total of $22,993 in restitution to his auto sale customers.

McCall says, had she known about the conviction, she wouldn't have signed up for a Plastk Visa.

Go Public interviewed McCall at her home in Edmonton, where she's had trouble making rent because of the delay getting her refund. (Sam Martin/CBC)© Provided by cbc.ca

"I would have never put my own money into this person's company."

As for DC Bank, it says it's not part of customers' credit agreements with Plastk.

"Plastk is the sole party responsible for this situation," it said in a statement emailed to Go Public.

Visa Canada also isn't taking responsibility, saying through a spokesperson that financial institutions that use the its network are "accountable" to their customers and for their business practices.

McCall says she didn't know where to turn — the entire ordeal was "mind boggling."

Go Public looked into it and found a complicated web of government departments, who say they can't help and instead point consumers elsewhere.

Service Alberta and Red Tape Reduction is the regulatory authority responsible for Plastk's secured credit card.

But when Go Public asked if it received any consumer complaints involving the company, or whether the agency has taken any action on behalf of consumers it didn't answer the questions.

"One thing that's missing is a clear path for consumers when they have an issue [with non-bank secured credit cards]," said Henderson, the finance expert.

"At the provincial level, there could be more resources put into more proactive enforcement of those rules that are in place to protect consumers. I think there's also scope to strengthen those rules and regulations… all Canadians deserve access to a safe and affordable credit card."

Getting her money back was "a huge relief," McCall said. "I can pay all the people I owe and my bank credit card off. I am still broke but I owe no one."

Meanwhile, Omobamiduro says he is working on another deal, planning to move his credit card company over to another sponsoring bank.

Story by Rosa Marchitelli • Yesterday

Constance McCall can't catch a break.

The Edmonton woman needed to fix her credit score after getting divorced, so she signed up for a secured credit card that promised to help her do that.

Instead, she's out thousands of dollars, and left with a credit score that's worse than when she started.

McCall, 59, is one of many cardholders stuck in the middle of a bitter legal battle between the credit card company and the bank it partnered with, Calgary-based Digital Commerce Bank, also called DC Bank.

She signed up for the Visa through Plastk Financial & Rewards after seeing it recommended on Credit Karma, a website she trusted.

Plastk promises cardholders the chance to improve their credit scores by reporting their transactions to the credit bureau Equifax.

As a secured card, the credit limit matches whatever customers prepay for a security deposit — between $300 and $10,000.

Plastk founder and CEO Motola Omobamiduro launched his company in October 2020, and partnered with Calgary-based Digital Commerce Bank. (Jenn Blair/CBC)© Provided by cbc.ca

Plastk says customers can cancel any time and get their deposit back after a two-month holding period if the account is in good standing.

After cancelling in December, McCall was expecting $4,500 to be returned in February. Without it, she's had to borrow from family and friends to pay for the basics.

"It was extremely humbling — $4,500 is not a little amount of money, especially for someone like myself. It's huge," she said.

"That was going to pay my next two months' rent, buy my food."

After Go Public brought McCall's case to the company's attention, Plastk refunded her entire deposit — four months after she was supposed to get it back.

Plastk has 7,000 customers across Canada. Go Public spoke to a dozen — hundreds more have posted complaints online — who say they too are out hundreds or thousands of dollars.

Gail Henderson, an expert in consumer finance, says consumers who use secured credit cards backed by non-bank lenders need to be better protected.

Credit cards backed by bank lenders are heavily regulated by the federal Financial Consumer Agency of Canada (FCAC), she says, but cards offered by organizations that are not banks — such as Plastk — have fewer regulations and are overseen by general provincial consumer protection branches.

The FCAC warns consumers to "be careful when applying for a secured card from an unknown financial institution," and recommends checking with the institution to make sure security deposits are insured.

The agency says, in a report published in June, that non-bank consumer complaints about financial products and services have a much lower rate of resolution than those about banks.

Gail Henderson, an associate professor in the Faculty of Law at Queen’s University, is an expert in consumer finance. (Alexis Raymon/CBC)© Provided by cbc.ca

The FCAC report also said most surveyed Canadians don't understand that financial products not backed by banks have less consumer protection.

It suggested that oversight of non-bank products and services ought to be brought up to the stricter level of federally regulated banks and credit unions.

Pedro Oliveira of Hamilton cancelled his Plastk card on Feb. 12 and is still waiting for his $1,000 deposit. After failing to get a resolution with Plastk after about 100 days he filed a complaint with the Better Business Bureau, then he turned to the government — and got sent in a circle.

"I reached out to Consumer Protection Ontario," he said, "and they told me to reach out to the Financial Consumer Agency of Canada who told me to reach out to Consumer Protection Ontario."

Brian Kline of Maple Ridge, B.C., never received hiscard from Plastk after he sent a $2,500 deposit. In late October he asked to cancel his card, and is still waiting for his refund.

He too reported to the Better Business Bureau, then DC Bank, which sent him back to Plastk. Then he tried the Ombudsman for Banking Services and Investments, which said the matter isn't under its jurisdiction. He says the Better Business Bureau closed his complaint as unresolved.

DC Bank says the problem with customer refunds is not its responsibility, since it's not part of the credit agreement between Plastk and its customers. (Google maps)© Provided by cbc.ca

"In all honesty, I'm not confident in ever having my hard-earned money lawfully returned to me," he said.

Plastk CEO and founder Motola Omobamiduro says he is trying to pay customers back, but their money is being held up by DC Bank.

Plastk and DC Bank partnered in April 2020. Court documents show their dispute started about two years later when DC Bank said Plastk owed unpaid fees and wasn't providing the required funds for the bank to pay Visa.

Plastk said the bank was unfairly imposing new rules and fees and that its technology didn't always work — limiting Plastk's ability to do business.

Plastk sued for $5 million in January, and DC Bank counter-sued for $3.8 million a few weeks later.

McCall says the real shock was finding out the businessman behind Plastk is a former used car salesman with a conviction for breaking a consumer protection law.

This screen grab of Google reviews, taken on June 7, shows a few of the many online complaints from Plastk customers who say they are waiting for refunds. (Google)© Provided by cbc.ca

On Nov 4, 2021, Omobamiduro pleaded guilty and was convicted under Alberta's Consumer Protection Act for not paying off liens on trade-in vehicle sales, leaving his customers with the debt.

Go Public spoke with two former customers, who say that ruined their credit scores.

Omobamiduro says he had nothing to do with failing to pay off the liens; that it was the fault of an employee in B.C.

"It was an employee that did the deal. The partner should have flagged it and stopped it. Unfortunately it went through and as a consequence, you know, I took responsibility," he said.

Omobamiduro was ordered to pay a total of $22,993 in restitution to his auto sale customers.

McCall says, had she known about the conviction, she wouldn't have signed up for a Plastk Visa.

Go Public interviewed McCall at her home in Edmonton, where she's had trouble making rent because of the delay getting her refund. (Sam Martin/CBC)© Provided by cbc.ca

"I would have never put my own money into this person's company."

As for DC Bank, it says it's not part of customers' credit agreements with Plastk.

"Plastk is the sole party responsible for this situation," it said in a statement emailed to Go Public.

Visa Canada also isn't taking responsibility, saying through a spokesperson that financial institutions that use the its network are "accountable" to their customers and for their business practices.

McCall says she didn't know where to turn — the entire ordeal was "mind boggling."

Go Public looked into it and found a complicated web of government departments, who say they can't help and instead point consumers elsewhere.

Service Alberta and Red Tape Reduction is the regulatory authority responsible for Plastk's secured credit card.

But when Go Public asked if it received any consumer complaints involving the company, or whether the agency has taken any action on behalf of consumers it didn't answer the questions.

"One thing that's missing is a clear path for consumers when they have an issue [with non-bank secured credit cards]," said Henderson, the finance expert.

"At the provincial level, there could be more resources put into more proactive enforcement of those rules that are in place to protect consumers. I think there's also scope to strengthen those rules and regulations… all Canadians deserve access to a safe and affordable credit card."

Getting her money back was "a huge relief," McCall said. "I can pay all the people I owe and my bank credit card off. I am still broke but I owe no one."

Meanwhile, Omobamiduro says he is working on another deal, planning to move his credit card company over to another sponsoring bank.

No comments:

Post a Comment