It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

New battery management system makes electric car batteries safer and more durable

In the EU project Nemo, a research team involving TU Graz has developed new models that make battery management systems significantly more intelligent. They detect damage at an early stage and increase the service life of electric car batteries

Just as an orchestra needs a conductor, a battery management system (BMS) controls the power storage of an electric vehicle. However, up to now the monitoring is only based on the voltages, currents and temperatures of the individual battery cells. Their ageing or possible damage can only be checked externally using complex calculations. In the EU project Nemo, Graz University of Technology (TU Graz), the Vrije Universiteit Brussel and partners from industry have developed intelligent models and algorithms that enable the safety, service life and performance of batteries to be monitored directly in the vehicle’s system.

Avoiding dangers

“The battery management system is an important tool for operating electric vehicles more safely and sustainably,” says Christoph Drießen from the Vehicle Safety Institute at TU Graz. “If we recognise faults and damage to individual battery cells at an early stage via the BMS, many dangers can be avoided. And thanks to the monitoring of the ageing process of each individual cell, their service life can also be extended substantially through intelligent control.”

The team at the Vehicle Safety Institute at TU Graz focused primarily on the safety aspects of the batteries. To this end, the researchers at the institute’s Battery Safety Center examined battery cells that were mechanically deformed, for example to simulate parking damage. They used this laboratory data to train models and algorithms they had developed themselves so that the BMS can recognise damage independently and indicate when maintenance is required. In order to obtain the necessary data from inside the cell, the team is using new sensor technology known as electrochemical impedance spectroscopy (EIS), which measures the electrical resistance inside the cells in the vehicle.

Internal findings on ageing

In addition, the Graz researchers developed a model that predicts the change in physical volume of the cells during charging and discharging. As excessive expansion increases the mechanical pressure in the battery pack and can lead to cracks and deformations, this model helps to minimise the risk of internal short circuits and thermal peaks.

The algorithms and models pertaining to service life and ageing were developed at the Vrije Universiteit Brussel. Their implementation in the BMS offers clear advantages over previous models or external checks. “Up to now, a test only showed how much the capacity has decreased compared to the original battery condition,” says Christoph Drießen. “But the new models also give us an insight into the changes within the cells as they age. This enables adjustments that are beneficial for performance, service life and safety.”

Demonstrator as a model for series production

Despite the numerous new functions, the enhanced BMS would not be significantly larger or heavier than before. For the additional EIS measurements, however, additional sensors and a correspondingly adapted integration into the BMS are required.

In order to further demonstrate the developed technologies, a follow-up project will work on their continued development and transfer towards industrial application. A demonstrator at module level has already been set up for this in the current project.

The project was Co-funded by the European Union. Additional funding came from the Swiss State Secretariat for Education, Research and Innovation. In addition to TU Graz and the Vrije Universiteit Brussel, Infineon Technologies Austria, Ingenieurgesellschaft Auto und Verkehr (IAV) and the Centre Suisse d’Electronique et de Microtechnique (CSEM) were on board as hardware and software providers as well as TTTech for the cloud implementation and ICONS as partners.

As part of the development of the battery management system, battery cells were subjected to a number of tests.

As part of the development of the battery management system, battery cells were subjected to a number of tests.

Development of a P2D-based model for battery swelling prediction under mechanical constraints

Sunday, June 21, 2026

New battery management system makes electric car batteries safer and more durable

In the EU project Nemo, a research team involving TU Graz has developed new models that make battery management systems significantly more intelligent. They detect damage at an early stage and increase the service life of electric car batteries

Just as an orchestra needs a conductor, a battery management system (BMS) controls the power storage of an electric vehicle. However, up to now the monitoring is only based on the voltages, currents and temperatures of the individual battery cells. Their ageing or possible damage can only be checked externally using complex calculations. In the EU project Nemo, Graz University of Technology (TU Graz), the Vrije Universiteit Brussel and partners from industry have developed intelligent models and algorithms that enable the safety, service life and performance of batteries to be monitored directly in the vehicle’s system.

Avoiding dangers

“The battery management system is an important tool for operating electric vehicles more safely and sustainably,” says Christoph Drießen from the Vehicle Safety Institute at TU Graz. “If we recognise faults and damage to individual battery cells at an early stage via the BMS, many dangers can be avoided. And thanks to the monitoring of the ageing process of each individual cell, their service life can also be extended substantially through intelligent control.”

The team at the Vehicle Safety Institute at TU Graz focused primarily on the safety aspects of the batteries. To this end, the researchers at the institute’s Battery Safety Center examined battery cells that were mechanically deformed, for example to simulate parking damage. They used this laboratory data to train models and algorithms they had developed themselves so that the BMS can recognise damage independently and indicate when maintenance is required. In order to obtain the necessary data from inside the cell, the team is using new sensor technology known as electrochemical impedance spectroscopy (EIS), which measures the electrical resistance inside the cells in the vehicle.

Internal findings on ageing

In addition, the Graz researchers developed a model that predicts the change in physical volume of the cells during charging and discharging. As excessive expansion increases the mechanical pressure in the battery pack and can lead to cracks and deformations, this model helps to minimise the risk of internal short circuits and thermal peaks.

The algorithms and models pertaining to service life and ageing were developed at the Vrije Universiteit Brussel. Their implementation in the BMS offers clear advantages over previous models or external checks. “Up to now, a test only showed how much the capacity has decreased compared to the original battery condition,” says Christoph Drießen. “But the new models also give us an insight into the changes within the cells as they age. This enables adjustments that are beneficial for performance, service life and safety.”

Demonstrator as a model for series production

Despite the numerous new functions, the enhanced BMS would not be significantly larger or heavier than before. For the additional EIS measurements, however, additional sensors and a correspondingly adapted integration into the BMS are required.

In order to further demonstrate the developed technologies, a follow-up project will work on their continued development and transfer towards industrial application. A demonstrator at module level has already been set up for this in the current project.

The project was Co-funded by the European Union. Additional funding came from the Swiss State Secretariat for Education, Research and Innovation. In addition to TU Graz and the Vrije Universiteit Brussel, Infineon Technologies Austria, Ingenieurgesellschaft Auto und Verkehr (IAV) and the Centre Suisse d’Electronique et de Microtechnique (CSEM) were on board as hardware and software providers as well as TTTech for the cloud implementation and ICONS as partners.

As part of the development of the battery management system, battery cells were subjected to a number of tests.

As part of the development of the battery management system, battery cells were subjected to a number of tests.

PARIS -- Artificial intelligence will lead to labour shortages, not the replacement of humans, Amazon founder Jeff Bezos predicted in a highly optimistic appearance at the VivaTech technology conference in Paris on Wednesday.

Bezos put forward a rosy vision of how technology will help humanity, speaking about projects including his space venture Blue Origin and his new AI startup Prometheus, which is aimed at speeding up physical manufacturing.

“I know there’s a lot of concern that many people have, including many smart people, that AI is going to make humans redundant and so on,” Bezos said. “I totally disagree with this point of view. And I think, in fact, AI is going to create a labour shortage.”

The comments come when global companies cut thousands of jobs after investing heavily in AI, with many, primarily tech firms, pointing to higher efficiencies from the technology’s rapid adoption.

U.S.-based employers announced 97,006 job cuts in May with AI linked to 40 per cent of the layoffs, according to a report from global outplacement firm Challenger, Gray and Christmas.

Half of Americans fear the rise of AI could put them or someone in their household out of work, a Reuters/Ipsos poll found this month.

From Gen Z entering the job market to unions at South Korean carmakers and Hollywood scriptwriters, there has been a widespread pushback against AI use.

Bezos, the world’s fourth-richest person with a net worth around US$250 billion, argued that people have “endless” things to do, and are currently limited by barriers that he said AI would lower.

Amazon, too, has trimmed some 30,000 corporate roles since late last year, partly due to AI efficiency gains. Its CEO Andy Jassy had previously said increasing automation through AI tools would result in corporate job losses.

Bezos’ space focus

One goal of space exploration is to move polluting industries off Earth, said Bezos, whose Blue Origin aims to compete with trillionaire Elon Musk’s SpaceX in rockets.

“If space travel gets reliable enough and inexpensive enough, and we can get materials from asteroids and near-Earth objects and the moon, then this garden planet can be returned to its pre-Industrial Revolution state,” Bezos said.

Amazon founder Jeff Bezos speaks at the Vivatech fair in Paris, Wednesday, June 17, 2026. (AP Photo/Emma Da Silva)

Appearing together with Bezos was Blue Origin CEO David Limp, who said reconstruction of the firm’s launch pad for New Glenn rockets has begun in Florida following a dramatic explosion in May.

Musk has also put forward a lofty vision for space ahead of last week’s SpaceX IPO, including plans to create cities on the moon and Mars. In an interview with JPMorgan CEO Jamie Dimon last week, he talked about firing AI data centres into space and having vacations on the moon.

(Reporting by Gianluca Lo Nostro, Toby Sterling and Louise Heavens; Additional reporting by Deborah Sophia; Editing by Peter Graff and Shilpi Majumdar)

Nvidia’s Jensen Huang says society needs ‘new social norms’ in the age of AI: AP Exclusive

SHERMAN, Texas — Nvidia CEO Jensen Huang — whose work helped enable artificial intelligence — stressed in an Associated Press interview Tuesday that society has no choice but to change in the advent of AI.

Huang has been optimistic about the technology’s potential to rapidly change society, creating faster economic growth and more scientific breakthroughs. But as the head of a computer chip company now developing AI systems, Huang has felt obligated to respond to critics who warn of job losses and threats to humanity itself.

“We need to create new social norms,” Huang said in an interview. “I would advocate that everybody use AI. Just go engage it.”

He said the ability of AI to build a website, analyze complex documents, guide advanced research or even plan a kitchen remodeling has helped to close the technological divide in America. People can now do advanced work on computers without having to know how to program or write software, he added.

Huang stressed that there is a need for government regulation and safety standards for AI, emphasizing that national security also needed to be a priority for the technology that has been powering stock market gains and much of the U.S. economy in recent years.

The head of the world’s most valuable company said society will adapt to AI just as it did to automobiles. He said cars were once portrayed as killing children, but the world changed its norms by having sidewalks and crosswalks and stopping kids from playing in the streets.

“When I was growing up, I used to play in the streets,” Huang said. “When cars came along, you obviously can’t play in the streets now.”

---

Josh Boak, The Associated Press

Israeli AI company Artlist to lay off 200 of its 500 workers

Israeli AI stock catalogue company Artlist confirmed that it would lay off 200 of its 500 employees in what has been categorised as a strategic move.

This forms part of a broader crunch that has impacted tech companies in Israel. In late May, AI21 Labs decided to lay off 110 of its 180 employees. Still, the financial pressures stemming from the Iran war have affected Israeli companies across the board, with Teva Pharmaceutical Industries announcing plans to cut approximately 250 jobs across its TAPI (Teva Active Pharmaceutical Ingredients) division over the next two years.

Artlist said in a press release that the reorganisation forms part of a broader "strategic reorganisation process in which the company will move to work in an operating model built for AI (AI-Native) with the aim of adapting the company's organisational structure to the new technological era and transforming it into a flat, fast and autonomous organisational structure."

"The process is being implemented from a position of economic resilience and continued growth," the company said, adding that it recently crossed $300mn in annual recurring revenue, growing 50% y/y.

The company said it "will provide a broad support package and favourable conditions" for departing staff, thanking them for their contribution. Affected employees have been summoned for hearings as part of the formal review process covering the approximately 200 roles.

Based in Tel Aviv, Artlist provides music, video, sound effects and templates to influencers, content creators and corporate marketing teams.

The cuts indicate a pattern accelerating across the digital content sector, where AI-generated assets have materially disrupted the market for licensed stock media over the past two years. Platforms that built scale around human-curated libraries are under pressure to restructure cost bases and workflows as generative tools compress both production costs and price points across music, video and visual content.

This trend seems to have strongly impacted the Israeli economy, with a large emphasis being placed on tech start-ups, particularly those in the AI space.

AI data centers are driving a surge in electricity demand, but the technology could also help improve energy efficiency in industry, power systems, and renewable energy operations.

Global energy-efficiency gains have stalled at around 1.3% annually, far below the IEA's target of 4%.

AI's own environmental footprint is growing rapidly, with data centers consuming increasing amounts of electricity and water

The surge of AI and the data center boom have started to pose challenges to the global energy system amid soaring power demand, spiking energy bills, and a higher environmental footprint.

As much as AI is changing the world and the economy, it could also offer assistance to one of the energy sector’s most pressing needs in times of rising demand, uncertainty in fossil fuel supply, and inflationary and supply-chain pressures in the renewables industry—energy efficiency.

AI could be the tool to help unlock additional energy gains and accelerate progress in efficiency, which has been slow in recent years. The advance of AI itself could be a leap toward energy efficiency, as data center developers will have to offset the negative image of drawing power and water resources from communities.

With increasingly stronger NIMBY movements to oppose data center locations in rural America and rising energy bills, AI could partly redeem itself by becoming the key enabler of massive progress in energy efficiency.

AI-Assisted Energy Efficiency

“We could be at a moment where we could step up efficiency progress, particularly in industry, unlocked by AI,” Brian Motherway, head of energy efficiency at the International Energy Agency (IEA), told the Financial Times.

At the end of last year, Motherway said that “slow efficiency progress is a wasted opportunity” as the world remains off track for the goal of doubling efficiency improvements to 4% per year by 2030.

Per the latest data from the IEA, rather than increasing towards the 4% goal, global efficiency progress has slowed in recent years. The average annual improvement since 2019 has been only 1.3%, well below the 2% starting point for the doubling goal.

In some regions, accelerating electricity demand growth has led to an overall increase in less efficient power generation, while increased access to air conditioners has pushed up cooling-related electricity demand, not necessarily with the most efficient air conditioners, Motherway argued.

In addition, policies have lagged progress in technology, “leaving significant savings on the table,” the official said.

While improved energy efficiency remains one of the fastest and most cost-effective ways to strengthen energy security, lower costs, and reduce emissions, it hasn’t lived up to expectations or to the IEA’s goals.

No one questions AI’s capabilities to be much more efficient than humans in recognizing where the wasted energy is, especially in industrial applications.

For example, renewable energy companies that have invested in AI and digital twin solutions could see huge benefits in their efficient operations, a 2025 study published in Energy Reports showed. The use of digital twin technology in renewable energy systems, combined with AI, boosts predictive maintenance efficiency. This reduces unplanned downtime by 35%, raises energy production by 8.5%, and reduces energy costs by 26.2%, according to the study by researchers at French and Moroccan universities.

Still, challenges to making AI mainstream in energy production, distribution, and transmission remain, “including high implementation costs, cybersecurity risks, and the complexity of integration,” the scientists noted.

To have AI-enabled efficiency gains, companies would need to invest in upgrades of equipment that would be expensive and often tailor-made, according to analysts.

“Companies need to go factory by factory investing in bits of kit that are often bespoke,” Sam Kimmins, director of energy at the non-profit Climate Group, told FT.

Efficiencies Cannot Offset AI Power Demand Surge

If AI could help accelerate efficiency gains, it could partly compensate for the surge in global power demand. Last year, electricity demand from data centers rose by 17%, and that of AI-focused data centers jumped even faster, soaring by 50%, the IEA said in a report in April. These surges in AI-driven power demand vastly outpaced the 3% growth in global electricity demand.

With the exponential surge in power demand, the AI value chain has seen a scramble for electricity, grid connections, manufacturing capacity, chips, and capital, the agency notes.

AI is not only sucking up energy, but it also uses water and other natural resources, including land.

The United Nations University Institute for Water, Environment and Health (UNU-INWEH) warned in a report earlier this month that by 2030, AI’s water use will match the needs of 1.3 billion people.

The AI data centers are also projected to consume 945 terawatt-hours of electricity globally by the end of the decade. This would nearly triple the combined annual electricity use of Pakistan, Bangladesh, and Nigeria—countries collectively home to more than 650 million people, the UN scientists say.

“This report is not a case against artificial intelligence, a technological transformation that is improving the lives of billions of people around the world,” said Professor Kaveh Madani, Director of UNU-INWEH, who led the investigation team.

“We have a narrow window to ensure that the backbone of the technological revolution of our era develops within planetary limits, and that the communities who provide the critical minerals for advancing AI and the ones that host its infrastructure and e-waste are also among those who benefit from it.”

By Tsvetana Paraskova for Oilprice.com

How AI Can Support the Evolution of Marine Propulsion

Artificial intelligence (AI) is accelerating marine system innovation, but its value relies on strong engineering governance, structured data and clear processes, writes Tobias Huuva, Engineering Manager, Berg Propulsion

Like other engineers, those focusing on marine propulsion find AI and machine learning (ML) increasingly useful for enhancing productivity and consistency in documentation, as well as enabling data-driven decisions over the system lifecycle. But as also experienced elsewhere, the extent of this usefulness depends on applying these tools with a clear engineering purpose

This is because the real “enabler” is not the algorithms themselves, but remains the foundation of well-organised data, clearly defined workflows, and experienced engineers who understand both the problem and the tools. At Berg Propulsion, we treat AI strictly as an addition to established engineering practices—not a replacement.

Traditional engineering methods remain central to propulsion system design. Experienced engineers are always responsible for final decisions, and their judgement is essential. Developing propulsion systems is a multidisciplinary endeavour, involving hydrodynamics, mechanical design, electrical integration, and validation work such as sea trials.

Propeller design alone involves analysing vessel characteristics and operating profiles, running simulations, and carrying out model tests, all of which are time-intensive processes.

Supporting the engineering workflow

Today’s AI and ML tools are mature enough to support these processes without disrupting them. Used correctly, they can ease bottlenecks in the workflow, particularly where large volumes of data need to be handled quickly. However, it remains critical that engineers review and validate all AI-supported results.

And it is long experience in hydrodynamics and propulsion technology, covering solutions ranging from controllable-pitch propellers to complete propulsion systems, that puts Berg in the position to harvest full value of these new tools.

Many of our applications, such as tugboats, place very high demands on aspects of performance that serve different ends. Requirements like bollard pull, fast thrust response, precise low-speed control, and energy efficiency all need to be balanced.

AI is helping Berg Propulsion engineers overcome the heavy workload and repetitive data-processing tasks they face in documentation, software programming, analysis, and design evaluation - allowing them instead to focus more on critical thinking.

Using the right tools in the right way

Different AI tools are also used for serve different purposes, and can be used individually or in combination.

Machine learning models, for example, are well suited for approximating relationships between propeller geometry, operating conditions, and performance metrics such as efficiency, thrust, cavitation, and noise. Once trained, these models can provide rapid performance predictions that support early-stage design decision-making.

Large Language Models (LLMs), on the other hand, are most useful for text-based work—drafting reports, reviewing documentation, and ensuring consistent terminology. These tasks often take up a significant amount of engineering time, and automation here allows engineers to stay focused on analysis and decision-making.

At Berg Propulsion, we are also working on agent-based solutions that combine LLMs with controlled access to internal data. These systems can retrieve approved templates, historical project data, and technical information while respecting governance rules. They can also respond to internal technical questions, support regulatory interpretation, and help prepare documentation tailored to specific customers.

For more advanced hydrodynamic work, graph neural networks (GNNs) offer interesting possibilities. By representing geometry and flow behaviour as interconnected structures, they can capture complex spatial relationships that are difficult to model with traditional regression-based methods. These tools are not intended to replace high-fidelity simulations but to complement them with quicker insights.

Active learning models provide another approach which offers promise for shortening propeller optimisation analysis. Instead of relying on predetermined algorithms and large numbers of simulations - as in traditional optimisation methods - it uses adaptive models that improve over time. This allows engineers to explore design alternatives more efficiently and reduce development time.

Digital twins add another layer of value. By combining sensor data with simulation models, they benefit performance monitoring, fault detection, and predictive maintenance. In addition, operational data from real vessels can be fed back into the design process, benefiting understanding in future product development.

The importance of governance

As AI technologies evolve, they will become increasingly integrated into engineering work. In marine propulsion, as elsewhere, they can strengthen efficiency, consistency, and sustainability - but only if they are implemented carefully.

In the first instance, as a principle, use should be made of these tools in supporting roles before they are adopted for decision-related tasks. Therefore, strong governance is essential throughout the engineering process - with data always verified as reliable, problems clear and defined, assumptions transparent, and results properly validated

Ultimately, AI is a powerful addition to the engineering toolbox—but its value depends on how well it is integrated with existing knowledge, processes, and expertise.

Tobias Huuva is the Engineering Manager at Berg Propulsion.

The opinions expressed herein are the author's and not necessarily those of The Maritime Executive.

If you've been investing in the AI boom, you probably own most of the same names everyone else does.

NVIDIA for the chips. Microsoft, Google and Amazon for the cloud. Maybe Meta for the consumer side. Maybe Palantir or one of the AI software names. Possibly TSMC for exposure to the manufacturing layer.

And that playbook has worked well for investors. NVIDIA alone has minted more wealth in two years than most companies create in a century. The hyperscalers have all hit fresh highs. AI software stocks that were speculative bets in 2022 now trade at premium multiples.

But every smart investor should be asking the same question right now. With most of these names sitting at or near all-time highs, where does the next leg of returns come from?

The answer won’t come from the obvious places. The chip trade, the cloud trade and the software trade have already been priced. To find the kind of returns that actually move the needle in 2026, you have to look one layer beneath the names everyone is talking about. You have to look at what makes all of it possible.

One company well positioned for what's coming is one most investors have never heard of. It's called Bitzero Holdings, Inc. (NASDAQ: AIBZ), and to understand why it matters, you need to understand the bottleneck nobody is talking about yet.

The Question Wall Street Forgot to Ask

Every company in the AI economy depends on one thing. NVIDIA's chips are useless without it. Microsoft's data centers are concrete shells without it. Google's models can't train without it. The entire industry runs on one input that almost nobody talks about.

Electricity.

And there isn't enough of it.

A single ChatGPT query consumes roughly 10 times the energy of a Google search. Training the next generation of large language models requires the equivalent power draw of small cities. Industry forecasts now put AI data center capital expenditure at roughly $5.2 trillion between now and 2030. Goldman Sachs Research projects global data center power demand will surge up to 165% by 2030 compared to 2023 levels.

The grid was not built for this. It was built for a world where electricity demand grew at 1-2% per year, predictably, with decades of warning. Now hyperscalers are showing up at utility offices asking for hundreds of megawatts on three-year timelines. The answer keeps coming back the same: we can't deliver it.

Read that again. Half of the projects on the books, projects backed by some of the deepest pockets in corporate America, will not happen. Not for lack of money or demand. The grid simply cannot deliver the power.

This is the bottleneck Wall Street has not priced in yet.

The Hyperscalers Already Know

If you want confirmation that power is the real constraint, look at what the smart money is doing.

These are not the moves of companies that think power will sort itself out. They are willing to commit billions and wait years to lock in scarce, secured, low-carbon electricity because they know that power is the binding constraint on their entire AI strategy.

Now ask yourself the obvious follow-up. If Microsoft is willing to restart a dormant nuclear plant to get power, what would it pay for power that already exists, already runs on 100% renewable energy and sits in a jurisdiction with EU data sovereignty protections?

The Nordic Advantage Most Investors Don't Know About

While American hyperscalers negotiate with utilities and wait on regulators, a different set of conditions exists across the Atlantic.

The Nordic countries (Norway, Finland, Sweden) sit on top of an abundance of hydroelectric and nuclear power, in cold climates that dramatically reduce the cooling costs for data centers, with stable governments and EU data protections built in. For AI workloads, this combination is close to perfect.

The catch is that almost none of that capacity is available to new entrants anymore. Norway has effectively closed the door, capping new operators at just 5 megawatts of initial allocation. Finland and Sweden are tightening as well. The companies that locked in Nordic power before the AI boom kicked into high gear are now sitting on something that cannot be replicated, no matter how much capital is thrown at it. The window is closed.

And one of those companies should be on your radar.

Bitzero Holdings: The Standout Play in a Closed Market

Bitzero Holdings, Inc. (NASDAQ: AIBZ) is one of the very few companies that locked in Nordic power capacity ahead of the surge. The story of how it did so explains why this stock is one of the rare chances to own real AI infrastructure before Wall Street catches on.

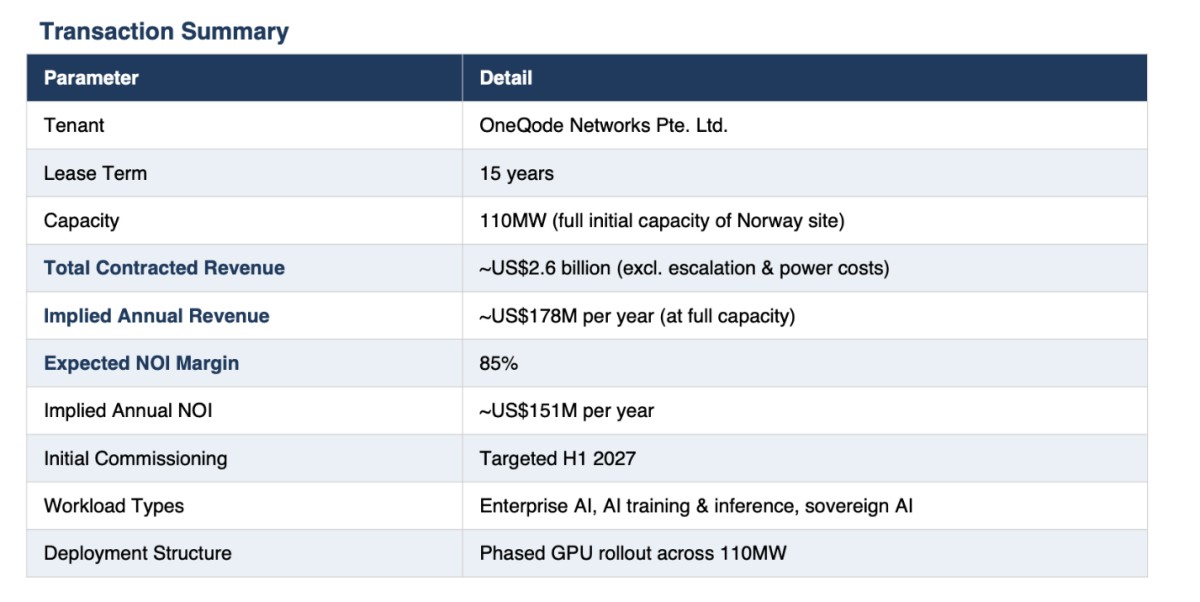

Bitzero controls more than 1 gigawatt of secured, low-cost power capacity across four strategic sites in Norway, Finland and the United States. That capacity is permitted, contracted and in many cases already operational. The largest single block of that capacity, the 110 megawatts at the company's Norwegian flagship, is now under a binding 15-year lease worth approximately $2.6 billion. More on that in a moment.

The crown jewel is the company's Norwegian flagship at Namsskogan, where Bitzero operates as a licensed grid operator at the 132 KV level. That's an unusual position. It is also an extraordinarily valuable one.

Most data center operators connect at 22 KV through a utility, paying middleman fees and waiting on utility timelines. Bitzero connects directly to the high-voltage grid and works directly with hydroelectric power plants, bypassing the middlemen and multi-year utility wait that hold most projects back.

The financial impact is dramatic. Bitzero's all-in power cost at its Norway facility, including grid fees, taxes and every other charge, currently sits at 3-4 cents per kilowatt-hour. The US average is closer to 12 cents. American data center operators competing for AI workloads are paying three to four times what Bitzero pays for the same electron.

The Deals That Changed What This Company Is

Three months ago, Bitzero looked like a small Bitcoin miner with an unusually good power position. Today it looks like something different entirely.

The transformation comes down to four announcements, all landing inside a single rolling window.

The biggest by far is OneQode. On May 5, 2026, Bitzero signed a binding letter with OneQode Networks Pte. Ltd. for a 15-year lease of the full 110 megawatts at its Namsskogan, Norway site. Total contracted revenue runs approximately $2.6 billion, with implied annual revenue of $178 million at full capacity and a net operating margin of 85%. The tenant is deploying GPU clusters for enterprise AI, large language model training and sovereign AI workloads. Commissioning is targeted for the first half of 2027, with the lease then running through 2042 at minimum. The buildout to convert the site to HPC-grade specifications runs roughly $1.1 billion, with debt financing in late-stage negotiation. The deal is subject to definitive documentation, which management has indicated could close within the next 60 to 90 days.

On a per-megawatt basis, the OneQode deal lines up with the comparable HPC leases driving the multi-billion dollar valuations of larger peers. TeraWulf sits on $12.8 billion in contracted HPC revenue. Hut 8 signed a $7 billion, 15-year lease with Fluidstack for 245 megawatts. Core Scientific signed a $10.2 billion deal with CoreWeave across roughly 500 megawatts. Each of those announcements rerated the company's stock substantially.\

The other three announcements build on the OneQode foundation.

When Microsoft, Google or Amazon needs to evaluate AI-ready capacity in Europe, CBRE is one of the first calls they make. With Norway under contract to OneQode, Finland becomes the next available block of AI-ready capacity in the Bitzero portfolio.

Hydra Host operates GPU clusters across more than 50 locations worldwide and brings Bitzero's compute capacity to a global enterprise customer base through its Brokkr platform. A few days later, Bitzero acquired its first eight NVIDIA Blackwell B300 servers (64 GPUs total) for deployment at the Norway site, marking the company's first direct entry into AI compute revenue.

Four announcements. One contracted long-term tenant worth $2.6 billion, one global brokerage marketing the next site to hyperscalers, one NVIDIA Cloud Partner distributing capacity to global enterprise customers, and the latest generation of NVIDIA chips already deployed. The company that exists today is fundamentally different from the company that existed 90 days ago.

Already Profitable…And Just Getting Started

The part that separates Bitzero from most early-stage infrastructure plays is simple. The company is not burning capital while it waits for AI deals to close. It is generating revenue today.

Bitzero mines Bitcoin at its Norway site at a blended power cost of approximately $0.03 to $0.035 per kWh. The all-in cost to mine one Bitcoin sits around $50,000, roughly half the industry average of $100,000. The company's hashrate has grown steadily from 0.4 EH/s in early 2024 to 1.08 EH/s by January 2025 to roughly 2.80 EH/s today, a 7x increase in two years. At current network conditions that's around 1.1 Bitcoin per day in production.

That revenue funds operations and demonstrates infrastructure reliability under sustained, real-world high-load conditions. AI customers want to see exactly that before signing multi-year hosting agreements.

The 110 megawatts at Namsskogan are now committed to OneQode under the 15-year lease, with HPC commissioning targeted for the first half of 2027. The growth runway extends well beyond that initial block. Bitzero has a clear path to approximately 325 megawatts at the same site by late 2027, with the largest infrastructure components, including a Siemens GIS breaker with 200 megawatt capacity, already paid for and installed. Whatever capacity does not flow to OneQode in later phases becomes available for either additional HPC tenants or expanded mining.

The Valuation Gap Is About to Close

Bitzero's pro forma revenue profile, once the OneQode lease commences, would put it in the same conversation as the Bitcoin mining and HPC infrastructure names already trading at multi-billion dollar market caps.

IREN Limited (Nasdaq: IREN) trades at a market cap above $21.75 billion. TeraWulf Inc. (Nasdaq: WULF) sits above $13 billion. Cipher Mining (Nasdaq: CIFR) is north of $10 billion. Hut 8 (Nasdaq: HUT) and Core Scientific (Nasdaq: CORZ) both trade above $8 billion. Each of these companies has built its valuation on the same thesis Bitzero is now executing: owned power infrastructure plus a credible long-duration HPC contract.

The broader data-center industry is reaching the same conclusion. Equinix (NASDAQ:EQIX), the world's largest colocation data-center operator, continues to expand aggressively across North America, Europe, and Asia, but has repeatedly highlighted power availability as one of the primary constraints on future growth. Digital Realty (NASDAQ:DLR), another global data-center giant with more than 300 facilities worldwide, is increasingly prioritizing campuses with existing grid access and long-term power visibility as AI customers demand ever-larger deployments. Meanwhile, Oracle (NASDAQ:ORCL) has emerged as one of the fastest-growing AI infrastructure providers through its cloud partnership with OpenAI and Stargate, forcing the company into a global hunt for energized capacity to support its next generation of AI workloads.

What is notable is that all three companies have access to vast amounts of capital. The challenge is no longer financing data centers—it is securing electricity. Across the industry, the conversation has shifted from "Where can we build?" to "Where can we get power?" As AI demand accelerates, companies that already control gigawatt-scale energy infrastructure are increasingly becoming strategic assets in their own right. In many markets, access to power is now more valuable than access to land, and that dynamic is reshaping how investors evaluate AI infrastructure opportunities.

Bitzero currently trades at a market cap of roughly $300 million.

A company with more than 1 gigawatt of secured capacity across four sites, a 15-year $2.6 billion AI lease signed with OneQode, profitable Bitcoin mining operations, CBRE marketing the Finland site to hyperscalers and NVIDIA Blackwell GPUs deploying in Norway trades at roughly 1% of IREN's market cap.

The company has raised approximately $100 million in capital to date, including roughly $75 million in equity and $25 million in debt. Phoenix Group, the publicly-listed Bitcoin miner ranked tenth globally by market capitalization, holds a 20.8% equity stake in Bitzero and a board seat. Kevin O'Leary is on the cap table. The proposed board includes investment banking veterans from Credit Suisse and JPMorgan.

The CSE listing has kept Bitzero off the radar of most US institutional money. The Nasdaq application changes that. The OneQode deal changes that. Once both confirm, the structural discount typical of small Canadian-listed names should compress quickly.

The Bottom Line

The AI boom is real and it is going to continue. But the names everyone has been buying are largely priced for the next several years of growth.

The smartest way to play the boom from here is to get in front of the constraint nobody is fully pricing yet. That constraint is power.

The hyperscalers know it, which is why they are restarting nuclear plants and signing 20-year contracts. Wall Street has not fully connected the dots yet, though it is now starting to.

Bitzero owns the asset every AI dollar eventually has to flow through, and it just signed a 15-year, $2.6 billion contract that proves the asset has buyers. The company generates profitable revenue today through Bitcoin mining, has CBRE marketing its Finland site to hyperscalers, has Hydra Host distributing its compute capacity globally and has the latest generation of NVIDIA Blackwell GPUs already deployed in Norway.

The valuation gap will not last. The window to position before the institutional crowd is open right now.