It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Thursday, September 04, 2025

Column: China feels the ripple effect of US copper tariff trade

China’s net imports of refined copper dropped to a one-year low in July as the world’s largest buyer found itself in competition with the US for metal.

The scramble to ship copper to the US ahead of threatened tariffs, deferred for now, extended to China’s bonded warehouse stocks.

China “exported” 121,000 metric tons of copper to the US in the first seven months of 2025. The shipments started after President Donald Trump announced a national security investigation into US copper import dependency in February.

However, since US customs counted in only 15 tons of refined Chinese copper over the first half of 2025, it’s clear that China’s “exports” were actually re-exports of previously imported non-Chinese metal.

The drain on bonded inventory has stimulated China’s own import appetite but the country has had to diversify its supply base to compensate for the US pull on refined copper.

China’s trade in refined copper

Record flows

China’s outbound shipments of refined copper totaled 426,000 tons in the January-July period, already higher than any previous calendar year with the exception of last year’s 458,000 tons.

The mid-year export spike in 2024 was caused by a short squeeze on the CME contract which resulted in the US premium over the London Metal Exchange (LME) price widening to what was then an unprecedented $1,100 per ton in May.

Chinese smelters made hay from the global pricing disconnect by shipping metal to LME warehouses in Taiwan and South Korea.

LME holdings of Chinese copper amounted to just 400 tons in February 2024. By August they had mushroomed to 164,000 tons.

It was, with hindsight, a dry run for this year’s even greater tariff disconnect.

The CME premium to the LME stretched to almost $3,000 in July before collapsing in August, when the US administration confirmed tariffs on copper products but pushed back a decision on refined copper until next year.

Chinese smelters have once again shipped metal to the LME, where registered stocks of Chinese copper jumped from 25,000 tons to 98,000 tons over the course of July.

The turnaround of metal in Chinese bonded warehouses has also been complemented by higher outright exports to Thailand and Vietnam. Neither country hosts LME warehouses, suggesting China has been plugging supply-chain gaps opened up by the scramble to get the right sort of copper for US delivery.

China’s refined copper imports by major supplier

Chilean diversion

CME’s list of deliverable brands is largely limited to domestic and South American brands, Chilean in particular.

US imports of Chilean copper exceeded 500,000 tons in the first half of the year, compared with 650,000 tons over calendar 2024.

Much of that extra metal was stripped out of LME warehouses and Chinese bonded stocks as well as the physical supply chain.

It’s noticeable that China’s imports of Chilean copper have cratered since the tariff trade started.

Arrivals of Chilean metal fell below 20,000 tons in both June and July for the first time since 2006. The year-to-date tally of 203,000 tons is down by almost half on the same period of 2024.

Chinese buyers have turned to the Democratic Republic of Congo, Russia and Zambia to compensate for the loss of Chilean copper.

The Congo has emerged as China’s main refined copper supplier over the last couple of years and that position has been cemented this year with cumulative imports of almost 820,000 tons in the January-July period.

Russia has long been a major import source for Chinese buyers, but the pace of arrivals has accelerated significantly this year.

Monthly imports of Russian copper are now regularly exceeding those from Chile and cumulative January-July arrivals of 269,000 tons were up by 123% on last year.

China’s imports of Zambian metal have also more than doubled to 95,000 tons as buyers look for alternative non-Chilean material.

Import appetite

The scale of China’s exports and re-exports masks the country’s continued hunger for refined copper.

Imports were 2.2 million tons in the first seven months of 2025, closely tracking last year’s levels.

Indeed, China’s import appetite seems to have grown stronger over the last couple of months in reaction to the combination of lower port stocks and direct smelter sales both to the LME and other Asian consumers.

The country is also facing a shortage of recyclable copper scrap, which means increased demand for refined metal. Imports of scrap fell by 1% in the January-July period relative to last year.

The US has historically been the largest supplier of scrap to China, but the trade has shrunk dramatically this year after China included copper scrap in its reciprocal tariffs on the US.

China’s year-to-date imports of US scrap have slumped by 49% and July’s count of 930 tons was the lowest monthly total in over 20 years.

As with refined copper, Chinese buyers are diversifying by lifting imports from Europe. But this may be only a short-term solution, given that the European Union is actively considering export restrictions on recyclable metal.

The geopolitical dislocation to the refined copper market may be close to running its course after the push-back of US tariffs, but the disruption to global scrap flows may only just have started.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

Ivanhoe Mines (TSX: IVN) announced on Thursday that it has made a copper discovery at its exploration joint venture in Kazakhstan’s Chu-Sarysu Basin, warranting further follow-up.

The Canadian miner, alongside UK-based partner Pallas Resources, is exploring a prospective land package of over 16,000 km², covering licences spread across seven projects. The landholding, according to Ivanhoe, represents one of the largest in Kazakhstan and is estimated to be seven times bigger than its Western Forelands project in the Democratic Republic of the Congo.

The new copper discovery resulted from the joint venture’s fieldwork on the Merke licence, which is located in the southern part of the Chu-Sarysu Basin and includes a 36-kilometre-long stratigraphic trend, with multiple samples returning between 1% and 5% copper.

While clearly not an economic occurrence in isolation, Ivanhoe’s team considers the copper mineralization — an outcrop on surface with an approximate 20-metre thick zone — to be “significant” as it strongly supports the thesis that mineralization is structurally controlled, with faults and fractures acting as conduits for copper-bearing fluids into a package of folded sedimentary carbonate rocks.

The joint venture will now follow up on this discovery by mapping these structures in detail, supported by high-resolution magnetic surveys to trace them at depth, and by evaluating basement contacts and fault systems as potential fluid pathways.

Shares of Ivanhoe declined 3.5% to C$12.02 by noon ET on the news, giving the Vancouver-based copper miner a market capitalization of C$16.22 billion ($11.72bn).

Third-largest basin

The entire Chu-Sarysu Basin, according to Ivanhoe, is ranked as the world’s third-largest sediment-hosted copper basin, after the Central African Copperbelt and European Kupferschiefer, hosting 27 million tonnes of known copper. The area hosts the world-class Dzhezkazgan deposit, which has been continuously mined for over a century.

The United States Geological Survey (USGS) estimates that there remains approximately 25 million tonnes of undiscovered copper in the Basin. Despite its significant prospectivity, greenfield exploration has largely been neglected across the entire region for over 40 years.

Kazakhstan as a whole has also been largely underexplored, even with its geological potential and status as a world-leading producer of uranium. S&P Global estimates that over the past 15 years, only $100 million has been spent annually on exploration in the country, far less than other major mining jurisdictions.

With that in mind, Ivanhoe and privately held Pallas teamed up in late 2024 to explore the 16,000 km² land package in Chu-Sarysu, leveraging the former’s exploration success in Congo and the latter’s experience in Kazakhstan. Ivanhoe is expected to sole-fund up to $18.7 million over the first two years, and can elect to earn into all seven projects under the JV, up to 80%, for a maximum consideration of $115 million over four years.

Drilling underway

Ivanhoe also said that a 15,000-metre drill campaign has commenced in the western section of the joint venture’s land package on the Glubokoe licence, located several hundred kilometres north of the Merke licence.

The first drill hole is expected to test the potential extensions of mineralization first noted in a Soviet-era stratigraphic hole drilled in the 1980s, which intersected three separate copper-bearing intervals over 26 metres, the company said.

The initial drill holes in the 2025 campaign are expected to be between 800 and 1,000 metres deep, and will assist with calibrating the results with historic and newly acquired geophysical datasets. This in turn will inform the stratigraphic and facies models, as well as help identify drill targets for the remainder of drill program, it added.

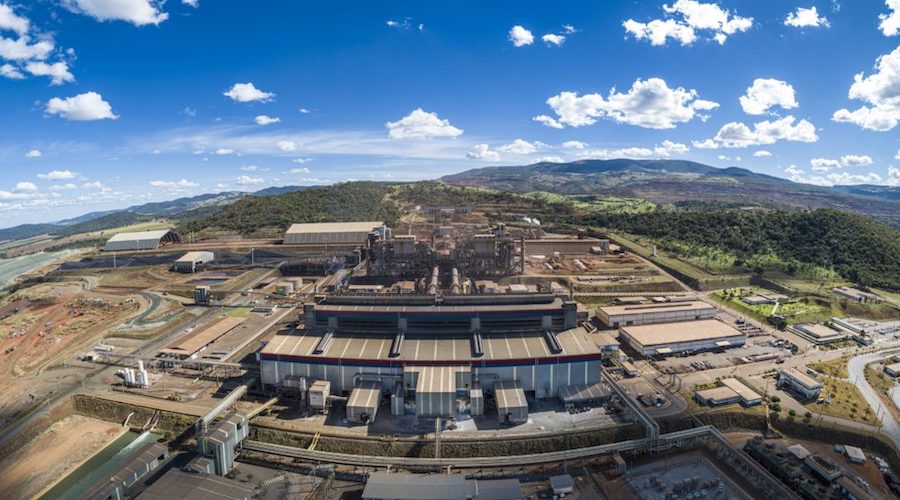

Teck hits pause on growth to fix Chile copper mine

Quebrada Blanca is an expanded, low-cost, long-life copper mine located in northern Chile. (Image courtesy of Teck.)

Teck Resources (TSX: TECK.A, TECK.B)(NYSE: TECK), Canada’s largest diversified miner, has deferred major expansion projects while it works to fix output problems at its flagship Quebrada Blanca (QB) copper mine in Chile.

A major overhaul of the mine high in the Andes came in $4 billion over budget and years behind schedule. In July, chief executive officer Jonathan Price was forced to cut production guidance. The main issue now is tailings storage.

The decision is part of a comprehensive operational review that was launched in August and is set to conclude in October, with a focus on improving performance. This review includes a detailed action plan for QB.

The Vancouver-based miner said the bulk of the work will focus on its tailings facility, where slow sand drainage has delayed development and constrained production since the mine’s recent expansion. Teck plans to raise the dam wall mechanically, add new rock benches to increase crest height, and accelerate drainage improvements.

BMO Capital Markets analysts said on Wednesday they see Teck’s operations review as a “necessary step” that “involves some pain including personnel change and perhaps further changes to future guidance”.

“We do not think this will be especially surprising to the Street, but uncertainty should remain until October,” managing director of equity research, metals & mining, Matthew Murphy, wrote. “We expect this process to ultimately drive greater confidence in the outlook and bolster the near-term free cash flow outlook by deferring further new project sanctioning.”

The company also announced management changes, including the retirement of Chief Operating Officer Shehzad Bharmal and the appointment of an unnamed industry veteran as advisor to senior leadership.

Affected projects

While large-scale project approvals are now on hold until QB achieves steady-state operations and meets ramp-up targets, BMO’s Murphy expects certain developments already sanctioned, such as the $2.4 billion Highland Valley expansion, to proceed unaffected.

San Nicolás in Mexico, in partnership with Agnico Eagle (TSX, NYSE: AEM), and Zafranal in Peru remain unsanctioned, and it is unclear how much near-term spending will be pared back or how their development timelines might shift, Murphy wrote.

Output impact

QB is central to Teck’s pivot toward energy transition metals after shedding its coal business. The mine underpins its target of producing 800,000 tonnes of copper annually by 2030.

Teck now expects QB to produce 210,000–230,000 tonnes in 2025, down from earlier projections of 230,000 to 270,000 tonnes. The company had guided copper production at 490,000 to 565,000 tonnes overall this year, but it later trimmed it to 470,000 and 525,000 tonnes. It now warns revised numbers will come with third-quarter results.

Last year, just over 200,000 tonnes of copper was produced last year at the mine, in which Teck has a 60% stake. Japan’s Sumitomo Corp. owns 30% of QB, and Chile’s state-owned Codelco, 10%.

Teck is also studying potential synergies with the nearby Collahuasi mine, jointly owned by Anglo American (LON: AAL) and Glencore (LON: GLEN).

Freeport CEO pushes for US incentives to expand copper

The Bagdad mine in Arizona is undergoing a $3.5-billion expansion. Credit: Freeport-McMoRan

United States mining giant Freeport-McMoRan (NYSE: FCX) is calling on the Trump administration to sweeten incentives for domestic copper producers and cut permitting times to help offset weak metal grades, CEO Kathleen Quirk says.

While US-based miners enjoy lower tax rates compared with other jurisdictions, copper grades in the US make investing in new domestic operations less attractive, Quirk said in an interview. Copper mines in the US often have grades of about 0.3%, compared with 1% or more elsewhere, she said.

“We have a challenge in the US because the ore grades that we mine here are very low relative to what we mine internationally,” Quirk told The Northern Miner by videoconference in August. “Companies want to go where the higher grades are. If there are things in place that can help incentivize the production in the US, that would be an advance.”

With annual output of about 4 billion lb. of copper and operations in countries such as the US, Indonesia, Chile and Peru, Phoenix-based Freeport is the world’s largest publicly-listed producer of the red metal. Its US output, which averages about 1.4 billion lb. a year, accounts for about 70% of the refined copper that’s produced in the country.

Unit costs

Operating costs vary greatly from country to country. While its unit costs in Indonesia are “close to zero” because the presence of a gold by-product generates substantial income, Freeport spends about $3 per lb. to produce copper in the US, Quirk says. And that doesn’t include the capital investments needed to start up a mine.

A recent so-called Section 232 review into copper imports, which resulted in some foreign-produced goods being taxed 50%, did provide relief for US-based miners, Quirk said. US President Donald Trump ended up excluding refined copper – the most widely imported form of the metal – from his planned import tariffs, surprising market participants and analysts alike.

“When you look at our mining in the US, there are structural aspects that make it less economic than mining internationally,” the executive said. “So one of the things we are hoping for is for the US to continue to look at policies that would help the domestic mining industry. The Section 232 investigation provided some tariffs and incentives for the US manufacturing of copper, and what we’re hoping to see more of in the future are incentives for upstream development.”

Favourable environment

Other helpful steps would include permitting reform and production tax credits, Quirk said without elaborating.

Freeport-McMoRan CEO Kathleen Quirk. Credit: Freeport-McMoRan

“Freeport in our view remains best positioned to benefit from 50% copper tariffs,” BMO Capital Markets mining analyst Katja Jancic said in a note following the release of the company’s second-quarter results in July. “Freeport’s US operations have tailwinds that in our opinion should translate to improved free cash flow profile and increased shareholder returns potential.”

To be sure, the Trump administration has already created a “much more conducive environment” for miners, Quirk stressed.

“We’re thrilled that governments around the world, and our administration here in the US, are more actively looking at how they can help incentivize the mining of critical minerals like copper,” she said. “There is a real desire to see the US regain its position in copper. Freeport is in a great position, with our existing production and pipeline of growth opportunities, to be a big part of that.”

Expansion projects

Those opportunities include three major expansion projects – two in the US and one in Chile – as well as a technological innovation that could lift annual output substantially.

The most advanced of those projects is a potential $3.5-billion expansion of the company’s Bagdad, Arizona mine that could double the concentrator’s capacity, boosting copper and molybdenum production. An investment decision is expected by year-end with a potential start-up planned for 2029.

“It’s ready to go. We are re-testing our economics,” Quirk said of the Bagdad project, which requires copper prices to average at least $4 a lb. to provide a return on investment.

“While all of us are very positive about the outlook for copper, we want to make sure that when we do the project, we have the capital cost well understood and we can execute within our budget,” she added.

Joint venture

Freeport is also looking at potentially increasing capacity at its Lone Star copper mine in Arizona and at Chile’s El Abra mine, a joint venture with Chilean state miner Codelco.

At Lone Star, a pre-feasibility study, now under way, is expected to be completed next year, with production possibly starting early next decade. The timeline for the proposed $7.5-billion expansion of El Abra is longer, with a potential 2033 target date.

“Eventually all these projects are going to be required,” Quirk said. “It’s just that they don’t happen overnight.”

El Abra, in particular, “is not an if project, it’s a when project,” she said. “We’ve done an enormous amount of work on it. Chile, like other countries is saying they want to produce more. They are going through a process to streamline permitting. What would have taken three or four years in the past to permit, we may be able to compress to under three years. That’s what we will be working on. Then it will be a three- or four-year construction period.”

Improved recovery

Quirk also has high hopes for a considerably cheaper initiative – extracting copper from material previously considered waste by injecting a water- and sulphuric acid-based solution.

Freeport estimates its facilities hold about 39 billion lb. of stockpiled copper that can’t be recovered with traditional leaching methods. About half of that amount sits at the company’s Morenci mine in Arizona.

“With data analysts and sensors, we can see within the stockpile that certain areas aren’t wet – they aren’t getting the benefit of having the solution access the rock,” Quirk said. “With these sensors, we can drill into the stockpile and inject the solution directly into the areas that need then. We can have targeted injections.”

Last year, Freeport’s so-called “leaching initiatives” generated about 214 million lb. of extra copper. By the end of the decade, the goal is to hit 800 million lb. annually, Quirk said. New additives, which the company is developing, could potentially improve recovery rates even more.

“In mining, you have to mine the material and you have to process it. In this case with the leach innovation, it’s already been mined so a lot of the costs have been incurred,” the CEO said.

“This is an incredible opportunity – the likes of which I’ve never seen in my 35 years of working for Freeport. It has risks, it still has some things to prove but as we’ve gone through it, we’ve gotten more and more excited about the potential. When we see that the world needs more copper, we feel really challenged to supply it to the customers and the societies that rely on us. This is something we think that Freeport can do.”

Brazil probes Anglo’s $500M nickel sale to China’s MMG

Brazil’s competition authority has launched an investigation into Anglo American’s (LON: AAL) plan to sell its nickel operations in the country to China’s MMG for up to $500 million.

The probe, first reported by the Financial Times, stems from a complaint filed by CoreX Holding, a global industrial group and direct competitor in the region. Anglo announced in February it would sell its Brazilian nickel mines to MMG, a Hong Kong–listed company controlled by state-owned China Minmetals. The deal is expected to close this quarter.

CADE, the Brazilian watchdog, said it opened an Administrative Procedure for Investigating an Act of Economic Concentration based on the complaint. The agency noted, however, that the probe does not automatically imply the transaction will be blocked.

Anglo declined to comment. CoreX and CADE did not respond to MINING.COM’s requests for further information.

Scrutiny in Brazil follows pressure in the United States, where the American Iron and Steel Institute urged Washington to intervene. The industry body argued that MMG’s acquisition would give China direct influence over sizeable nickel reserves, strengthening its hold on a metal critical for electric vehicle batteries and stainless steel. Anglo’s Brazilian mines produce ferronickel primarily for stainless steel producers, with Europe as a key market, according to MMG.

The company’s streamlining plan comes in the wake of a failed takeover bid by BHP (ASX: BHP). But progress has faltered. A $3.8 billion deal to sell its Australian coal portfolio collapsed last month after Peabody Energy (NYSE: BTU) walked away.

A mine in eastern Congo (Photo by Sasha Lezhnev. Courtesy: ENOUGH Project/Flickr CC BY-NC-ND 2.0)

Maman Soki is among a small group of Congolese women undertaking heavy mining work for survival after escaping a deadly attack on her village by Islamic State-aligned rebels that killed her daughter and her sister.

In April, the 49-year-old widow left her home in the east of the Democratic Republic of Congo with her son, grandson and her sister’s children to flee the Allied Democratic Forces – one of many armed groups in the mineral-rich region.

Soki now works alongside two other women at Pangoyi gold mine, lugging 30 kg sacks of debris up a muddy slope for a few dollars a day to feed the four children in her care.

“Sometimes we want to enter the pits to dig, but we’re told women aren’t allowed,” Soki said in an interview. “That’s why we always carry the already-dug sand for processing.”

A photograph of her lost sibling is among the few reminders of the life Soki left behind.

Soki now cares for her sister’s two small children, as well as her orphaned grandson. Soki’s 12-year-old son Muhindo Obed looks after his three adopted siblings while Soki is at work.

In Congo, mining is traditionally dominated by men, but women are often driven to undertake the back-breaking work to survive.

Women in mining often face discrimination and harassment by male colleagues, and perform lower-paying tasks, according to the national association RENAFEM, a Western-funded group that aims to protect the rights of female workers.

Soki hopes to save enough to open a small food store and leave mining behind, but there is little left over after paying for the children’s food, school fees and expenses.

“We worry for her safety when she goes to Pangoyi,” her son Obed said.

In July Islamic State-backed rebels killed at least 43 worshippers in a church in Komanda, and in August they killed at least 52 civilians in the Beni and Lubero areas of eastern Congo, UN and local officials said.

(Reporting by Gradel Muyisa; Writing by Jessica Donati, Editing by Alexandra Hudson)

Nippon Steel settles disputes with USW, Cliffs over US Steel deal

Nippon Steel said on Wednesday it has resolved all legal disputes with the United Steelworkers union and steelmaker Cleveland-Cliffs tied to its $14.9 billion acquisition of US Steel, which closed in June.

The settlement includes the dismissal of a lawsuit brought by Nippon Steel, its North America unit and US Steel against USW president David McCall, as well as the withdrawal of an unfair labor practice charge the union had filed against US Steel with the National Labor Relations Board.

The companies also dropped claims involving Cleveland-Cliffs and its CEO Lourenco Goncalves, who had opposed the deal.

Nippon and US Steel had accused Cleveland-Cliffs, its CEO Lourenco Goncalves and United Steelworkers president David McCall of trying to block the deal.

The union had also filed an unfair labor practice charge with the National Labor Relations Board, alleging US Steel intimidated workers and sought to suppress opposition to the sale.

The buyout, announced in late 2023 and completed on June 18, 2025, faced months of political scrutiny and union resistance over foreign ownership of a storied American steelmaker.

Nippon said no financial compensation was exchanged as part of these settlements. The parties added they remain focused on steelmaking operations and collective bargaining.

(By Apratim Sarkar; Editing by Arun Koyyur)

Zelim Urges Use of Situational Awareness Technology to Prevent Collisions

Zelim, the Edinburgh-headquartered maritime safety and security innovator, is calling for the mandatory adoption of advanced situational awareness technology to help prevent ship collisions, reduce fatalities, and improve operational safety at sea.

The call follows the recent publication of the Marine Accident Investigations Board’s (MAIB) 2024 Annual Report, which noted: “We need to radically rethink the role of human watchkeepers in the digital age. Humans do not make good monitors and if under-stimulated, they will find other things to occupy themselves.”

This was also reinforced in MAIB's preliminary report on the Solong and Stena Immaculate incident in the North Sea, where the lack of real-time situational awareness contributed to the severity of events.

On 10 March 2025, the Portugal-registered container ship MV Solong collided with the anchored oil tanker Stena Immaculate near the Humber Estuary, rupturing a cargo tank and triggering a major fire. Thirty-six crew were rescued; one seafarer remains missing and presumed dead.

Zelim CEO, Sam Mayall, said: “We wholeheartedly support the MAIB’s position on this. By combining AI-powered cameras and real-time alerting, advanced technologies such as our ZOE system can help crews act faster, prevent incidents from escalating, and provide trusted records post-event. Beyond preventing collisions and man-overboard incidents, these systems can also provide critical forensic data to support investigations and regulatory compliance. Crucially, today’s situational awareness technology reduces reliance on human vigilance alone, allowing crews to focus where their judgment and experience matter most.”

India has already taken decisive action to reduce the risk of collision and lives lost to man-overboard incidents. Earlier this year, its Directorate General of Shipping mandated CCTV systems on all domestic vessels of 500 GT and above, with full implementation required by 2028. The regulation specifies comprehensive camera placement, resolution standards, and integration with AI-based monitoring. It is designed not just for surveillance, but for proactive detection, tracking, and alerting to protect lives at sea.

“Voluntary measures are no longer enough. To strengthen safety and security at sea, global regulators must follow India’s lead and mandate advanced situational awareness solutions. Smarter ships result in safer sea,” added Mayall.

The products and services herein described in this press release are not endorsed by The Maritime Executive.

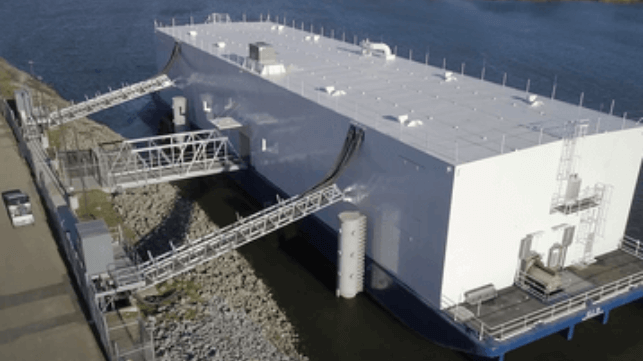

Floating Data Centers on Fast-Flowing Rivers

Industry has recognized the potential of floating data centers, like this example in Stockton by Nautilus Data Technologies (Nautilus Data Technologies file image)

Advances in information processing technology and programming have increased the need for data centers capable of processing massive volumes of information. Data centers that float on water provide ready access to cooling capacity, with potential to convert the energy from sea waves and river currents to electrical energy to operate the onboard technology.

Introduction

Data centers process massive amounts of information and require continuous and reliable access to large amounts of electric power and substantial cooling capacity. When located on land in arid regions where solar photovoltaic energy is available, data centers require roof-mounted air-cooling technology that consumes massive amounts of electrical power. While waterfront coastal locations provide easy and available access to water cooling, market demand for such locations is very high, with high real estate prices.

A cubic volume of water can provide over 3,400 times the thermal capacity of an identical cubic volume of air. Even in warm climates, the temperature of coastal seawater and river water is often cooler than air temperature. At locations where winds blow constantly, wind energy generates waves. It is possible for some technologies to convert energy from a choppy water surface to electrical energy. At other locations next to rivers, there may be scope to install a waterwheel or a turbine to convert the kinetic energy of flowing water to electrical power. While such locations are no longer available in large cities, some suitable sites might still be available in rural and remote locations to operate a data center.

Kinetic Turbines

During an earlier era, undershoot waterwheels converted river flow kinetic energy to mechanical power to operate sawmills or to drive milling wheels for grinding wheat into flour. In the modern era, kinetic turbines have replaced the classical waterwheel. While some kinetic turbines are placed on a river floor or seabed, stationery floating structures restrained by cables are able to carry kinetic turbines under the hull.

A kinetic turbine tested along the St. Lawrence River southwest of Montreal incurred higher cost for electric power compared to hydroelectric power dams. The river floor installation of the turbine reduced access for maintenance and especially during icy winter months. Floating technology that carried turbines under the hull were tested along the St. Lawrence River, downstream of the Moses – Saunders power dam. Counter-rotating pairs of vertical-axis turbines located under the hull, with a flow defector, would place generating technology and main support bearing inside the floating structure, allowing easy access for maintenance and repair. A submerged counter-flow heat exchange unit under the structure would provide cooling during summer weather. During winter, information processing technology would generate enough heat for interior heating.

River Requirements

Rivers deemed suitable for floating data centers would require the combination of sufficient water flow velocity and sufficient water depth to operate kinetic turbines efficiently. Cables connected to shore or anchored to the river floor would restrain the floating structure either near midstream or near a river bank. A current-driven kinetic ferry would carry employees between river bank and floating data center. An extended floating dock would be an option, as would having the data center floating in the river stream with a telecommunications connection to a land-based office where programming employees work.

Suitable Rivers

Data centers require a constant and reliable supply of electrical power, from rivers with reliable and steady water flow, with minimal variation in flow velocity and water depth. The East River in New York City is a suitable candidate. While looking like a river and flowing like a river, it is actually an oceanic channel with flow driven by ocean current. Downstream of Niagara Falls, the Niagara River provides steady water depth and steady flow velocity while being close to a large population. At either location, floating docks restrained by cables could provide access between shore and data center.

East of Lake Ontario and downstream of the Moses – Saunders power dam, water of sufficient depth and velocity flows through the north and south channels of the Upper St Lawrence River. Further east and southwest of Montreal, a section of the St. Lawrence River could sustain operation of a floating data center. Kinetic ferry vessels driven by water current could carry technical personnel between shore and midstream floating data center, and optic telecommunications cable could connect between the data center and shore-based work stations, reducing the number of workers who travel by ferry between shore and data center.

Other Rivers

Many rivers across North America and internationally offer sufficient water depth and water flow velocity, with near steady year-round steam flow rate to sustain operation of floating data centers. Many such rivers are navigable and transit ships, as is the case of sections of the St. Lawrence River. Ferries operate along the East River of New York City despite the powerful water current. Operation of floating data centers also requires access to a suitably qualified workforce, which is available in New York City, the Niagara region and even along sections of the St Lawrence River.

The combination of suitable river characteristics and availability of a suitably qualified workforce would determine future locations of floating data centers. It is uncertain as how to regulatory authorities would classify a floating data center, as it is essentially a vessel with the equivalent of a propeller extending downward under the hull.

Conclusions

Advances in information processing technology along with the development of advanced programming have increased the need to expand the capabilities of data centers. Data centers consume massive amounts of electrical energy and have massive cooling requirements. A data center that floats on water where powerful currents flow, likely have access to required cooling capacity along with the ability to convert river flow energy into electrical power to sustain data center operation. Some future data centers would likely float on fast flowing rivers that pass near large or through cities.

The opinions expressed herein are the author's and not necessarily those of The Maritime Executive.

Stock image.

Stock image.

Assy Plateau, Kazakhstan. Stock image.

Assy Plateau, Kazakhstan. Stock image. Quebrada Blanca is an expanded, low-cost, long-life copper mine located in northern Chile. (Image courtesy of Teck.)

Quebrada Blanca is an expanded, low-cost, long-life copper mine located in northern Chile. (Image courtesy of Teck.)