Why the Iran War May Have Just Killed the AI Boom

- The $1.5 trillion in committed AI infrastructure spending by major tech companies is built on an assumption of a functional global supply chain, which the Iran conflict has fundamentally broken.

- The war's effects, including the collapse of shipping insurance in the Strait of Hormuz, attacks on data centers, and a spike in oil prices, are structural problems that will increase component costs and slow the AI buildout.

- Compounding issues—higher costs for fuel and fertilizer, coupled with elevated electricity bills from data center demand—will shorten the political window for the AI transition and fuel consumer backlash.

The stock market spent the first week of the Iran war doing something strange: mostly shrugging. Oil spiked. Insurance markets effectively collapsed. Amazon had two data centers blown up. And the Nasdaq dipped, steadied, and the conversation shifted within days to whether the Fed might still cut in June.

The prevailing read was: disruption, yes. Catastrophe, no. This thing will be over soon. I think that read is wrong.

And wrong in a specific, structural way, not because the war will necessarily escalate further, but because the damage being done right now is the kind that compounds quietly.

It hits a system that had no room left to absorb it. And it is aimed, with surprising precision, at the single largest economic bet America has ever made.

The $1.5 Trillion Bet

Add it up. Meta has pledged over $600 billion in US AI infrastructure by 2028. Apple committed $500 billion over four years. Amazon is projecting $200 billion in data center spending in 2026 alone, up from $131 billion last year. Google sits at $175 to 185 billion. Microsoft is tracking toward $105 billion for the year.

That is roughly $1.5 trillion in committed AI capital, most of it tied to data centers, chips, and the supply chains that feed them.

These numbers have a numbing quality. They are so large they start to feel theoretical.

But they’re not theoretical. They’re the load-bearing wall of the current bull market.

Goldman Sachs noted in December that consensus capex estimates have been too low for two years running, with actual spending growth exceeding 50% in both 2024 and 2025 against forecasts of 20%.

The market has priced in the spending, the compounding returns that spending is supposed to generate, the AI productivity boom, the new revenue streams, the structural advantage that justifies Nvidia trading at the multiples it does.

The whole thing is a bet. A very large, very confident, very specific bet. And that bet has one core assumption embedded in it: that the global supply chain stays roughly functional.

Tiffany Wade, a senior portfolio manager at Columbia Threadneedle, was already nervous before the war started. "This feels like a return to Meta's old days of overspending," she told Bloomberg. "Investors are losing patience." That was November. Before the Strait of Hormuz closed.

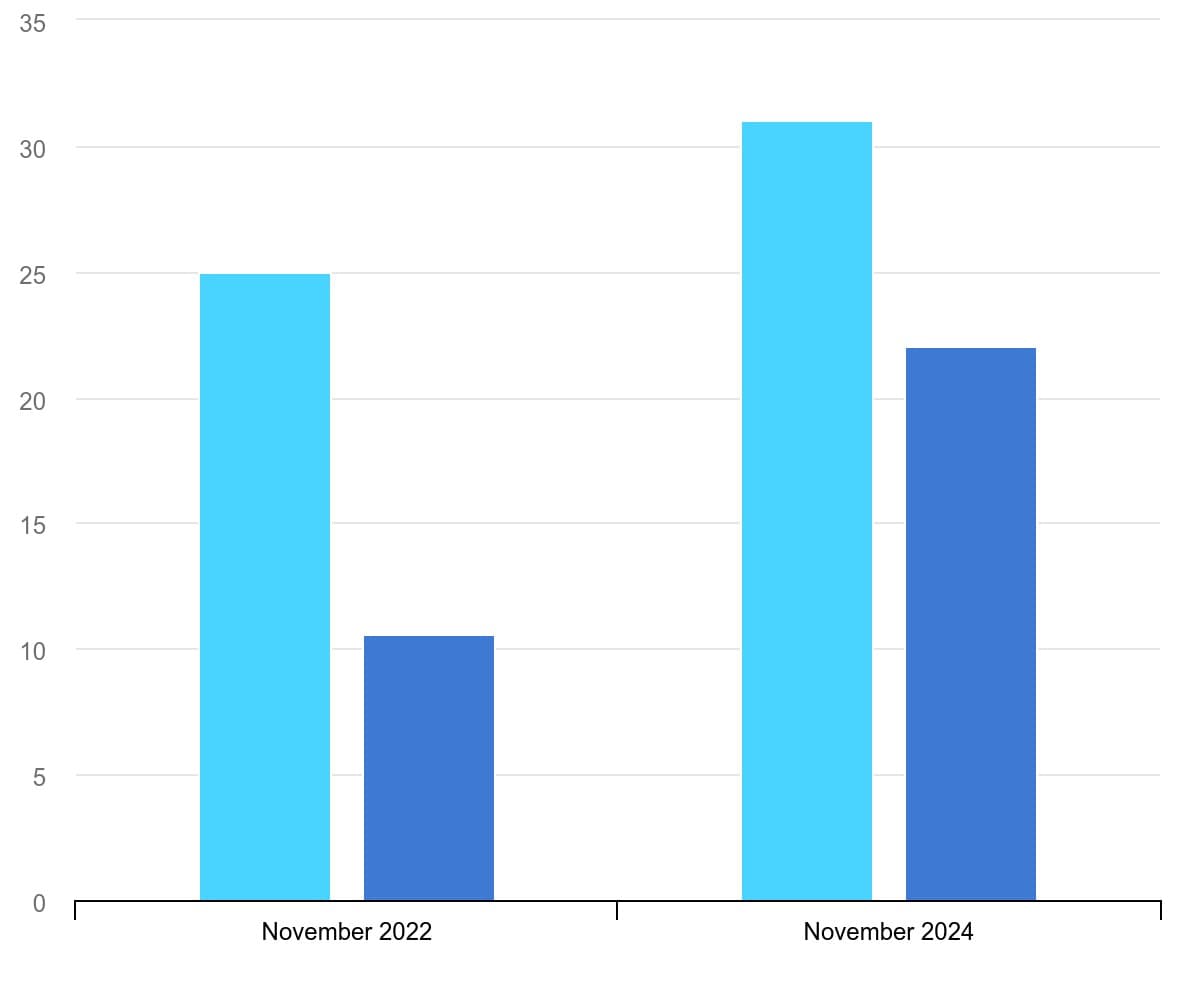

Annual average market capitalisation of S&P 500 companies, November 2022 and November 2024

Source: IEA, Energy and AI (2025)

The Supply Chain Nobody Draws

Here is something most people don't know: a single semiconductor chip crosses more than 70 international borders before it reaches an end customer.

The journey takes up to 100 days and involves more than 1,000 discrete manufacturing steps. This is not a quirk. It is the architecture.

Silicon wafers start in Japan or Germany. Chip design happens in the US or the UK. The actual fabrication, for the most advanced chips that power AI workloads, is done almost entirely in Taiwan (92%) and South Korea (8%). Assembly and testing happen in Malaysia, Vietnam, the Philippines. The finished chip ships to a US data center.

There are more than 50 points across this chain where a single country controls more than 65% of global market share. Each one of them just got more expensive and more uncertain.

Every step in that chain costs energy. Every border crossing costs money. Every logistics node, the freight forwarders, the marine insurers, the fuel for the container ships, is now running hotter than it was on February 27th.

The friction is structural and it compounds with time. It does not resolve when the headlines move on.

Oh, and the Gulf also produces a significant share of the world's helium, a critical input for semiconductor manufacturing. These things connect in ways that don't make the front page.

Halving the Dream

Here's the part that doesn't get enough attention.

Those $1.5 trillion in AI pledges weren’t just announcements; they are the reason the stock prices are where they are.

When Meta says it's committing $600 billion in AI infrastructure, the market hears something more: $600 billion in projected returns, plus whatever multiplier you want to apply for future AI dominance. The capex is the proof of conviction.

Now imagine what happens when that budget doesn't go as far as it was supposed to. Component costs up. Shipping up. Energy up. Insurance on every supply chain touchpoint up.

Related: No Missiles, No Drones: What Happens When Rare Earths Stop Flowing?

The dollar amount of the pledge stays the same. The buildout it actually buys does not. You're not getting less ambition, you're getting the same ambition running into a world that charges more for everything it needs.

The pledges don't disappear. The compounding future returns that were priced in do. And the correction, when it comes, is not proportional to the shortfall. It's proportional to the distance between what was promised and what gets built.

Markets priced in the full vision. They didn't price in the friction.

The Pin

On February 28th, the US and Israel launched Operation Epic Fury. Within days, the Strait of Hormuz, through which roughly 20 million barrels of oil flow every day, about one-fifth of global oil consumption, was effectively closed.

The IEA called it the biggest oil supply disruption in history.

Brent crude went from $70 a barrel to touching $120. It's sitting around $110 as I write this, which sounds like a retreat until you remember where it started three weeks ago.

But the oil price is almost the least interesting part of what happened to shipping. What happened to shipping was a collapse of the insurance architecture that makes global trade work.

Before the war, insuring a tanker through the Strait of Hormuz cost between 0.02% and 0.05% of the vessel's value. For a $120 million tanker, call it $40,000 a trip.

Bloomberg reported last week that coverage has leaped to roughly 5% of hull value. The same tanker now costs $5 million to insure for a single voyage. That cost does not stay with the shipowner. It travels through the price of everything on that ship.

All 12 of the Protection and Indemnity Clubs, mutual insurers that cover 90% of the world's ocean-going tonnage, gave 72 hours' notice of war cover cancellation in the Gulf. Hapag-Lloyd added a War Risk Surcharge of $3,500 per container. Daily charter rates for supertankers quadrupled to nearly $800,000 a day. Iran has made 21 confirmed attacks on merchant ships as of March 12th. That is not a threat. That is a policy.

And then there's the data centers.

Iran's IRGC-linked Tasnim News Agency published a target list: Amazon, Microsoft, Palantir, Oracle, captioned "Enemy's technological infrastructure: Iran's new goals in the region."

Within days, AWS confirmed drone strikes had damaged two UAE facilities and one in Bahrain, causing structural damage, power disruptions, and water damage from fire suppression.

AWS told customers to consider migrating workloads out of the Middle East entirely.

On pro-Iranian Telegram channels, researchers at SITE Intelligence Group documented hackers posting: "The datacenters need to be taken out. They host the brains of USA's military communication and targeting systems."

Both the Red Sea and the Strait of Hormuz are now active conflict zones simultaneously, severing the undersea cables connecting Gulf data centers to Africa, South Asia, and Southeast Asia.

First time both chokepoints have been closed at once. The $1.5 trillion bet on AI infrastructure assumed those cables would stay intact.

Why It'll Last Longer Than You Think

Markets are pricing this as a short-term disruption, a bad few weeks, a ceasefire, a slow normalization of shipping routes.

That's wrong, and wrong for a specific reason: Iran's incentive structure.

Iran cannot win this war militarily. That was decided on day one. But Iran doesn't need to win. Iran needs to make the war expensive enough for everyone else that the pressure to de-escalate lands somewhere other than Tehran.

Every week the Strait is effectively uninsurable costs the global economy more than the week before. Every data center attack is essentially free, drones are cheap, reputational damage to cloud infrastructure is not.

Every shipping delay, every fertilizer shortfall, every spike in electricity prices is a cost Iran isn't paying.

The incentive to cause economic chaos outlasts the incentive to sue for peace. The math on oil is already severe.

Oxford Economics estimates that every $10 sustained increase in oil prices knocks 0.1% off global GDP.

Federal Reserve models suggest the same $10 increase pushes US inflation up by roughly 0.35%.

Oil is up about $30 from pre-war levels right now. If prices reach $140 and hold for two months, the US approaches a temporary economic standstill. Europe, the UK, and Japan face mild contractions.

There is a historical pattern here that economists keep raising: 1973, 1978, 2008. Every significant oil shock has been followed, in some form, by global recession.

The Gulf War of 1990 to 1991 is the most instructive parallel, prolonged disruption, sustained high prices, meaningful economic slowdown even though the military phase was fairly brief.

Gregory Daco, chief economist at EY-Parthenon, put it plainly: "The longer this lasts, the more significant the shock would be."

Why would this time be different? Especially when there's less cushion than there's ever been.

The Federal Reserve entered this conflict with inflation already above its 2% target, the easing cycle already paused, and American consumers already financially stretched.

The WEF's 2026 Global Risks Report described the economy as "already navigating tariffs, post-pandemic debt overhangs and inflationary pressures." Cut rates to stimulate growth and inflation comes back. Raise rates and a stretched consumer breaks. There is no clean move.

The Part That Connects Back to the Bet

Here is where the story loops back to the $1.5 trillion.

People think of oil shocks as a gas pump problem. They are also a food problem, a chip problem, and a financing problem.

It’s the three F's: fuel, fertilizer, and financial markets. All three are now in motion, and all three eventually hit the AI buildout.

Start with fertilizer, because it's the one nobody is watching. The Persian Gulf is a fertilizer corridor, not just an energy corridor.

According to Al Jazeera's reporting on the crisis, 46% of global urea supply comes from the Gulf. Qatar's QAFCO alone supplies 14% of the world's urea. Since LNG output from Qatar collapsed, here is what has happened in the span of weeks:

- India cut output from three of its own urea plants

- Bangladesh shut four of its five fertilizer factories

- The US is already close to 25% short of fertilizer supply for this time of year

- Urea export prices surged roughly 40%, from ~$500 to ~$700 per metric tonne

- Nitrogen fertilizer prices could roughly double; phosphate up ~50%, per Morningstar analysts

This lands in the middle of spring planting season. Farmers who can't get fertilizer don't just have higher costs, they have lower yields. Lower yields mean food supply pressure in three to six months, well after the news cycle has moved on. The cause and effect will look disconnected. They won't be.

Zippy Duvall, president of the American Farm Bureau Federation, wrote directly to Trump warning that the US "risks a shortfall in crops" that "could contribute to inflationary pressures across the US economy."

Jet fuel is up 58% since the war began. United Airlines has already warned fares will rise.

Here is how this connects back to AI. Higher food prices, higher energy bills, higher airline tickets... these all hit the same consumer who was supposed to start seeing AI productivity gains show up in their lives in the next two to three years.

The patience required to get through the transition costs just got shorter.

The political window for the buildout just got narrower.

And the financing conditions that made $1.5 trillion in capex possible, low rates, stable inflation, patient investors, are all moving in the wrong direction at once.

Everything that makes the AI bet work is getting more expensive. Everything that makes it politically survivable is getting harder.

The Backlash Engine

AI already had a political problem before any of this. The job displacement anxiety is real and growing. The IP lawsuits are piling up. The environmental footprint was drawing scrutiny. But the resentment was abstract, it didn't have a number attached to it.

Energy costs give it a number.

US data centers already consume roughly 4.4% of national electricity, about 176 terawatt hours a year, according to Lawrence Berkeley National Lab.

The IEA projects that roughly half of all US electricity demand growth over the next five years will come from data centers. Goldman Sachs estimates that data center electricity demand will add 0.1% to core US inflation in both 2026 and 2027. Retail electricity prices are already up 42% since 2019, significantly outpacing CPI.

The PJM Interconnection, managing the grid serving 65 million people from New Jersey to Illinois, saw data center capacity costs add $9.3 billion to the 2025 to 2026 cycle. That works out to $16 to $18 more per month on the average residential electricity bill. People are noticing.

An AI server rack requires 40 to 100 kilowatts of power. A traditional server rack needs 5 to 15. A single AI workload consumes roughly 1,000 times more electricity than a traditional web search. These are not marginal differences. They show up on bills.

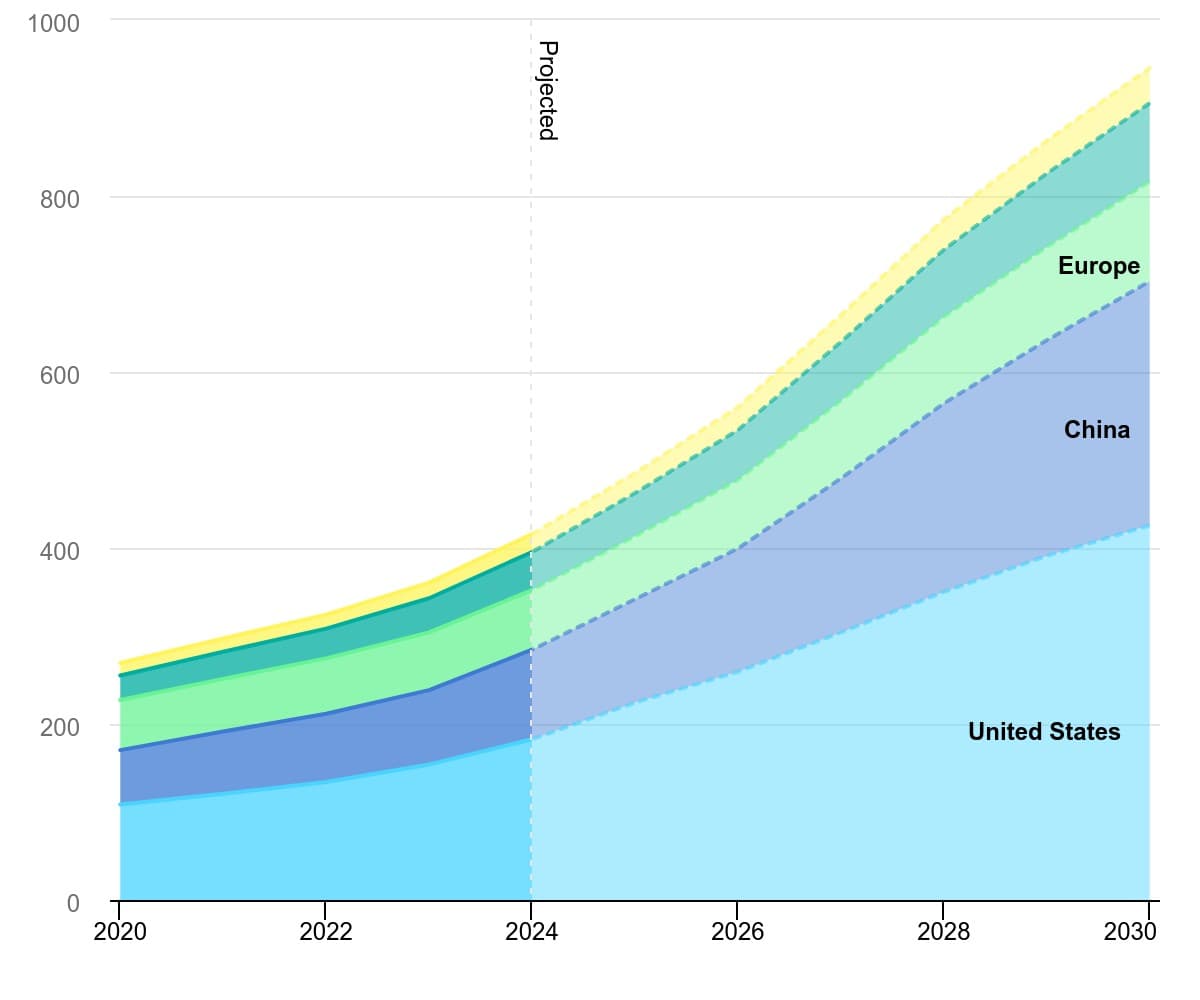

Data centre electricity consumption by region, Base Case, 2020-2030

Source: IEA, Energy and AI (2025)

When the energy price shock from the Iran war lands on top of bills already elevated by data center demand, the politics shift.

And when you consider the environmental impact…

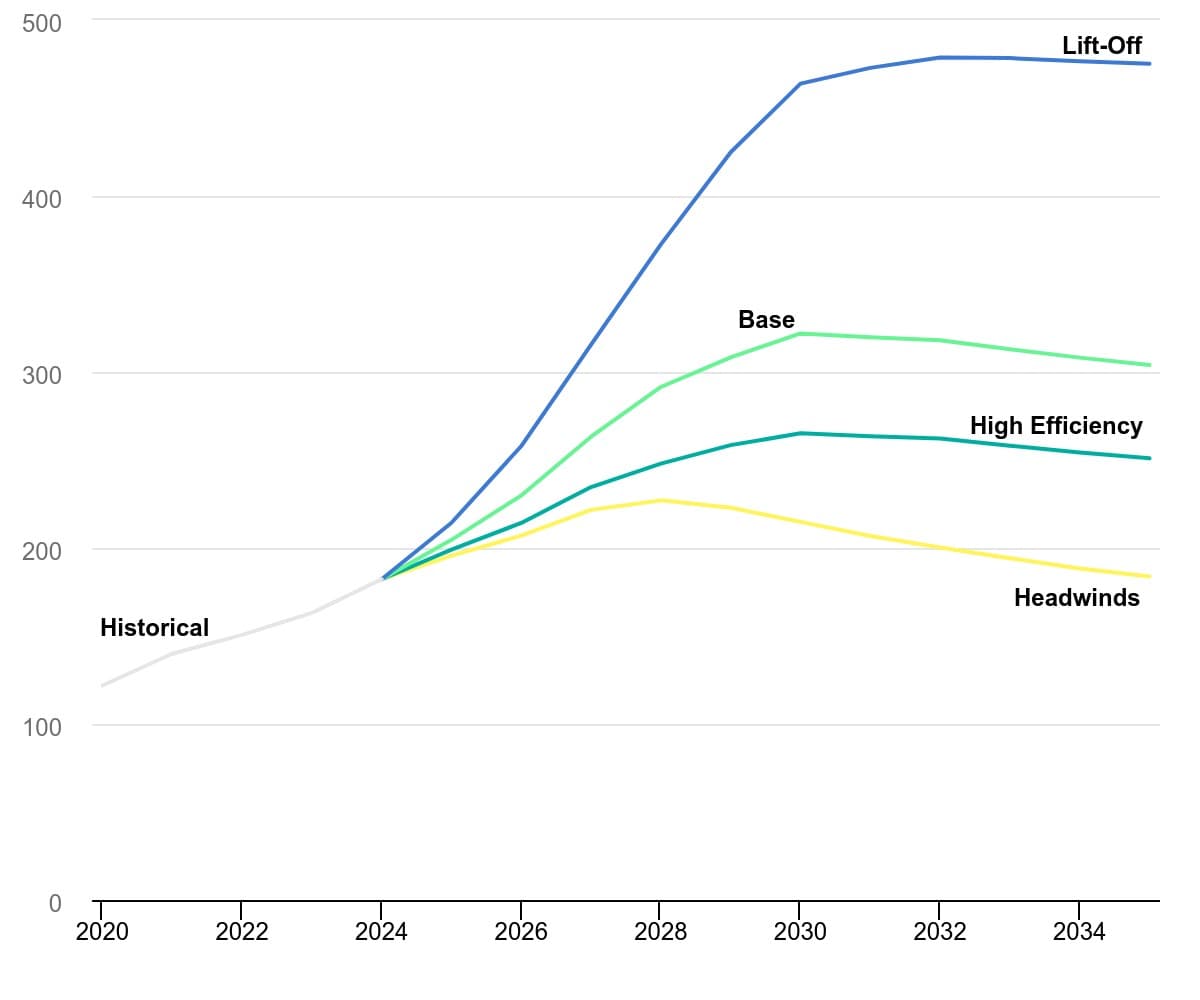

CO2 emissions associated with electricity generation for data centres by case, 2020-2035

Source: IEA, Energy and AI (2025)

...permitting battles get even harder. Grid priority legislation becomes real. State-level pushback on data center tax exemptions accelerates.

The buildout was already being slowed by cost. Now it gets slowed by politics. And those two forces amplify each other.

China Watches

There is one more actor in this story that has not fired a single shot. Yet.

China controls roughly 90% of rare earth processing globally and about 70% of rare earth mining.

Since July 2023, Beijing has been running a methodical escalation of export controls on the materials that underpin semiconductor manufacturing:

- July 2023: gallium and germanium controls

- October 2023: graphite controls

- August 2024: antimony and superhard materials

- February 2025: tungsten and tellurium

- April 2025: seven medium and heavy rare earth elements

- October 2025: comprehensive controls, for the first time asserting jurisdiction over foreign-made products containing Chinese-origin rare earths and over rare earth technology know-how globally

The October controls were suspended through November 2026 after US-China talks.

Clark Hill, analyzing the announcement, described it as "a pause in escalation, not a strategic reversal."

The underlying architecture is fully intact. The US Geological Survey has estimated that a total gallium and germanium ban alone could cost the US between $3.4 and $9 billion in GDP. The weapon is built. Beijing is deciding when to use it.

China doesn't need to do anything dramatic right now.

The US is bogged down in a Middle East war. AI capex timelines are slipping. Supply chains are taking friction from every direction.

Beijing can wait, let the situation compound, tighten rare earth flows through "administrative review" if the moment calls for it, and emerge in 18 months having closed the AI development gap while everyone else was watching Hormuz.

The Question Markets Haven't Asked Yet

The AI bet was not irrational. It was made by serious people with real conviction, backed by genuine technological progress. The case for AI productivity gains is not fabricated.

But it was a bet made under specific conditions: stable energy prices, accessible components, functional shipping lanes, cooperative geopolitics, and a consumer with enough slack to absorb a few years of transition costs before the gains showed up on their side of the ledger.

None of those conditions exist right now.

The insurance market has already repriced the Strait of Hormuz as a war zone. The fertilizer market is already pricing a supply shock. The shipping market is already pricing in a new risk premium that will not disappear when the shooting stops, because once underwriters reprice a region, they don't unwind it quickly. Reputational risk is sticky. Supply chain reroutes are sticky. Political backlash, once it finds a number to attach to, is very sticky.

The question is not whether the AI buildout survives this. Some version of it will. The question is whether the market has actually updated its model, or whether it is still running on the assumption that this resolves in a few weeks and everything returns to February 27th.

I don't think it resolves in a few weeks...

The bet was made. The conditions changed. The math is what it is.

By Michael Kern for Oilprice.com