It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Saturday, March 21, 2026

AU

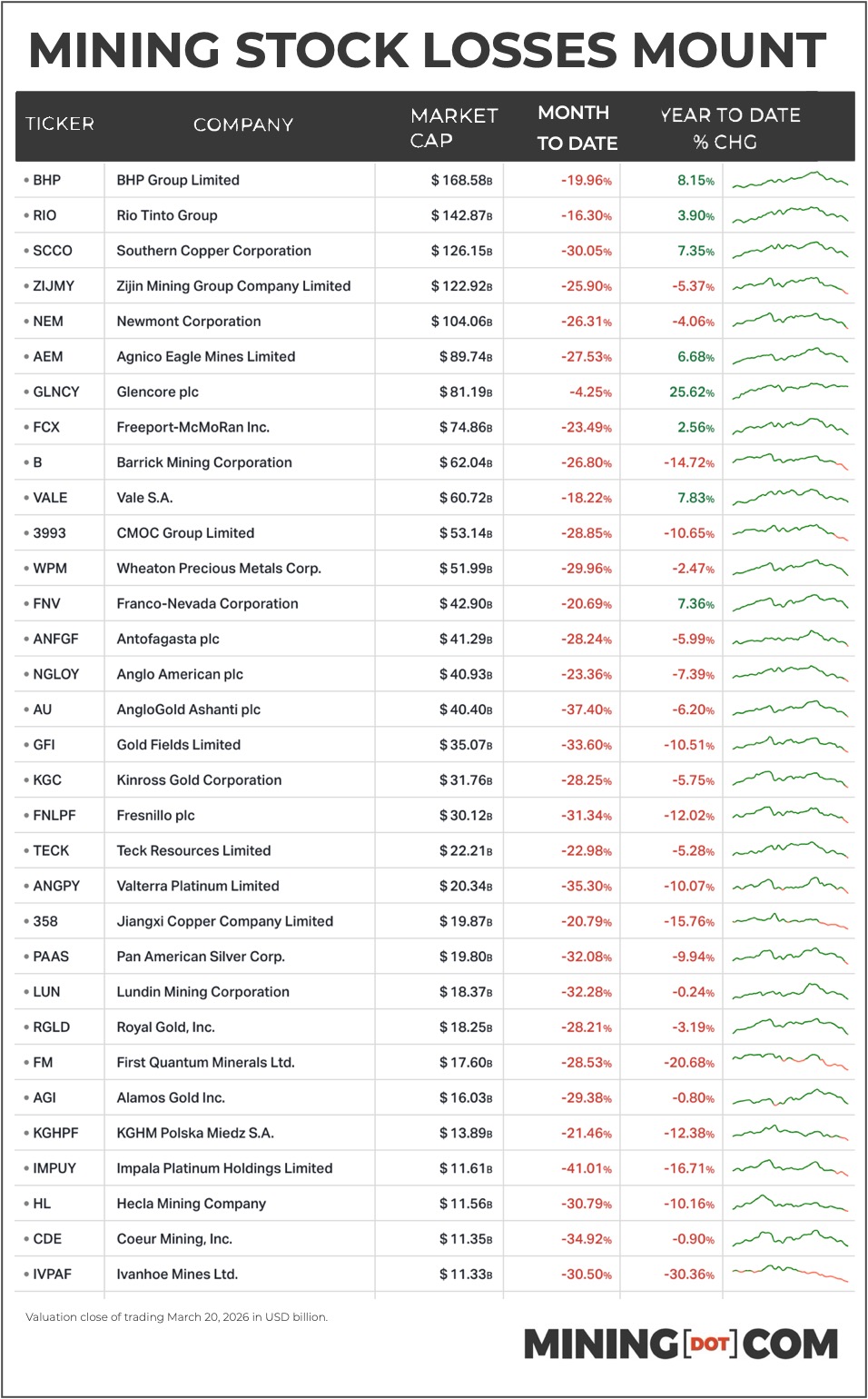

CHART: Billions wiped of mining stocks as gold, silver, copper prices plummet

Gold (and copper and silver) bears are out. Image: The Scott

Stock losses for world’s biggest mining companies near 30% since war’s start as copper enters bear market, silver falls 40% from high and gold suffers worst week in decades.

Gold futures in New York fell by $225 an ounce from opening levels to last trade at $4,492 an ounce by late afternoon, a 3.5% decline on the day and more than 11% for the week. As usual silver’s swings were wilder with the precious metal exchanging hands for $67.81 in after hours trade, a 6.9% drop from the start of trading on Friday.

Copper ended the day down 4.0% and was last worth 5.30 per pound ($11,690 a tonne), down 7.4% for the week. Gold, silver and copper entered a technical bear market with gold down more than $1,100 or just over 20% from its January 29 record, silver dropping 44% and copper giving up just shy of 20% or more than $2,800 per tonne from its all-time high struck at the same time.

Gold, silver and platinum stocks were hardest hit with Newmont (NYSE:NEM) now trading 26.3% below levels seen just before the start of the Iran war at the end of February after Friday’s heavy selling which saw 30.7 million shares traded.

Barrick Mining (NYSE:B) is down 26.8% over the same period with 29.1 million shares exchanging hands on Friday. Newmont is now worth $104 billion in New York down from a peak of $143 billion at the end of January while Barrick’s market worth is down $27 billion since then for a $62 billion market cap on Friday.

Shares in Anglogold Ashanti (NYSE:AU) are down an eye-watering 37.4% so far in March for a market value of $40 billion while Gold Fields (NYSE:GFI) has lost 33.6% to $35 billion. Kinross Gold’s slide reached 28.3% for a market cap of $32 billion.

Royalty and streaming companies Wheaton Precious Metals (NYSE:WPM) has fallen just under 30% since the start of hostilities in the middle east and is now worth $52 billion compared to a more modest drop of 20.7% for Franco-Nevada at a $43 billion evaluation.

Over the counter units of silver miner Fresnillo (OTCPK:FNLPF) trading in the US is down 31.3% in March shaving its market cap to $30 billion while Pan American Silver (NYSE:PAAS) has suffered a 32.1% decline to under $20 billion. Valterra Platinum (OTCPK:ANGPY) has been one of the worst performers dropping 35.3% from a multi-year high hit on the Friday before the bombing campaign started, ending up at a $20 billion market cap just three weeks later.

Some copper producers and diversified companies fared better than the precious metal sector but losses top 20% across the board with only a couple of exceptions.

BHP (NYSE:BHP) shares trading in the US have shed 20.0%, sliding from a record high valuation (for any mining stock in history) of $213 billion at the start of the war. Record profits for the Melbourne-based company and China as its main customer has not been enough to shield the firm from the broader fallout of the war.

Southern Copper (NYSE:SCCO) underperformed other copper majors, with losses for March of 31.1% to $126 billion, seeing the company in the Grupo Mexico stable lose its edge as the world’s second most valuable miner over Rio Tinto (NYSE:RIO) which has come of relatively lightly with a 16.3% decline to a $143 billion market cap.

Rio Tinto stock received a lift after the company said on Monday it has gained control of acreage in Arizona needed to build the Resolution mine, a project slated to become one of the largest US sources of copper. Rio Tinto said it would now embark on a $500 million drilling campaign to delineate the deposit which is co-owned by BHP.

Freeport-McMoRan (NYSE:FCX) was one of the most heavily traded mining stocks with more than 25 million shares exchanging hands. After a 23.5% retreat for March, Freeport is now worth $74 billion after briefly reaching the $100 billion mark (only the 8th mining stock to ever do so) in February.

A Chilean business paper earlier this week reported that the Phoenix-based company has begun the environmental permitting process for a $7.5 billion expansion of its majority owned El Abra copper mine in Chile. The expansion would increase annual copper output by more than 300,000 tonnes, compared with 91,000 tonnes produced last year.

Glencore (OTCPK:GLNCY) has managed to emerge relatively unscathed, only losing 4.3% since the start of US and Israeli operations in Iran in part to its extensive oil trading business which should do well as crude and gas prices jump. The Switzerland-headquartered company trades around 4 million barrels of oil equivalent per day. Glencore is now worth $81 billion and year to date the company is now the best performer among mining’s heavyweights with a 25.6% advance.

There was speculation last week from large investors in Glencore that a recent surge in coal prices will help bring Rio Tinto back to the table for a fresh attempt at creating the world’s biggest mining company after meeting with leaders of both companies in Australia.

Vale (NYSE:VALE) stock has declined by 18.2% for a market cap of $61 billion, one of the better performing large-cap miners. The CEO of Vale’s base metals spin-off, Shaun Usmar, told Bloomberg at the beginning of March the sprawling nickel-and-copper business is ready for a potential initial public offering by midyear, sooner than previously indicated. The task of bringing down costs, lowering capital intensity and accelerating the project pipeline is moving ahead at a faster clip than previously envisaged Usmar said.

Anglo American (OTCPK:NGLOY) losses since the beginning of the month have climbed to 23.4% matching the decline of merger partner Teck Resources (NYSE:TECK) affording the Canadian miner a $22 billion valuation compared to Anglo’s $41 billion.

Punter’s favourite Ivanhoe Mines (TSX:IVN) is now trading 30.5% lower for March at $11 billion while copper specialist First Quantum Minerals (TSX:FQM) has fallen by 30.5% to $18 billion over the same period. Pink sheets of Antofagasta (OTCPK:ANFGF), and KGHM (OTCPK:KGHPF) dropped 28.2% to $41 billion and 21.5% to $14 billion respectively.

Chinese heavyweight Zijin Mining (OTCPK: ZIJMY) has settled in as the world’s fourth most valuable mining firm despite its US over the counter units plunging by 30.2% since the start of the conflict for a $123 billion market value.

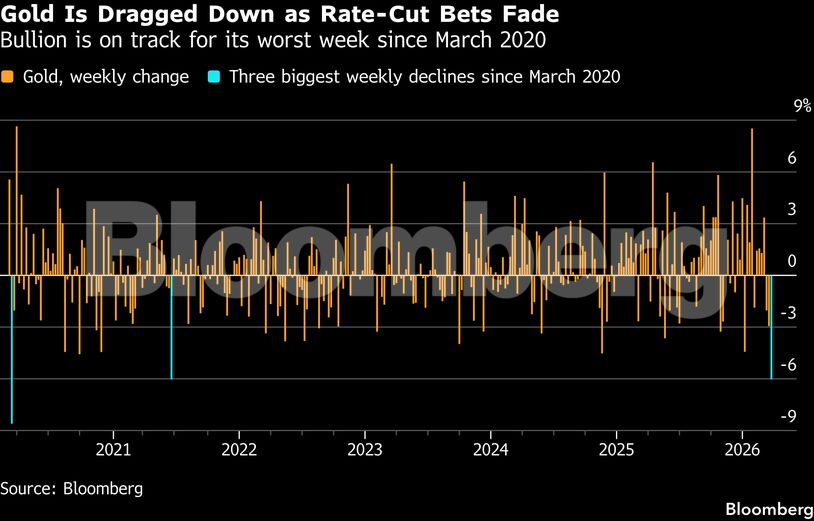

Gold price set for worst week in 4 decades as war curbs rate-cut bets

Gold headed for its biggest weekly loss since 1983, as war in the Middle East boosted energy prices and reduced expectations for interest-rate cuts.

Bullion’s decline deepened as the dollar and bond yields rallied after CBS reported that the US is preparing to potentially deploy ground forces into Iran. Traders increased their bets on rate hike to 50% by October amid concern that a protracted conflict could stoke inflation. Higher rates hurt gold as it doesn’t pay interest.

Iranian officials have become reluctant to even discuss reopening the Strait of Hormuz as they focus on surviving the attacks, according to a person involved in direct, high-level contacts with Tehran. The Wall Street Journal reported that the Pentagon is sending three warships and thousands of additional Marines to the Middle East.

Gold — widely viewed as a haven — has dropped every week since the US and Israel attacked Iran last month. The retreat has come as the US dollar gained ground while investors sold stocks and bonds amid concerns over the ripple effects of elevated energy costs to inflation and global growth.

Gold’s pullback reflects a combination of profit-taking and liquidation amid concerns about less monetary easing, according to Rhona O’Connell, an analyst at StoneX Financial.

Prices above $5,200 had attracted a lot of buyers, leaving the market vulnerable to correction, O’Connell said. When prices started to fall, many investors hit their stop-loss levels — automatic instructions to sell if prices drop to a certain point — so selling quickly accelerated, she said. Technical signals, particularly moving averages, added to the downward pressure, she added.

Forced selling tied to the equity rout may also have contributed to gold’s decline, while slower central bank buying and outflows from exchange-traded funds have further weighed on sentiment, according to O’Connell.

Bullion-backed ETFs are set for a third week of outflows, with holdings falling more than 60 tons in that period, data compiled by Bloomberg show.

Despite the recent pullback, gold remains about 4% higher this year. Prices touched a record just below $5,600 an ounce in late January, supported by a wave of investor enthusiasm, central-bank buying, and concerns over threats to the Fed’s independence posed by President Donald Trump.

Gold fell 3.1% to $4,508.96 an ounce as of 3:03 p.m. in New York, on course for a eight-day losing run, the longest since October 2023. That drop dragged the metal’s 14-day relative-strength index — a gauge of momentum — below 30, a level that some traders see as oversold.

In other precious metals, silver fell 6.3% to $68.20 an ounce, down by more than 15% this week. Palladium and platinum were also on track for weekly losses. The Bloomberg Dollar Spot Index rose 0.5%.

(By Yvonne Yue Li)

Gold mining stocks set to erase 2026 gains as rate cut bets fade

Global gold mining stocks tumbled, and are now in the red for this year, as traders ratcheted back expectations for interest rate cuts with oil prices surging amid the Iran war.

The NYSE Arca Gold Miners Index fell 6.6% on Thursday to the lowest level since December. The index, which includes companies from the US, Canada, the UK and Australia, is now down about 1.9% in 2026. It was up as much 35% on March 2, the first trading day after the US and Israel launched strikes on Iran, and as Iran retaliated.

The sector’s weakness deepened Thursday as escalating attacks in the Persian Gulf pushed up crude prices and drove down gold for a seventh session, marking the longest losing streak for the metal since October 2023.

The metal has declined about 12% since the start of the war as costlier energy risks sparking inflation and making it harder for central banks to reduce borrowing costs. That poses a risk for bullion, which performs better when rates are lower since it offers no yield. Traders no longer see Federal Reserve policy easing this year and some are hedging for a potential hike.

“For now, investor attention is on margins and the potential double whammy of lower gold prices and higher energy/consumable costs,” Christopher Lafemina, an analyst at Jefferies LLC, wrote in a note to clients. “In a prolonged conflict scenario, it’s possible to see more pressure on gold from higher rate expectations and a stronger US dollar.”

The other force working against gold in recent weeks is that the US dollar has emerged as a key haven during the conflict, with the Bloomberg Dollar Spot Index gaining 1.5% in March. Bullion is priced in dollars, so the precious metal has become relatively more expensive for buyers in other currencies.

Gold mining stocks saw large inflows in 2025, when the Bloomberg dollar index sank about 8%. Bullion gained 65% last year and hit a series of record highs. Newmont Corp., Agnico Eagle Mines Ltd. and Barrick Mining Corp. all rose over 115% in 2025 — the type of gains that are usually expected more from speculative assets than a metal seen as a haven. Now with the war dragging on, some investors are dumping the stocks.

“When volatility hits, the market sells anything liquid, and miners are liquid,” Matthew Tuttle, chief executive office of Tuttle Capital Management, wrote in a note to clients. “Add the fear that oil stays high, and you get a fast, ugly unwind — even in companies that are still printing cash.”

Barrick is expected to see annual earnings growth of 55% this year, while Agnico Eagle is projected to register a 72% year-over-year increase, according to analysts tracked by Bloomberg. Both companies are based in Toronto.

While lower gold prices would weigh on revenue, the large mining firms will likely be cushioned by the big run-up in the metal in recent years, analysts say.

After all, since the end of 2023, bullion prices have soared more than 120%, a major tailwind for the index of gold miners, which has gained more than 170% in that period.

If oil prices stabilize and pressure from interest rates and the dollar eases, miners with net cash, lower costs and high-quality assets like Newmont and Agnico Eagle will likely rebound, Tuttle wrote.

Gold exports from Switzerland in February fell 18% from the previous month to the lowest level since August as shipments to Britain and India slowed, Swiss customs data showed on Thursday.

Deliveries from Switzerland, the world’s biggest bullion refining and transit hub, to the UK fell to 20 metric tons last month from 43 tons in January. The UK is home to the world’s largest over-the-counter gold trading hub.

Supplies to India, a major bullion consumer, slowed to 13 tons in February from 23 tons with bullion trading at a discount in the local market amid subdued demand.

Kazakh construction tycoon buys gold miner Altynalmas

Kazakhstan Almaty city. (Stock image by podgorakz.)

One of Kazakhstan’s most prominent construction tycoons agreed to buy gold producer JSC AK Altynalmas and its units as he continues to expand his business interests.

Shakhmurat Mutalip’s Central Asia Resources Holding Ltd. signed a purchase agreement with majority owner Gouden Reserves BV and eight other shareholders, the company said in an emailed statement, without giving a value for the transaction. A representative of Altynalmas confirmed the deal.

“The acquisition of JSC AK Altynalmas is an important step in the implementation of the Holding’s long-term investment strategy,” Mutalip said in the statement Thursday. “This transaction reflects our confidence in the Group’s potential and its future development.”

Altynalmas is one of Kazakhstan’s largest gold producers, with output totaling 15.9 metric tons of gold in 2024.

Mutalip and Nurlan Artykbayev, who bought copper producer Kazakhmys in December, have emerged as prominent members of a business elite that’s become more influential since President Kassym-Jomart Tokayev consolidated power in the wake of riots in 2022. Since then, there has been a noticeable shift of wealth and authority away from circles that flourished during Nursultan Nazarbayev’s long-term rule.

Mutalip, the owner of infrastructure building group Integra Construction KZ, is in discussions with Glencore to purchase the miner’s 70% stake in zinc and gold producer Kazzinc Ltd., Bloomberg reported last month, citing people familiar with the matter. Mutalip is also in discussions to buy 40% of Eurasian Resources Group from the families of two of the Kazakh mining group’s founders, the people said.

(By Nariman Gizitdinov)

Diana Vows Proxy Fight After Genco Again Rejects Merger Proposal

Diana said it will proceed with its efforts to elect new independent directors in its takeover battle for Genco (Diana Shipping)

The takeover battle designed to consolidate the dry bulk shipping with the merger of Diana Shipping and Genco Shipping & Trading continues as both sides appear entrenched in their position. Genco’s board has twice rejected proposals from Diana, with the battle appearing to be headed to the shareholders after Diana put forward an alternate slate of directors for Genco.

“Rather than constructively engage with Diana regarding our premium proposal, the Genco Board has for the second time dismissed it without seeking any clarification,” wrote Diana in its latest salvo in the takeover fight. The company asserts that combining the two companies is ideal based on the start of a strong cycle in the sector.

Diana had increased its proposed price per share and reported that it had secured financing. It also said that it had an agreement with Star Bulk to sell 16 of Genco’s vessels after completing the combination. For its part, Genco’s board has reputedly said the proposals are “well below Genco’s intrinsic value and NAV and fail to provide a premium for control of Genco.” The board says it unanimously agreed the proposals are not in the best interest of Genco shareholders.

Rumors of a takeover began last year when Diana began buying shares of Genco. It accumulated approximately 14.8 percent and then, in November, went public with its proposals. It increased the offer in March but says Genco has not engaged in discussions.

Further, Daiana asserts that the board “continued to raise unfounded questions about its financing.” Early on, Genco also said that it had a stronger balance sheet and that maybe it should be buying Diana. Now, Diana asserts the board is making comments that are “simply false and appear intended to divert attention.” Genco, in its response this week, called the proposed sale of vessels a “fire sale” and raised doubts about Diana’s reported $1.433 billion fully committed financing.

“Genco’s actions lead us to conclude that this board and management team are more focused on entrenching themselves than maximizing value for their shareholders. We, therefore, have no choice but to proceed with our effort to elect to the Genco board independent directors who will act in the best interest of all shareholders by exploring all meaningful opportunities for value creation,” said Diana.

The Genco board says it “remains open to engaging with Diana upon receipt of an offer that appropriately reflects Genco’s intrinsic value and upside potential.”

Genco Rejects Diana’s Revised Offer Citing Value and “Fire Sale” of Ships

Genco for a second time rejected a proposal from Diana again saying it undervalues the company (Genco file photo)

The battle to further consolidate the dry bulk segment continues with Genco Shipping & Trading announcing that its board unanimously rejected the revised, non-binding indicative proposal from Diana Shipping to acquire the company. Two weeks ago, Diana had increased its offer while detailing financial commitments and saying that after closing, it would sell 16 Genco vessels to Star Bulk.

“Our board reviewed and rejected Diana’s revised proposal and determined that it is substantially below Genco’s intrinsic value and fails to appropriately compensate Genco shareholders, especially in light of our superior returns, premium earning assets, leading commercial operating platform, spot-focused commercial strategy, and sizeable operating leverage in a strengthening drybulk market,” it writes in the response.

Diana has cited what it considers to be “an opportune time of the cycle” for the dry bulk sector, saying the combination would use Diana’s operating platform and increase the scale and flexibility of the fleet while enhancing leverage to the market. The combined company could have as many as 80 bulkers, giving it a strong position in the segment.

The original proposal made in November 2025 was at $20.60 per share of Genco and followed Diana’s open market transactions in which it had accumulated approximately 14.8 percent of the shares. It later raised the offer to $23.50 per share, saying that it represented a 31 percent premium on the stock price before the merger was proposed. It said the increased proposal was supported by $1.433 billion of fully committed financing and that it had agreed with Star Bulk to sell 16 of Genco’s vessels after closing for $470.5 million.

Genco responded that the proposal “fails to provide an appropriate premium to NAV,” while asserting Diana was using the lowest analyst NAV projection and not the mean estimate of $251. Further, it asserts there is an execution risk while calling the agreed sale of vessels to Star Bulk “fire sale” prices. It says it also introduces uncertainty and deprives Genco shareholders of full value. It also continues to question the committed financing behind the proposal.

Genco initially said that it had the stronger balance sheet and said that if anything, it should be acquiring Diana. Now it says it remains open to engaging with Diana upon receiving an offer that appropriately reflects its intrinsic value and upside potential.

Diana had presented the increased offer on March 6. As an alternative, it has also presented an alternative slate of directors to Genco’s shareholders for a vote at the upcoming annual meeting.

Filing Confirms MSC is Buying into Sinokor and Behind Tanker Buying Spree

MSC is buying into Sinokor which has been buying up VLCCs (file photo)

Public filings in Cyprus and Greece are ending months of speculation, providing the first confirmation that the Aponte family and MSC Mediterranean Shipping are in fact linked to a sudden and dramatic wave of tanker acquisitions that began in late 2025. South Korea’s Sinokor Maritime was the name associated with the buying spree of very large crude carriers, while speculation linked the money and the ultimate buyer as MSC.

It has now been revealed that MSC, through its SAS Shipping Agencies Services division, has acquired a 50 percent ownership stake in Sinokor Maritime. It will share ownership of the company with Ga-Hyun Chung, the founder of Sinokor and previously the company’s sole owner. The company, on its website, says it launched the first Korea-China container liner service in 1989 as Sinokor Merchant Marine Co., and over the years, it has expanded mostly in containerships and dry bulk.

The companies, according to an in-depth article in Forbes, started a relationship when MSC was moving aggressively to buy secondhand tonnage in the container segment. They believe Sinokor sold MSC at least 11 vessels as part of a buying spree in which $40 billion was spent between January 2022 and March 2025 on containerships, according to Forbes. Today, MSC is reported to own or have on charter a total of nearly 1,000 containerships with a total capacity of over 7.2 million TEU.

Sinokor, which is equally as private as MSC, was linked to a rapid series of VLCC tanker acquisitions, with Forbes writing that market sources told it that it appeared it was buying as many large oil tankers as “it could get its hands on.” There were deals with Dynacom Tankers and Frontline, as well as smaller companies. Forbes cites data from Veson Nautical, which says by March, $3.3 billion had changed hands for at least 60 tankers.

In its exposé, Forbes dug into the corporate records in Panama and Equasis. It identified 31 tankers linked to Sinoor but not owned by the company. It found 11 of them registered to a company headed by Mario Aponte and with the address of MSC Shipmangement in Cyprus. There was a total of 18 similar companies, but it was unclear if the other seven had or were buying tankers as well. It notes that another 20 tankers are registered in Liberia, where the records are not public.

Forbes’ sources put the total number of tankers acquired at 76, while other analyses believe it is higher, reaching possibly 100 or more VLCCs. Bloomberg estimates the partnership will eventually control about 150 supertankers, giving it a 40 percent market share. Others put it closer to 25 percent.

It appears to be a well-timed play into the tanker sector as valuations soared in 2026. The war with Iran, however, raises uncertainties for the longer-term outlook for the market.

It is not the first time MSC has used SAS to make its move into other segments. In 2024, SAS purchased Gram Car Carriers to get the group into that market segment. MSC has also expanded its investment into ferries and cruise ships, as well as launching airfreight and buying into railroads and onshore logistics. It took a half interest in the operator of the Port of Hamburg and is said to still be pursuing the acquisition of CK Hutchison’s international port terminal portfolio.

In typical Aponte, MSC fashion, there has been no acknowledgement of the investment in Sinokor or the tankers. The company does not comment on its strategic intent or the opportunities for integration in its operations.

Op-Ed: Ships Should Meet the Polar Code Before Entering Canadian Arctic

Even experienced and well-equipped operators can encounter challenges in the Canadian Arctic, as seen in the Thamesborg grounding last year, above (CCG press handout)

The United Nations International Maritime Organization (IMO) adopted the Polar Code in November 2014 to reduce loss of life at sea caused by inadequate preparedness for operations in polar regions, which are more isolated and challenging than lower-latitude waters. The Code entered into force on January 1, 2017 and initially applied to seagoing vessels of 500 gross tonnage (GT) and above, as well as certain vessel classes such as cruise ships. On January 1, 2026, the IMO expanded the categories of ships that must comply with the Code to include fishing vessels of 24 meters and above, pleasure yachts of 300 GT and above, and cargo vessels between 300 and 500 GT operating in polar waters.

The Polar Code sets standards for ship design and construction, crew qualifications, onboard safety equipment, operations, training, and environmental protection in polar waters. Although the initial version did not resolve all challenges of polar navigation, it represented a major step forward. It specifically calls for a high standard of design and performance for survival equipment, recognizing the unpredictable weather, isolation, and lack of infrastructure in both the Canadian Arctic and Antarctic, where search and rescue (SAR) assets may be several hours, if not days, away.

In 2023, the International Organization for Standardization (ISO) published ISO 24452:2023, “Ships and marine technology — Personal and group survival kit for use in polar water,” which specifies minimum design and performance requirements for personal and group survival kits used under SOLAS and the Polar Code. The Code defines “maximum expected time of rescue” as the time used for designing equipment and systems that provide survival support, and states that this period shall never be less than five days. In 2025, the United States Coast Guard confirmed the requirement that survival equipment for polar operations must support at least five days of survival.

Maritime traffic is increasing in the Canadian Arctic. Shrinking polar ice, attributed to global warming, is a major driver of rising marine activity, but other factors are also making the Northwest Passage more attractive: water restrictions affecting the Panama Canal, ongoing security issues in the Red Sea, tensions with Russia and its Northern Sea Route, and persistent ocean piracy in other key choke points. Combined with growing mining activity, these trends are leading to more traffic in Canada’s Arctic waters, thereby increasing the risk to a fragile environment with a short vertical food chain on which many Inuit rely for subsistence, as well as elevating the potential for loss of life in a region with extreme weather and minimal infrastructure.

The greatest concern is not the traditional annual community resupply shipping companies, which are experienced operators that typically meet Polar Code requirements, but rather those with limited arctic experience, including adventurers and superyachts. Too many of these vessels arrive poorly prepared for a hostile operating environment. Increasing numbers of cruise ships are entering the waters of the Arctic Archipelago to experience the fabled Northwest Passage, and cruise ships running aground in Canada is not longer a theoretical scenario, as several groundings have already occurred in Nunavut.

The cruise ship Hanseatic ran aground in 1996 because the bridge team deviated from the prepared navigation plan and relied on a navigation buoy left from the previous season that had shifted. The MV Clipper Adventurer grounded near Kugluktuk in 2010 with its forward-looking sonar inoperable. The Akademik Ioffe, a retrofitted icebreaker operated as a cruise vessel, ran aground in 2018 about 78 nautical miles north-northwest of Kugaaruk, after the officer of the watch was multitasking, the helmsman was fully occupied steering, and no other crew were assigned to monitor the echo sounders and maintain lookout, with the echo sounder alarms turned off. Even among seasoned arctic operators, several fuel tankers have grounded in the Canadian Arctic, including the Mokami in August 2010, the MV Nanny in February 2012 and again in 2014, and the Kivalliq W in October 2022.

These events illustrate failures in navigation practice, equipment readiness, and bridge resource management that the Polar Code is intended to address; had those ships fully met the standards and practices now required by the Code, these accidents might have been avoided.

?Serious maritime incidents—loss of propulsion, allisions, steering failures, groundings, and fires—occur worldwide on a daily basis, and a loss of steering or power in confined or coastal waters can rapidly lead to disaster. The destruction of the Francis Scott Key Bridge in Baltimore by the container ship MV Dali demonstrated how quickly events can escalate when a large ship loses controllability near critical infrastructure.

Another instructive example occurred off the coast of Norway when the cruise ship Viking Sky lost power in a storm. On March 18, 2019, Viking Sky issued a mayday call after experiencing engine problems in heavy seas off Norway’s western coast, with 1,370 passengers and crew onboard. In very rough conditions, the vessel began drifting toward the coast, and the sea state was too severe to safely launch lifeboats. A large-scale helicopter evacuation was initiated, and in very challenging conditions, about 400 passengers were airlifted to safety before the crew managed to restart one engine and steer the ship away from danger. Dozens of people were injured, and several required hospitalization. Had the vessel grounded, waves could have repeatedly smashed the hull against the shore, potentially forcing passengers and crew to abandon ship into frigid waters without adequate protection. The Norwegian Safety Investigation Authority later criticized Viking Sky, noting that the vessel came within roughly one ship’s length of grounding.

In the Canadian Arctic, SAR resources are often many hours or even days away. When the Clipper Adventurer grounded near Kugluktuk, it took 42 hours for a Canadian Coast Guard vessel to arrive on scene. Vessels responding to distress in the Arctic must typically proceed slowly because of ice-infested waters, harsh weather, and the fact that much of the Arctic Archipelago is only partially charted to modern standards.

Canadian Forces SAR aircraft are based in southern Canada, including Canadian Forces Bases Winnipeg, Trenton, and Halifax. Aircraft on SAR standby can usually take off within two hours, and flight times to the Northwest Passage range up to 8-10 hours (for the FLIR-equipped CC-295 Kingfisher). Survivors may still be in frigid water or on exposed ice for 10 hours or more before they are located. Without an appropriate level of thermal protection and survival equipment designed for at least five days, an operation that begins as search and rescue is likely to become search and recovery.

The Polar Code requires vessels operating in polar waters to obtain a Polar Ship Certificate confirming that the ship, its crew and their qualifications, and its life-saving appliances meet the Code’s requirements. Polar certificates are issued by recognized organizations—classification societies such as the American Bureau of Shipping, Bureau Veritas, and Lloyd’s Register—acting on behalf of flag administrations. These societies have a duty to exercise due diligence before issuing certificates. For vessels intending to enter the Northern Canada Vessel Traffic Services Zone (NORDREG), these certificates must be submitted to Canadian authorities months in advance.

Transport Canada has indicated that it will increase inspections of vessels operating in the Canadian Arctic, consistent with recommendations from the Transportation Safety Board of Canada that call for more detailed inspections of passenger vessels entering Arctic waters. This enhanced oversight will encourage shipowners to ensure proper vessel design, that critical safety equipment such as forward-looking sonar is installed and operational, that crews are appropriately trained and certified, and that survival equipment can keep people alive for at least the minimum five-day rescue window.

Improved compliance with the Polar Code will reduce the likelihood of serious accidents and major environmental spills in a fragile arctic ecosystem with a short vertical food chain. The Code has now been in force for more than eight years. With its scope expanded to new categories of vessels that may be less familiar with polar hazards, it is time to strengthen awareness and increased enforcement in the Canadian Arctic.

Colonel (Retired) Pierre Leblanc is an experienced Arctic practitioner.

The opinions expressed herein are the author's and not necessarily those of The Maritime Executive.

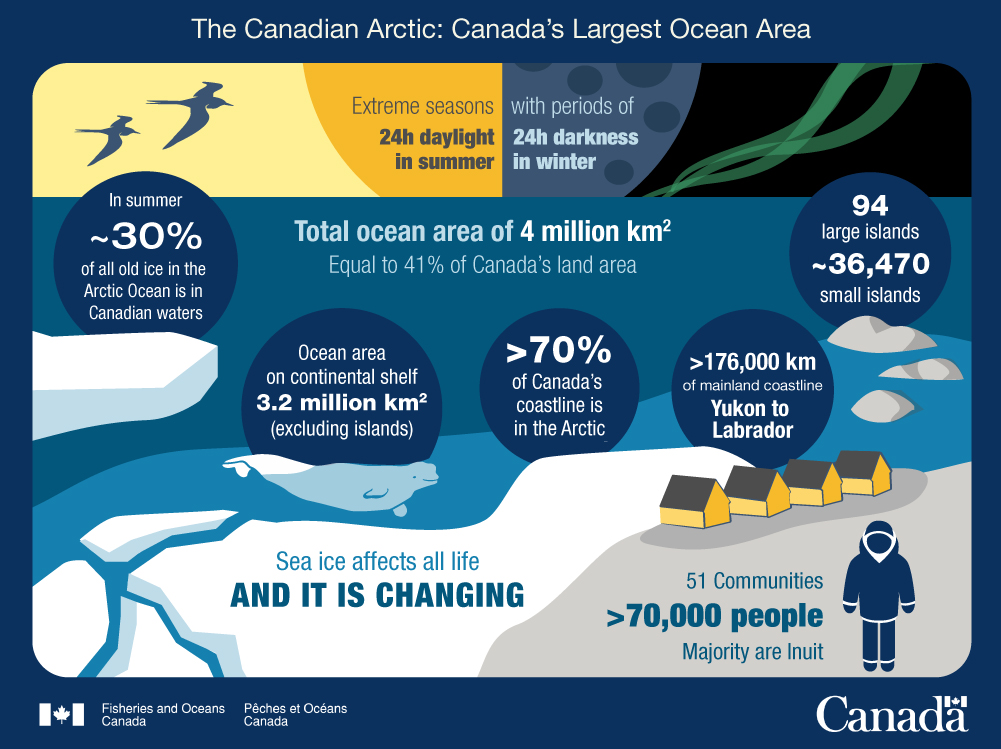

Infographic 1 — The Canadian Arctic: Canada's largest ocean area

Long description

An infographic shows a simplified Canadian Arctic coastal scene with various facts written in blue bubbles and throughout. A human figure stands by a small community on the shoreline where a beluga swims by the coastal ice. Several islands are depicted in the water along with pieces of ice. The sky at top is split between day and night. The left sky has a sun and is yellow with birds flying, the right sky is black with northern lights and a moon.

extreme seasons with periods of 24h daylight in summer 24h darkness in winter

total ocean area of 4 million km2

equal to 41% of Canada's land area

in summer ~30% of all old ice in the Arctic Ocean is in Canadian waters

ocean area on continental shelf 3.2million km2 (excluding islands)

>70% of Canada's coastline is in the Arctic

>176,000 km of mainland coastline Yukon to Labrador

South Korea is reporting that one of the knock-on effects of the stoppage of energy exports from the Middle East is threatening parts of its shipbuilding industry. The government has been working to clarify the extent of the problem while also supporting efforts to find alternative sources of naphtha, a refined crude oil product.

The imported naphtha is cracked at South Korea’s petrochemical plants to produce ethylene. While only accounting for a small portion of the market, Business Korea reports ethylene is critical to the shipbuilders, which use it to cut steel plates. Industry sources told the news outlet that without the chemical, it will be impossible for the shipbuilders to continue cutting steel.

The concerns began to intensify when South Korea’s largest petrochemical company, Yeochun NCC, declared “Force Majeure.” It said the problem was the supply of raw materials, and since then, at least three other leading producers, Lotte Chemical, LG Chem, and Hanwha Solutions, have also warned of potential supply problems.

South Korea’s Ministry of Trade, Industry and Energy held an emergency meeting on March 13 and launched an investigation to assess the short-term ethylene requirements and the amounts still on hand. The Ministry also organized a meeting between the shipbuilders and the chemical companies to plan shorter-term supply volumes.

The Ministry reported today, March 18, that its concerns have weakened but that it was continuing to work to ensure there would not be disruptions in the supply of the critical chemicals. A refined product, naphtha is also used in the production of propylene and high-grade gasoline, as well as an industrial solvent, dry cleaning agent, and cleaning solvent.

South Korea reports it is supporting the chemical companies’ efforts to secure alternative sources. It is contacting its overseas diplomatic missions and trade centers to secure alternate import supplies of naphtha.

The Deputy Prime Minister and Minister of Economy and Finance, Koo Yoon-chul, released a statement saying the government was also temporarily designating naphtha an “economic security item.” He also said they would be proactive in securing alternative import sources. Further, the government is placing export restrictions.

The potential disruption would come at a time when the shipbuilding industry is operating at a high capacity and working to stay ahead of competition from China. The yards have fully booked their building slots for years to come, and any delay in steel supplies could have a cascading effect on deliveries.

WAIT, WHAT?!!

Scotland’s CMAL Selects Chinese Yard to Build Freight Flex Ferries

CMAL has named a lead bidder to build its next generation freight flex vessels (CMAL)

The Scottish government-owned ferry company Caledonian Maritime Assets Limited (CMAL) reported it has concluded a project that began in September 2024 by selecting China’s Guangzhou Shipyard International as the lead bidder for two new ferries. The project is seen as a key part of the efforts to modernize and expand ferry operations in the northern part of Scotland, with the new vessels scheduled to run between Orkney and Shetland.

“GSI’s bid demonstrated a commitment to innovation and efficiency, and we are confident they will deliver a reliable, robust pair of vessels to support the Northern Isles Ferry Service for years to come,” said Kevin Hobbs, Chief Executive of CMA.

CMAL went public with the project in September 2024, reporting that the Scottish Government was supportive of the Northern Isles Freight Vessel Replacement Project. It said the goal was to increase capacity and improve reliability on the route served by vessels built in 1997 and 1999. CMAL said it had been actively looking to purchase second-hand tonnage for the Aberdeen to Kirkwall/Lerwick route, with three vessels taken forward to the purchase stage, but it had been unable to conclude purchases. While it was still exploring second-hand tonnage, it launched the newbuild project.

The tender was launched in September 2025, calling for two 140-meter (459-foot) long freight flex ferries. The company highlighted that it was an innovative design that would provide extra freight capacity and quicker crossing, while also being flexible to allow space for up to 200 passengers during peak travel periods.

Two yards in Turkey were among those invited to submit proposals, along with a partnership between Stena UK and a Chinese yard, and Guangzhou Shipyard. There was some concern that a UK yard had not even been invited to tender, but CMAL said that none of the UK yards had expressed interest or had the capabilities to build the ships.

Bids were assessed by an independent panel using a scale of 70 percent for technical capabilities and 30 percent for financial criteria. CMAL experts also participated in the process, and they said in the end, Guangzhou emerged as the clear winner.

The contract is valued at approximately £200 million ($265 million). No timeline was announced for the project, but previously CMAL had said it did not anticipate the ships would enter service before 2028 at the earliest.

“These replacement freight vessels will bring additional freight capacity, higher operating speeds, and the ability to carry up to 200 passengers on each vessel during peak times – helping address demand for car deck and cabin capacity on these routes,” said Scottish Cabinet Secretary for Transport, Fiona Hyslop. “This will enhance the efficiency and reliability of ferry services to better support the priorities of Northern Isles communities and businesses for years to come.”

CMAL is in a required 10-day standstill period after announcing the selection of the lead bidder. It then plans to complete the contract. The vessels, when they enter service, will be owned by CMAL and operated under contract by NorthLink Serco Ferries. CMAL currently has a fleet of 37 ferries, five of which are leased to Serco NorthLink Ferries for the Orkney and Shetland routes.

.jpg)

Stock image.

Stock image.

Stock image.

Stock image.