by John Rachel / April 10th, 2025

History adds clarity and perspective.

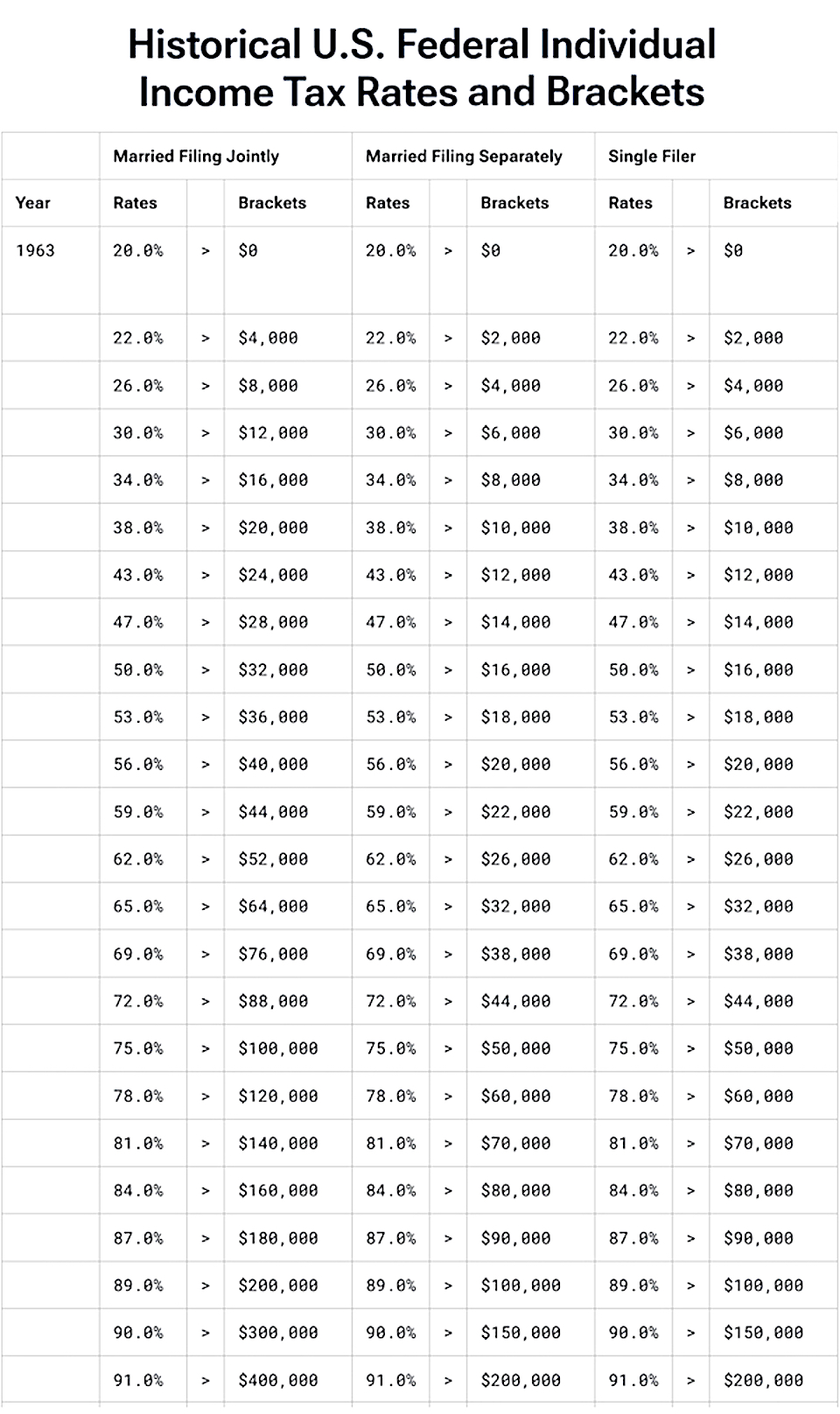

Here is the U.S. Federal Income Tax Rate Schedule from 1963.

Back then, if your gross income was $4,000 or less, you paid a 20% rate. If your gross income was $400,000 or more, on the earnings over $400,000 you paid a 91% rate. This scaling of tax liability is based on a straightforward, if highly contentious principle. The more you earn, the larger portion of those earnings should go toward the general funding of government and greater good of society. What is tendered in taxes is apportioned by ability to pay.

Granted, the above chart represents an extreme example of progressive taxation in our history. But it was very typical for almost two decades. The 91% rate was in effect 1946-1951 and 1954-1963. It was only exceeded at the end of WWII, 1944-1945 (94%) and two years in the 50s, 1952-1953 (92%).

Obviously, this inspired a lot of odium among the wealthy. They claimed such a contrivance is intrinsically flawed. Because we are all just individuals, one person equal to every other in the eyes of God, we all should receive equal treatment. Just because some individuals are cleverer or financially better off than others should not single them out to be penalized or punished. Conservatives insist that tax rates should therefore be regressive – no fancy formulas and sliding scales – as opposed to progressive. We currently have a progressive tax schedule, though not as drastic as in 1944-1963. The range is 10% to a maximum of 37%.

The most radically regressive counter to progressive taxation schedules proposed by extreme conservatives is the flat tax. We merely calculate how much money is needed and based on that, derive a single percentage, a tax rate applied across the board equally to everyone.

While it is elegantly simple and seems to smack of common sense, let’s do a simple thought experiment to see how it would play out in the real world.

For our example, let’s use a fairly modest flat tax rate of 30%.

Current HHS Poverty Guidelines state that for the 48 contiguous states and District of Columbia, the poverty threshold for a family of four is $30,000. Such a family unit would be required to pay $9,000 in federal taxes, leaving them $21,000 to cover all family living expenses for the year. That would be housing, food, transportation, clothing, utilities, health care, etc. All the necessities for basic subsistence for four people on $21,000. The brutal truth is they would be confronted with a choice between eating and having a roof over their heads. The average rent for the 48 contiguous states and District of Columbia is $1,095 per month. There goes $13,140 for the year. That leaves $5.38 per day to feed each member of the family. I guess if they ate dog food, they could survive. Of course, there would be no money for anything else.

Mind you, the figures just quoted are regarded by many credible COL sites as ridiculously conservative. One says a family of four needs $70,784 to survive. Another one puts it at $92,989, more than three times the poverty line figure we used as an example.

Moving on.

Jeff Bezos’ “annual earnings” is hard to nail down. It’s definitely a lot of money and one site claims it’s $64 billion. At the same time, he sometimes manages to pay little or no taxes. Considering how convoluted his personal finances are, capturing what his “taxable income” might be is like trying to grab grasshoppers in a field at night, blindfolded, using tweezers. For our purposes here, we’ll say the 30% flat tax applies to the whole $64 billion, which comes to $19,200,000,000. Brace yourselves and get out the tissues. I’m fighting my own tears as I report this. This means poor Mr. Bezos would be forced to eke out something resembling a decent life for the year on a mere $44,800,000,000. Of course, if he came up short, he could tap into his $161 billion of personal wealth. You know, to make the credit card payments on time and keep gas in the tank. Incidentally, as an aside, spending a million dollars a day, it would take over 440 years to spend Bezos’ fortune. How long would it take that family of four to go through the after-flat tax $21,000? Three months?

The obvious point is that debates on political philosophy are non-starters in the real world. Arguing over whether Jeff Bezos deserves to be so rich or not, or whether the Ten Commandments of neoliberal capitalism demand that the ultra-wealthy be handled with kid gloves when it comes to paying taxes, whether grotesque levels of wealth inequality are acceptable, is simply absurd. None of this plays in the real world. We have a country to run and lives to live. We have a nation to cohere and a large complex, highly diverse society to manage and nurture. Divided we fall. Fragmented we fail. The greater good may require the lesser good to be dragged kicking and screaming to embrace compromises which have the greater consensus. Who was it who said “democracy is messy”? The divine right of kings didn’t survive modern societal evolution. What place does the divine right of the rich have in a modern functioning democratic nation? I’m not being facetious. Do we have to enforce sensible, constructive tax policy with a guillotine?

By the way, there’s method to my madness here.

I’m focusing here on tax policy and its real-world outcomes, because I think that’s the perfect vehicle for contrasting our nation’s two major political religions: liberal vs. conservative. While recent dramatic shifts on a host of specific issues have caused some confusion as to what these terms precisely mean, they’re still useful in identifying the two main political tribes in the U.S. As they too often say, follow the money. The antithetical ways conservatives and liberals approach tax policy pretty much sums up their respective views on the proper relationship between government and the governed.

Having said that, I have no intention of attempting to arbitrate the opposing dogmas of sociopathic conservatism and bleeding-heart liberalism. Each is supported by meticulously cherry-picked facts and impeccable illogic. The simple, straightforward truth is that since these antagonistic positions are generated by completely different, totally incompatible premises and mutually exclusive world views, they inevitably arrive at very different places. There is no way to resolve the differences. However, as I hope you’ll discover by the end of this book, that is not to suggest that we as a society must remain mired in confrontation and paralyzed by gridlock.

Back to reality.

I’ve been citing “official” numbers in terms of what people are supposed to contribute in taxes. The vast majority of everyday citizens play by the book. The wealthy, despite their sanctimonious virtue signaling and interminable whining about onerous tax burdens, do not.

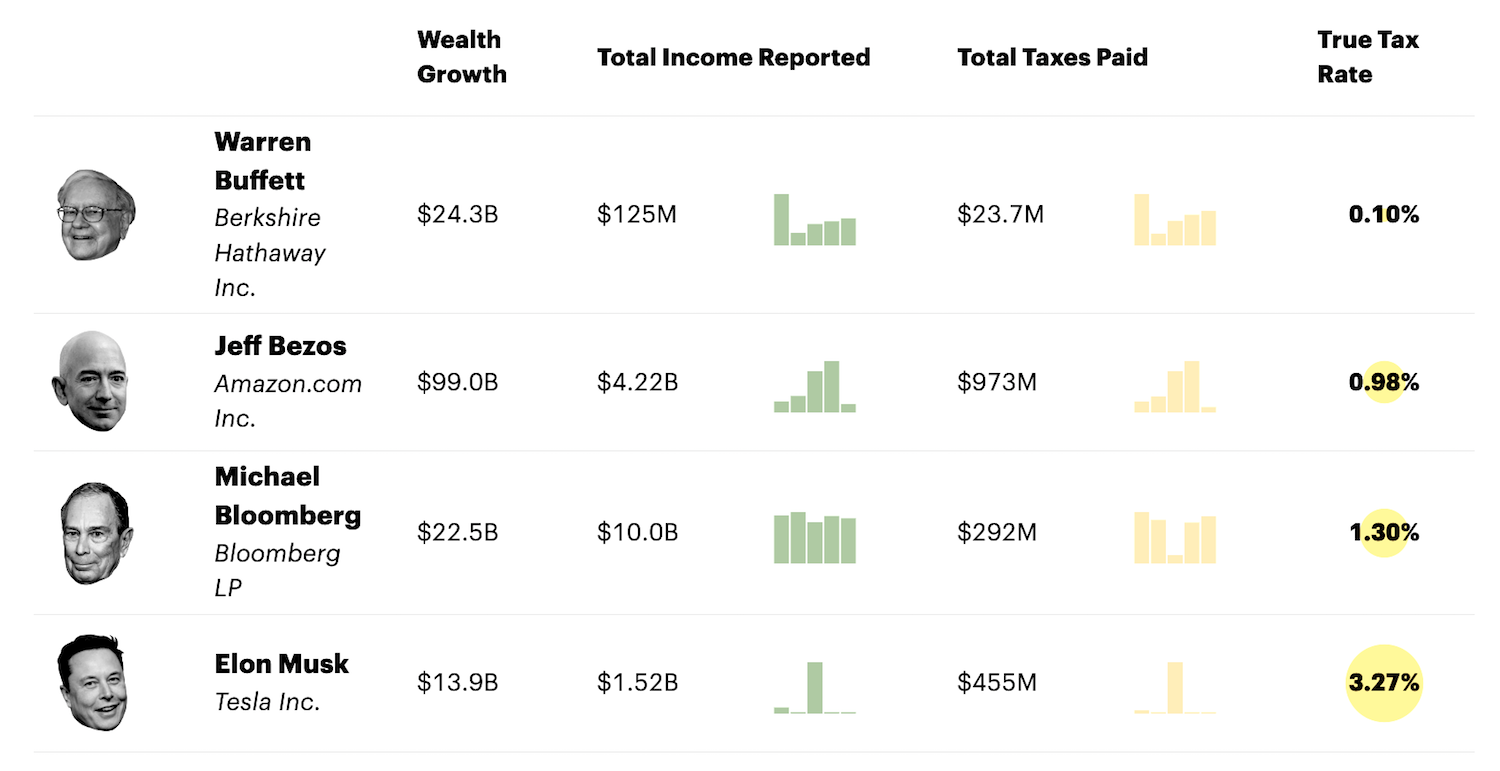

With armies of tax consultants and tax code attorneys at their disposal, the rich don’t pay anything close to the official rate. Just look at these four paragons of the neoliberal profit-over-people paradigm.

The agenda of the super-wealthy is not at all opaque or complicated. They want to keep as much money as they can by paying as little in taxes as possible. This dramatically and negatively impacts all of us. To keep their overall tax burden down, they aggressively cut spending. The list is chilling: Medicare for veterans; funding for schools with low-income students and students with disabilities; funding for pre-school and child care; meager allocations for WIC, i.e. nutrition assistance for women, infants and children; funding for Meals on Wheels which provides nutrition services for seniors; housing choice vouchers for seniors and veterans; funding for NIH, which means delays in cancer and Alzheimer’s research. Still high on the Republican agenda is the longstanding goal of cutting Social Security and Medicare.

Taking a sledgehammer to initiatives which offer comfort, relief and support, often to the most vulnerable and disadvantaged, appears to liberals as cruel, selfish, inhumane, unconscionable, vicious and diabolically insensitive. Yet – and it pains me to say this – it’s important to acknowledge that for conservatives, it’s none of the above. For them it’s merely being prudent and responsible, only paying for what we can afford. They insist we simply don’t have the money to take care of everyone in need. Of course, conservatives install a big, fat monkey wrench in the machinery. Relentlessly insisting on tax decreases guarantees we are always short on money. And the con doesn’t stop there. Their relentless calls to cut taxes is then given further justification. We’re told that letting the “job creators” keep more of their personal wealth and corporate profits is great for the economy. And a thriving economy eliminates the need for all those expensive social programs. Thus, the less the wealthy pay in taxes, the better off we all are. So the argument goes.

Quite a web of magical thinking being floated, for sure.

At the same time, it is powerful, persuasive magical thinking, propagated by well-funded think tanks, promoted by influential economists, reinforced constantly by toadying pundits and the wholly captured media. Understand, this assault on the common good has been underway for over five decades. The focus and hard work of this blitz shows. The wealthy have perfected their game, while the defenders of us everyday citizens have been left scrambling, often bickering among themselves like alley cats, thrown into disarray by getting pointlessly sidetracked – identity politics, though valid and important, is a perfect example of such squandering of energy and time – thus rendered incapable of formulating and agreeing on a coherent alternative vision, based on fairness and respect for the general welfare and common good. Or as with the Democratic Party, would-be reformers have simply been bought out.

We need a fresh start. We need to look at our situation with fresh eyes.

This is where the candidacy of Robert F. Kennedy Jr. came in. He was asking the right questions, the tough questions, the necessary questions.

What kind of country do we want to live in and what do we need to do to make that happen? In a true democracy, the ‘we’ runs the show. Everyone has to give, as well as take. Everyone has to make sacrifices. Everyone has to think in terms of the “everyone”.

Timeless inspiration helps.

“Ask not what your country can do for you. Ask what you can do for your country.” – John F. Kennedy, 01/20/61

This is a very tall order, both profound and fragile. Yet, it sounds as fresh and relevant today as it did sixty plus years ago when it was first spoken.

Though the election is behind us and Kennedy was forced to join the ranks of Donald Trump, we are still presented with the opportunity to meet that challenge.

RFK Jr’s message couldn’t be more timely or critical for our future. The posturing by both major parties is a deadly pas de deux that’s impoverishing everyday citizens, vanquishing the middle class, destroying the American dream, and further bloating the vast fortunes of the wdes – Republicans and Democrats – in a call for unity and a promise of hope. ealthy. It’s easy to blame just the Republicans for this, but Mr. Kennedy consistently reached out to both sides – Republicans and Democrats – in a call for unity and a promise of hope. [See “An Epistle to Robert F. Kennedy, Jr.— DV ed]

I only hope his enemies – the enemies of “the people” – are paralyzed and incapable of torpedoing what may be our last chance to save America. Time is not on our side.

R is for regressive.

R is for rapacious.

R is for ruthless.

This is an excerpt from my book, Electing A Kennedy Congress, a thoroughly misunderstood and maliciously denigrated attempt at restoring our country to a recognizable version of itself, one which aligns with the grossly misleading, totally fabricated image it peddles to its citizens and the world.

McKinley or Lincoln? Tariffs vs. Greenbacks

President Trump has repeatedly expressed his admiration for Republican President William McKinley, highlighting his use of tariffs as a model for economic policy. But critics say Trump’s tariffs, which are intended to protect U.S. interests, have instead fueled a stock market nosedive, provoked tit-for-tat tariffs from key partners, risk a broader trade withdrawal, and could increase the federal debt by reducing GDP and tax income.

The federal debt has reached $36.2 trillion, the annual interest on it is $1.2 trillion, and the projected 2025 budget deficit is $1.9 trillion – meaning $1.9 trillion will be added to the debt this year. It’s an unsustainable debt bubble doomed to pop on its present trajectory.

The goal of Elon Musk’s DOGE (Department of Government Efficiency) is to reduce the deficit by reducing budget expenditures. But Musk now acknowledges that the DOGE team’s efforts will probably cut expenses by only $1 trillion, not the $2 trillion originally projected. That will leave a nearly $1 trillion deficit that will have to be covered by more borrowing, and the debt tsunami will continue to grow.

Rather than modeling the economy on McKinley, President Trump might do well to model it on our first Republican president, Abraham Lincoln, whose debt-free Greenbacks saved the country from a crippling war debt to British-backed bankers, and whose policies laid the foundation for national economic resilience in the coming decades. Just “printing the money” can be and has been done sustainably, by directing the new funds into generating new GDP; and there are compelling historical examples of that approach. In fact, it may be our only way out of the debt crisis. But first a look at the tariff issue.

Trump Channels McKinley

Trump said at a 2024 campaign event, “In the 1890s, our country was probably the wealthiest it ever was because it was a system of tariffs.” And in his second inaugural address on January 20, 2025, he said, “The great President William McKinley made our country very rich through tariffs and through talent.”

That may have been true for certain industries, but it did not actually hold for the broader population. The Tariff Act of 1890, commonly called the McKinley Tariff because it was framed by then Representative William McKinley, raised the average duty on imports to almost 50%. The increase was designed to protect domestic industries and workers from foreign competition, but the 1890s were marked by severe economic instability.

The Panic of 1893 plunged the U.S. into a depression lasting until 1897. Unemployment soared to 18.4% in 1894, with over 15,000 businesses failing and 74 railroads going bankrupt. The stock market crashed, losing nearly 40% of its value between 1893 and 1894. Far from being the wealthiest era, this period saw widespread hardship that tariffs not only failed to prevent but exacerbated.

Farmers and factory workers were hit particularly hard. The McKinley Tariff raised the cost of imported goods, squeezing rural and working-class budgets. Farmers faced a deflationary spiral as crop prices plummeted. Real wages for industrial workers stagnated or declined, with purchasing power eroded from high tariffs inflating the prices of consumer goods.

In the 1860s, President Lincoln issued debt-free money in the form of unbacked U.S. Notes or “Greenbacks;” but new issues of Greenbacks were discontinued in the 1870s, and gold was made the sole backing of currency. The resulting economic distress fueled the Greenback movement, which sought a return to the “lawful money” issued by President Lincoln. The Greenbacks were considered lawful because they were issued directly by the government as provided in the Constitution, rather than by private banks.

The Greenback Party faded, but its policies were adopted by the Populist Party and were pursued by a grassroots movement called “Coxey’s Army.” It staged the first-ever march on Washington in 1894, seeking a return to the Greenback solution. The march was considered the plot line for the 1900 classic American children’s story, The Wizard of Oz, with the scarecrow as the farmers, the tin man as the factory workers, the lion as William Jennings Bryan, and Dorothy as populist leader Mary Ellen Lease. Like the powerless Wizard, then-President Grover Cleveland turned the marchers away at the gate. (For a fuller history, see my book, The Web of Debt.)

As with McKinley’s tariffs, President Trump’s tariffs are said by critics to be backfiring, contributing to a dramatic stock market drop and prompting retaliatory tariffs and trade withdrawals from other countries. Economists warn of broader fallout. According to a New York Times analysis on March 9, tariffs and retaliation could slash U.S. GDP growth by a full percentage point in 2025, and households are potentially facing an extra $1,000 annually in costs due to tariff-driven inflation. Internationally, the tariffs have triggered withdrawals and realignments. Reuters highlighted on March 10 that the U.S. stock market had lost $4 trillion in value as recession fears grew, and the S&P 500 lost $1.7 trillion just on April 3.

The Lincoln Alternative

Rather than alienating our trading partners and stressing investors and consumers, Trump could take a page from Abraham Lincoln’s playbook. Lincoln wasn’t opposed to tariffs. Campaigning for the Illinois state legislature in 1832, he said, “My politics are short and sweet, like the old woman’s dance. I am in favor of a National Bank, I am in favor of the Internal improvement system, and a high protective tariff. These are my sentiments and political principles.” The tariffs were intended to protect the country’s fledgling industries from foreign competition, but they needed a national bank to provide the credit necessary to flourish.

President Washington set the model with the First U.S. Bank, which was essentially a national infrastructure and development bank. According to Treasury Secretary Hamilton’s Reports to Congress — the First and Second Reports on Public Credit, the Report on Manufacturing, and the Report on a National Bank — the Bank’s primary purposes were to manage the government’s Revolutionary War debt by turning it into a productive asset, using debt-for-equity swaps to provide capitalization; to issue a uniform national currency; and to provide credit for infrastructure and manufacturing, spurring economic development at a time when capital was scarce.

The Second U.S. Bank followed that model. But President Andrew Jackson declared war on the Bank, and its charter expired in 1836. During the ensuing “Free Banking Era” (roughly 1837 to 1863), the country was left without a national currency or a national bank. Individual banks chartered by states could issue their own banknotes, usually redeemable in precious metals held in reserve by the issuing bank. It was a chaotic system, with the value of the notes varying according to the distance of the customer from the bank. Distance mattered in case the bank ran out of precious metals in a bank run, a common occurrence.

Lincoln didn’t get his national bank, but he did sign the National Banking Acts of 1863 and 1864, which stabilized the chaotic money supply with a single currency backed by precious metals and federal securities; and he avoided trapping the country into a crippling debt at exorbitant interest rates by issuing debt-free Greenbacks to fund the Civil War. With this financing, Lincoln’s government not only won the war but funded major infrastructure and development, including completing the transcontinental railroad that connected the country from coast to coast.

Greenbacks constituted 40% of the national currency in the 1860s. Today, increasing the money supply by 40% would mean adding about $8.8 trillion. Yet this massive money-printing during the Civil War did not lead to hyperinflation. Greenbacks suffered a drop in value as against gold, but according to Milton Friedman and Anna Schwarz in A Monetary History of the United States, 1867-1960, this was not due to printing money. Rather, it was caused by trade imbalances with foreign trading partners on the gold standard. And price inflation abated after the war.

Today’s Treasury Could Follow Lincoln’s Model

The most direct way for the present Treasury to solve its debt problem is to follow our first Republican president and issue currency directly. One possibility is to issue trillion dollar coins. The Constitution provides, “Congress shall have the power to coin money and regulate the value thereof.” That approach and its constitutionality is detailed here. President Lincoln solved his debt crisis with paper U.S. Notes or Greenbacks, a move that was upheld by the Supreme Court.

Economists will cry that money printing on a major scale will result in hyperinflation, devaluing the currency and driving up consumer prices. But that did not occur with the Fed’s QE following the 2008-10 Global Financial Crisis, and the inflation objection can be overcome if the new money is used specifically for expenditures on infrastructure and new goods and services. When supply and demand remain in balance, prices remain stable, and the currency can retain its value.

To economists, “inflation” means an inflated money supply; but “too much money” drives up prices only when “chasing too few goods.” The price of eggs recently doubled, but it wasn’t because the number of customers demanding eggs suddenly doubled. It was because the supply of eggs was radically reduced by the culling of over 20 million egg-laying chickens due to the bird flu scare. The obvious solution is to increase the chicken population. Increase supply to meet demand.

Some Historical and Contemporary Examples

China transformed itself from one of the poorest countries in the world to global superpower in only four decades. Where did it get the money? Mainly, it just issued the yuan, as shown in my last article here. The chart in that article from Trading Economics is now behind a paywall, so here I will use the dates and figures that are still publicly visible on their web page. Citing the People’s Bank of China, it states, “Money Supply M2 in China averaged 93486.82 CNY Billion from 1996 until 2025, reaching an all time high of 320526.31 CNY Billion in February of 2025 and a record low of 5840.10 CNY Billion in January of 1996.” 320526.31 divided by 5840.10 = 54.88, which can be rounded to a factor of 55 or 5500%.

At the same time, the U.S. money supply increased by only 600% ($3647.9 in Jan. 1996 to $21,671 in Feb. 2025). The U.S. money supply is increased by bank lending, so 600% can be considered an average increase from that source over 29 years. That leaves a 4900% increase in the Chinese money supply from “money printing,” through mechanisms explained in my last article. Despite this dramatic increase in “demand,” price inflation remained relatively stable and was actually lower overall than in the U.S. The new money created new GDP, which shot up along with the money supply.

In the U.S. from 1930 to 1945, the money supply approximately doubled to finance economic recovery and the war effort. Consumer prices swung from deflation during the Depression to inflation during World War II, but the overall average remained low. The new money was largely injected through loans from the Reconstruction Finance Corporation, a federal agency that took on the role of an infrastructure bank. The debt to GDP ratio in 1946 reached a high of 121% — as high as in recent years — but it dropped down to a very manageable 31% by 1974, not because the debt was paid down but because GDP increased from the money poured into manufacturing and infrastructure in the 1930s and ‘40s.

Germany began the 1930s literally bankrupt. New money was injected in the form of a labor-backed currency (“Mefo bills”) issued by the government, directed specifically to manufacturing and infrastructure. MEFO bills allowed billions in military and public-works funding, but inflation did not increase.

Contrary Examples

What about the hyperinflation of Weimar Germany in the 1920s, or the Zimbabwe hyperinflation of 2007-09? According to Prof. Michael Hudson, who has studied this issue extensively, “Every hyperinflation in history stems from the foreign exchange markets. It stems from governments trying to throw enough of their currency on the market to pay their foreign debts.” The new money did not go into creating new goods and services. It was used to pay foreign debts in a currency over which the country had no control. This left the domestic currency vulnerable to rampant short selling by speculators, resulting in serious devaluation and hyperinflation.

Commentators often point to the 2020 COVID-19 payments to consumers — the stimulus checks under the CARES Act and subsequent relief packages — as the culprit driving up prices in the following years. The assumption is that demand outstripped supply purely because people had more cash to spend. Personal disposable income did spike by about 10% in 2020; but in a properly functioning economy, higher demand spurs production. That did not happen in the COVID-19 years because supply could not respond.

Nearly 100,000 small businesses were closed permanently due to COVID-19 by mid-2021. Meanwhile, global supply chains were clogged. The Los Angeles and Long Beach ports saw container ship wait times jump from days to weeks, while production was crippled by factory shutdowns in Asia along with labor shortages. A 2024 Brookings analysis concluded that “COVID-19 inflation was a supply shock.” Again the remedy is to increase supply along with demand (money).

How to Ensure that New Money Is Channeled into New GDP

The economic miracles of China, Germany and the U.S. following the Civil War and Great Depression demonstrate that governments can at least double the money supply—sometimes multiplying it manyfold, as in China — without spiking consumer prices, provided new money fuels infrastructure and production to match money supply growth with GDP growth.

In China, this is enabled by a sprawling network of over 2,000 publicly-owned banks, in addition to the three federal policy banks including China Development Bank (CDB). The Big Four national banks are predominantly owned by the central government, through entities that sell shares to private investors but retain government control, while thousands of city and rural banks are controlled by local governments at the county level. These institutions channel credit into local projects, amplifying economic output.

At the national level, China’s three giant policy banks funnel credit into the federal government’s long-range plans for infrastructure and development. This multi-year focus has been called a major advantage of Chinese “command capitalism” over Western “stakeholder capitalism,” in which private companies are required to focus on short-term profits for their stakeholders. However, the United States could form a publicly-owned national infrastructure bank like the CDB with long-range capabilities, on the model of Hamilton’s First U.S. Bank and Roosevelt’s Reconstruction Finance Corporation. The latter was not actually a depository bank but was a federal agency formed by President Hoover, expanded by Roosevelt’s government into a massive credit-generating machine for infrastructure and manufacturing.

HR 4052, titled “The National Infrastructure Bank Act of 2023,” is currently before Congress and has 47 co-sponsors. Like Roosevelt’s Reconstruction Finance Corporation, the bank is designed to be a source of off-budget financing, without adding new costs to the federal budget. For more information, see https://www.nibcoalition.com/.

At the local level, state-owned infrastructure banks could do something similar. Currently our only state-owned bank is the Bank of North Dakota, but it is a very successful model that not only funds state infrastructure and development but generates income for the state and acts as a “mini-Fed” for local banks. For more information, see the Public Banking Institute website.

The U.S. could also issue money directly, as Lincoln did in the 1860s with Greenbacks, and the German government did in the 1930s with Mefo bills, among other examples. The German government avoided speculative exploitation of the funds by issuing Mefo bills as payment for specific industrial output. The British did something similar in the Middle Ages with tally sticks issued as payment for goods and services, a system that lasted over 600 years. Keeping federal payments honest and transparent is possible today with modern IT technology, one of the assigned tasks of the DOGE IT team.The possibilities were framed in an editorial directed against Lincoln’s debt-free Greenbacks, attributed to the 1865 London Times (though not now to be found in its archives):

If that mischievous financial policy which had its origin in the North American Republic during the late war in that country, should become indurated down to a fixture, then that Government will furnish its own money without cost. It will pay off its debts and be without debt. It will become prosperous beyond precedent in the history of the civilized governments of the world. The brains and wealth of all countries will go to North America. That government must be destroyed or it will destroy every monarchy on the globe.

Without trade wars or kinetic wars, President Trump is in a position to achieve the vision for which President Lincoln might have taken a bullet, through the time-tested expedients of publicly-issued money and publicly-owned banks.