It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Monday, April 06, 2026

Pakistan Emerges as Key Mediator in Push to End Hormuz Crisis

The United States and Iran have both received via Pakistan a plan for an immediate ceasefire that could reopen the Strait of Hormuz, Reuters reported on Monday, citing a source with knowledge of the proposals.

The plan could come into effect as early as today and allow an opening of the Strait of Hormuz, the world’s most vital oil and LNG chokepoint, according to the Reuters source.

Under the provisional so-called ‘Islamabad Accord’, an immediate ceasefire could come into effect, allowing for talks to continue for up to another 15-20 days for a final comprehensive agreement, the source told Reuters.

On Sunday, U.S., Israeli, and regional sources told Axios that the United States, Iran, and mediators in the region are discussing details and terms of a potential 45-day ceasefire.

According to Reuters’ source, Field Marshal Asim Munir, the chief of Army Staff of Pakistan, has been in contact “all night long” with Iran’s Foreign Minister Abbas Araqchi, U.S. Vice President JD Vance, and special U.S. envoy Steve Witkoff.

Reports of proposed ceasefire plans emerged hours after U.S. President Donald Trump threatened Iran, again, in an expletive-ridden post on Truth Social, demanding the immediate opening of the Strait of Hormuz, which was open to free vessel traffic before February 28.

“Tuesday will be Power Plant Day, and Bridge Day, all wrapped up in one, in Iran. There will be nothing like it!!! Open the Fuckin’ Strait, you crazy bastards, or you’ll be living in Hell - JUST WATCH! Praise be to Allah,” Trump wrote on Easter Sunday.

Iran dismissed the threat and threatened in turn the U.S.

Senior Iranian military officer, General Ali Abdollahi Aliabadi, said in response to Trump’s threat that “the gates of hell will open for you” while official Iranian accounts on social media openly mocked Trump’s threat.

“We’ve lost the keys,” the Iranian Embassy in Zimbabwe posted on X in response to the demand to open the Strait of Hormuz.

Jibes aside, even an immediate and unconditional re-opening of the Strait of Hormuz would be followed by months needed to normalize flows of oil, petroleum, products, LNG, ammonia, sulfur, helium, and other products key to critical supply chains.

By Tsvetana Paraskova for Oilprice.com

U.S. Battery Expansion Surges Ahead of Demand Curve

U.S. battery production capacity is growing so rapidly that it may exceed domestic demand by 2026

Government incentives under the Inflation Reduction Act have driven major foreign investment and reduced manufacturing costs

Despite expansion, the U.S. remains heavily dependent on China for critical battery materials and supply chain inputs

The United States is rapidly becoming a major international battery manufacturing power, as it works to compete with other producers, such as China. The battery manufacturing industry is forecast to grow so much in the coming years that supply may soon outstrip demand.

Demand for batteries in the United States has grown significantly in recent years, with demand for energy storage expected to increase by 21 percent this year. This has been driven primarily by the increase in the deployment of renewable energy capacity across the U.S., which requires battery storage to ensure a stable supply of energy through the day and night. Going forward, the accelerated rollout of data centres is expected to drive demand even further.

The U.S. battery manufacturing industry has been rapidly growing since the passing of the Inflation Reduction Act (IRA) in 2022, under President Biden. The IRA introduced incentives for both domestic battery manufacturers and for storage developers who use U.S.-made products. In addition to supporting the accelerated growth in the U.S. renewable energy and cleantech market, increasing domestic battery production has helped reduce the country’s reliance on foreign supply chains, and, particularly, on Chinese batteries

According to data from the Centre on Global Energy Policy, the IRA awarded credits for local investment and production that drove down battery-making costs by as much as 30 percent. This helped to attract foreign investment to the U.S. market and was particularly appealing to Korean producers who aimed to compete with China in a market in which they did not have access.

Last year, U.S. production plants had the capacity to manufacture around 70 GWh of complete grid storage systems annually, a figure that could rise to 145 GWh this year. This means that the U.S. can now produce enough batteries to meet domestic demand. In 2026, around 28 percent of new U.S. power plant capacity is expected to be dedicated to battery production, with domestic production expected to outstrip demand by the end of the year.

Noah Roberts, the executive director of the U.S. Energy Storage Coalition, stated, “For the first time, the United States now has the capacity to supply 100 percent of domestic energy storage project demand with American-built systems. That is a fundamental shift from where we were just a year and a half ago, when the majority of battery storage systems were imported.”

The current production capacity marks a significant shift from the situation just two years ago, when the U.S. had almost no factory capacity for battery cells designed for grid usage, which are different to those used in electric vehicles. The industry growth has been supported by major investments from foreign companies, such as LG and Samsung. South Korean producers have invested around $20 billion in expanding capacity and are expected to contribute over two-fifths of the growth in production between 2025 and 2029, Benchmark Minerals estimated in 2024.

In 2025, Korea’s LG Energy Solution Vertech developed a dedicated cell production line for grid storage in Holland, Michigan, expanding production capacity to 16.5 GWh through a $1.4 billion project. The firm is expected to continue growing its manufacturing capacity across North America to reach 50 GWh by the end of the year. LG had previously focused on producing EV batteries at the plant, but with the EV market struggling and the demand for grid-scale batteries increasing, LG shifted lanes.

Despite the massive growth in the U.S. battery manufacturing capacity, the country still relies heavily on imports of high-value battery materials from countries such as China. For storage alone, the U.S. has imported over $100 billion in batteries and components since 2021, according to S&P Global, around half of which came from China. According to the International Energy Agency (IEA), “The lack of investment in midstream supply chains in these markets poses a growing risk to global supply security.

The IEA adds that production capacity and technical expertise for essential components, such as active materials and their precursors, remain heavily concentrated in China. Korea and Japan are the only other countries with notable midstream battery industries, offering opportunities to diversify some component sources. Nearly all batteries used for power grids rely on China for at least one step of their supply chain.”

With the introduction of high tariffs on multiple Chinese products under the Trump administration, there are always fears of retaliatory duties from China. Beijing still controls supply chains for the raw materials, such as graphite, meaning that battery producers in the U.S. must maintain good relations with their Chinese counterparts, which could be hindered if political relations between the two countries become strained.

The United States has significantly increased its battery manufacturing capacity in recent years, shifting from a focus on EV battery production to grid-scale storage. Significant incentives, introduced by the Biden administration, have encouraged high levels of foreign investment in the sector, particularly from Korean companies. However, the continued dependence on China and other countries for raw materials presents a risk to the supply chain, particularly with the ongoing geopolitical tensions and conflicts being seen across the globe.

By Felicity Bradstock for Oilprice.com

U.S. Auto Industry Proposes Vehicle Fee to Replace Gas Tax

Rising EV adoption in the United States is reducing gas tax revenues, putting the Highway Trust Fund under increasing financial strain.

The auto industry proposes replacing the outdated gas tax with a weight-based vehicle fee so all vehicles contribute to road funding.

The shift is driven by long-term funding gaps, inflation, and the transition away from gasoline-powered cars, which threatens infrastructure financing.

The growing share of electric vehicles and the expected increase in EV sales this year amid soaring gasoline prices are reducing the revenues for the U.S. Highway Trust Fund, which pays for America’s roads.

Most of the revenue for the fund comes from the 18.4% per gallon federal gas tax, which hasn’t been changed since 1993.

Yet, over the past 30 years, the funding for the trust fund has been declining, due to inflation and the fact that EVs now represent 2.5% of total light-duty vehicles in operation in America, and the market share of internal combustion engine vehicles has dropped by 24 percentage points since 2016.

The new oil crisis and U.S. national average gasoline price topping $4 per gallon could prompt more potential buyers to look to purchase an EV—whose owners, obviously, don’t pay the federal gas tax.

More EVs means lower revenues for the Highway Trust Fund, which is teetering on bankruptcy every year and needs to be regularly backfilled by Congress. Therefore, the current oil crisis “shows why it’s time to dump the gas tax,” John Bozzella, president and CEO of Alliance for Automotive Innovation, said this week.

The auto industry trade association, which represents most U.S. and foreign automakers in America, proposes to scrap the federal gas tax and replace it with a single fee on every vehicle based on weight.

“This policy would guarantee every vehicle on the road contributes something to maintaining America’s transportation network,” Bozzella wrote in a blog post this week.

“We can drive with the devil we know… or get behind a new policy that requires every vehicle on the road to contribute to the upkeep of America’s roads and bridges.”

The auto industry group’s latest analysis of U.S. EV data showed at the end of March that a total of 164 electric models are now available for sale in the U.S. Although EV sales fell last year from 2024, electric vehicles represented 9.6% of new U.S. light-duty vehicle sales for full-year 2025.

EVs now account for 2.5% of total light-duty vehicles in operation in the United States, while the market share of internal combustion engine vehicles, whose owners pay the federal gas tax, has decreased by 24 percentage points since 2016.

In January 2026, hybrids were 19% of all light-duty vehicle sales, the Alliance’s CEO Bozzella said.

As gasoline prices spike due to the war in the Middle East, the U.S. might see an additional shift in the marketplace toward EVs and hybrids, the industry group said.

“Online searches for EVs are up 20 percent since the conflict began,” Bozzella wrote.

The Alliance for Automotive Innovation argues that a single, weight-based vehicle fee can fully fund the Highway Trust Fund, unlike the gas tax.

For over 20 years, transportation spending has exceeded the dedicated revenue flowing into the trust fund as the gas tax has failed to keep pace with inflation, and vehicles are becoming more fuel-efficient, the Committee for a Responsible Federal Budget says. It estimates that the Highway Trust Fund would be insolvent by 2028.

Since increasing the federal gas tax is a nonstarter in any Congress, the solution to fix the problem with the dwindling revenues for the Highway Trust Fund is to replace it with a fee for every vehicle using the road, regardless of how it’s powered/fueled, the Alliance for Automotive Innovation says.

Bozzella notes that the proposed weight-based vehicle fee is simple, and nobody would need to track how many miles you drive, like some proposals out there, to determine what you pay.

“Beyond that, it’s an overdue policy change that insulates infrastructure spending – a $3.5 trillion national need over the next decade – from gas price shocks and inevitable geopolitical disruptions,” Bozzella noted.

Beijing is studying Operation Epic Fury closely, watching US precision strike capabilities, munitions depletion rates, and the administration's decision-making process in real time.

Retired Maj. Gen. Mick Ryan says Trump's impulsiveness is genuinely unsettling for Chinese war planners, but Washington's one-war capacity and stripped-down NSC process may offset that deterrent effect.

With US missile interceptor stocks being drained in the Middle East, some analysts warn a strategic window for Beijing could be opening, particularly if Washington remains distracted through the midterm election cycle.

Five weeks into the US-Israel air campaign against Iran, the world is tallying the economic wreckage: Brent crude at $114 a barrel, the Strait of Hormuz effectively closed to commercial traffic, and the International Energy Agency calling it the largest supply disruption in the history of the global oil market. Beijing is watching all of it. And not just the energy markets.

Operation Epic Fury, launched Feb. 28, has given China’s military planners an unprecedented real-time window into how the United States wages high-end warfare, according to Mick Ryan, a retired Australian major general and senior fellow at the Lowy Institute in Sydney. “The US military is still a very powerful organization,” Ryan told RFE/RL this week. “It can deploy overwhelming force and conduct sustained precision operations, at least from the air and from the sea.”

That part is not reassuring to Beijing. But the fuller picture is more complicated, and potentially more useful to Chinese planners.

Ryan says the Trump administration has demonstrated a critical limitation alongside its firepower: it can manage one major war at a time, and it has stripped out much of the institutional decision-making architecture that would normally govern a conflict of this scale. “These decisions look to be being made much more on impulse,” Ryan said, pointing to what he described as shifting and inconsistent strategic objectives since the campaign began.

For Xi Jinping and the People’s Liberation Army, that combination — overwhelming capability paired with constrained strategic bandwidth — is worth studying carefully. If Beijing has a clearer strategy than Washington does, Ryan argues, that gap matters as much as any hardware comparison. “Strategy is even more important than battlefield performance,” he said. “Having the right strategic assumptions and the right strategic decision mechanisms for executing that strategy is something the Chinese might think that they’re better at than the United States at the moment.”

The strategic implications extend well beyond tactics. China receives roughly a third of its crude oil through the Strait of Hormuz. The closure has forced Beijing to scramble for Russian and alternative supplies even as it publicly opposes the war and calls for de-escalation. Iran, notably, granted Chinese-flagged vessels passage through the strait on March 26, a gesture that underscored the careful line Beijing is walking: rhetorical opposition to Washington, functional diplomacy with Tehran, and eyes fixed on the Taiwan question.

China’s military budget grew 7% in 2026 to roughly $277 billion, and its official military media outlet has published formal analyses of the conflict’s lessons, covering everything from the role of AI in US targeting to the effectiveness of leadership decapitation strikes. The PLA had drones mounted on armored vehicles at last year’s military parade — Ryan says those were Ukraine lessons absorbed and adapted, and the Iran war is only adding to the pile.

One of the more alarming data points for Western defense planners is the pace of US missile interceptor depletion. American and allied forces have expended an estimated 2,000 interceptors in the campaign so far, and production rates are nowhere near sufficient to replenish them quickly. Some analysts have begun describing that gap explicitly as a strategic window. “That may be the best time for Beijing to strike,” wrote defense analyst David Axe, noting that the US “simply won’t have enough interceptors” if another front opens.

Ryan is more cautious about the immediacy of that threat. Trump’s unpredictability, while analytically frustrating for Beijing, is also a genuine deterrent. Unlike any of his predecessors, Trump cannot be reliably war-gamed. “The Chinese can’t really war game what his reaction to any kind of event might be because he just really is all over the place,” Ryan said. That uncertainty, he argues, probably induces caution in Xi.

Still, Ryan sees two scenarios gaining traction in Chinese strategic planning. The first: a grand bargain between Trump and Xi in which Washington signals it would not defend Taiwan militarily. The second: a swift, decapitating military strike designed to outpace any US response. Neither requires Beijing to be reckless. Both require Beijing to see an opening.

The congressional midterm cycle, running through October and November, could provide one. A Trump administration managing a protracted Middle East campaign, depleted munitions stocks, and an increasingly hostile domestic political environment is a different adversary than one operating at full capacity and full attention.

Taiwan is not sitting still. Taipei’s defense ministry submitted a report to lawmakers in March outlining the “T-Dome” layered air-defense architecture it is rushing to complete, drawing explicit lessons from the Iran and Ukraine wars on the need for low-cost interceptors capable of handling drone swarms. The debate over a nearly $40 billion special defense budget is ongoing in the legislature, with opposition lawmakers raising questions over cost and feasibility.

As for how Xi is reading the broader picture, Ryan’s read is that the Chinese leader sees his long-standing narrative confirmed: the West in decline, US alliance systems fraying, and Washington’s credibility with allies eroding. “Whether that’s right or not remains to be seen,” Ryan cautioned. “But I think from his perspective, that’s probably what he sees.”

The war in Iran has not settled anything about Taiwan. But it has handed both sides new information, and neither is ignoring it.

The U.K. is pushing G7 nations to speed up clean energy adoption to reduce exposure to volatile fossil fuel markets.

New data questions the effectiveness of North Sea oil and gas expansion, reinforcing the case for renewables.

The Iran-related disruption and Hormuz blockage highlight the urgency of diversifying global energy systems.

Britain has urged some of the world’s biggest powers to adopt clean energy at a faster pace to boost energy security during a time of geopolitical turmoil. The United Kingdom’s Chancellor of the Exchequer, Rachel Reeves, appealed to world leaders to accelerate the global green transition during the G7 Foreign Ministers’ meeting, held in France from 26th to 27th March.

The Group of Seven (G7) wealthy nations includes the U.S., Britain, Canada, France, Germany, Italy, and Japan, along with the European Union. Reeves attended the conference alongside U.K. Energy Minister Ed Miliband, who is well-known for his staunch support for renewable energy sources.

Ahead of the G7 meeting, Reeves told journalists, “As we move faster on renewables and nuclear, our partners in the G7 must do the same – because staying stuck on the rollercoaster of global oil and gas prices will help nobody.” She added, “That transition is strongest when countries act together. By working across the G7, we can accelerate investment and build momentum. Energy bills are coming down for families this week thanks to the actions of this Labour government – action that was opposed by the Tories and Reform.”

Reeves has been strongly criticised by the U.K. Conservative Party (Tories) and the right-wing Reform Party for her vocal opposition to new fossil fuel projects. The Chancellor said that she turned down calls from the Conservatives to issue new oil and gas licenses in the North Sea as she believed they would not protect the U.K. from further energy shocks or drive down consumer energy bills. Since coming into government in 2024, Labour has banned new oil and gas licensing to focus on growing Britain’s renewable energy capacity, a move that has been widely welcomed by economists and climate experts.

Meanwhile, new evidence suggests that hundreds of North Sea licences granted by the Tories have, so far, produced just 36 days of gas. Research conducted by the energy consultancy Voar and the campaign group Uplift shows that between 2010 and 2024, the Conservative government approved hundreds of new North Sea oil and gas licences in seven licensing rounds. The report suggests that the 20 new and relicensed fields that have the potential, over their life span, to provide enough gas to supply the U.K. for half a year, have provided just 36 days of extra gas to date.

This has led many to doubt the effectiveness of the Conservatives' and Reform’s calls for new oil and gas drilling in the North Sea, as a means of boosting energy security and driving down energy bills, particularly as many of the U.K.’s oil reserves have long been depleted. Meanwhile, Reeves has accused the Tories and Reform of chasing headlines rather than addressing the root causes of energy security.

Some have already suggested that the current geopolitical challenges may be the wake-up call the world needs to take the importance of a more diverse energy mix seriously. The ongoing war in Iran has caused the largest oil disruption in history, according to an analysis by consulting firm Rapidan Energy. With the global trade significantly impeded by the almost complete closure of the Strait of Hormuz – a key trade corridor connecting the Persian Gulf with the Gulf of Oman and the Arabian Sea, the world’s ongoing dependence on fossil fuels has become evident.

Sam Butler-Sloss, the research manager at global energy thinktank Ember, told journalists, “The Iran crisis accelerates the shift to renewables and electrification. High fossil prices drive switching, making already cheap electrotech even more competitive.” Butler-Sloss added, “In the old fossil fuel world, energy security meant diversifying fuel supply. With electrotech, nations now have the tools to increasingly eliminate imported fuels altogether.”

Meanwhile, the International Energy Agency (IEA) is pushing harder than ever for countries to deploy more green energy capacity, as well as strengthen their energy supply chains, by reducing reliance on foreign powers for key materials and components. “I expect one of the responses to this crisis will be [an] acceleration of renewables. Not only because they are helping to reduce the emissions but also, they are a homegrown domestic energy source,” the IEA’s Executive Director, Fatih Birol, said during a press event in March.

It is still unclear whether the ongoing Middle East conflict will be enough of a reason to pursue a new era of green energy revolution, as was seen during and following the Covid-19 pandemic; however, some powers are pushing for an accelerated rollout of renewable energy to boost energy security. As the U.S. shifts away from an energy policy focused on green transition, the U.K. has stepped up to the global stage to encourage the world to diversify its energy mix, to reduce reliance on fossil fuels and help avoid another global energy crisis.

By Felicity Bradstock for Oilprice.com

Global Fuel Shortage Pushes Governments Toward Demand Controls

Fuel rationing is spreading across Asia and Europe as supply losses mount, raising fears of a prolonged energy crisis.

High prices and shortages are triggering demand destruction, particularly in Asia and Europe.

Both governments and markets are forcing reduced consumption, likely hurting the global economy.

This week saw something that does not happen very often. WTI, normally trading at a discount to Brent crude, moved higher than the North Sea-focused benchmark. Traders explained it with fears of tight supply in the immediate term and some relief later this year. Some, however, doubt this relief would come soon enough to avoid something few like to talk about: demand destruction.

Indonesia has started rationing fuel, capping daily fuel purchases to 50 liters per car for private consumers and sending civil servants to work from home to conserve fuel. Thailand is preparing its own fuel rationing plans. In Bangladesh, rations are in effect, universities have closed, and the country is nevertheless close to running out of fuel, as it imports 95% of what it consumes.

The rationing is spreading to Europe as well. Slovenia became the first European country to impose fuel rations at the same 50-liter level as Indonesia. In fairness, this amount of fuel for personal use on a daily basis is not really a meaningful ration since very few people consume a full tank of gasoline or diesel on a daily basis unless they travel for work purposes. But the move could be seen as symbolic, and the start of demand management measure should the fuel supply situation get worse, which is quite likely.

In mid-March, Kpler reported that the cumulative oil production losses from the U.S.-Israel war against Iran had reached 133 million barrels. Daily production was down by 10.7, which could reach 11.5 million barrels daily by the end of the month—and quite likely did. But as the war continues, oil supply losses would only grow. If hostilities are not over by the end of this month, the losses may well reach the amount that the International Energy Agency said it would release to fill the supply gap, namely 400 million barrels.

Meanwhile, diesel futures in Europe hit $200 after news broke that three tankers carrying diesel from the United States to Europe had diverted to Asia. Calls have started for fuel rationing in the European Union, and the EU’s energy commissioner just admitted to the Financial Times earlier today that rations are being considered as an option to manage demand for energy in a context of shortages. “This will be a long crisis ... energy prices will be higher for a very long time,” Dan Jorgensen told the FT.

Demand destruction is a concept that the oil and gas industry is quite familiar with and has every reason to dislike. Demand gets destroyed either when an unexpected event forces people to stop consuming oil and gas, or when the price becomes too high, making oil and gas simply unaffordable. The first scenario played out in 2020 when the world went into lockdown to avoid mass infection with COVID-19. The second is playing out right now. With over 11 million barrels daily in lost physical oil supply and a solid portion of the world’s natural gas supply, both are getting a lot more expensive than most consumers could stomach, and demand will start declining.

Bloomberg’s Javier Blas said in a recent column that the introduction of measures to destroy demand on purpose was the fourth step in the response to lost supply from industry and politicians after releasing fuel from stockpiles, rerouting whatever supply can be rerouted, and, as step three, more releases from stockpiles. The demand destruction step could take two forms: deliberate, guided by governments, or spontaneous, governed by market fundamentals. Blas argues that the latter form is the worse option because of its impact on the economy. Yet the first form is no more sparing for the economy: it is simply a matter of managed versus unmanaged disaster.

According to Blas, the world would need to reduce oil demand by a minimum of 8 million barrels daily. Measures suggested so far, by the International Energy Agency and the EU, include lower speed limits on highways, work from home, public transport instead of personal vehicle use, and car sharing plus boosts in fuel efficiency. These will not be enough even if implemented flawlessly, which is already doubtful. And this means that what we will probably see in terms of demand destruction would be a combination of deliberate and spontaneous shifts in demand, which will inevitably hurt the economy, wherever they take place.

At that stage, the question will become how long the damage will last, but we have not reached that stage yet. Per analysts, the return to normal would take between three and six months—once the war ends. The longer the bombing continues, the further away those three to six months move, and they also extend, because shut-in oil wells take longer to restart the longer you keep them shut-in. In short, the rest of this year is going to be no picnic.

By Irina Slav for Oilprice.com

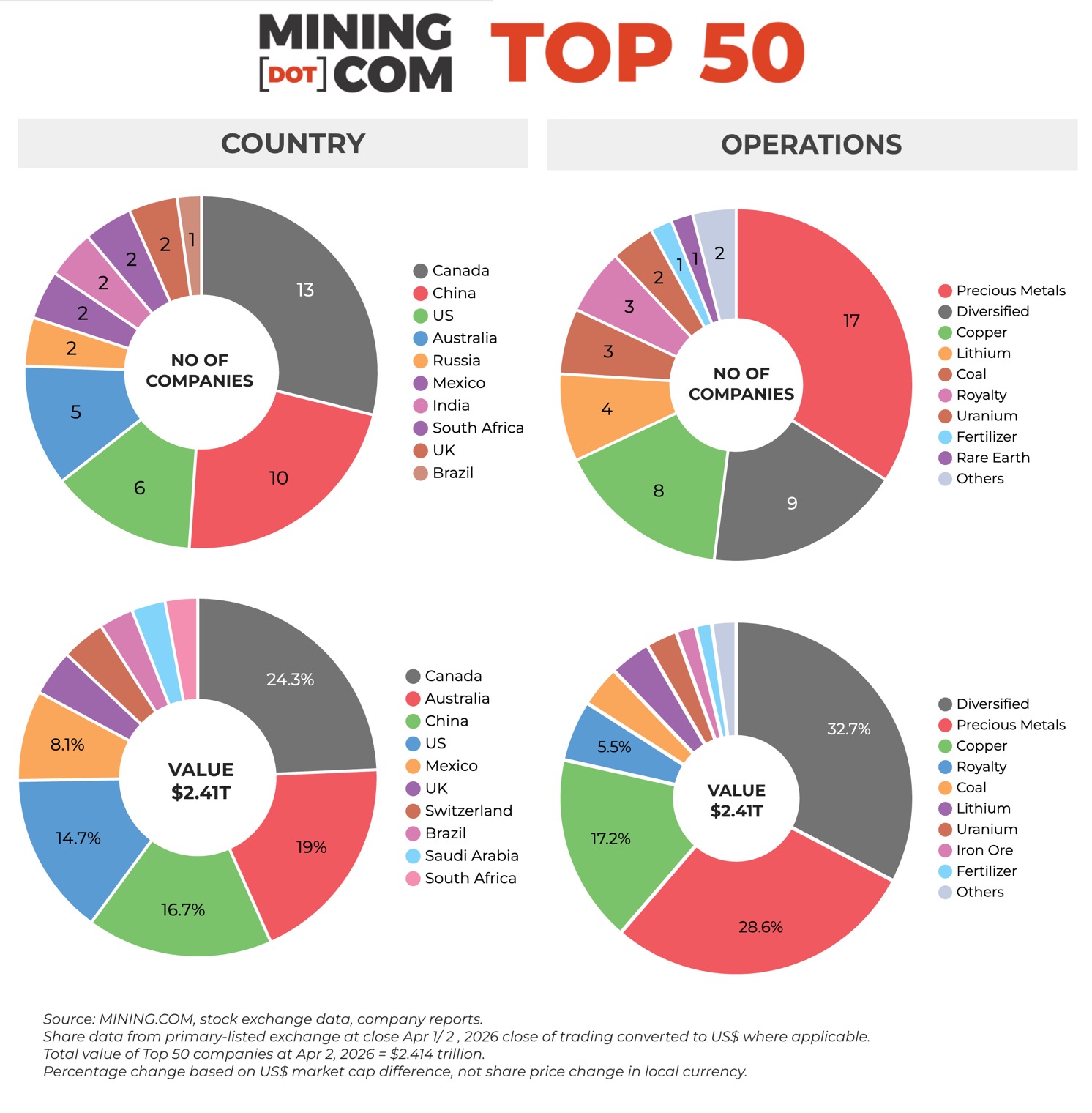

Top 50 mining companies power through Iran war – up $250 billion in 2026

At the end of the first quarter the MINING.COM TOP 50* ranking of the world’s most valuable miners had a combined market capitalization of $2.41 trillion, up $250 billion so far in 2025.

The market correction for the world’s major miners and the metals that power them, came a full month before the start of the US-Iran war when gold and silver prices cratered after hitting record highs at the end of January. Stocks of precious metals producers and streamers tanked after gold dropped by double digits and silver entered freefall.

Gold has traded sideways since then hovering above $4,700 an ounce and silver looks safe above $70 an ounce for now, although that’s still down 50% from its gravity defying spike. While gold did not receive the safe harbour investment a hot war in the Middle East would demand, the yellow metal is still showing a healthy 8% gain year to date. Silver is also trading in positive territory for 2026.

Copper is now down a modest 2% since end-2025 after hitting an all- time high of $6.50 per pound or more than $14,000 the day before the Friday massacre, but at least one commodities trading desk is saying the bellwether metal is “oversupplied and overpriced” even after a $2,000 a tonne climbdown.

Lithium’s resurgence saw Chile’s SQM (NYSE:SQM) and US producer Albemarle (NYSE:ALB) return to the Top 50 in Q4 2025, bringing the number of lithium stocks in the Top 50 back to three (from the peak of six in 2022). The two companies together with China’s Ganfeng Lithium (SZSE:002460) also join the best performers list this quarter.

Mining’s majors have not exactly shrugged off the war, but measured from the start of 2026 most stocks are trending well into positive territory with only a few exceptions.

Tide not lifting all boats

Among the upper echelons Barrick Mining (NYSE:B) stands out with a 5% retreat year to date (versus Newmont’s (NYSE:NEM) 11% gain and Agnico Eagle’s 22% rise) as the company tries to unlock value from its portfolio by separately listing its North American gold assets and pursue a growth path in copper (hence the swap of gold for mining in the company name).

All things being equal, it values its risky operations in countries like military coup prone Mali, its Zambian copper assets and its massive Pakistan copper-gold project at only $10 billion at its current market cap. Things aren’t going well at Riko Diq and just last week Barrick warned of “significant increases” to the project’s budget and an extended timeline.

Another regular underperformer, Amman Minerals (IDX:AMMAN), tops the quarter’s worst list for the second time in a row with a 27% fall as production problems and delays at smelter commissioning in Indonesia (the country bans concentrate exports) takes the counter down another notch or two.

Amman was the first Indonesian company to make it into the top 50 after its blockbuster 2023 debut. After a fierce rally the owner of the Batu Hijau copper and gold mine and developer of the adjacent Elang project, even managed to pierce the top 10 briefly 18 months later, but it’s been downhill since.

*Coeur Mining completed its $7B acquisition of New Gold in March.

Punter’s favourite Ivanhoe Mines (TSX:IVN) has lost almost a third of its value and after dropping to a market worth below $11 billion at the end of Q1, no longer makes the grade for the Top 50, where the cut-off has risen to an $18 billion market capitalization.

Ivanhoe put its Kamoa-Kakula mine in the DRC into production mid-2021, the largest (and highest grade) copper mine to come online in decades. In 2024, the chairman of Zijin Mining which owns 39.6% of the project and another 10 of Ivanhoe, said the company’s ambition is to make Kamoa-Kakula a 1 million tonne mine.

Just last week, Ivanhoe stunned investors eager for Ivanhoe to continue its DRC success story after slashing production guidance for 2026 to 290,000 to 330,000 tonnes, down from 380,000 to 420,000 tonnes. Next year will be even more disappointing: previously the company said it would produce as much as 540,000 tonnes, now the expectations are for 100,000 tonnes less than that.

The $100-billion club

Since inception, the MINING.COM TOP 50 was headed by two firms – BHP and Rio Tinto – the only miners with consistent market capitalizations above $100 billion (with a wobblehere and there). Before 2025 the only other company to have that distinction was Vale (BOVESPA:VALE3) which for fleeting few days was also trading above this level during Q1 2022, the market’s previous peak.

Now there are six firms with the distinction. Agnico Eagle, (TSX:AEM) in January year entered the ranks of the triple digit billion dollar miner.

The Toronto-based company joined Chinese champion Zijin Mining (SHA: 601899), Southern Copper (NYSE: SCCO), the mining arm of Grupo Mexico, and Denver’s Newmont Corporation (NYSE: NEM) which rode gold and copper prices all the way to the top towards the end of last year.

BHP (ASX:BHP) managed to top $200 billion at the beginning of March, a distinction no other mining company has ever achieved (and for the second time – the first time was April 2022 although that lasted for a day). The Melbourne-based company released bumper profits in its half-year report with copper, including byproducts such as gold, contributing $7.95 billion to BHP’s operating earnings, topping iron ore for the first time.

BHP and Rio Tinto (LSE:RIO) once again hold the two top spots. Rio Tinto was pushed out by Zijin and Southern Copper in January but the traditional order seems to have been restored, with some daylight between the Anglo-Australian giant and its competitors.

Rio Tinto stock received a lift after the company said on Monday it has gained control of acreage in Arizona needed to build the Resolution mine, a project slated to become one of the largest US sources of copper. Rio Tinto said it would now embark on a $500 million drilling campaign to delineate the deposit which is co-owned by BHP.

Glencore, Freeport rebound

After being a perennial underperformer Glencore (OTCPK:GLNCY) now has a better shot at joining the triple digit club. Glencore is now worth $87 billion and year to date the company is now the best performer among mining’s heavyweights with a 37% advance.

The Switzerland-headquartered company has escaped much of the fallout of US and Israeli operations in Iran in part to its extensive oil trading business which should do well as crude and gas prices jump, and a revival in coal.

The firm trades around 4 million barrels of oil equivalent per day. There was speculation last month from large investors in Glencore that a recent surge in coal prices will help bring Rio Tinto back to the table for a fresh attempt at creating the world’s biggest mining company after meeting with leaders of both companies in Australia.

Freeport McMoran (NYSE:FCX) came within $1 billion of $100 billion towards the end of February after the stock rebounded from its September 2025 drop following a devastating mud-rush at the block cave underground operation in Indonesia.

It was reported in March that the Phoenix-based company has begun the environmental permitting process for a $7.5 billion expansion of its majority owned El Abra copper mine in Chile.

NOTES:

Source: MINING.COM, stock exchange data, company reports. Share data from primary-listed exchange on December 30, 2025 close of trading converted to US$ where applicable. Percentage change based on US$ market cap difference, not share price change in local currency.

As with any ranking, criteria for inclusion are contentious. We decided to exclude unlisted and state-owned enterprises at the outset due to a lack of information. That, of course, excludes giants like Chile’s Codelco, Uzbekistan’s Navoi Mining (the gold and uranium giant may list later this year), Eurochem, a major potash firm, and a number of entities in China and developing countries around the world. Another central criterion was the depth of involvement in the industry, and how far upstream is the bulk of its revenue, before an enterprise can rightfully be called a mining company.

For instance, should smelter companies or commodity traders that own minority stakes in mining assets be included, especially if these investments have no operational component or even warrant a seat on the board? This is a common structure in Asia and excluding these types of companies removed well-known names like Japan’s Marubeni and Mitsui, Korea Zinc and Chile’s Copec.

Levels of operational or strategic involvement and size of shareholding were other central considerations. Do streaming and royalty companies that receive metals from mining operations without shareholding qualify or are they just specialized financing vehicles? We included Franco Nevada, Royal Gold and Wheaton Precious Metals on the basis of their deep involvement in the industry.

Vertically integrated concerns like Alcoa and energy companies such as Shenhua Energy or Bayan Resources where power, ports and railways make up a large portion of revenues pose a problem. The revenue mix also tends to change alongside volatile coal prices. Same goes for battery makers like China’s CATL which is increasingly moving upstream, but where mining will continue to represent a small portion of its valuation.

Another consideration is diversified companies such as Anglo American with separately listed majority-owned subsidiaries. We’ve included Angloplat (now Valterra) to track PGM representation in the ranking but excluded Kumba Iron Ore in which Anglo has a 70% stake to avoid double counting. Similarly, we excluded Hindustan Zinc which is listed separately but majority owned by Vedanta.

With other groups like Mexico’s Penoles where refining and chemicals make up a substantial part of the business where possible the Top 50 would include separately listed operating subsidiaries that are dedicated to mining. This is also why Southern Copper represents Grupo Mexico in the ranking. Many steelmakers own and often operate iron ore and other metal mines, but in the interest of balance and diversity we excluded the steel industry, and with that many companies that have substantial mining assets including giants like ArcelorMittal, Magnitogorsk, Ternium, Baosteel and many others.

Head office refers to operational headquarters wherever applicable, for example BHP and Rio Tinto are shown as Melbourne, Australia, but Antofagasta is the exception that proves the rule. We consider the company’s HQ to be in London, where it has been listed since the late 1800s.

Please let us know of any errors, omissions, deletions or additions to the ranking or suggest a different methodology: email Frik Els at fels@mining.com with Top 50 in the subject line.