It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

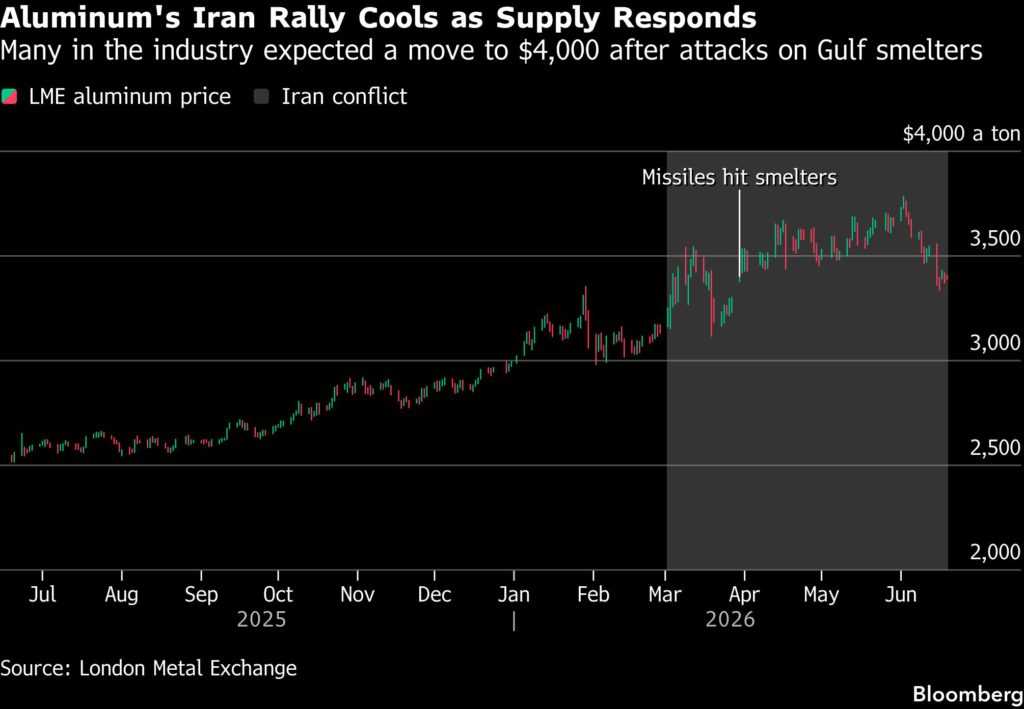

The Iran war caused one of the biggest supply shocks to ever hit the aluminum market, but the runaway price surge that many were bracing for has been blunted by the ingenuity of producers from the Middle East to China.

When the conflict began, market watchers warned that unless the Strait of Hormuz reopened quickly, smelters were likely to run out of raw materials within weeks, potentially forcing widespread shutdowns that would plunge the global market into crisis and send prices to record highs above $4,000 a ton.

Those fears escalated dramatically when Iran targeted smelters in the region in missile strikes, and there was broad agreement that aluminum looked set to be one of the worst-hit commodity markets outside of oil and gas.

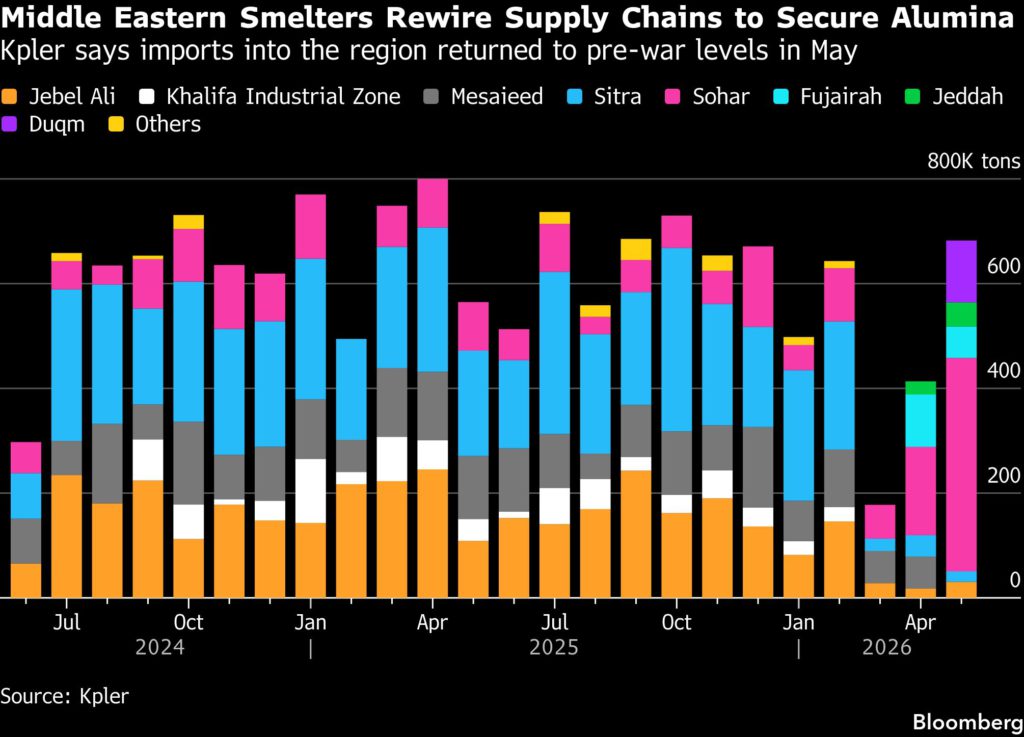

However, in recent weeks Middle Eastern smelters have carried out a series of complex logistical operations — including daring voyages through the strait — to replenish reserves of alumina and other raw materials, helping to avert widespread closures in a region that accounts for nearly 10% of global supply. And outside the Gulf, smelters in China and Indonesia have been instrumental in keeping the global market in check as buyers wait for exports to rebound.

Now, with analysts, traders and investors staking their bets on where prices are heading next, stark disagreements are emerging on how quickly the market will recover from the squeeze.

“A full-blown physical supply freeze has been averted thanks to a combination of rerouted Middle Eastern alumina imports, rising Chinese exports, and ramping Indonesian production,” said Amelia Xiao Fu, head of commodities strategy at Bank of China International. “While the market managed to survive the last few months by drawing down inventories, these operational buffers have now been decreased.”

Middle Eastern smelters have been forced to make heavy cuts to output, but the clandestine nature of their efforts to shore up their supply chains means the precise scale of the losses is tough to quantify. Meanwhile, a regulatory cap on production in China and power constraints in Indonesia are only adding to the challenge of assessing how quickly supply and demand will rebalance.

Some of the market’s biggest bulls have trimmed their price forecasts in recent days, with JPMorgan Chase & Co. saying that a move to $4,000 a ton is taking longer than expected due to a strong supply response in Asia and an aggressive drawdown in the industry’s hidden inventories.

At the other end of the scale, Goldman Sachs Group Inc. sees prices moving towards $3,000 a ton over the coming year, even after raising forecasts it made at the start of the conflict to reflect a slower rebound in Middle Eastern supplies than anticipated. Futures in London are currently trading around $3,400.

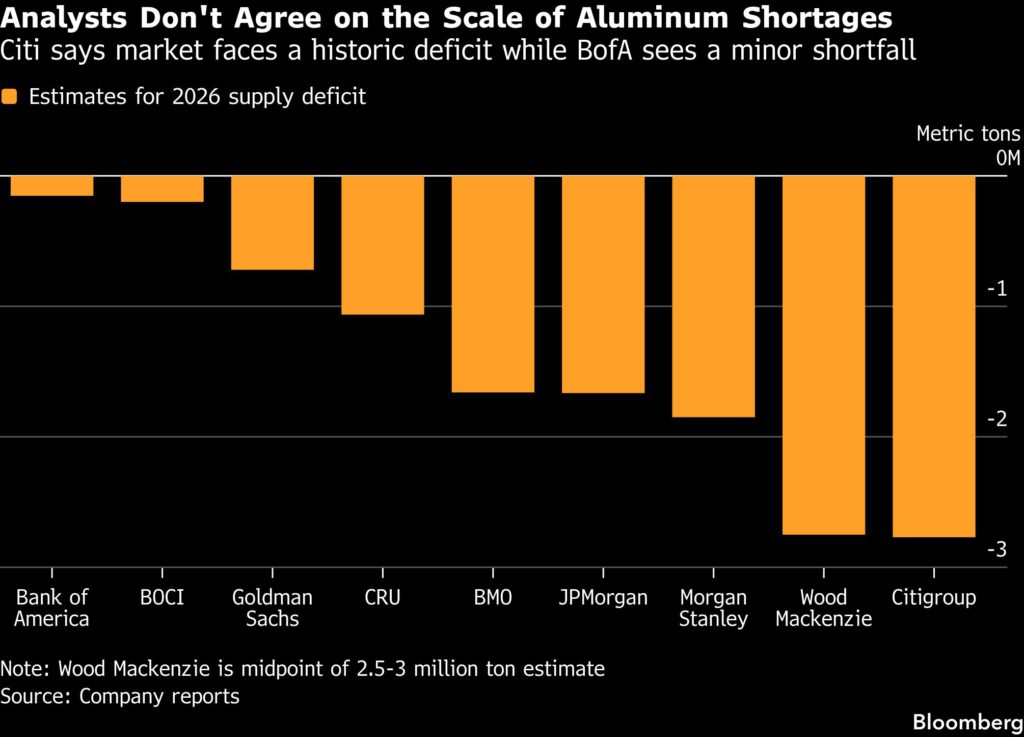

Differences in estimates for aluminum’s underlying supply balance are even starker, with Citigroup Inc. expecting the biggest supply shock in more than 50 years, while Bank of America Corp. expects supply and demand in the 76-million-ton market to be more or less balanced.

Alumina flows

Part of the discrepancy stems from expectations that raw-material shortages have inflicted deeper supply losses on Persian Gulf smelters than they’ve publicly disclosed. But for Ben Ayre, an analyst at ship-tracking firm Kpler, a growing stream of alumina flows into the region signals that, even with Hormuz closed, smelters have made strides in replenishing their reserves.

In recent weeks, a handful of vessels have shown an appetite to move in alumina directly through the strait, switching off their tracking systems to undertake the kind of dark transits that have kept a trickle of oil flowing to global markets through the crisis, according to Kpler’s analysis.

Even greater volumes of alumina have been unloaded in ports in Oman and dispatched to smelters via trucks, in a major test of the region’s logistical capabilities. Thanks to those efforts, imports of the raw material into the Persian Gulf returned to pre-war levels in May, data from the firm show.

“It has resulted in some really novel solutions, and we’ve had to work quite hard to keep up,” Ayre said in an interview. “It’s not unique, but it is somewhat exceptional in terms of its reflection of the value of keeping these operations running.”

Shadow stocks

The challenge in assessing the scale of the supply squeeze doesn’t end in the Gulf, and JPMorgan says the market impact of global shortages has also been blunted by an aggressive drawdown in privately held inventories that are notoriously hard to monitor.

“When we speak with clients there’s a clear sense that it is tight out there, but the first port of call is those invisible stocks,” said Greg Shearer, the bank’s head of base and precious metals research. Still, he believes that it’s only a matter of time before those reserves are depleted and exchange stocks will start being drawn too, driving prices higher. “It’s taking longer than expected, but there are significant deficits that need to be covered.”

China shock

The behavior of Chinese smelters has added another analytical headache. Before the conflict, a bullish mood had swept through the aluminum industry, as smelters in China started to bump up against a regulatory cap on production that looks set to bring a long era of oversupply to an end.

Since the war started, however, official statistics have suggested that Chinese smelters are producing comfortably above that 45-million-ton cap, with April figures pointing to an annualized run-rate of 47 million tons. With exports surging, some analysts are betting that Chinese smelters could solve the global shortage single-handedly if they keep their plants running in overdrive.

In assessing whether they will, analysts need to take a view on how strictly China will enforce the cap, and how far engineers can go in feeding plants with more power than they’re designed to handle. That’s a process that one industry veteran likens to trying to balance an elephant on a finger.

Indonesia wildcard

A final wildcard is a prospective wave of new supply in Indonesia. A surge in Indonesian aluminum exports has sharpened the industry’s focus on its emerging role as a major global supplier, and there’s a growing expectation that producers there will divert scarce power to aluminum plants at the expense of less-profitable nickel operations.

“We always knew there would be capacity additions, but the view up to now was that production would lag because power wasn’t available,” said Amy Gower, head of metals and mining strategy at Morgan Stanley. “We haven’t changed our models yet, but the risk now, with power being reallocated from nickel, is that new supply could come even quicker.”

Taken together, the combination of rebounding Middle Eastern supply, elevated Chinese production and skyrocketing Indonesian output is creating a consensus in the industry that prices will head lower in the long term. But as the US and Iran negotiate a deal to end the war permanently, a debate is still raging about whether the market will face a final squeeze as inventories run dry before the new supply arrives.

“I think if it was going to happen, it would have happened by now,” said Helen Amos, head of commodities research at BMO Capital Markets. “It’s likely that aluminum is past the peak point of the deficit.”

(By Mark Burton and Julian Luk)

Column: Guinea bets bauxite dominance can reshape aluminum supply

Large piles of bauxite ore sit at a treatment area storage in Guinea. (Stock image by Igor Groshev.)

The West African country of Guinea has grown to be the world’s largest supplier of bauxite, the raw material ultimately transformed into aluminum.

It’s now looking to use this newfound dominance to exert greater control over both price and industry structure, just as Indonesia has done in nickel and the Democratic Republic of Congo is attempting to do in cobalt.

All three resource giants are struggling to rein in mining sectors that have grown too big too fast, swamping global markets and crashing prices.

Indonesia is using mining quotas, the Congo export quotas, and Guinea looks minded to implement a mix of both as a way of stopping operators exporting more than their mining quotas allow them to produce.

For Conakry, it’s also a chance to emulate Indonesia by capturing more of its resource value by moving from bauxite mining to alumina refining.

Bauxite is the third most abundant element in the Earth’s crust but is mostly too dispersed or too low quality to allow for conversion into alumina.

Guinea not only boasts the world’s largest reserves of metallurgical bauxite but also produces a high-purity product prized for its natural low silica content.

Thanks to heavy Chinese investment, the country overtook Australia as the world’s largest bauxite producer in 2023 and now accounts for around 40% of global output and 70% of the seaborne export market.

Guinea’s exports jumped by 25% year on year to 183 million metric tons in 2025, which unsurprisingly caused prices to slump by almost half over the course of last year and the first part of 2026.

That is why the government is searching for the most effective way of hitting the brakes without generating the sort of market disruption caused by Congo’s cobalt export quota system.

China has grown increasingly dependent on Guinea’s bauxite.

Chinese dependency

China has become increasingly reliant on Guinea for bauxite to feed its huge aluminum production sector.

Imports of Guinean material mushroomed from just 334,000 tons in 2015 to 149 million tons in 2025, by which point they accounted for 74% of all bauxite imports.

China has its own bauxite reserves but they’ve been depleted by decades of mining and are lower quality than those in Guinea.

Moreover, the country has massively expanded its aluminum smelting capacity this century, requiring a similar build-out in alumina refining, far beyond its domestic bauxite mining capacity.

Guinea’s planned crackdown on its runaway bauxite sector has been well flagged, and Chinese buyers have had plenty of time to build precautionary stocks. March imports from Guinea hit a monthly record of 18 million tons.

But there’s little prospect of breaking the dependency, given the scale of the material flow. What will change, however, is the nature of that dependency.

It’s the first major overseas investment in alumina by China’s state giant. It’s also the third Chinese-backed alumina refinery project to be announced in recent months.

Guinea’s only existing refinery is the Friguia plant, built in the 1960s and owned first by France’s Pechiney, then by US producer Reynolds and since 2008 by Russia’s Rusal. It was out of action between 2012 and 2018 but is operating again, albeit below its 650,000-ton-per-year capacity.

The Conakry government is aiming for five or six more processing plants with a combined capacity of 7 million tons of alumina by 2030.

The seizure of mining assets from Emirates Global Aluminium last year for its failure to follow through on a commitment to refining has served as a stark warning for other operators.

New industry hub

Guinea is following closely in the footsteps of Indonesia, which banned bauxite exports in 2023 as a way of forcing miners to build out processing capacity.

While Indonesia has plenty of coal-fired power to both refine alumina and smelt the intermediate product into aluminum, Guinea doesn’t currently have sufficient energy resources to go beyond the alumina stage.

But if Guinea can successfully implement its strategy, it will turbo-charge the creation of a West African alumina hub.

Not least because other African bauxite producers are travelling the same value-added pathway to keeping more of their mineral revenues.

Nigeria has signed a $1.3 billion investment deal with Africa Finance Corporation (AFC) to build an alumina refinery, while Ghana is looking to do the same under the auspices of the Ghana Integrated Aluminium Development Corporation.

The African shift from mining to first-stage processing could have transformative effects on the aluminum supply chain.

The seaborne bauxite market will shrink. The global alumina export market will expand and China’s domestic alumina refineries will find themselves in competition with their largest raw material supplier.

(The opinions expressed here are those of Andy Home, a columnist for Reuters.)

From microbial dark matter to living library: New biobank decodes survival secrets of extreme acid mine drainage microbes

How culturomics unlocks acid mine drainage's hidden microbial universe. This graphical summary illustrates the study's workflow and key findings. Researchers collected acid mine drainage (AMD) samples (pH ~2.5) from diverse habitats including mine tailings and weathered minerals. Using 12 culture conditions (Fe²⁺, S⁰, organic media at 30 °C and 45 °C), they built the Microbial Biobank of AMD (mbAMD), which comprises 42 species (21 novel) across 22 genera and 13 families, covering 86.7 % of core AMD bacterial taxa identified from 226 metagenomic datasets. Functional assays confirmed 36 taxa with active iron or sulfur metabolism. Comparative genomics revealed that horizontal gene transfer (HGT) drives extremophile adaptation, with adaptive genes for acid tolerance, metal resistance and energy pathways preferentially acquired from phylogenetically close relatives.

Acid mine drainage (AMD) – one of Earth's most hostile habitats – forms when sulfide minerals are exposed to air, water and microbes, generating pH levels below 3 and high concentrations of heavy metals. Despite this harshness, AMD hosts diverse and specialized microbial communities that drive iron and sulfur geocycling, accelerating mineral weathering and acid generation. These microorganisms have stringent physiological needs – including specific electron donors, pH homeostasis and sometimes symbiotic dependencies – make them notoriously difficult to isolate. So far, over 97 percent of microorganisms in AMD have never been cultured, leaving their metabolism and adaptation strategies locked as "microbial dark matter." Now, a new culturomics‑driven resource called the Microbial Biobank of AMD (mbAMD) changes that. The collection contains 652 isolates spanning 42 species, including 21 novel taxa, and covers 86.7 percent of the global AMD core microbiome. Functional tests confirmed that 36 of these species actively metabolize iron or sulfur. Among them are the first pure cultures of acid‑tolerant sulfate reducers, organisms long sought for their potential to remediate AMD pollution.

A team led by scientists at the Institute of Microbiology, Chinese Academy of Sciences, publishing (DOI: 10.1016/j.ese.2026.100722) in Environmental Science and Ecotechnology on June 11, 2026, constructed the mbAMD – a culturomics-derived biobank from AMD samples collected at three mining sites in China. Using 12 tailored culture conditions, high-throughput plating and microfluidic technology, they recovered 652 phylogenetically distinct strains, including 11 formally described novel species, four new genera and one previously undescribed family.

The mbAMD's power lies in its functional validation. Through culture-based assays and comparative genomics, the team showed that 36 taxa actively oxidize or reduce iron or sulfur. Among the most striking finds: three novel acid-tolerant sulfate reducers – Alicyclobacillus curvatus ALEF1T, Alicyclobacillus mengziensis S30H14T and Acidiferrimicrobium ferridurans MYW30-Hm14 – are the first pure cultures of their kind, holding promise for bioremediation of acidic, metal-laden waters. Genomic analysis also uncovered surprises: several validated iron oxidizers lack all known iron-oxidation systems, hinting at entirely unknown electron transport pathways. Meanwhile, horizontal gene transfer (HGT) emerged as a dominant evolutionary driver, contributing 3.5–39.6 percent of genome content across AMD taxa. Transferred genes are functionally enriched in acid tolerance (e.g., clcA, kdpC), metal resistance (e.g., merA, mntH, znuB) and energy metabolism. The network analysis revealed that extremophiles preferentially acquire adaptive genes from phylogenetically close relatives rather than distant donors – a modular acquisition pattern that may accelerate niche specialization.

"For years, AMD's microbial dark matter remained out of reach – we knew it was there, but we couldn't identify their functions, let alone exploit them." the authors said. "With mbAMD, we've turned sequence predictions into living resources. Seeing that 70 percent of our isolates actively metabolize iron or sulfur, and discovering the first pure acid-tolerant sulfate reducers, was incredibly rewarding. Even more striking was the HGT pattern: these extremophiles don't borrow genes randomly. They consistently trade stress-survival tools with their close relatives. That's a very different picture of adaptation than what we see in many other environments."

The mbAMD provides a functional foundation for biohydrometallurgy and environmental remediation. The newly isolated sulfate reducers could be developed into bioremediation agents that precipitate metals under low-pH conditions – a long-standing challenge for treating AMD. Similarly, the collection’s iron- and sulfur-oxidizing strains may help optimize bioleaching processes for metal recovery from low-grade ores. Beyond applications, the resource enables a shift from metagenomic prediction to empirical testing, allowing researchers to validate metabolic pathways, dissect stress responses and explore evolutionary trade-offs in extreme environments. The study also offers a replicable culturomics framework that can be applied to other underexplored ecosystems – from deep-sea vents to alkaline soda lakes – to unlock their own microbial dark matter.

This work was funded by the Strategic Priority Research Program of the Chinese Academy of Sciences (XDB0810000), the Major Research Plan of National Nature Science Foundation of China (grant 92251307, 91851206), the National Natural Science Foundation of China (32570129), the National Key R&D Program of China (2022YFC2105300).

Environmental Science and Ecotechnology (ISSN 2666-4984) is an international, peer-reviewed, and open-access journal published by Elsevier. The journal publishes significant views and research across the full spectrum of ecology and environmental sciences, such as climate change, sustainability, biodiversity conservation, environment & health, green catalysis/processing for pollution control, and AI-driven environmental engineering. The latest impact factor of ESE is 14.3, according to the Journal Citation ReportsTM 2024.

An international research collaboration between the University of Vienna and Lawrence Berkeley National Laboratory in the United States has used machine learning to re-examine one of the most hotly debated signals in astrophysics. The so-called Galactic Center Excess (GCE), a faint, roughly spherical glow of gamma rays at the center of the Milky Way, has fascinated physicists for more than a decade. The new results suggest that an explanation in terms of dark matter cannot currently be ruled out. The results have now been published in the journal Physical Review Letters.

The Galactic Center Excess (GCE) is a roughly spherical glow of gamma rays extending over thousands of light years around the center of the Milky Way. Several explanations have been proposed for this unusual signal: theoretical predictions are consistent with self-annihilating dark matter. Another possibility is a large population of rapidly rotating neutron stars known as millisecond pulsars. The origin of the signal at the center of our galaxy therefore remains unresolved.

“Interpreting the signal is particularly difficult because the Galactic Center is an exceptionally bright and crowded region of the gamma-ray sky,” explains Florian List, study author and researcher at the University of Vienna.

Including Photon Energies for the First Time Brings a Decisive Change

The pulsar hypothesis has been supported by previous statistical studies. However, earlier analyses did not include a crucial piece of information: the energy of each individual detected photon. In the new study, the research group developed a machine-learning method trained on more than a million simulated gamma-ray observations. The aim was to evaluate spatial and spectral information simultaneously for the first time.

Including this energy information changes the picture substantially. Whereas earlier analyses pointed to comparatively bright, unresolved light sources (point sources), the new results show that these point sources would have to be extremely faint. “Our new analysis shows that the sources would have to be so faint that they would be almost indistinguishable from the emission expected from annihilating dark matter”, says Nick Rodd, study author and scientist at the Lawrence Berkeley National Laboratory.

For the pulsar hypothesis, this would imply that there must be at least 35,000 such sources in the center of the Milky Way — significantly more than the few hundred to few thousand sources assumed in some previous studies.

Dark matter remains plausible in the debate about the center of the Milky Way

“The origin of the Galactic Center Excess is one of the longest-running debates in astrophysics,” says Florian List. “Our work does not show that dark matter is responsible for the signal. However, it suggests that it is still too early to rule out this possibility.”

The new results weaken one of the strongest arguments so far against the dark-matter hypothesis. Although the study does not provide direct evidence for dark matter, the hypothesis that the Galactic Center Excess is due to dark matter remains a plausible explanation in the debate.

Summary:

The Galactic Center Excess (GCE) is a roughly spherical glow of gamma rays at the center of the Milky Way.

One possible origin of this glow is a population of rapidly rotating neutron stars, known as millisecond pulsars. The new results show that dark matter also remains a plausible explanation.

In the new study, the research group developed a machine-learning method that incorporated photon energies for the first time.

The study does not show that dark matter is responsible for the signal. However, it suggests that it is still too early to rule out this possibility.

About the University of Vienna:

At the University of Vienna, curiosity has been the core principle of academic life for more than 650 years. For over 650 years the University of Vienna has stood for education, research and innovation. Today, it is ranked among the top 100 and thus the top four per cent of all universities worldwide and is globally connected. With degree programmes covering over 180 disciplines, and more than 10,000 employees we are one of the largest academic institutions in Europe. Here, people from a broad spectrum of disciplines come together to carry out research at the highest level and develop solutions for current and future challenges. Its students and graduates develop reflected and sustainable solutions to complex challenges using innovative spirit and curiosity.

Astronomers have followed a faint, cosmic trail of gas to a third galaxy that has no dark matter.

In a new study in The Astrophysical Journal, a team of Yale astronomers reports on a dwarf galaxy located45 million light-years from Earth — called NGC 1052-DF9 — that appears to have formed in a straight line with nine other galaxies.

Two of those other galaxies, DF2 and DF4, were previously shown to lack dark matter — an invisible, theorized material that gives shape to the universe and is thought by most astronomers to be essential to galaxy formation.

Now, DF9 has joined the no-dark-matter club.

“A line of galaxies lacking dark matter has never been seen before,” said Michael Keim, a Ph.D. student in astrophysics in Yale’s Graduate School of Arts and Sciences and first author of the new study. “The discoveryprovides some of the strongest evidence yet that these galaxies formed through an extreme and previously unseen process and offers a rare new window into the nature of dark matter itself.”

Keim’s advisor, Yale astronomer Pieter van Dokkum, led the original studies that analyzed DF2 and DF4, using data from the Hubble Space Telescope. Van Dokkum, the Sol Goldman Family Professor of Astronomy and professor of physics in Yale’s Faculty of Arts and Sciences, is co-author of the new study.

During his doctoral work with van Dokkum, Keim found DF9 — which had been misidentified as a supermassive black hole — and proposed a thorough analysis with W.M. Keck Observatory’s Cosmic Web Imager, in Hawaii, which is designed specifically to study faint starlight such as the light emitted by DF9.

The researchers measured the motions of stars within DF9 to determine its mass. They found that DF9 has the mass of 100 million suns — which is consistent with the expected amount of visible matter in a galaxy of its size — and nothing else. If DF9 also had the expected amount of dark matter, its mass would be equal tomore than 10 billion suns.

DF9’s lack of dark matter strongly suggests that DF2, DF4, and DF9 formed together in the same violent event, such as a high-speed collision between galaxies, Keim said. In this scenario, the collision would have separated out gas from the galaxies’ dark matter — and that gas went on to form new galaxies in a linear trail.

“Up until now it was assumed galaxies formed within pools of dark matter called ‘halos,’” Keim said. “This system shows that stars and galaxies can form outside of dark matter ‘halos’ in extreme events and indicates that dark matter is a physical substance that can act independently of normal matter or gas, challenging alternative theories that dark matter is gravity.”

In this regard, the new study reaffirms van Dokkum’s original work on DF2 and DF4, which also suggested that dark matter is a separate material.

The researchers are now conducting follow-up observations with other telescopes — including the new Mothra telescope co-founded by van Dokkum and University of Toronto astronomer Roberto Abraham — to search for any gas that was left behind after the initial galaxy collision.

Co-authors of the study are former Yale Ph.D. student Zili Shen, Yale postdoctoral researcher Imad Pasha, and Princeton astronomer Shany Danieli.

Research led by the Tata Institute of Fundamental Research, Mumbai along with Professor Subir Sarkar from the University of Oxford questions the widely accepted argument that the expansion rate of the universe is accelerating and that this is driven by ‘dark energy’ arising from the quantum vacuum. Their letter has been published in Monthly Notices of the Royal Astronomical Society. The findings divide opinion; in the same journal issue, a paper co-authored by Professor Maria Vincenzi also from the University of Oxford maintains that evidence does indeed point to the universe still accelerating.

In his work, Professor Subir Sarkar of Oxford's Rudolf Peierls Centre for Theoretical Physics, together with Animesh Sah and Mohamed Rameez of the Tata Institute of Fundamental Research in India, revisited one of cosmology's most important observational datasets: the Pantheon+ compilation of more than 1,700 Type Ia supernovae. For more than 25 years, astronomers have used observations of these supernovae – exploding stars – to measure the expansion of the universe. Analysis of such observations led to the groundbreaking discovery that cosmic expansion appears to be accelerating – a finding that won the 2011 Nobel Prize in Physics.

The team analysed the supernovae from the Pantheon+ dataset, one of the most comprehensive catalogues of its kind, and incorporated a recently proposed correction that takes into account the age of the stars that eventually produce these supernova explosions. They also checked whether the inferred acceleration of the expansion rate is indeed the same in every direction, as is assumed in the standard cosmological model.

‘There is increasing evidence that the brightness of Type Ia supernovae depends on the age of the stars they come from,’ said Professor Subir Sarkar of Oxford's Rudolf Peierls Centre for Theoretical Physics, a co-author of the study. ‘If this effect is not accounted for, it can lead to the erroneous conclusion that the expansion rate is accelerating.’

After applying the correction, the researchers found that the data no longer support a picture of a uniformly accelerating Universe. Instead, their analysis suggests that cosmic expansion is overall slowing down rather than speeding up.

Professor Sarkar and his colleagues came to their conclusion by considering whether the inferred acceleration may in fact be anisotropic, meaning it exhibits different properties when measured in different directions and therefore deviates from the standard cosmological model. If that were true, they argue that dark energy couldn’t be responsible for driving the acceleration because an effect of the quantum vacuum cannot be anisotropic.

‘We found that the inferred acceleration is directed mainly along the direction that we are moving locally, as indicated by the hotspot in the cosmic microwave background, and dies away with distance,’ explains Professor Sarkar. ‘This is unaffected by the correction to the supernova brightness – so rejects dark energy independently of whether the correction is applied or not. The correction turns the isotropic component into a deceleration – which again rules out dark energy.’

This paper’s findings go against the widely accepted viewpoint that the universe is still accelerating – a discovery that was awarded the Nobel Prize in 2011. In the same journal issue, a paper co-authored by Professor Maria Vincenzi also from the University of Oxford maintains that evidence does indeed point to the universe still accelerating and she comments: ‘The lead authors of our study are world experts in understanding how the environments of Type Ia supernovae affect cosmological measurements with more than a decade of experience in both supernova astrophysics and galaxy evolution. Our recent findings provide further confidence in the cosmological framework that has emerged over the past three decades and allow the research community to focus on one of the biggest unanswered questions in physics: the nature of dark energy itself.’

Looking ahead, both schools of thought will be able to test their findings and explore further using data from the Rubin Observatory’s Legacy Survey of Space and Time (LSST), which will soon measure hundreds of thousands of supernovae.

Oxford University has been placed number 1 in the Times Higher Education World University Rankings for the tenth year running, and number 3 in the QS World Rankings 2024. At the heart of this success are the twin-pillars of our ground-breaking research and innovation and our distinctive educational offer.

Oxford is world-famous for research and teaching excellence and home to some of the most talented people from across the globe. Our work helps the lives of millions, solving real-world problems through a huge network of partnerships and collaborations. The breadth and interdisciplinary nature of our research alongside our personalised approach to teaching sparks imaginative and inventive insights and solutions.

Through its research commercialisation arm, Oxford University Innovation, Oxford is the highest university patent filer in the UK and is ranked first in the UK for university spinouts, having created more than 300 new companies since 1988. Over a third of these companies have been created in the past five years. The university is a catalyst for prosperity in Oxfordshire and the United Kingdom, contributing around £16.9 billion to the UK economy in 2021/22, and supports more than 90,400 full time jobs.

To understand and define the boundaries of our heliosphere, SwRI researchers collaborated with other scientists to use existing numerical simulations to reveal the structure of the heliosphere and its interaction with the interstellar medium. Solar wind data and solar wind pressure forecasts provide important information for heliospheric models to help predict when the New Horizons spacecraft will encounter the heliospheric termination shock, on its way to joining the Voyager 1 and 2 spacecraft in interstellar space.

SAN ANTONIO — June 22, 2026 —Southwest Research Institute (SwRI) scientists are using a solar wind forecasting method combined with analytic and numerical heliosphere models to find out where the first plasma boundary of the outer heliosphere lies as NASA’s New Horizons spacecraft hurtles toward this mysterious region of space.

The heliosphere, a vast bubble of plasma created by the solar wind flowing outward from the Sun, surrounds the entire solar system and shields it from much of the high-energy galactic radiation found in interstellar space. Scientists believe the heliosphere resembles a comet because the Sun moves through the interstellar medium, creating a rounded “nose” region and a trailing “tail.” Other models predict a croissant-shaped heliosphere.

SwRI researchers are studying the heliosphere’s dynamic outer boundaries, including the termination shock and the heliopause, where the solar wind slows and then abruptly stops when interacting with interstellar material. These boundaries constantly expand and contract in response to changing solar conditions. During solar maximum, the “turbocharged” solar wind expands the heliosphere. During solar minimum, the ebbing solar wind allows the heliosphere to contract.

Two recent scientific papers are exploring how to accurately predict the location of the termination shock, particularly in the direction New Horizons is traveling.

After completing historic flybys of Pluto and Kuiper Belt object Arrokoth, New Horizons continues deeper into the outer solar system on a trajectory toward the heliosphere’s forward region. It will reach the termination shock and later leave the solar system, only the third spacecraft to do so after Voyager 1 and 2. Scientists hope to determine when the spacecraft will encounter this plasma boundary surrounding the solar system.

“We want to understand when the spacecraft will reach the termination shock to prepare to take measurements and download data about this region,” said Dr. Jonathan Gasser, lead author of the two papers. “Based on our research, we predict that New Horizons will encounter the termination shock as early as 2029 or as late as 2040. And it is possible that it could cross the boundary more than once as the heliosphere continues to expand and contract.”

The research could improve our understanding of how the heliosphere interacts with interstellar space and help future missions explore the boundaries between the solar system and the interstellar space beyond.

To read the Astrophysical Journal paper titled “Solar Wind Forecasting for Long-term Variations of the Global Heliosphere,” go to https://doi.org/10.3847/1538-4357/ae3152.

Schematic of the A-GBPS-augmented GNSS positioning system: GNSS satellites (black) and A-GBPS base stations (gold) broadcast positioning signals; the CBM station (gray) receives these signals and forwards carrier-phase observations to the user (blue). The base stations operate without time synchronization.

As demand grows for high-precision navigation in autonomous vehicles, mobile mapping, robotics, and other real-time applications, one challenge continues to limit performance: the long time required for satellite positioning systems to reach full accuracy. A new study proposes a solution by combining satellite navigation with signals from asynchronous ground-based transmitters that do not require costly time synchronization. The researchers developed a tightly coupled positioning framework that fuses information from both sources, enabling faster convergence and improved positioning accuracy. The findings suggest that existing terrestrial communication infrastructure could be repurposed to enhance next-generation navigation services with low deployment complexity and cost.

Precise Point Positioning (PPP), a high-accuracy Global Navigation Satellite System (GNSS) technique, offers the advantage of centimeter-level positioning without relying on local reference stations. However, PPP often requires many minutes—and sometimes longer—to achieve full precision, making it less suitable for dynamic environments. Previous efforts have shown that Ground-Based Positioning Systems (GBPS) can accelerate convergence by providing additional geometric constraints. Yet most GBPS solutions depend on highly accurate time synchronization among base stations, which increases infrastructure costs and limits deployment flexibility. Asynchronous Ground-Based Positioning Systems (A-GBPS) remove this synchronization burden, but their potential for augmenting PPP has remained largely unexplored. Deeper investigation into practical PPP augmentation with A-GBPS is needed.

Researchers from the Department of Electronic Engineering at Tsinghua University report a new GNSS augmentation framework in a study published (DOI: 10.1186/s43020-026-00200-4) in 2026 in the journal Satellite Navigation. The researchers developed a tightly coupled positioning architecture that integrates GNSS with A-GBPS. By combining satellite and A-GBPS observations, the framework significantly accelerates positioning convergence and improves solution stability, offering a practical pathway toward more efficient high-precision navigation services.

Rather than requiring all base stations to share the same clock, the new framework embraces their asynchronous nature. The researchers developed a method that uses a dedicated monitoring station to correct transmitter clock biases before integrating the measurements with GNSS observations. This allows the system to exploit the strong signal power and favorable geometry of ground-based transmitters without the operational burden of network-wide synchronization.

The team first established a theoretical model showing that adding A-GBPS observations should reduce positioning uncertainty. Numerical simulations then demonstrated that adding A-GBPS can significantly strengthen geometric constraints, particularly in the directions where satellite-only positioning is weak. The benefits became even more pronounced after the positioning solution stabilized, suggesting that A-GBPS can complement GNSS throughout the positioning process.

To test the approach under real-world conditions, the researchers deployed six A-GBPS base stations and conducted field experiments using a mobile receiver platform. Compared with GNSS-only positioning, the augmented system reached higheraccuracy with faster convergence and delivered more stable positioning performance. The experiments also revealed an important engineering insight: adding more base stations generally improved performance, but the gains began to level off beyond about five or six stations. This finding may help future network designers balance positioning performance against deployment costs.

The authors said the work demonstrates that high-precision PPP augmentation does not necessarily require tightly synchronized GBPS. Instead, asynchronous GBPS can provide valuable geometric information that improves both convergence speed and positioning reliability. They said the results indicate that existing terrestrial communication facilities, like 5G, could potentially support future positioning services. Such an approach may offer a practical pathway toward more accessible high-precision navigation without high deployment expense and complexity, which usually associated with synchronized GBPS.

The implications extend beyond navigation research. Faster and more reliable positioning could benefit autonomous driving systems, unmanned aerial vehicles, intelligent transportation networks, surveying operations, and mobile mapping platforms that depend on rapid access to precise location information. Because the framework is compatible with existing radio infrastructure, it may lower barriers to deployment and expand positioning coverage in challenging environments. The researchers note that future work will focus on eliminating the need for a dedicated monitoring station and evaluating performance under more complex urban conditions, where signal blockage and multipath interference are more prominent.

Satellite Navigation(ISSN: 2662-1363; ISSN: 2662-9291) Satellite Navigation is the official journal of the Aerospace Information Research Institute. The aims to report innovative ideas, new results or progress on the theoretical techniques and applications of satellite navigation. The journal welcomes original articles, reviews and commentaries.

A GNSS PPP framework augmented using asynchronous ground-based positioning systems

Article Publication Date

12-Jun-2026

Tracing a neutrino ghost to distant “shadow blaster” galaxy

Gemini North telescope on Maunakea helps uncover strongest evidence yet that distant star-forming galaxies contribute to the production of one of the Universe’s most mysterious ghost particles

Association of Universities for Research in Astronomy (AURA)

Left: the field around the gravitationally lensed galaxy nicknamed “Shadow Blaster.” This galaxy lies 11 billion light-years away and sits just behind the bright red galaxy at the center of this image.

Center: a close-up of the gravitational lens in which the red foreground galaxy is causing the light from the more distant Shadow Blaster galaxy to bend around it, creating multiple distorted images of the galaxy that appear as yellow arcs.

Right: a close-up of the gravitationally lensed Shadow Blaster galaxy.

These images were captured with the Atacama Large Millimeter/submillimeter Array (ALMA) and the Gemini North telescope, one half of the International Gemini Observatory, partly funded by the U.S. National Science Foundation and operated by NSF NOIRLab.

Credit: International Gemini Observatory/NOIRLab/NSF/AURA/ALMA (ESO/NAOJ/NRAO) Image Processing: T.A. Rector (University of Alaska Anchorage/NSF NOIRLab), D. de Martin & M. Zamani (NSF NOIRLab) Acknowledgment: PI: Yuji Urata (MITOS Science Co., LTD.)

Neutrinos are one of the fundamental particles of the Universe. They live a ghostly existence with no electric charge, very little mass, and extremely few interactions with matter. They are also the most abundant particles with mass in the Universe, and can be created through a variety of processes, such as the decay of heavy particles, nuclear reactions in the Sun, and the explosions of stars.

Instruments on Earth have detected high-energy neutrinos arriving from space since the 1960s, and identifying their origin has been a long-standing challenge in astronomy. While scientists have identified a small number of nearby neutrino sources [1], they cannot account for the total amount of neutrinos our instruments measure arriving from across the Universe, referred to as the cosmic neutrino background. Astronomers, therefore, suspect that other major source populations exist but remain hidden.

In a study published today in Nature Astronomy, a team led by Yuji Urata of MITOS Science Co., LTD. in Taiwan presents the analysis of a new neutrino source candidate — an extremely bright galaxy, JCMT0402−0424, nicknamed “Shadow Blaster.” This galaxy is located about 11 billion light-years away, has trillions of times the luminosity of the Sun in the infrared, and may provide the long-sought link between high-energy neutrino production and distant star-forming galaxies.

The discovery was made in part using observations from the Gemini North telescope, one half of the International Gemini Observatory, partly funded by the U.S. National Science Foundation (NSF) and operated by NSF NOIRLab. The study also utilized observations from the James Clerk Maxwell Telescope (JCMT), operated by the East Asian Observatory, and the Submillimeter Array (SMA), a joint operation between the Center for Astrophysics | Harvard & Smithsonian and the Academia Sinica Institute of Astronomy and Astrophysics. All three of these telescopes are located on the summit of Maunakea in Hawai‘i.

In 2021, the NSF IceCube Neutrino Observatory in Antarctica alerted the scientific community to a high-energy neutrino event, dubbed IC 210922A, coming from a region of space in the direction of the constellation Eridanus. This alert triggered rapid follow-up observations across the electromagnetic spectrum to search for a counterpart signal that, if detected, could help identify the neutrino’s source.

Multiple teams of scientists conducted follow-up observations using a variety of telescopes and instruments. However, they all reported no convincing gamma-ray, X-ray, or optical counterpart, nor any gamma-ray burst, supernova, or tidal disruption event that could be associated with the alert [2].

Then, a couple of days after the initial alert, Urata and his team initiated observations with JCMT and SMA and discovered Shadow Blaster, whose location and brightness made it a promising candidate for the source of the signal. To investigate this galaxy further, the team organized follow-up observations with the Atacama Large Millimeter/submillimeter Array (ALMA), managed for North America by the NSF National Radio Astronomy Observatory, and they discovered that Shadow Blaster is located behind a strong gravitational lens[3].

Thanks to this lensing effect, the team would be able to study the internal structure of Shadow Blaster, which would otherwise be too distant and too faint to resolve in such detail. However, to use the lensing effect correctly and to understand how much the lens amplified the neutrino signal, they first needed to know the distance, nature, and mass distribution of the foreground galaxy. To decipher these details, they used two powerful instruments on Gemini North: the Gemini Multi-Object Spectrograph (GMOS) and the Gemini Near-InfraRed Spectrograph (GNIRS).

“The combined GMOS and GNIRS data helped us measure the distance to the lensing galaxy and determine that it is a massive elliptical galaxy. This information was crucial for estimating the lens mass distribution and constructing a model of the gravitational lens,” says Urata.

Combining the lens model with the ALMA imaging data revealed that the central region of Shadow Blaster contains an extremely compact core that is densely packed with gas and dust and forming new stars at an intense rate. Theoretical models predict that such an extreme environment can act as a natural particle accelerator, where energetic particles repeatedly collide with gas and produce neutrinos. Additionally, Shadow Blaster does not display any characteristics of possessing an active black hole. This strongly suggests that high-energy neutrinos can be produced not only by spectacular black-hole jets as scientists have observed in nearby galaxies, but also by the intense, densely packed star formation that is common in very distant galaxies.

“This breakthrough shows how particle detectors and telescopes become far more impactful when they work together, opening a powerful 'multi-messenger' window on the Universe,” says Martin Still, Program Director, NSF Office of Research Infrastructure. “By combining signals from particles and light, scientists can explore distant cosmic environments and events in unprecedented detail — revealing phenomena that were once only theoretical.”

Around 10 billion years ago, the Universe was populated with galaxies like Shadow Blaster that were actively forming stars. During this epoch, galaxies were theoretically producing large numbers of cosmic rays, which are high-energy streams of particles that can generate neutrinos. Yet obtaining observational evidence that links an individual neutrino event to such a distant galaxy has been extremely difficult since these galaxies are very far away and often deeply hidden behind thick layers of dust. Shadow Blaster's serendipitous location behind a gravitational lens makes finding this observational evidence much easier.

“Shadow Blaster possesses the kind of dense, gas-rich environment that theoretical models have long suggested could efficiently produce high-energy neutrinos,” says Urata. Combined with the absence of any more compelling counterpart despite extensive follow-up searches, Shadow Blaster is the most plausible candidate for the source of IC 210922A. “If confirmed, Shadow Blaster would be the first-ever individual dusty star-forming galaxy directly linked to a high-energy neutrino event.”

Compact star-forming galaxies like Shadow Blaster may be numerous throughout the Universe. As a population, they may therefore contribute a significant fraction of the high-energy neutrino background that fills the cosmos. “Our analysis suggests that this population could contribute up to roughly 20% of the observed diffuse neutrino background measured by IceCube,” says Urata.

Notes

[1] Astrophysical neutrino sources, or candidate source associations, that have been identified include the Sun and Supernova 1987A at lower energies, and, at high energies, the blazar TXS 0506+056, the active galaxy Messier 77, the active galaxy PKS 1424+240, and diffuse emission from the plane of the Milky Way. Candidate high-energy associations have also been reported with tidal disruption events such as AT2019dsg and AT2019fdr.

[2] Facilities used for follow-up observations: NASA's Fermi Gamma-ray Space Telescope, ANTARES neutrino telescope, NASA's Neil Gehrels Swift Observatory, Zwicky Transient Facility, High-Altitude Water Cherenkov Observatory, and the Department of Energy-funded DESI Transients Survey. In particular, DESI “spare fibers” — fibers that can’t be matched to targets from the main DESI program on a given pointing — obtained spectra for 249 galaxies within the IceCube localization region.

[3] Gravitational lensing occurs when a very massive foreground galaxy bends spacetime, acting as a cosmic magnifying glass that enlarges and distorts the image of a more distant galaxy behind it. In this case, the gravitational lens amplified the brightness of Shadow Blaster from 2.7 trillion to 33 trillion times the luminosity of the Sun in infrared light.

More information

This research is presented in a paper titled “Compact dusty starbursts at cosmic noon linked to high-energy neutrinos,” appearing in Nature Astronomy. DOI: 10.1038/s41550-026-02884-9.

The team is composed of Y. Urata (MITOS Science Co., LTD/National Central University, Taiwan), K. Huang (Chung Yuan Christian University, Taiwan), B. Hatsukade (National Astronomical Observatory of Japan/The Graduate University for Advanced Studies/The University of Tokyo, Japan), M. Kasliwal (California Institute of Technology, USA), S. S. Kimura (Tohoku University, Japan), Y. Matsuda (National Astronomical Observatory of Japan/Ministry of Education, Culture, Sports, Science and Technology, Japan), Y. Miyamoto (Fukui University of Technology, Japan), H. Nagai (National Astronomical Observatory of Japan/The Graduate University for Advanced Studies, Japan), K. Nakanishi (National Astronomical Observatory of Japan/The Graduate University for Advanced Studies, Japan), and R. Stein (University of Maryland/NASA Goddard Space Flight Center, USA).

The scientific community is honored to have the opportunity to conduct astronomical research on I’oligam Du’ag (Kitt Peak) in Arizona, on Maunakea in Hawai‘i, and on Cerro Tololo and Cerro Pachón in Chile. We recognize and acknowledge the very significant cultural role and reverence of I’oligam Du’ag to the Tohono O’odham Nation, and Maunakea to the Kanaka Maoli (Native Hawaiians) community.

The James Clerk Maxwell Telescope is operated by the East Asian Observatory, which is funded by the Academia Sinica Institute of Astronomy and Astrophysics (ASIAA, Taiwan), the National Astronomical Research Institute of Thailand (NARIT), the Science and Technology Facilities Council (STFC, United Kingdom), and other partners.

Compact dusty starbursts at cosmic noon linked to high-energy neutrinos

Article Publication Date

17-Jun-2026

This image shows the field around the gravitationally lensed galaxy nicknamed "Shadow Blaster." This galaxy lies 11 billion light-years away and sits just behind the bright red galaxy at the center of this image. The red foreground galaxy acts like a cosmic magnifying glass, enlarging and distorting the image of the more distant Shadow Blaster galaxy behind it.

International Gemini Observatory/NOIRLab/NSF/AURA/ Image Processing: T.A. Rector (University of Alaska Anchorage/NSF NOIRLab), D. de Martin & M. Zamani (NSF NOIRLab) Acknowledgment: PI: Yuji Urata (MITOS Science Co., LTD.)

This image shows the gravitationally lensed galaxy nicknamed "Shadow Blaster," which astronomers have identified as the likely source of the high-energy neutrino event IC 210922A, detected by the IceCube Neutrino Observatory in 2021.Gravitational lensing occurs when a very massive foreground galaxy bends space-time,

acting as a cosmic magnifying glass that enlarges and distorts the image of a more distant galaxy behind it. In this case, the red foreground galaxy is bending the light of the more distant Shadow Blaster galaxy, creating multiple distorted images of it that appear here as yellow arcs.

This composite image was created using data from the Atacama Large Millimeter/submillimeter Array (ALMA) and the Gemini North telescope, one half of the International Gemini Observatory, partly funded by the U.S. National Science Foundation and operated by NSF NOIRLab.

Credit

International Gemini Observatory/NOIRLab/NSF/AURA/ALMA (ESO/NAOJ/NRAO) Image Processing: T.A. Rector (University of Alaska Anchorage/NSF NOIRLab), D. de Martin & M. Zamani (NSF NOIRLab) Acknowledgment: PI: Yuji Urata (MITOS Science Co., LTD.)

This image shows a close-up of the gravitationally lensed galaxy nicknamed "Shadow Blaster," which astronomers have identified as the likely source of the high-energy neutrino event IC 210922A, detected by the IceCube Neutrino Observatory in 2021.

Gravitational lensing occurs when a very massive foreground galaxy bends spacetime, acting as a cosmic magnifying glass that enlarges and distorts the image of a more distant galaxy behind it. In this case, a foreground galaxy, which is not visible in this image, is bending the light of the more distant Shadow Blaster galaxy, creating multiple distorted images of it that appear here as yellow arcs.

Credit

NOIRLab/NSF/AURA/ALMA (ESO/NAOJ/NRAO) Image Processing: T.A. Rector (University of Alaska Anchorage/NSF NOIRLab), D. de Martin & M. Zamani (NSF NOIRLab)

The James Clerk Maxwell Telescope located near the summit of Maunakea in Hawai‘i.

Credit

William Montgomerie, EAO/JCMT

The Submillimeter Array at the summit of Maunakea in Hawaiʻi.