It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Wednesday, September 17, 2025

Japan's JERA Looks to Seal $1.7 Billion U.S. Shale Gas Deal

Japanese energy firm JERA is in advanced discussions to buy shale gas assets in the United States worth about $1.7 billion, sources with knowledge of the talks have told Reuters.

If a deal is finalized, this would be a major investment from Japan in the U.S. energy industry, per the U.S.-Japan trade agreement.

JERA, Japan’s biggest power producer, has emerged as the top bidder to buy assets currently owned by GEP Haynesville II in the Louisiana shale basin Haynesville, according to Reuters’ sources.

GEP Haynesville II is a joint venture (JV) between GeoSouthern Energy and Williams Cos, and operates around 50,000 net acres in the Haynesville shale formation.

Japan and JERA are exploring offtake agreements to buy LNG from the planned export project in Alaska as part of the Japanese pledge to buy $7 billion worth of U.S. energy products. Earlier this month, U.S. President Donald Trump signed an executive order to implement the U.S.-Japan trade agreement reached in July.

Under the agreement, Japan gets a 15% tariff on its goods and pledges to buy $8 billion worth of American products per year. The Government of Japan has agreed to invest $550 billion in the United States, the White House said.

Japanese companies have been considering investments in the $44-billion Alaska LNG project, but they have appeared to be concerned that the costs may be too high, considering the cold weather in Alaska and the scale of the pipelines needed to bring the project on stream. But after the trade agreement, Japan is now actively considering offtake deals.

JERA, in particular, is reportedly considering joining companies making commitments for purchases of liquefied natural gas from the Alaska LNG project, with a preliminary letter of intent mentioning 1 million tons annually over a 20-year period.

The developer of the $44-billion Alaska LNG project, Glenfarne, has been busy in the past months finding companies willing to make offtake commitments. The company is yet to make a final investment decision on Alaska LNG, but plans to make one for the facility’s pipeline by the end of the year, and another for its export terminal in 2026.

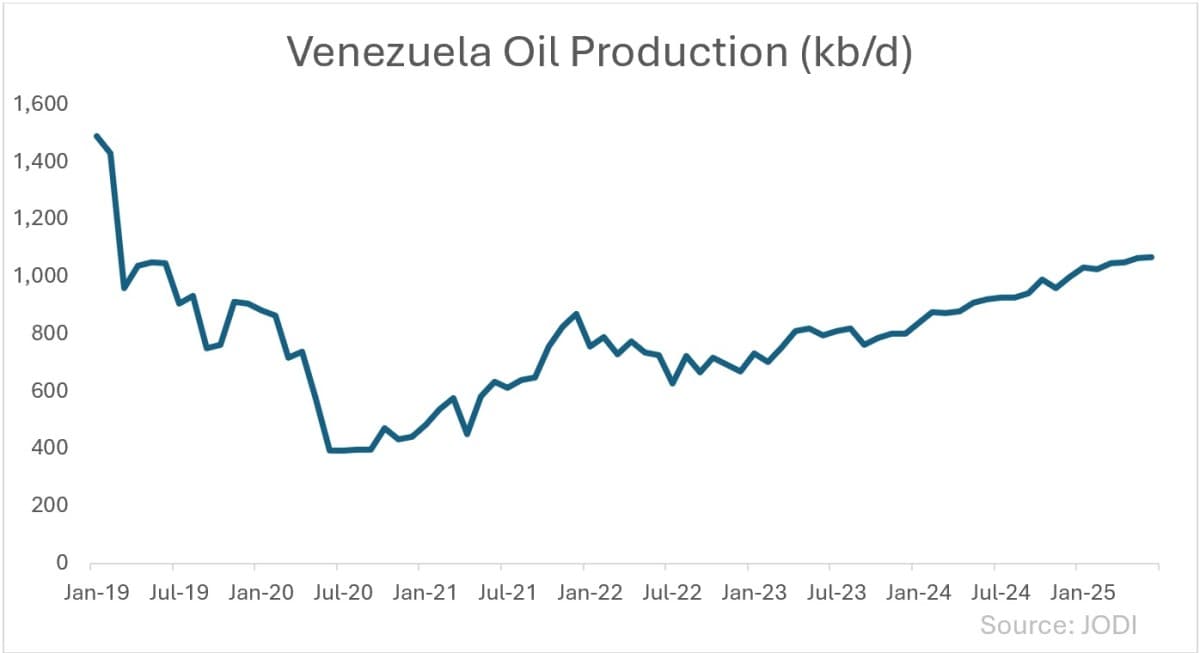

Chevron’s return to Venezuela has revived oil flows to the US —but beneath the surface lies a volatile mix of sanctions, waivers, and political risk.

Venezuela avoided a production collapse over the summer months when Chevron was barred from operating, supported by robust Chinese demand.

Despite favourable economics, Chevron’s future in Venezuela remains hostage to Washington’s geopolitical calculus—not market fundamentals.

Chevron has returned to Venezuela, but the move may prove problematic given the frictions in the US–Venezuela relations. What appears at first as an oil company regaining lost ground could be in fact another failed attempt to normalize oil production in Venezuela, marred by high-stakes political games.

The seesawing of US policy on Venezuela began in 2019, when Donald Trump’s first administration imposed sweeping sanctions on Venezuela’s state oil company PDVSA. The measures prohibited any US persons and companies from doing business with it, effectively shutting Venezuelan crude out of the US market. Imports halted entirely, and Caracas was forced to rely on opaque routes to Asia while its domestic infrastructure was steadily collapsing. Nearly 4 years later, under President Joe Biden, a narrow opening appeared. In 2022, the Treasury allowed Chevron to restart work in its Venezuelan joint ventures – Petroboscán (where it owns about 40 %), Petroindependiente (25%), Petropiar (30%), and Petroindependencia (around 35%) alongside smaller partners. The waiver came with tight conditions: revenues could only be used to cover operating costs or repay billions of dollars in arrears that PDVSA owed Chevron, in the form of unpaid dividends, cost reimbursements, and loans for project development. No finances were allowed to reach PDVSA or the central government.

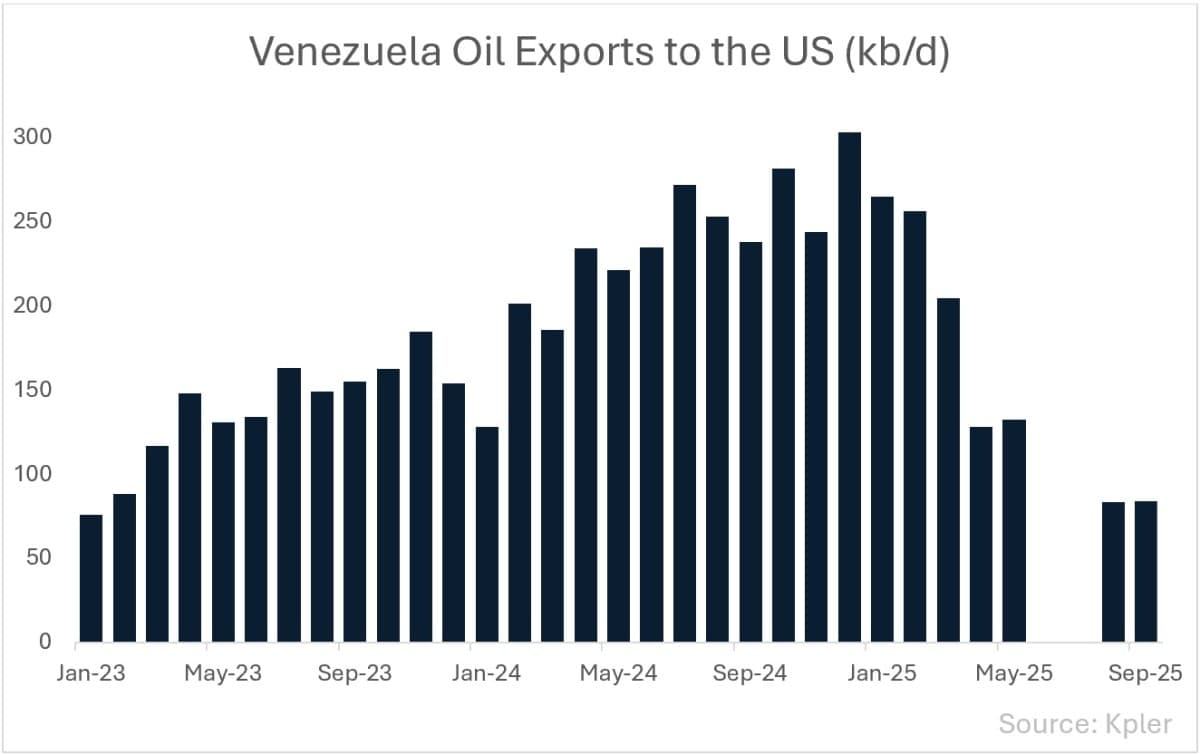

Even under those restrictions, Venezuela’s oil sector rebounded. Output climbed steadily from 715,000 b/d in 2022 to around 900,000 b/d in early 2025, while US imports of Venezuelan crude rose from some 75,000 b/d in January 2023 to nearly 300,000 b/d by December 2024. Chevron gained access to discounted heavy crude well suited to its refining system, and PDVSA benefited from foreign expertise and a legal export outlet that consolidated its operations. Moreover, the Venezuelan government started receiving Chevron’s equivalent of royalties in incremental production that it could send towards Asian markets, too.

That trajectory was broken with Trump’s return to the White House. In February 2025, his administration revoked Chevron’s license, ordered a 30-day wind-down period, and imposed a 25% tariff on all U.S. imports from countries that buy Venezuelan oil. With China taking 85 to 90% of Venezuela’s exports by mid-2025, the measure looked like another front in Washington’s economic confrontation with Beijing. In May, a narrow authorization was granted to Chevron to preserve assets and reduce seizure risks, but that did nothing for exports. Shipments to the US vanished entirely by June. Then, in late July, Treasury quietly issued a restricted license allowing Chevron to resume operations without making direct payments to PDVSA or the Venezuelan state. Details of the license were not disclosed, unlike earlier waivers. But tankers sailed almost immediately: in August, US imports of Venezuelan crude resumed at 84,000 b/d, according to Kpler data.

The context for Chevron’s return is more complex than it appears. During the company’s two-month absence in the summer, Venezuela’s crude production remained surprisingly steady. Official figures from Caracas put output at more than 1.1 million b/d in June and July, though the export and refining volumes suggest those numbers likely include condensate and natural gas liquids, inflating the totals. Even so, export flows tell a similar story: shipments held steady at around 700,000 b/d, revealing the country’s ability to sustain stable volumes despite Chevron’s temporary absence, mostly thanks to Chinese buyers. This suggests that the US company’s comeback in August should result in rising crude production and export numbers in the months to come.

The economics are clear. Production costs for Venezuela’s heavy crude remain well below current oil prices at around $30-35 per barrel, and Chevron’s refineries – particularly Pascagoula, Mississippi – are designed to process it. Little surprise then that the first cargoes after Trump’s July waiver headed straight from the José terminal to Pascagoula. There were rumours on the market suggesting Chevron might be reselling Venezuelan barrels to other US refiners, and data confirmed it: in August and September, most of the cargoes Chevron lifted ended up at Valero’s Port Charles and Port Arthur refineries.

The physical nature of Venezuelan crude adds another complication. Much of it is extremely heavy, often below 10 degrees API, and cannot flow without dilution. PDVSA blends it with lighter products such as naphtha to produce diluted crude oil grades like Hamaca DCO. Diluent imports, therefore, reflect prospective export potential. When exports to the US halted in June and July, naphtha inflows dropped to their lowest levels since late 2023. As Chevron’s operations resumed in August and September, naphtha imports surged again. The source of those imports has also shifted: before Trump’s full ban, most diluent came from the US, but now Russia has become the main supplier. This begs the question whether Chevron sees the Trump waiver as a temporary stopgap measure rather than a long-term solution, remaining wary to supply its own naphtha as it did before 2025.

For Venezuela, Chevron’s role is indispensable. Every license renewal since 2019 must have caused many sleepless nights in Caracas: the US major’s operations have underpinned Venezuela’s fragile production recovery and provided a lifeline of incremental export volumes. Even the short suspension in June-July undermined PDVSA’s finances and highlighted its dependence on Chevron’s know-how to keep fields in the Orinoco Belt running. For Chevron, the seesawing of US foreign policy has been detrimental to the sustainability of its operations. Its sanctions waivers were rescinded on several occasions, from GL-41 to GL-41A to GL-41B, with little notice, and could be revoked again.

Trump has sharpened Washington’s posture, linking sanctions on Venezuela to drugs, crime, and migration. In September 2025, the administration declared Venezuela a major drug-transit country that had ‘failed demonstrably’ to meet its obligations. The announcement came days after US forces struck two Venezuelan vessels accused of drug trafficking, strikes that president Nicolás Maduro denounced as ‘aggressions’.

Amidst plunging Mexican crude exports to the US, the Trump administration ought to weigh the pros and cons of depriving the US Gulf Coast of much-needed heavy barrels. Therefore, it is most likely that Chevron will maintain its restricted license all the way through the remaining months of 2025, shipping part of its Venezuelan equity volumes to Pascagoula and reselling some barrels to Valero. But the downside is clear: a fresh political confrontation could push Washington to cancel the waiver, dropping US imports back to zero. At the end of the day, Trump’s second administration is actively showcasing that for them, economics is secondary – and the timetable is set by politics.

Chevron and state-owned Israel Natural Gas Lines Ltd have signed an agreement to build a natural gas pipeline from Israel’s giant Leviathan gas field to Egypt, Leviathan project participant NewMed Energy has said.

Chevron’s unit Chevron Mediterranean Limited, the operator of the Leviathan Project, agreed with Israel Natural Gas Lines to provide transmission services for the flow of natural gas from the Leviathan reservoir to Egypt through the Nitzana Project.

The project is for onshore connection between the Israeli transmission system and the Egyptian transmission system in the Nitzana area, said NewMed Energy, which leads a partnership with a 45.34% in Leviathan.

The project includes the construction of a pipeline and a compressor station in the Ramat Hovav area in southern Israel and about 65 km of pipeline (40 miles) to the Nitzana border crossing.

The new pipeline will enable up to 600 million cubic feet per day to flow toward Egypt once the project comes on stream.

Chevron plans to raise Israeli pipeline gas deliveries and add more U.S. LNG into Egypt to cover surging demand, even as regional tensions persist.

“Egypt needs all the gas it can get,” said Freeman Shaheen, Chevron’s president for global gas, at the Gastech conference in Milan last week, per Bloomberg.

Egypt flipped back to LNG importing last year after domestic output fell, tightening its power balance and pushing it to tap more spot and term cargoes. New floating import terminals have come online, and 2025 LNG receipts have already doubled versus 2018 levels. Piped volumes from Israel have become a core pillar of supply.

Chevron operates Israel’s Leviathan and another offshore field that feed gas to Egypt. Leviathan was briefly shut during the Israel-Iran conflict for security reasons, but flows have resumed. In August, Israel and Egypt unveiled a long-term gas agreement worth roughly $35 billion—Israel’s largest to date—reinforcing Cairo’s import strategy.

In the old days, big factories joined the grid and everyone’s rates fell thanks to economies of scale; that era is over.

AI/data centers need massive new power and water, forcing pricey grid upgrades that utilities will likely spread across all customers—think ~15% higher bills, especially for households.

Unless AI’s benefits are guaranteed and broadly shared, Big Tech should cover its own electricity tab, not socialize it through your bill.

That seemed to be the argument. The academic patiently explained to the TV interviewer that cost of electricity would rise for all consumers because putting those big AI centers into operation would raise costs for the grid, and everyone has to share grid costs. That’s the way it always worked. That’s the way it works, so tighten your belt and stop complaining.

Actually that was not how he put it, but you get the idea. So, let’s go back in time when large industrial users of electricity produced their own, because that was cheaper than buying from the local utility. They began to buy from the utility when utility power looked like a better buy, and it became in part a better buy because they switched to the utility. Large industrial power users added volume to the utility grid that enabled the utility to take advantage of economies of scale. The utility’s overall cost per unit fell for all customers. It was a win-win situation, to use an overused term. Later on, in the 1940s to 1960s, utilities and local governments pursued a policy of industrial development for the service territory. They wanted industry to move in because the new factory hired thousands of workers, paid taxes, and the additional demand for electricity enabled the utility to reach greater economies of scale, which lowered power prices. Everyone’s electric rates fell as a result. A true Goldilocks outcome.

That picture changed in the 1970s and 1980s when the electricity industry ran out of economies of scale, and double digit inflation raised both capital and operating costs dramatically, thanks in part to Middle East oil embargoes. And the cost of serving new electric load rose significantly over the cost of serving old load. In economic parlance, incremental cost exceeded average cost. At that point, electric companies started to preach the virtues of conservation, of more efficient use of electricity. They actually paid people to use less at strategic times.

Fast forward. Two decades of slow to no growth in electrical demand dampened interest in these matters. Now, huge corporations with immense wealth want to erect AI and data centers that will, over a short time, put immense pressure on local electricity and water resources. The utilities affected will have to put into service new assets that cost many times the cost of existing assets. We suspect that most of these utilities may already be operating at the limits of economies of scale, so we don’t expect to see cost reductions from added volume. Roughly speaking, we would expect the AI boom, if it materializes, to raise the price of electricity, on average, by at least 15%, and possibly more for residential customers who won’t get industrial discounts.

To put the case simply, in the past, the electric industry socialized the costs of new customers, especially large industrial customers, because doing so attracted new loads and that reduced per unit costs for everyone. Society benefited along with big power users. In the case of AI today, that means socializing large incremental costs and there are no savings. Socializing the costs incurred to serve loads like AI will raise costs for everyone. If you believe that AI will reduce economic costs for everyone in society, and cure numerous diseases, and the benevolent developers of AI will share those cost reductions and health benefits with the general public rather than pocket and monetize those goodies, then you might make a case to socialize AI’s electricity costs. Presumably, you also believe in the tooth fairy. We, on the other hand, don’t want to share our electric bills. They have enough money to pay their own.

By Leonard Hyman and William Tilles for Oilprice.com

Trump’s London Visit Coincides With a £31 Billion Tech Investment Surge

Microsoft will invest £22bn in UK AI infrastructure, including the country’s largest supercomputer, as part of a £31bn US-UK Tech Prosperity Deal.

Google, Nvidia, Salesforce, OpenAI, and others are also committing billions, expanding UK data centres, AI hubs, and quantum research.

While hailed as historic, the deal raises concerns about Britain’s technological sovereignty, reliance on US-led infrastructure, and uncertain nuclear financing.

Microsoft has announced its largest ever UK investment, pledging £22bn to expand AI infrastructure and build the country’s largest supercomputer, as president Donald Trump touched down in London for his state visit.

The commitment forms part of a wider US-UK Tech Prosperity Deal, encompassing £31bn of American investment across AI, quantum computing, and advanced nuclear energy in a move hailed as “historic” by tech chiefs and diplomats.

Prime minister Sir Keir Starmer described the mega cash injection as “a generational step change in our relationship with the US, shaping the futures of millions on both sides of the Atlantic, and delivering growth, security and opportunity up and down the country”.

Google is committing £5bn over two years to AI research and a new data centre in Hertfordshire, while Nvidia will deploy 120,000 processors – its largest European rollout – to accelerate British AI.

Salesforce is investing £1.4bn to make its UK operations an AI hub for Europe, and AI Pathfinder will commit over £1bn in computing capacity.

ChatGPT developer OpenAI will also partner with UK firm Nscale to launch the Stargate data centre in a new AI growth zone in the North East.

Tech Minister Kanish Narayan told City AM: “One of the things that’s very exciting, in particular in relation to the growth zones, but also on our wider investment announcements with Microsoft, is that Nscale – a British headquartered firm – is going to be right at the heart of it”.

He added that commitments on Nvidia chips include British firm Arm “being right at the heart of powering that as well, in terms of chip design”.

On quantum, he noted “both smaller companies like Cesco Magnetics… but also Oxford Quantum Circuits and Oxford Ionics are right at the heart of the commercial investments that we’re hoping to announce”.

A person close to the matter told City AM that no regulatory or planning changes have yet been made in response to the investment plans, although a memorandum of understanding on licensing and safety was signed yesterday.

City AM understands that data centres will be fast-tracked, while the nuclear element of the deal is a medium-term commitment.

Companies involved in small modular reactors, such as Rolls-Royce, are seeking revenue support for investment, though it is unclear whether this will affect taxes or consumer bills.

On AI, the government sees the UK positioned between EU and US regulatory approaches, allowing scope to develop trade with both markets.

State-backed institutions like the AI Security Institute are expected to be crucial in enabling UK companies to scale and in fostering a domestic AI ecosystem.

Jensen Huang, Nvidia’s chief, called the agreement “a historic chapter in US–United Kingdom technology collaboration” and said “The United Kingdom stands in a Goldilocks position, where world-class talent, research and industry converge.”

Sam Altman, OpenAI’s chief executive, said: “The UK has been a longstanding pioneer of AI, and is now home to world-class researchers, millions of ChatGPT users, and a government that quickly recognised the potential of this technology.”

A test of sovereignty amid US-led investment

While the deal promises a surge in infrastructure and investment, questions over technological independence remain and there are concerns that amid the US investment, domestic startups could struggle to retain independence amid heavy US involvement.

The UK government promises that the partnership will encourage a sovereign AI ecosystem, while initiatives like the AI Security Institute and the Stargate project aim to bolster homegrown capabilities.

Yet concerns persist over potential reliance on US-led infrastructure and uncertainty over nuclear revenue support, which may leave taxpayers exposed.

Shadow Science, Innovation and Technology secretary Julia Lopez also warned that despite this “vote of confidence”, declining foreign investment and paused pharmaceutical projects highlight structural challenges in the UK’s innovation landscape.

She added that “Britain has world-leading scientists, innovators and tech firms, but this country’s potential is being squandered.”

“The loss of major pharmaceutical deals, including AstraZeneca’s decision to pause its planned £200m nvestment in Cambridge, is a damning indictment of Labour’s failure to provide a stable and competitive business environment”, she said.

The deal could accelerate breakthroughs in medicine, clean energy, and AI-driven research, but its success will hinge on whether Britain can leverage US capital to truly become an ‘AI maker’, rather than a consumer of foreign technology.

China churned out less coal and steel in August as the government tightened controls on production.

Coal output dropped year-on-year for a second consecutive month and steel for a fourth. Other construction materials such as cement and glass also declined as the impact of China’s years-long property crisis continues to reverberate.

Factory deflation in August eased for the first time in six months, offering an early indication that Beijing could be making headway with its anti-involution drive. Curtailments of heavy industry around Beijing to clear the skies for a military parade in early September also affected commodities like steel.

The 3.2% decline in coal output to 391 million tons came after heavy rains and government curbs on overmining. Firms were under less pressure to produce as power needs rose only modestly due to a slowing economy and milder August weather, while renewables continue to make an increasing contribution to electricity generation.

Steel, another industry in the crosshairs of the campaign to rein in excessive competition, saw production drop 0.7% to 77.4 million tons. Mills have been reducing output to lift margins since May. The nationwide total was also suppressed by anti-pollution curbs in the steelmaking hub of Hebei that neighbors the capital, where the parade marking the end of World War II took place.

Among other commodities, aluminum output was steady at 3.8 million tons, while oil refining surged 7.6% to 63.5 million tons as more plants restarted following seasonal maintenance.

Upstream crude and gas output also increased, as drillers remain committed to delivering energy security and cutting the nation’s import bills.

US in talks to set up $5 billion fund for critical mineral deals

The US is in talks to set up a $5 billion fund to invest in mining, in what would be the government’s most significant foray into dealmaking to boost supplies of critical minerals.

The US International Development Finance Corp. is in discussions to establish the fund as a joint venture with New York-based investment firm Orion Resource Partners, according to people familiar with the matter, who asked not to be identified because the talks are private. Key details are still being negotiated, and there’s no certainty a deal will be agreed, they said.

Trump has touted the prospect of minerals deals in Ukraine and Greenland, while the White House is also keen to promote US investment into the Democratic Republic of Congo’s mining industry. But the joint fund with Orion, if it is finalized, would provide a new avenue for the US government to engage in large-scale deals itself.

The Trump administration has made it a priority to shore up access to critical minerals such as copper, cobalt and rare earths. The logic behind the potential collaboration between the DFC and Orion is widespread anxiety about supply.

In the near term, concerns are fixed on China, which processes the bulk of a wide range of minerals from copper to antimony, while Chinese companies continue to snap up overseas mining assets to feed facilities at home. In the longer run, deep shortages are forecast for some metals due to insufficient investment, declining grades and protracted permitting processes.

A representative for Orion declined to comment. A DFC official declined to comment on potential projects, but said it is seeking collaboration with both private sector partners and host governments in eligible countries.

Created towards the end of Trump’s first term, the DFC has already approved multiple investments in the mining industry, via credit, equity stakes and technical assistance grants. That includes a loan of $150 million to support Syrah Resources Ltd., which operates a graphite mine in Mozambique and has a deal to supply the battery material to Tesla Inc.

During Joe Biden’s presidency, the DFC also committed more than $550 million in financing to upgrade the Lobito Corridor’s railway infrastructure, which transports minerals from central Africa’s copper-belt to an Atlantic port in Angola. If the DFC was to commit the full $2.5 billion, the venture with Orion could rank as the largest in the agency’s history, government data indicate.

Orion is a major financier to the mining industry, with about $8 billion in assets under management and a business spanning private equity, private credit, venture capital and commodity trading.

The partnership being considered would see both parties provide the same amount of money, scaling up over time towards a combined total of about $5 billion, the people said. The structure would be similar to the $1.2 billion venture that Orion announced earlier this year with Abu Dhabi sovereign wealth fund ADQ, according to one of the people.

Orion’s chief executive officer, Oskar Lewnowski, has previously told Bloomberg News that nation states need to take a more active role in critical minerals markets, and urged them to follow China’s example by building strategic stockpiles as a buffer against supply shocks.

Last month, the Department of Defense launched its first tender to stockpile cobalt since the end of the Cold War. In July, the Pentagon also made a landmark $400 million investment in US rare earths producer MP Materials, and struck a supply deal with a guaranteed floor price to protect the firm’s profits during market downswings.

Orion is already in talks to buy a copper-cobalt miner in Congo that’s become a symbol of the growing competition for mineral deals between the US and China. The central African country is the world’s biggest producer of cobalt and second-largest source of copper, with output of both metals surging in recent years after investments by Chinese miners.

Lewnowski’s firm has teamed up with Virtus Minerals – which is run by veterans of the US military and intelligence services – to bid for Chemaf Resources Ltd, Bloomberg News reported in July.

A previous deal for a unit of Chinese state-owned arms manufacturer Norinco Group to acquire Chemaf was abandoned because Congo withheld the necessary approvals, while US officials also urged President Felix Tshisekedi’s administration to prevent the transfer to the Chinese firm.

The DFC is set to become a more important part of US foreign and economic policy in Trump’s second term, with the White House seeking to double or triple its investment capacity through a reauthorization process expected to happen next month. The organization is also expected to gain flexibility to invest in wealthier countries and take on riskier projects so it can attract more private-sector backers.

Trump picked Ben Black – the son of billionaire Apollo Global Management Inc. co-founder Leon Black – to lead the DFC in January, but the Senate is yet to approve the appointment. In his confirmation hearing three months ago, the younger Black told lawmakers that the federal agency “should never be crowding out private capital” and must have more exposure to New York City financial firms.

(By William Clowes, Jack Farchy and Loukia Gyftopoulou)

US interested in funding Friedland-backed scandium project

A drill site at the Sunrise cobalt-nickel-scandium project in Australia, 350 km west of Sydney. Credit: Clean TeQ Holdings

Sunrise Energy Metals (ASX: SRL), an Australian scandium explorer backed by Robert Friedland, is being lined for a potential loan from the Export-Import Bank of the United States (EXIM) for its Syerston project in central New South Wales.

As stated in a letter of interest, announced by the company Tuesday, EXIM would provide a debt financing up to $67 million. Based on current estimates, this amount represents approximately half of the project development costs, the company said.

The Syerston project, located 450 km west of Sydney, hosts one of the world’s largest and highest-grade scandium deposits, with nearly 46 million tonnes of measured and indicated resources at a grade of 414 parts per million. The resource was recently updated and has double the contained metal (19,000 tonnes) over its previous estimate.

The EXIM, in its letter, cited the Syerston scandium project as a potential candidate to support the development of a reliable and secure supply chains for the US industry. The mineral is vital to some of the most important civilian and defence sector technologies, from semiconductors that power mobile communications to aerospace and automotive applications.

Shares in Sunrise climbed almost 30% on Tuesday in Sydney to A$4.35 each. Year-to-date, the stock price is up around an eye-popping 1,800%, leaving the company with a market capitalization of A$513 million ($343m).

The US accounts for approximately 90% of the overall demand, but its rival China controls most of its supply, making the mineral easily exposed to supply chain disruptions.

“Global supply remains tight since China’s export controls were imposed in April 2025, positioning Syerston as a strategically important source for future scandium supply,” Sunrise’s managing director Sam Riggall said in a press release last week.

Friedland, co-chair of Sunrise, said the letter from EXIM underscores the importance of scandium to the US, with the metal serving as a critical component in key sectors.

“As a key ally of the United States, Australia’s significant endowment of strategic metals positions it to be an important supplier in the future,” he said.

Should the company proceed with a formal loan application, the bank will conduct due diligence to determine if a final lending commitment would be made based on its criteria and the project’s eligibility.

“We are encouraged by this strong show of support by EXIM for the financing and development of the Syerston scandium project. We expect it to strengthen our engagement with customers to secure off-take arrangements as we move the project towards a final investment decision and development,” Riggall added.

The company is currently in the process of completing a feasibility study for Syerston, expected in mid-to late October 2025.

In addition to Syerston, Sunrise also holds a nickel-cobalt project in NSW. This project, which shares the same name as the company, is said to host the largest cobalt deposit outside the Democratic Republic of Congo, with a contained cobalt resource of 170,000 tonnes.