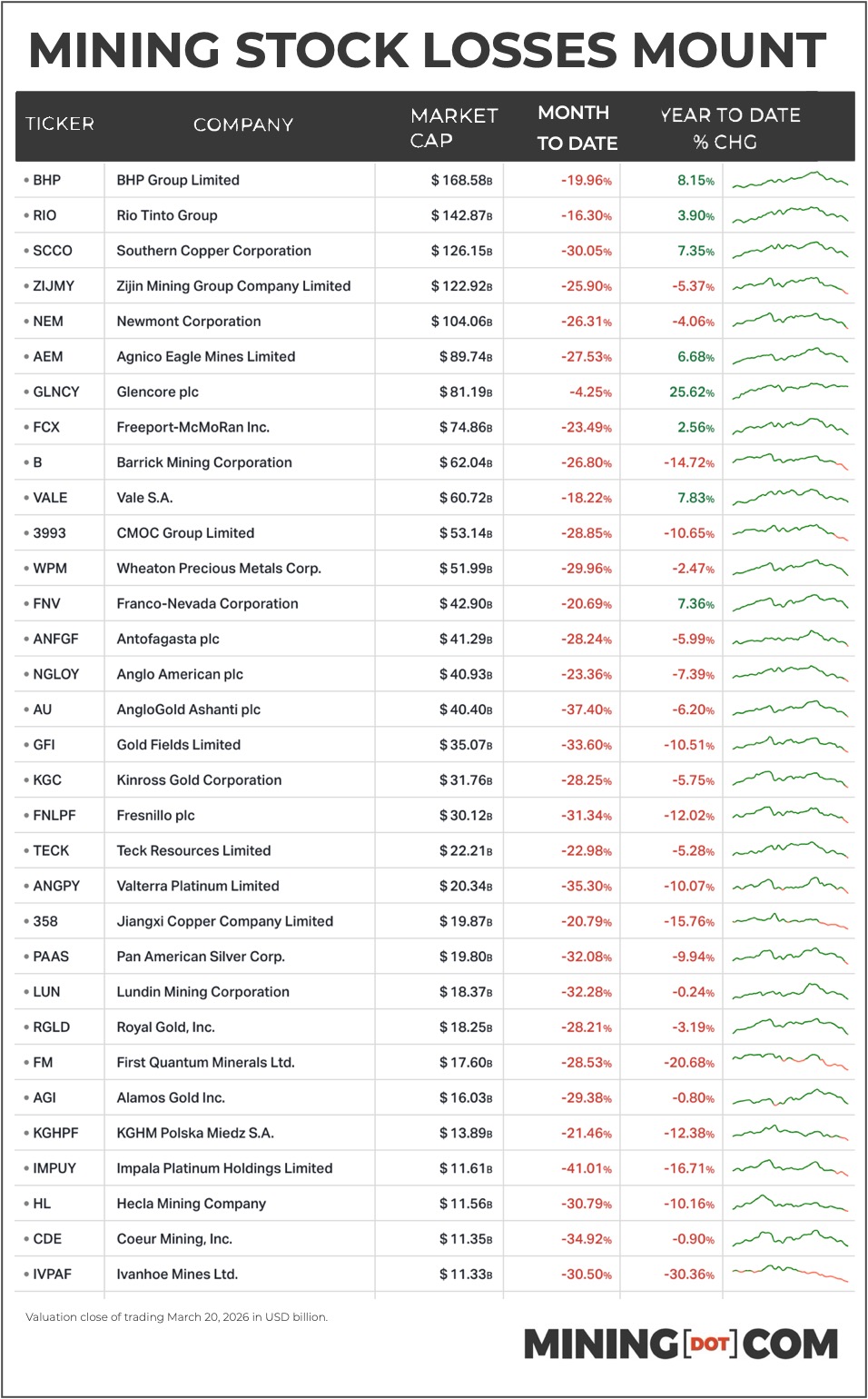

US House Democrat blasts Commerce’s ‘highly concerning’ $1.6B USA Rare Earth deal

A senior House Democrat accused US Commerce Secretary Howard Lutnick on Thursday of structuring Washington’s $1.58 billion investment into USA Rare Earth in a way that gives the government “highly concerning” leverage over the company while boosting Lutnick’s family-run investment firm.

In a 10-page letter, Representative Zoe Lofgren, the ranking member of the House Committee on Science, Space, and Technology, wrote that the proposed deal would let the Commerce Department keep an equity stake even if it decides not to invest while also leaving the company reliant on a $1.5 billion private capital raise led by Cantor Fitzgerald, the financial firm previously led by Lutnick and now run by his sons.

“This deal creates a massive personal conflict by granting the Secretary of Commerce overwhelming leverage to influence the behavior of a private company while positioning him to promote the interests of his sons as a condition of his support,” wrote Lofgren, a California Democrat.

The letter offers a glimpse into the types of investigations Democrats could pursue if they regain power in Washington after the November midterm elections, as lawmakers scrutinize the administration’s aggressive use of federal financing and equity stakes to reshape supply chains for critical minerals and other strategic industries.

CEO Barbara Humpton and a spokesperson for USA Rare Earth were not immediately available to comment. The Commerce Department did not immediately respond to requests for comment.

Funding in exchange for equity stake

The Commerce Department’s CHIPS Program Office in January signed a non-binding letter of intent to provide up to $1.58 billion in funding to USA Rare Earth — including a $277 million grant and a $1.3 billion loan — in exchange for an equity stake of between 8% and 16%.

The funds are slated to help the company develop a mine in Sierra Blanca, Texas, slated to open by 2028, and a magnet manufacturing plant in Stillwater, Oklahoma, which is expected to open this year.

According to the company’s regulatory filings, the government could retain its equity stake even if the deal falls through or if funding is clawed back, a provision Lofgren called “deeply strange” for a federal investment.

The company must meet a series of milestones to receive the funding, including raising additional private capital, completing technical studies and demonstrating market demand for its manufacturing plans, according to the filing.

Lofgren argues those conditions could leave the company dependent on the discretion of Commerce officials and create the potential for undue influence, especially given that the private capital raise from Cantor Fitzgerald is a condition for finalizing the government investment.

“The interplay between the company’s vulnerability and your personal conflict is a glaring red flag,” Lofgren wrote.

The lawmaker also questioned whether the Commerce Department has legal authority to take equity stakes in companies under the CHIPS and Science Act, arguing that the law’s “other transaction” authority does not allow government stakes in private firms.

The Trump administration has used similar structures to take equity positions in a range of companies, arguing the investments are needed to strengthen domestic supply chains and national security.

Lofgren asked the department to provide the committee with documents tied to the deal’s negotiation by April 3.

Reuters reported in January that a US Senate committee is separately reviewing at least one other equity deal in the critical minerals sector.

(By Jarrett Renshaw and Ernest Scheyder; Editing by Sergio Non and Rod Nickel)

The Three Companies Rebuilding America’s Rare-Earth Arsenal

Three small American companies are quietly rebuilding one of the most strategically important supply chains in the modern economy - the rare-earth pipeline that feeds the magnets inside missiles, fighter jets, electric vehicles, and advanced manufacturing.

In California, MP Materials operates the Mountain Pass Mine, the country’s only large-scale rare-earth mining complex and the primary domestic source of rare-earth concentrate.

And in Utah, Energy Fuels processes monazite sands at the White Mesa Mill, producing rare-earth carbonate that feeds downstream refining and metal production.

In Ohio, REalloys already operates the only heavy rare-earth metallization capability in North America at its facility in Euclid, where rare-earth oxides are converted into the metals and alloys used to manufacture high-performance permanent magnets.

Now REalloys is expanding that platform, announcing a fully financed buildout of what is expected to become the largest heavy rare-earth metallization facility outside China.

The effort is unfolding with the full force of U.S. defense procurement policy behind it. Modern weapons systems - from missile guidance to radar and advanced aircraft - depend on rare-earth magnets, yet the supply chain for those materials remains heavily concentrated in China.

Beginning in 2027, U.S. procurement rules will prohibit defense systems from using magnets derived from Chinese rare-earth supply chains, forcing manufacturers to secure alternative sources.

“The establishment of heavy rare earth metal production on U.S. soil is a defining moment for North American industrial strategy,” said Stephen duMont, Chairman of REalloys. “The Ohio facility will create the metallization capability that bridges Canadian oxide production with U.S. magnet manufacturing — a critical link that’s never existed at scale in the West. This is not a pilot plant; this will be full scale commercial capacity, and full compliance with Title 50 defense sourcing requirements. This is how we rebuild supply sovereignty from the ground up.”

Reports from the South China Morning Post and Reuters indicate Washington may have only months of certain rare-earth inventories available for defense manufacturing if supply disruptions deepen. The warning comes as the United States continues a high-tempo air campaign against Iran that is consuming large quantities of advanced weapons systems.

For decades the United States and its allies allowed the most technically demanding stages of the rare-earth supply chain to migrate overseas. Mining continued in several countries, but the industrial processes that convert rare-earth oxides into metals and magnet materials consolidated overwhelmingly in China.

That concentration now represents one of the most sensitive vulnerabilities in the Western defense industrial base.

Beginning in 2027, U.S. procurement rules will prohibit defense systems from using magnets derived from Chinese rare-earth supply chains, forcing manufacturers to secure alternative sources across the entire value chain—from mining to metallization and magnet production.

And these three companies are doing it all…

#1 REalloys (NASDAQ:ALOY) — Rebuilding the Precision Stage of the Supply Chain

If mining begins the rare-earth supply chain, and processing takes it further, metallization is where the materials finally become usable.

Rare-earth oxides - the powder produced after separation - cannot go directly into manufacturing. Before magnets can be produced, those oxides must be chemically reduced into pure metals and blended into precise alloys that serve as feedstock for permanent magnet production. That step requires tightly controlled reactions, high-temperature furnaces, and complex process control systems capable of maintaining stable yields and purity across multiple rare-earth elements.

For decades, that metallurgical conversion took place overwhelmingly inside China.

In Ohio, REalloys is rebuilding that capability.

At its facility in Euclid, the company converts rare-earth oxides into finished metals and magnet alloys used by defense contractors and advanced manufacturers. It remains the only operating heavy rare-earth metallization capability in North America.

“Metallization is the least developed part of the value chain outside China,” said REalloys co-founder Tim Johnston. “It requires deep operating expertise and process control systems capable of managing complex variables in continuous production.”

Now the company is preparing to scale that capability significantly.

REalloys has announced plans to construct what is expected to become the largest heavy rare-earth metallization platform outside China, capable of converting rare-earth oxides into roughly 600 tons per year of high-purity metals, including neodymium, praseodymium, dysprosium and terbium.

Those metals form the core feedstock for permanent magnets used in electric motors, radar systems, drones, missile guidance units and advanced industrial machinery.

The expansion is being developed in partnership with the Saskatchewan Research Council, which is building North America’s first fully integrated commercial rare-earth processing facility in Saskatoon. Under the agreement, REalloys will fund upgrades to the facility and secure the majority of its production, including high-purity neodymium-praseodymium metals as well as dysprosium and terbium oxides used to manufacture high-temperature defense magnets.

Once processed in Canada, those materials will move to Ohio for metallization and alloying, creating one of the first fully allied rare-earth supply chains linking Canadian processing with U.S. manufacturing.

It’s no small feat. Even under ideal conditions, replicating heavy rare-earth metallization capability can take years.

“We’ve already solved the hardest part—proving that rare-earth metallization and alloying can be done domestically to the specifications real customers require,” Johnston said.

The company’s ambitions extend further downstream as well.

REalloys is also developing a large-scale permanent magnet manufacturing facility designed to produce 3,000 tons of NdFeB magnets annually in its first phase and eventually scale to roughly 18,000 tons per year. At full capacity, that output could supply magnets for 1.5 to 2 million electric vehicles annually, along with thousands of wind turbines, robotics systems and large volumes of industrial motors.

Defense applications remain among the most demanding uses for these materials, requiring magnets capable of operating under extreme temperatures and mechanical stress.

The strategic importance of rebuilding this capability has attracted attention well beyond the industrial sector. The company recently appointed retired U.S. Army four-star general Jack Keane, former Vice Chief of Staff of the Army, to its board.

Keane has long been one of Washington’s most prominent voices on defense readiness and supply chain resilience, and his involvement underscores the growing national-security significance of rebuilding the rare-earth materials pipeline inside North America.

#2 MP Materials (NYSE:MP): Rebuilding America’s Rare-Earth Mine

In California, MP Materials Corp is positioned right at the very beginning of America’s rare-earth supply chain.

The company operates the Mountain Pass Mine in California’s Mojave Desert - the only large-scale rare-earth mining operation currently active in the United States and the primary domestic source of rare-earth concentrate.

For decades, MP Materials and its predecessor companies have tried to restore rare-earth mining to the continental United States and reduce reliance on foreign supply chains that feed technologies ranging from electric vehicles and wind turbines to advanced defense systems.

The challenge has never been geology. Rare earth deposits exist around the world.

The problem is China’s dominance of the industrial system that processes those materials. China accounts for roughly 70% of global rare-earth extraction and about 90% of processing, giving Beijing enormous leverage over the supply chain.

That dominance has repeatedly destabilized the market. At times China has restricted exports of rare-earth materials, sending prices sharply higher. At other times it has flooded the market with exports, driving prices so low that Western producers struggle to survive—a cycle that previously forced the bankruptcy of Mountain Pass’s former owner, Molycorp.

Washington has now stepped in to change that dynamic.

In July 2025, the U.S. Department of Defense announced a series of measures aimed at accelerating domestic rare-earth production and reducing reliance on foreign supply chains. The plan included a $400 million investment in preferred stock in MP Materials, a 10-year offtake agreement guaranteeing purchases of neodymium-praseodymium (NdPr) oxide, and $150 million in financing to expand heavy-rare-earth separation capacity and build a large-scale magnet manufacturing facility.

MP Materials has already selected a site for that next phase. The company plans to construct its “10X” magnet manufacturing facility at a 120-acre site in Northlake, Texas, where it aims to eventually produce 10,000 metric tons of rare-earth magnets annually.

If successful, the project would move the company further downstream in the rare-earth value chain - from mining and processing toward full magnet manufacturing - an industry long dominated by China.

#3 Energy Fuels (NYSEAMERICAN: UUUU) — The Processing Support

In Utah, Energy Fuels controls one of the most strategically important pieces of industrial infrastructure in the American critical-minerals landscape: the White Mesa Mill.

Located near Blanding, the facility is the only operating conventional uranium mill in the United States and the only plant in the country capable of processing monazite concentrates into separated rare-earth oxides. After more than four decades of continuous operation, the mill represents something extremely rare in the Western rare-earth sector: fully permitted, operating processing infrastructure.

That capability places Energy Fuels at an important stage of the rare-earth supply chain in between MP Materials and REalloys. Energy Fuels operates the industrial step in between - separating rare-earth minerals into the individual oxides that downstream metallization facilities require.

The company is now moving to scale that role dramatically.

Energy Fuels plans to expand White Mesa’s rare-earth processing capacity from roughly 10,000 tonnes of monazite feed per year to as much as 60,000 tonnes annually, producing up to 6,000 tonnes of neodymium-praseodymium (NdPr) oxide along with hundreds of tonnes of dysprosium and terbium oxides.

Energy Fuels is also moving downstream in the supply chain, with plans to acquire Australian Strategic Materials in a transaction valued at roughly $299 million and geared toward vertical integration.

Energy Fuels CEO Mark Chalmers described the transaction as a major step toward building a fully integrated Western supply chain for rare-earth materials used in automotive, robotics, energy, and defense technologies.

By. Charles Kennedy

A New U.S. Facility Could Break China’s Grip on Critical Materials

REalloys (NASDAQ: ALOY) has announced a fully financed buildout of the largest heavy rare-earth metallization facility outside China, a project aimed squarely at one of the most fragile links in the Western defense supply chain just as Washington prepares to enforce its 2027 ban on Chinese-origin rare earth materials in U.S. weapons systems.

The timing coincides with rapidly growing concern about supply availability. Chinese and Western media reports indicate Washington may have only two months of critical rare-earth inventories available for defense manufacturing if supply disruptions deepen.

Shortages are already beginning to surface in industrial markets. Reuters reports that suppliers to U.S. aerospace and semiconductor companies have started turning away some customers as supplies of niche rare earth materials tighten.

Rare earth elements underpin key components of modern warfare, from missile guidance systems and drone propulsion to radar arrays and advanced fighter aircraft electronics.

“If China said we’re not going to give you rare earths, that means no F-35s, no missiles,” said Mike Crabtree, CEO of the Saskatchewan Research Council (SRC), in an interview with oilprice.com last month.

The reach of these materials extends far beyond the defense sector.

“Almost everything you can point to either has rare earths in it to make it work or was produced by something that had rare earths in it to be able to produce that article,” Crabtree said.

Yet the West spent decades allowing the most technically demanding parts of this supply chain to move offshore. Mining continued in various parts of the world, but the industrial stages that transform rare earth materials into usable metals and magnets steadily consolidated in China.

“In the last 10 to 15 years, the majority of the upstream and midstream supply chain for rare earth has been controlled by China,” Crabtree said.

That concentration now represents a strategic exposure for Western industry and defense planners alike. Beginning in 2027, U.S. procurement rules will prohibit defense systems from using magnets derived from Chinese rare earth supply chains, forcing manufacturers to secure alternative sources.

Rebuilding those capabilities is complicated and time-consuming.

REAlloys’ metallization operations in Euclid, Ohio represent one of the few facilities in North America already converting rare-earth oxides into metals and magnet-grade alloys.

The rare earth supply chain moves through several stages. Ore is mined and processed into concentrates, which are then separated into individual oxides such as neodymium and praseodymium.

But oxide powder is not what manufacturers use.

Before entering production, those oxides must be chemically reduced into rare earth metals and blended into specialized alloys that serve as feedstock for permanent magnets.

For decades, that metallurgical step—from oxide to metal—has taken place overwhelmingly inside China, even when the raw materials themselves were mined or separated elsewhere.

That gap has long represented the weakest point in the Western supply chain.

REAlloys (NASDAQ: ALOY) is seeking to close it, quickly.

At its Euclid facility, the company converts rare-earth oxides into finished metals and magnet alloys through high-temperature reduction and refining processes. These materials supply magnet manufacturers and advanced industrial customers.

“Metallization is the least developed part of the value chain outside China,” said REAlloys co-founder Tim Johnston. “It requires deep operating expertise and process control systems capable of managing complex variables in continuous production.”

Even under ideal conditions, replicating that capability takes years.

The project announced this week aims to accelerate that rebuilding effort.

In partnership with the Saskatchewan Research Council, REAlloys plans to construct the largest heavy rare-earth metallization facility outside China. The platform will integrate with the company’s existing operations and supply materials for the U.S. defense industrial base and Defense Logistics Agency stockpiles.

SRC’s processing facility in Saskatoon will produce key rare-earth materials, including neodymium-praseodymium alloys, along with dysprosium and terbium oxides. These elements enhance the strength and heat resistance of high-performance permanent magnets.

“What REAlloys will be buying from SRC will be both the bulk NdPr and the smaller but highly valuable quantities of dysprosium and terbium oxides,” Crabtree said.

Those materials will then move through REAlloys’ metallization and alloying processes before entering magnet manufacturing for use across defense systems, renewable energy equipment, robotics and advanced industrial machinery.

The company is also planning a large-scale NdFeB magnet manufacturing facility in the United States capable of producing roughly 3,000 tons annually in its initial phase and scaling to as much as 10,000 tons per year.

If it achieves that level of output, the facility could supply magnets for roughly 1.5 to 2 million electric vehicles each year, along with thousands of wind turbines and large volumes of industrial motors, robotics systems and medical equipment.

This potential shift in the rare-earth supply chain also has major implications for U.S. defense contractors. Companies such as General Dynamics (NYSE: GD), Honeywell (NASDAQ: HON), and L3Harris Technologies (NYSE: LHX) depend on a reliable domestic source of high-performance magnets for platforms ranging from Patriot missiles to advanced radar systems. By establishing a fully allied supply chain with REalloys and SRC, the defense industrial base could mitigate the risks posed by Chinese supply concentration and align production timelines with critical procurement schedules

By combining upstream resource partnerships, Canadian rare-earth processing and U.S. metallization and manufacturing, the REAlloys-SRC platform aims to establish a fully allied rare-earth supply chain.

If the buildout proceeds as planned, it will represent one of the largest non-Asian rare-earth magnet production hubs in the world.

And it will come online just as the United States begins enforcing new procurement rules designed to remove Chinese rare earth materials from the defense supply chain.

“Rare-earth projects outside China today often rely, directly or indirectly, on Chinese inputs, including process technology, investment capital, and the procurement of key equipment, systems, or consumables. Even many ‘non-Chinese’ producers remain exposed to China somewhere in their value chain, REalloys’ chief technical officer, Andy Sherman, told Oilprice.com in an interview.

“REalloys’ strategy is to remove this nexus entirely, because any reliance on China creates strategic vulnerability and leaves supply chains open to geopolitical influence. To be even 1% reliant on China is, in practical terms, to be 100% exposed.”

By. Josh Owens

.jpg)