It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Monday, April 27, 2026

Brazil left wing party asks court to halt rare earths miner’s sale

Serra Verde’s mine in Brazil. (Image: Serra Verde)

Left-wing Brazilian political party Rede Sustentabilidade asked the country’s Supreme Court to suspend the sale of mining company Serra Verde Group to USA Rare Earth Inc on national security grounds.

In a filing submitted on Friday, the party argued that Brazilian legislation doesn’t provide sufficient safeguards for the national interest as required by the Constitution in the exploitation of strategic mineral resources. The party said that no transaction should be carried out that could directly or indirectly transfer significant economic control over the country’s strategic mineral assets.

USA Rare Earth offered $2.8 billion in cash and stock for Serra Verde, which would mark one of the largest transactions in the rare earths industry to date.

Serra Verde’s Pela Ema operation in Goiás is being upgraded and currently produces about 100 metric tons of rare earth oxides per year. Output is expected to rise significantly, reaching around 6,400 tons annually by the end of next year.

Serra Verde’s press office declined to comment. USA Rare Earth didn’t immediately respond to a request for comment outside of normal business hours.

(By Daniel Carvalho)

Brazil rejects ‘TerraBras’ as US minerals deal stalls

Brazil’s government sees no need for a state-run critical minerals company. (Stock image)

Brazil sees no need to create a state-run critical minerals company, Industry Minister Marcio Elias Rosa said Friday, pushing back on proposals for a state-backed entity.

“There is no need whatsoever to create a state-owned company to carry out the exploration or processing of critical minerals,” Rosa told local broadcaster CanalGov, adding the current regulatory framework already offers incentives for the sector.

His comments come as a proposed national framework for critical minerals remains stalled in Congress and the Lula administration misses its own deadline to deliver a broader mining strategy.

The bill, led by federal deputy Arnaldo Jardim, includes a fund of up to 5 billion reais ($1 billion) to back mining projects, though officials have raised concerns about provisions that could expand state intervention.

Finance Minister Dario Durigan said the forthcoming framework will prioritize national sovereignty and domestic value creation without relying on broad tax breaks,. He argued strong global demand is already sufficient to attract investment while targeted tools like the Eco Invest programme will be used selectively to support projects.

“Brazilian critical minerals are too great for any potential political impediments to stand in the way,” Neil Harrington, senior vice president for the Americas at the US Chamber of Commerce, said at a São Paulo summit last month.

“It makes too much sense from a strategic, economic and investment perspective for both countries not to engage in this sector,” Harrington noted.

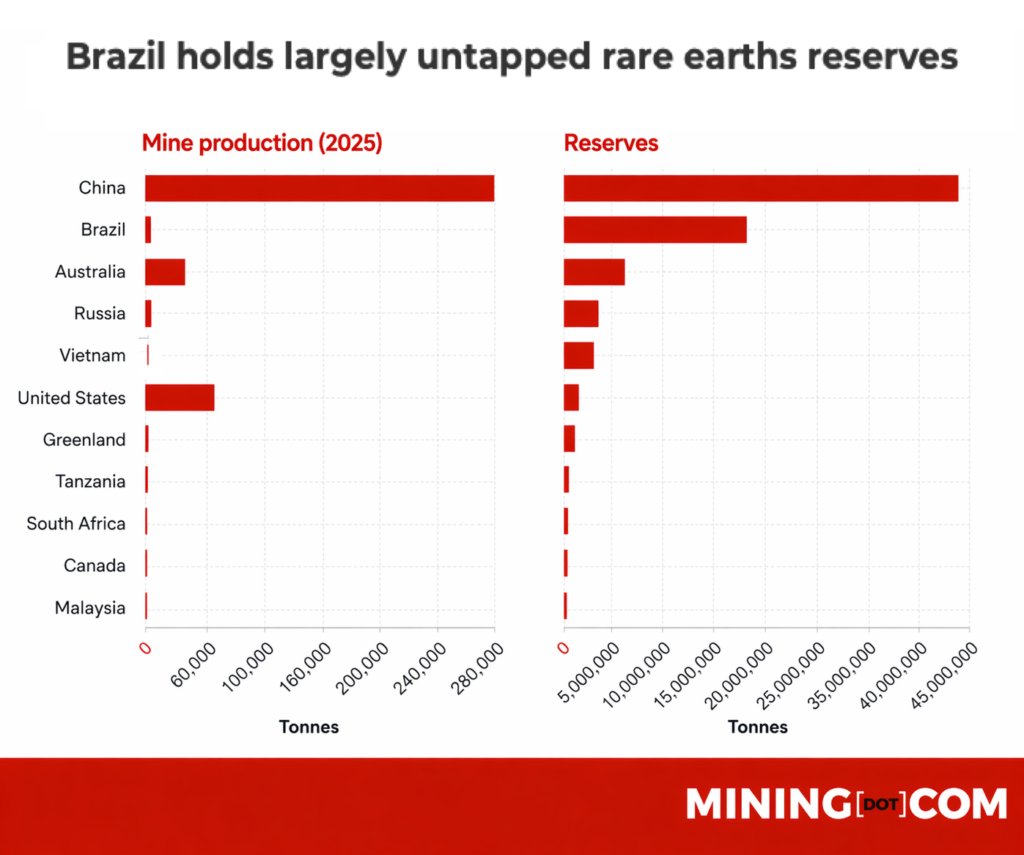

Brazil has the world’s second-largest rare earths reserves only behind China, but it produces less than 1% of global output. (Data source: USGS – metric tonnes.)

Policy uncertainty is not halting projects but is making capital allocation more selective, particularly for higher-risk downstream investments, as developers seek clearer signals on permitting, financing and the state’s role, Carlos Nogueira, senior advisor Brazil at consultancy Plusmining, told MINING.COM.

The absence of a clear policy is not stopping investment but is limiting how much capital Brazil could attract, while measures such as fast-tracked permitting could significantly accelerate project timelines, Adriano Drummond Trindade, a Brazilian mining lawyer, added.

Other analysts point to a broader policy vacuum that is highlighting rising friction between Brasilia and Washington, with missed diplomatic engagements, blocked visits and trade tensions complicating efforts to secure a bilateral minerals agreement ahead of Brazil’s October election.

State by state

Despite the lack of a federal deal, the US is deepening engagement at the regional level. Goiás is advancing a memorandum of understanding with US partners to expand research, investment and processing tied to the Serra Verde rare earths operation.

The deal could potentially create one of the few Western producers of heavy rare earths outside China. It includes a 15-year supply arrangement with minimum pricing, marking a shift from previous exports to China.

Pela Ema rare earth mine in Brazil. (Image courtesy of Serra Verde.)

Rafaela Guedes of the Brazilian Centre for International Relations said the transaction strengthens Brazil’s role in diversifying supply but warned it falls short of building an industrial base.

“Without clear policies for adding value, building technology, and aligning mining with industry, Brazil may end up negotiating assets one by one instead of from a national strategy,” she said.

Other companies, including Aclara Resources (TSX: ARA) and Meteoric Resources, have also secured US-backed financing for early-stage projects.

Strategic market

Brazil’s vast rare earth reserves make it a strategic prize as Beijing tightens export controls. President Luiz Inácio Lula da Silva has pushed for domestic processing and diversified partnerships, including recent agreements with India, while resisting pressure to simply export raw materials.

Domestic processing is increasingly driven by project economics rather than policy alone, particularly in rare earths and lithium where pre-processing is often necessary, though it raises capital costs and execution risks for investors, Nogueira said.

Building a competitive rare earths value chain will likely require partnerships with the US to access advanced processing technology and innovation, as Brazil faces steep technical barriers to matching China’s capabilities, Juan Ignacio Guzman, head of GEM consulting said.

Incentives rather than export restrictions are the more effective path to building domestic processing, while proposals such as export taxes or state intervention risk undermining competitiveness, Trindade said. He added that current geopolitics could favour Brazil as a neutral investment destination if policy clarity improves.

Debate over a potential state-backed entity, often dubbed “TerraBras” (Terra= land or earth in Portuguese and Bras= shorthand for Brazil), has added to regulatory uncertainty, even as authorities insist no such plan is under consideration. Instead, officials say the focus remains on attracting private investment and expanding refining capacity.

Geopolitical competition is likely to steer Brazil toward a flexible framework that avoids choosing between the US and China, preserving access to Chinese processing while encouraging Western investment and technology partnerships, Nogueira said.

Advisory firm Speyside Group points to Brazil’s combination of mineral diversity and relatively clean energy as a competitive advantage, but warns that fragmented policy, weak implementation and misalignment with global ESG standards could delay projects and raise costs.

With 13 bills related to critical minerals under review, according to the National Mining Agency (ANM), analysts say legislative gridlock is already weighing on investment decisions and delaying partnerships. Without a unified strategy, experts say Brazil risks missing a window to align foreign interest with its industrial ambitions as demand for critical minerals accelerates.

Latin America is heading into 2026 with resources at the centre of a growing global power struggle, as governments and investors focus on who controls critical minerals and the supply chains behind them. If the region matters to you, don’t miss MINING.COM’s series tracking the geopolitical forces reshaping it and why markets are increasingly driven by global alliances as much as local politics.

Serra Verde’s Pela Ema mine in Brazil. Credit: Serra Verde

Brazil’s Serra Verde Group — the target of a $2.8 billion acquisition by USA Rare Earth Inc. — expects about one-third of its future production to come from heavy rare earth elements, a category currently dominated by China.

The company’s Pela Ema operation in Goiás is being upgraded and now produces roughly 100 metric tons of rare earth oxides each year, according to chief operating officer Ricardo Grossi. Production is expected to increase significantly, reaching about 6,400 tons annually by the end of next year.

A recent wave of deals underscores a global push to build rare earth capacity after China last year threatened widespread industrial shutdowns by restricting exports. Earlier this month, USA Rare Earth agreed to acquire Serra Verde in one of the largest deals in the industry.

Heavy rare earths are less abundant and more valuable than lighter ones. That’s prompting companies to expand production outside China, including in the US and South America.

For the expected output from Pela Ema, about 32% will be terbium and dysprosium — less common elements that are essential for high-performance magnets. The rest will include neodymium-praseodymium — at 22% — and yttrium — 42%, according to Grossi.

Serra Verde has signed a 15-year supply agreement with a US-backed partner. The deal sets minimum prices of $2,050 per kilogram for terbium and $575 per kilogram for dysprosium. Grossi said the materials will be sold only to Western markets.

The company is also considering carrying out part of the processing — known as oxide separation — in Brazil, with a final investment decision expected by early 2027.

“We’ve developed a pricing model that isn’t tied to highly volatile Asian benchmarks, which enhances revenue visibility” Grossi said, adding that the structure could help unlock other projects in Brazil.

(By Mariana Durao)

Leftist candidate in copper giant Peru wants new mining rules

A leftist presidential candidate on the verge of reaching Peru’s runoff election is pledging to overhaul mining rules in one of the world’s leading copper-exporting countries.

Vowing to redistribute wealth to Peru’s rural communities, Roberto Sánchez, 57, plans to review tax contracts with major mining companies, redraft the country’s market-friendly constitution and hike taxes to levy windfall profits at a time of buoyant metals prices. He also wants to phase out open-pit mining — the way virtually all of Peru’s big mines operate — blaming the practice for harming the environment.

“We don’t want to expropriate a single dollar or an inch of land from anyone, we want to broaden the benefits by democratizing access to wealth,” Sánchez said in an interview. “Neocolonial Peru is over.”

Sánchez currently holds a razor-thin margin of only around 17,000 votes over right-wing populist Rafael López Aliaga for the chance to take on conservative Keiko Fujimori in a June 7 runoff. An electoral court is reviewing tally sheets that represent as many as a million votes. Whoever wins will become Peru’s 10th president in a tumultuous era and will not have a congressional majority, which could hinder any efforts to revamp existing policies.

The Andean country is the world’s third-largest copper producer and a key supplier of gold, silver and zinc, with mining accounting for 60% of its exports. It is a significant base of operations for global mining companies including Glencore Plc, Anglo American Plc, Freeport McMoRan Inc. and MMG Ltd.

Sánchez also said he wants to review free trade agreements and a host of contracts involving the Camisea natural gas fields which supply a major liquefaction terminal, known as Peru LNG, on the Pacific coast. Major players in Camisea include Pluspetrol SA and Shell.

“Standards must be set in a way that benefits the people,” Sánchez said in the interview at his party headquarters in the capital Lima. He declined to say who are serving as his top economic advisers.

Tapping international reserves

Sánchez has been critical of Peru’s veteran central bank chief Julio Velarde, considered the steady hand that has largely insulated the resource-based economy from the country’s chronic political turmoil.

He declined to say whether he’d nominate Velarde for a fifth term, stressing he would meet with him with the caveat that “no one is indispensable.”

But in a sign of pragmatism, he stressed the importance of preserving the institution’s autonomy and the country’s macroeconomic stability.

Sánchez added he is considering using Peru’s almost $100 billion in international reserves — which are vast by any measure, at about a third of gross domestic product – to fund spending on health, infrastructure and education.

“We need a strong fiscal chest for the major transformations we want to carry out,” he said.

Sánchez said the country’s needs would prevent him from prioritizing a controversial plan to buy new fighter jets, a decision that current Interim President José María Balcázar has said will fall onto the next administration.

A signing ceremony for an up to $3.5 deal with Lockheed Martin Corp. was abruptly postponed last week, drawing US backlash. In the wake of the controversy on Wednesday, Peru’s defense and foreign ministers resigned.

Currently a lawmaker, Sánchez served as foreign trade minister under the administration of ousted former President Pedro Castillo, while Fujimori will face her fourth consecutive runoff vote, having lost the last three.

Overall, Sánchez’s platform mimics the key promises that swept Castillo into the presidency in 2021, spooking investors at the time while drawing support in Peru’s impoverished Andean regions. Castillo was eventually ousted and arrested in late 2022 after attempting to shut down congress and the judiciary.

Sánchez has campaigned as Castillo’s heir, donning the same traditional hat from Peru’s Cajamarca region and promising to pardon him on Day 1 of a future administration.

Since Peru’s April 12 election, the country’s sol currency has been the worst performer in Latin America, with analysts pointing to Sánchez’s unexpected rise as the key factor. Government bonds handed investors less than 0.3% return, underperforming most emerging-market sovereign peers.

Still, if elected, Sánchez’s ambitious reforms are bound to hit roadblocks, including a new bicameral congress where left-wing forces will be outnumbered by conservative ones. To redraft Peru’s constitution, for example, Sánchez is proposing to repeal a law that prohibits convening a constituent assembly through a referendum. But to do that he would need conservative support in congress.

Similarly, while Castillo offered big reforms during his presidential campaign, once in office he failed to deliver them, a fate that could also beset a Sánchez presidency.

The leader of the Juntos por el Perú party is now in second place in the official vote count with just over 94% of votes tallied. But with as many as one million challenged ballots, Sánchez’s spot in the second round still isn’t secured. Electoral authorities say final results may take until mid-May.

The first round got off to a rough start when ballots arrived late to some polling stations mainly around Lima, which prompted authorities to allow some voters to cast ballots the next day.

López Aliaga, who has the most support in Lima, seized on the logistical problems to allege fraud. Sánchez has said he will respect the final results.

Since election day, López Aliaga has called for a redo of the entire election, later softening his demands to propose adding more voting days to accommodate the large share of Lima voters who were impacted by the logistical snags.

Sánchez said the delays had not tainted the election and criticized the resignation of electoral agency head Piero Corvetto amid the controversy. The candidate claimed the pressure that led to Corvetto’s departure was part of an alleged right-wing plot to “take control of the country’s institutions.”

“This is a serious damage because they intend to boycott and disregard the will of the people,” he said.

BV Calls for Greater Connectivity Across Value Chains

Bureau Veritas Marine & Offshore (BV), a world leader in testing, inspection, and certification (TIC), declared its vision for the future of maritime trade during Singapore Maritime Week, with Executive Vice-President, Industrials & Commodities, Matthieu de Tugny delivering a keynote address detailing how digitalization, artificial intelligence, and the energy transition are fundamentally reshaping shipping and the global value chains it underpins.

During the keynote address, de Tugny outlined that the industry’s trajectory will be shaped by three intersecting forces: decarbonization, digitalization, and industry resilience. He stressed that the sector is moving beyond fragmented, vessel-level optimization towards more sophisticated inter-connected intelligence across the entire value chain, a shift that demands multi-sector collaboration.

Regarding artificial intelligence, de Tugny highlighted that AI is already generating tangible results across vessel operations, engineering, ports, and supply chains. The integration of sophisticated smart systems is supporting voyage optimization, predictive maintenance, digital twins, routing efficiency, and smarter logistics, delivering real-world gains today.

However, de Tugny also cautioned that AI’s potential can only be realized when underpinned by reliable, structured, and trusted data. Critically, he emphasized that human expertise remains central to the industry’s future, with AI serving to augment decision-making rather than replace the professionals who drive it.

De Tugny also highlighted BV’s capabilities in this area, having developed a suite of advanced solutions designed to help clients as they navigate this transformation:

- Digital Class: Integrates design, construction, and operational data to enable continuous, real-time assurance in place of periodic inspections, giving operators and owners a live view of vessel condition and compliance.

- Augmented Surveyor 3D: Combines drone-based inspections, AI-supported defect detection, and digital 3D asset models to improve the speed, accuracy, and safety of survey operations.

- SmartShip Framework: Supports clients along a progressive journey from connected vessels to autonomous functions and fully integrated maritime ecosystems, managing both the technical and regulatory dimensions of the transition.

De Tugny also addressed the global energy transition, calling for ambitious long-term planning alongside pragmatic near-term action. While next-generation fuels – including LNG, methanol, and ammonia – alongside new infrastructure and financing models are essential to achieving net-zero targets, de Tugny emphasized that existing fleets can already reduce their emissions footprint today through digital optimization, energy-saving technologies, and improved operational performance.

SINAY Boosts Maritime Intelligence Platform with MariTrace Acquisition

(L-R) Yanis Souami, CEO & Founder of SINAY; Thomas Owen, CEO & Founder of MariTrace; David Lelouvier, COO & Managing Director at SINAY; and Simon Rathbone, Director of Software Development at MariTrace

Maritime intelligence specialist SINAY has acquired UK-based vessel tracking platform MariTrace, strengthening the French company's position as an integrated provider of security, operational and environmental intelligence.

The move builds on earlier acquisitions of marine weather analytics provider OpenOcean in 2022 and container tracking service Safecube in 2024, and represents another step towards combining vessel, cargo and environmental data into a single source of operational intelligence for maritime stakeholders.

CRITICAL INTELLIGENCE PLATFORM Amid strong market demand for reliable data, MariTrace provides real-time intelligence across maritime security, risk assessment, trade analytics and vessel tracking, with particular strength in the world's highest-risk maritime corridors, including the Strait of Hormuz, the Gulf of Aden and the Red Sea. The platform is used by 100-plus customers across insurance, security, ship-owning, offshore contracting and commodities, and operates in 24 countries worldwide.

SINAY CEO and founder Yanis Souami said: "This acquisition fully aligns with our mission to become the leading full end-to-end supply-chain visibility platform in the maritime industry. By bringing together vessel tracking, cargo visibility and environmental intelligence, we are giving customers the tools they need to make better-informed operational and commercial decisions in an increasingly complex risk environment."

STRATEGIC SYNERGIES Safecube already enables SMBs to track their containers with ease, centralising shipment data and delivering automated alerts for ETAs and key events. Integrating MariTrace's vessel tracking with Safecube's container-level visibility gives customers a unified view that links cargo to its carrier, enriched with risk intelligence and more accurate ETA predictions.

At the same time, SINAY's expertise in environmental monitoring – including CO2 emission calculators and underwater noise assessment tools – provides an additional environmental compliance layer for MariTrace's customer base of vessel owners, offshore contractors and insurers, alongside existing security and risk data.

MariTrace CEO and Co-founder Thomas Owen said: "Joining SINAY allows us to expand our offering by combining our risk and tracking capabilities with a broader set of data and analytics. Together, we can deliver deeper insight into both operational risk and performance."

Founded in 2008, SINAY has grown into an international provider of maritime data intelligence, with 130 employees, EUR 10m in annual revenue and EUR 12m raised from international investors.

The products and services herein described in this press release are not endorsed by The Maritime Executive.

Winning Formula

For residents living near ports, seafarers working aboard ships and passengers stepping ashore, the question is no longer abstract: Why am I still breathing this?

(Article originally published in Jan/Feb 2026 edition.)

Sulphur oxides (SOx), nitrogen oxides (NOx) and particulate matter (PM) from ship exhausts are a daily reality in many port cities. A 2023 World Bank report estimated that more than 250 million people globally are exposed to air pollution around ports, underscoring that maritime emissions are not only a climate issue but a public-health issue.

Regulators are increasingly shifting the conversation beyond what comes out of the funnel to *well-to-wake emissions* — the full carbon and pollution footprint of a fuel – from how it's produced and transported to how it's ultimately consumed onboard.

Beginning in 2030, the E.U.'s FuelEU Maritime regulation will require container and passenger vessels to connect to onshore power supply when docked or demonstrate equivalent well-to-wake emissions reductions through alternatives such as biofuels, fuel cells and e-fuels. What matters now is not which fuel wins in 2050 but what can be deployed today without disrupting operations.

As regulators push shipowners to account for emissions beyond the exhaust stack, including upstream fuel production and transport often captured under so-called Scope 3 emissions, attention is shifting toward systems that make those fuels usable at sea.

That lens puts the spotlight on companies like Auramarine, a Finnish specialist in alternative-fuel readiness for marine fuel supply systems, and PowerCell, a Swedish hydrogen fuel cell developer bringing megawatt-scale electric power into commercial maritime operations.

Auramarine: A Layered Approach

Auramarine frames today's reality through a pragmatic split between newbuilds and retrofits.

In newbuilds, momentum is shifting. "The focus, especially in newbuilds, is increasingly methanol-fueled dual-fuel vessels," the company says, pointing to an orderbook that already runs into the hundreds of methanol-capable ships expected over the next few years.

Retrofits are being shaped by safety rules, downtime and economics. Auramarine says the near-term focus is on fuels that are directly compliant with SOLAS Chapter II-2 without requiring alternative design approvals. In Auramarine's internal terminology, "biofuels" refers specifically to liquid, non-toxic, non-volatile fuels with a flashpoint above 60 degrees Celsius, including hydrotreated vegetable oil (HVO) and fatty acid methyl ester (FAME). These can often be drop-in replacements (i.e., usable in existing engines and fuel systems with little or no modification).

"These SOLAS II-2 compliant fuels provide an opportunity to meet carbon reduction targets with minimal capital expenditure," Auramarine explains. It adds that "especially the biofuels covered by ISO 8217:2024 offer a rare combination of safety, immediate emissions reduction and near zero capital expenditure," making them one of the most practical tools for short- to mid-term decarbonization.

Beyond higher-flashpoint biofuels, Auramarine says operators are evaluating low-flashpoint and gas-fueled dual-fuel pathways such as methanol, ethanol, liquefied biogas (LBG) and ammonia, particularly for newbuilds and younger vessels.

For smaller fleets, "emissions pooling" (meeting emissions targets collectively rather than ship by ship) can also play a role, helping manage exposure to the Carbon Intensity Indicator (CII) framework and the E.U. Emissions Trading System (EU ETS) while technical upgrades are phased in.

The result, Auramarine says, is a layered approach: near-term efficiency improvements, mid-term system upgrades and longer-term alternative-fuel strategies with the fuel supply system increasingly treated as a critical enabler of that multi-step transition.

From a fuel-supply perspective, the easiest retrofit pathways are those that avoid structural change. "Higher-flashpoint, drop-in biofuels fit this best," Auramarine says, because they typically require minimal tank, piping or safety-system modifications, delivering meaningful carbon reductions with low capital expenditure and minimal downtime.

Vessel age heavily influences practicability: Older ships tend to stick with low-capital blends, mid-life vessels can justify moderate upgrades and younger ships and newbuilds typically support the economics of full dual-fuel installations aimed at long-term transition readiness.

Automation and monitoring are becoming central to this equation, and owners are getting more disciplined about what they measure.

Auramarine says decisions often hinge on fuel-consumption stability, system reliability and uptime, maintenance impact and component lifetime, automation and reporting quality and operational flexibility when switching fuels or modes: "The most successful solutions are those that deliver measurable emissions benefits without introducing operational risk and that support a transparent, data-driven compliance pathway."

Where is adoption moving fastest?

Auramarine points to segments where regulatory exposure, commercial pressure and predictable operations align. Short-sea, feeder and regional vessels with frequent calls in European waters are often early adopters. Tanker, ro-ro and ro-pax fleets with regular schedules and centralized fleet management are also moving quickly.

In the newbuild space, container feeders and chemical and product tankers show strong momentum for methanol dual-fuel solutions.

PowerCell: Past the Pilot Stage

PowerCell approaches the problem from the conversion side: turning clean fuels into electricity onboard. It argues that while deep-sea tonnage dominates emissions, a large near-term opportunity exists in smaller vessels.

"While large ocean-going ships make up approximately 85 percent of the industry's carbon footprint," the company explains, "the other 15 percent of smaller shortsea vessels, representing approximately 150 million tons of annual carbon emissions, can almost all realistically be decarbonized via fuel cells right now."

Fuel cells have historically been strongest in short-sea, fixed-route operations like passenger ferries and in shoreside "cold ironing" (powering berthed ships from shore) solutions where grid connections are limited.

PowerCell says that picture has broadened: "Hydrogen and methanol marine fuel cell systems matured significantly in 2025" with commercial orders now spanning ro-pax vessels, bulk carriers, superyachts and cruise ships. Megawatt-scale orders indicate growing confidence in longer, more varied duty cycles.

A milestone was PowerCell's first commercial sale of its integrated methanol-to-power system, valued at approximately $17 million and including a 2 MW installation (enough to power approximately 2,000 homes).

For cruise operators, the company sees a clear target: auxiliary engines and generators that power hotel loads. Fuel cells can eliminate SOx, NOx, and PM at the point of use and reduce greenhouse gas emissions when powered by green fuels. Proton-exchange membrane (PEM) fuel cells also offer a practical onboard advantage: low vibration and noise.

Methanol reforming enables onboard conversion of methanol to hydrogen, providing a practical pathway to hydrogen-electric systems without waiting for dedicated hydrogen bunkering infrastructure to mature.

PowerCell adds that methanol can be used about 30 percent more efficiently in fuel cells than in internal combustion engines and that PEM systems deliver high power density in a compact footprint. It argues that reformer technology can also make fuel cells more fuel-agnostic over time and that developing ammonia reformers is technologically feasible, offering a pathway toward a zero-carbon solution if fuel production scales.

Demonstration projects remain essential for an industry built around reliability.

"The most important learning comes from operational data over time," PowerCell says, including reliability, uptime, degradation rates, maintenance needs and performance under variable loads and conditions. It says this kind of transparency is what de-risks adoption and builds confidence among shipowners, yards, class societies and regulators.

One Ship at a Time

Fuel availability, for now, sets the outer boundary.

PowerCell expects renewable methanol and other green fuels to remain scarce in the near term. Auramarine faces the same operational challenge: more complex fuels require careful design, system integration, crew training and real-world operating experience.

Progress is incremental by necessity, but each vessel that clears those hurdles lowers the barrier for the next.

The opinions expressed herein are the author's and not necessarily those of The Maritime Executive.

Report: The Race is On to Bring Unmanned Combatants to Life

The JARI "Orca" unmanned combatant vessel (via Chinese social media)

American defense tech consultancy Janus has just published a major review of autonomous naval systems in all global markets. After Ukraine's success with USVs in the Black Sea, interest in unmanned naval warfare is taking off - notably in the United States, with real backing from the U.S. Navy. But America is not alone in seeking an unmanned edge: China is moving towards development of "larger, more capable unmanned surface vessels" with long endurance and heavier payloads - "beyond anything the United States currently has deployed," the consultancy warns.

Janus points to the unveiling of CSSC's JARI-USV-A, or Orca, the world's largest (acknowledged) unmanned surface combatant. The trimaran vessel was revealed to the public at the Zhuhai Airshow in November 2024, and at a displacement of about 300-500 tonnes, it is about three times larger than the U.S. Navy's nearest equivalent, the Sea Hunter. The Orca is outfitted with VLS cells, torpedo tubes, an AESA radar, and a helideck for multipurpose operations. As a shallow-draft trimaran, it would be suitable for littoral operations in the Taiwan Strait, Janus says.

Looking ahead, China's abundant shipyard capacity positions it not just as a leader in modern warship and merchant ship production, but also as a tough competitor in scaled-up unmanned systems. "Chinese commercial shipyards produce more tonnage annually than the rest of the world combined. The structural advantage in production capacity that underlies every U.S. concern about naval competition does not disappear because the vessels are unmanned. It is, if anything, more relevant when the goal is to build dozens or hundreds of vessels rather than a handful of exquisite ones," Janus warns.

In the U.S., the unmanned-vessel space is crowded with competitors - a good thing for choice, but it is likely to lead to future consolidation, according to Janus. The big names in the startup world - Saronic, Anduril, Blue Water Robotics and others - are being joined by countless smaller companies, and by the defense primes as well. "The Navy will have a sustained number of orders once programs of record materialize, but not at the kind of scale that will keep a dozen companies in business simultaneously," predicts Janus.

The consultancy expects the Navy to begin moving swiftly into production orders under the newly-restructured MUSV "marketplace" concept (formerly MASC). The Navy now wants production-ready products, not development programs, and reliability at sea will be a primary focus, Janus says. This year should be one to watch for the future of the industry. "The structure of the award — how many companies receive contracts, whether it includes one or multiple hull variants, and how the OTA pathway shapes ongoing development will determine the industry landscape for years," the firm says.

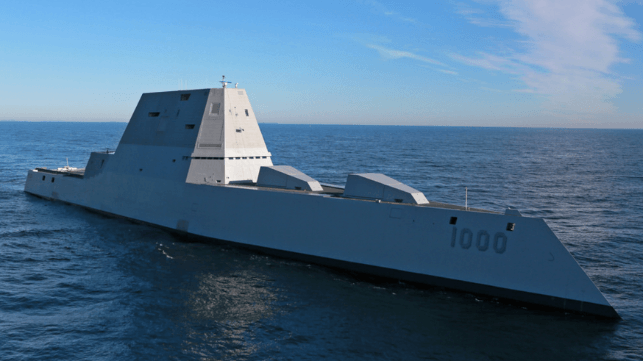

Report: Three Injured in Fire Aboard USS Zumwalt

USS Zumwalt on her initial sea trials (USN file image)

A fire aboard the first-in-class destroyer USS Zumwalt has injured three sailors, according to the U.S. Navy.

Zumwalt is currently at shipyard in Pascagoula, Mississippi to undergo modifications needed to launch the service's next-generation hypersonic missile. Launch tubes and equipment have replaced both of the Zumwalt's iconic deck guns, which were designed to deliver high velocity, high tech shore bombardment from a stealthy platform.

According to USNI and Naval Surface Forces, a fire was reported aboard Zumwalt at about 2145 hours on April 19. The crew managed to put it out, but three sailors were injured; two were treated at the scene, and the third was taken to the hospital. All are in stable condition.

An investigation into the circumstances of the blaze and the extent of the damage is under way.

The U.S. Navy's futuristic Zumwalt-class destroyers have had an uneven history in service, and have deployed only rarely. Their unique deck guns have never been used: After the number of vessels in the class was cut back from 32 to three due to budget concerns, the manufacturing cost per round for their special ammunition rose to an impractical $800,000-$1 million per shot. The production run of ammunition was canceled, and the guns are functionally unusable.

Aboard USS Zumwalt, the deck guns have now been replaced with four launch tubes for the Conventional Prompt Strike hypersonic missile system, each built to carry an all-up round pack with three missiles. This high-powered arsenal adds to Zumwalt's 80 existing VLS cells. The modification will cost up to $2 billion to complete for all three vessels in the series.

Serra Verde’s mine in Brazil. (Image: Serra Verde)

Serra Verde’s mine in Brazil. (Image: Serra Verde)