China’s Subsidy Machine Is Reshaping Global Capitalism

ALL CAPITALI$M IS STATE CAPITALI$M

- Governments are pouring record amounts into strategic industries, with global subsidies reaching $108 billion as countries try to secure supply chains.

- China is outspending the West by a wide margin, providing firms with 3–8 times more state support than OECD peers and helping Chinese companies dominate sectors such as semiconductors and solar panels.

- The result is a growing global subsidy race, as Western countries respond with tariffs and incentives while debating whether free-market capitalism can compete against China's state-backed industrial strategy.

The COVID-19 pandemic and the geopolitical conflicts to follow exposed severe weaknesses in global supply networks, prompting governments, caught off guard and complacent, to pour money into critical sectors like semiconductors, critical minerals, and pharmaceuticals to prevent future shortages and reduce dependence on geopolitical rivals. Consequently, governments across the globe have increasingly been doling out state subsidies to local firms in a bid to secure supply chains, accelerate the transition to green energy, and protect domestic manufacturing against aggressive foreign competitors. A landmark report by the Organisation for Economic Co-operation and Development (OECD) has revealed that global state subsidies have surged to a total of $108 billion, good for an average of 1.3% of company revenues across 15 key industrial sectors and the highest level since the 2008-2009 financial crisis. But China takes this game far more seriously, giving the state natural resource power the West only dreams of, and making this the onset of what could be a subsidy race that changes the rules of capitalism in order to compete with Beijing.

According to the OECD, Chinese firms in strategic sectors received between three and eight times more state support than competitors in OECD countries over the past 20 years, giving Chinese firms a huge leg up in highly competitive markets. Indeed, OECD estimates that this massive government aid--spanning direct grants and below-market loans-- drove roughly 60% of Chinese companies' global market share gains over the past two decades. Chinese companies receive subsidies equivalent to roughly 2.5% of their revenue, compared to just 0.3% seen by firms in peer nations like Japan and South Korea.

The disparity is most extreme in the semiconductor and solar panel industries, with China's booming semiconductor sector receiving government subsidies equivalent to ~10% of revenues in recent years, compared to 2% of revenues for the global semiconductor sector. China's state-backed investment vehicles, including "Big Fund III" established in 2024, are channeling roughly $47.5 billion into advanced logic and memory capacity. And, Beijing’s largesse is driving massive growth here: China's integrated circuit (IC) exports surged by 83.7% year-over-year to $103.5 billion in the first four months of 2026, reflecting a massive expansion in domestic chip manufacturing capabilities driven by billions in state-backed investments and soaring domestic demand.

Chinese memory firms are now challenging global industry leaders: Domestic players like Yangtze Memory Technologies Corp (YMTC) and ChangXin Memory Technologies (CXMT) are rapidly taking market share and preparing for major public listings to fund further expansion, with YMTC poised to become the world's third-largest NAND flash producer after South Korea’s Samsung (OTCPK:SSNLF) and SK Hynix. Despite global trade restrictions, Chinese firms are achieving important breakthroughs: Chinese engineers have reportedly developed working prototypes of advanced EUV lithography machines, a critical step toward complete manufacturing self-sufficiency by 2028-2030. Additionally, companies like Huawei are pioneering new "logic folding" architectures to boost performance without relying on traditional miniaturization methods.

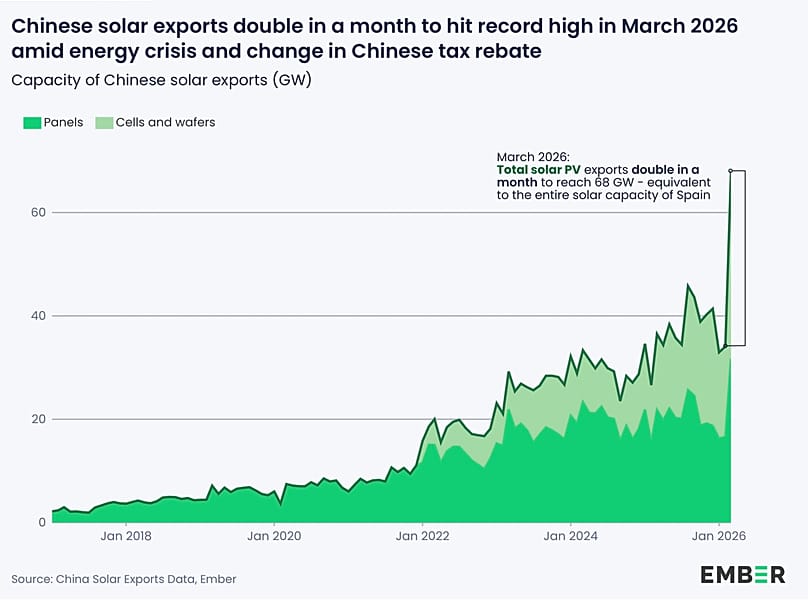

China’s solar panel manufacturing continues to receive heavy state funding, helping it to dominate the global market regardless of short-term market conditions.

State-backed Chinese subsidies averaged nearly 3.2% of annual firm revenues, enabling manufacturers to heavily outinvest competitors and secure over 80% control of the entire photovoltaic supply chain.

This generosity has incentivized Chinese producers to expand manufacturing under any market conditions. China's annual solar manufacturing capacity has reached approximately 1,200 GW, nearly double the total global installation demand. According to the OECD, this aggressive support has resulted in subsidy-fueled overcapacity and driven the average selling price of solar panels down by 90% over the last decade and a half, often forcing panels to be sold below the break-even point.

But while it may give states more power to wield, the OECD warns that these ongoing, large-scale subsidies are fueling global industrial overcapacity, artificially depressing international prices and undercutting firms that are actually better and more innovative.

And overly generous government subsidies have backfired on Chinese companies before. Whereas the overcapacity and subsequent price cuts have made solar energy highly affordable globally and driven historic deployment records in emerging markets (such as a 176% jump in Chinese module exports to Africa), it has also resulted in severe financial distress, declining profitability and heavy domestic consolidation for Chinese solar companies. To address those problems and maintain some balance, Beijing has begun to phase out support. For instance, the Chinese government reduced and fully abolished the 9% Value Added Tax (VAT) export rebate on photovoltaic products, while battery energy storage systems saw their export tax rebates reduced from 9% to 6%, with a full phase-out expected by 2027.

Meanwhile, Western nations and trading blocs are increasingly trying to come up with ways to keep China’s clean energy hegemony in check with its own incentives. But more often, with retaliation. Most recently, the U.S. unveiled significant levies across China’s renewable sector products, including 50% tariffs on solar cells (whether or not assembled into modules) and strict actions against Chinese steel, aluminum, and advanced batteries. The Trump administration has also announced a 100% punitive tariff on Chinese EVs, making entry into the American market prohibitive. Additionally, the European Commission has adopted definitive countervailing duties of up to 35.3% on BEVs from China, valid for five years. These are applied on top of the standard 10% vehicle import duty.

The uncomfortable reality is that Western economies assumed for decades that private capital, comparative advantage, and open markets would determine the industrial winner. However, China has spent that time building national champions with patient state capital, cheap financing, protected domestic markets, and long-term strategic planning. Tariffs can slow the flow of Chinese products across borders, but little else. The West’s biggest economies now face the choice of whether to try to compete with China on similar terms or whether there is still faith in a private market free-for-all to operate in the national interest.

By Alex Kimani for Oilprice.com

New Geometry Of Innovation: China’s Path From Peripheral Outpost To The Technological Core Of Global Change – Analysis

By Paweł Gałecki

The global economic architecture is undergoing one of the most significant transformations since the Industrial Revolution, and its epicenter is shifting from Western decision-making centers toward dynamic Asian ecosystems. China, which for the past four decades has been perceived in the economic consciousness primarily as the “world’s factory” – a place of cheap production, mass export, and global supply of components – is steadily evolving toward a model based on knowledge, research and development, and co-creation of technology. This fundamental metamorphosis is not merely a consequence of a natural economic cycle, but the result of a deliberate, long-term state strategy, supported by growing confidence from international corporations, academic institutions, and geopolitical partners from different continents. Statements by leaders of global technology corporations, strategists, and research experts clearly indicate that the narrative of China as merely an assembly site has been consigned to history. It has been replaced by a reality in which Beijing, Shanghai, Suzhou, and Shenzhen are becoming laboratories of the future, where solutions are born and then exported to the markets of Europe, North America, Africa, and the Middle East. This shift carries consequences for business models, supply chain architecture, regulatory standards, and long-term competitiveness strategies.

China as a Global Innovation Hub: Philips and Bosch Redefine the Future of Technology and Industry

Royal Philips, a Dutch conglomerate with more than a century of presence on the Chinese market, is an excellent example of strategic evolution. The company’s CEO, Roy Jakobs, recently stated unequivocally that China has transformed from a key market into one of the global centers of innovation. This assertion is not a marketing claim but a reflection of a deeply rooted operational strategy, whose pillar is the slogan “In China, for China, for the world.” Philips has built a comprehensive value chain in the Middle Kingdom: from advanced research and development, through production, commercial operations, sales and services, to strategic partnerships within the local healthcare ecosystem. Last year the group announced the establishment of the China Research and Innovation Headquarters in Beijing, which acts as a coordinator for regional R&D centers and an accelerator for localizing medical solutions. At the same time, the Suzhou facility integrates R&D functions, manufacturing, and global export, while Shenyang specializes in the development of computed tomography, serving as a global innovation center in this field. Such geographic and functional distribution of competencies demonstrates that China has ceased to be a peripheral outpost and has become a technological core generating value for more than a hundred countries where Philips provides its services.

Jakobs emphasized that the vast Chinese market and rapidly developing digital infrastructure create unique conditions for scaling innovations, which is crucial for the medical technology sector, where deployment time and accessibility of solutions can determine patients’ lives. The Chinese healthcare sector is currently undergoing a qualitative transformation: from models based on scale and reactive disease treatment toward proactive health management, therapy personalization, and continuous diagnostics. Artificial intelligence acts as a catalyst in this metamorphosis, enabling the processing of large medical datasets, optimization of hospital processes, and the development of telemedicine. By combining the global capabilities of corporations with China’s speed of adaptation and solution scalability, Philips intends to deepen cooperation in digital health, AI-based solutions, medical imaging, and green healthcare. Deep rooting in the local ecosystem, strengthened by investments in building capacity for medical personnel and alignment with China’s policy frameworks for sustainable development, becomes a strategic choice that allows the company to remain resilient and to influence both locally and globally.

A parallel but equally significant transformation is observed in the automotive sector, where Robert Bosch GmbH sees in China not only the largest and most dynamic market in the world, but above all a key source of technological innovation. Markus Heyn, member of the management board and chairman of Bosch Mobility, at the International Motor Show in Beijing in 2026 stressed that the group has full confidence in local domestic demand and research potential, which is reflected in the concentration of resources and prioritization of the Chinese market. A symbolic proof of deepening cooperation and the shift from supplier-recipient relationships to a value co-creation model is the joint development with a Chinese manufacturer of a low-voltage power solution. This system was designed specifically to meet the growing demand for computing power in vehicles, which are becoming increasingly software-integrated and dependent on advanced electronic systems. This solution will be developed and put into mass production in cooperation with Chinese customers, illustrating a new paradigm of collaboration where technologies are co-designed from the ground up rather than merely adapted to local specifications.

In 2025 Bosch Mobility achieved sales in China at the level of 122.3 billion yuan, which translates to about 17.83 billion US dollars and represents an annual growth of 4.9%. Importantly, about 70% of these revenues were generated by Chinese brands, which proves that local manufacturers have become the main driving force of innovation and consumers of advanced solutions. Bosch supported about 300 models of Chinese brands entering foreign markets. This path of knowledge transfer – from China to the rest of the world – is groundbreaking because it reverses the traditional direction of technology flow. For the German giant, China is currently the place where, outside Europe, the largest workforce engaged in the development of new technologies is located, and local R&D competencies, a global innovation network, and close cooperation with partners allow parallel development in electrification and intelligent transformation. Concentration on the local market and continued investment in expanding technological reach prove that the future of the automotive industry will be shaped in Chinese laboratories and production halls, and business success will depend on the ability to integrate with the local innovation ecosystem.

China–Saudi Arabia Strategic Partnership and the Rise of a Multipolar Innovation Economy

Economic and technological cooperation between China and Saudi Arabia constitutes another pillar of the new architecture of global value chains, based on mutual transfer of competencies, long-term partnerships, and a strategic development vision. Rayan Al Amoudi, executive director for strategy and business development at Nesma Infrastructure & Technology and chair of the China-Saudi Arabia Technological Innovation Center, points out that bilateral relations long ago exceeded the boundaries of trade and engineering contracts and have evolved toward cooperation encompassing technology transfer, production localization, joint investments, digital transformation, and AI development. The Saudi firm focuses with Chinese partners on areas such as smart cities, critical infrastructure, energy, and digitization of operational processes, which perfectly align with the national modernization agenda. The contemporary Saudi market no longer seeks only ready-made imported products for Saudi Arabia but expects technology to come with the partner, enabling the building of local competencies, knowledge transfer, and independence from a pure consumption model. The pace of corporate cooperation has significantly accelerated, and Chinese technology companies, such as Huawei, have made a deep impression with their expansion, solution quality, and ability to deliver complete systems. Local perception of Chinese technology has markedly improved: more and more government institutions and companies realize that they offer an optimal price-to-quality ratio, fully capable of meeting the requirements of advanced infrastructure and digital projects.

Looking to the future, Saudi Arabia and China see strong cooperation opportunities in green infrastructure, water treatment, digital transformation, and AI data centers. Saudi Arabia’s geographic, energy, and political advantages make it highly competitive in building regional artificial intelligence hubs, and local firms expect to play a larger role in these projects by leveraging Chinese experience and technologies. Saudi Vision 2030 proves highly compatible with China’s Belt and Road Initiative, and deepening exchanges in technology, industry, education, and people-to-people contacts opens broad prospects for economic cooperation based on mutual gain and long-term stability.

The global economic order is ceasing to be dominated by a one-way flow of technology and capital and is moving toward a networked, multipolar innovation ecosystem in which China evolves from the role of end producer to a strategic partner co-creating standards, funding research, and scaling solutions.

The dynamics of European investment and technological cooperation with China are taking on particular strategic significance in the context of growing trade tensions, export restrictions, and customs measures along the European Union – United States – People’s Republic of China axis. While Washington consistently tightens trade restrictions, imposes protective tariffs on Chinese goods, introduces anti-subsidy mechanisms, and promotes a “de-risking” strategy aimed at reducing dependence on Chinese supply chains in strategic sectors, the European Union is in a difficult position of balancing between protecting its own industry, implementing the Green Deal objectives, and maintaining access to key technologies and markets. European giants such as Philips and Bosch are not withdrawing from China; on the contrary – they are deepening localization of research, co-creating products, scaling innovations, and treating the Chinese ecosystem as a source of solutions exported globally. Customs actions and trade barriers may, in the short term, lengthen supply chains, raise operating costs, and force restructuring of business models. However, at the same time these same mechanisms compel companies to greater flexibility, production localization in multiple regions, diversification of partnerships, and investments in compliance with new climate and digital standards.

European investment in China, as well as partnerships with Middle Eastern countries, show that the future of global trade will not be based on isolation and protectionism but on managed interdependence, where tariffs, regulations, and technological standards will become negotiating tools and quality filters rather than absolute barriers. For companies this means the necessity of building resilient, multipolar value chains with operational redundancy and localization of key competencies. For the European Union – balancing between strategic autonomy and openness to cooperation that accelerates economic and climate transformation. For China – continuing the transformation toward a knowledge-based, innovation – and sustainability-driven economy that will constitute a stable pillar of the new economic architecture of the twenty-first century.

About IFIMES

IFIMES – International Institute for Middle-East and Balkan studies, based in Ljubljana, Slovenia, has special consultative status with the Economic and Social Council ECOSOC/UN since 2018. IFIMES is also the publisher of the biannual international scientific journal European Perspectives. IFIMES gathers and selects various information and sources on key conflict areas in the world. The Institute analyses mutual relations among parties with an aim to promote the importance of reconciliation, early prevention/preventive diplomacy and disarmament/ confidence building measures in the regional or global conflict resolution of the existing conflicts and the role of preventive actions against new global disputes.

View all posts by IFIMES →