AU

US Mint gold source tied to criminal networks in Colombia: NYT

The United States is increasingly being drawn into the opaque supply chains of illicit mining after an investigation by The New York Times tied some of its gold supply to Colombian criminal networks.

Drawing on interviews, trade records and field reporting, the NYT detailed how illegally mined gold in Colombia — often controlled by armed groups and drug cartels — is laundered through intermediaries and exported with seemingly legitimate paperwork before entering global supply chains.

In some cases, that gold made its way into the supply chain of the US Mint, which under federal law must use America-mined gold for its investor-grade coins.

The report highlights a fragmented chain of accountability. When questioned by a Times reporter, the US Mint blamed its suppliers, who then deflected the responsibility to other intermediaries. All parties maintained they had stopped accepting Colombian gold.

The US Department of the Treasury, which oversees the Mint, also denied the accuracy of these findings. A spokesperson also told the publication that buying foreign gold for investor coins does not violate the law.

At the same time, the NYT investigators noted that the Mint had long used a loose definition of “US gold,” allowing foreign material to qualify if offset by domestic purchases — a requirement that has not been enforced for more than 20 years, according to a 2024 federal watchdog report.

That year, roughly $1.5 billion of Colombia’s $4.1 billion gold exports ended up in the US, making it the largest single destination, according to trade data compiled by the United Nations.

Illegal gold in US market

The findings add to a growing body of evidence that illicitly mined gold has been penetrating formal US markets for years.

Previous investigations and enforcement actions have traced gold from Latin America — including Peru and Colombia — into North American refiners and traders, often after being mixed with legitimate supply and exported with falsified documentation.

Those cases have repeatedly exposed how difficult it is for downstream buyers to fully verify origin in a commodity that has such a long history in the global financial system. A World Wide Fund for Nature UK report earlier this year found that over 80% of financial institutions, including those in the US, were at risk of exposure to dealings with illegal mining for gold.

The latest findings also further highlight the persistent challenges in achieving full transparency in gold supply chains, as well as the limitations of existing oversight mechanisms.

Following the latest investigation, the Treasury said it is now reviewing the Mint’s procurement practices and has tightened its sourcing standards, the NYT report said.

The dead asset wakes up as crypto magic makes gold pay interest

Jewelers have long used a simple mechanism to protect themselves against volatile gold prices — borrow the precious metal rather than buy it outright.

It’s a trick with origins in antiquity and used from the gold souks of Dubai to the bullion desks of India, allowing artisans to produce and sell their wares before settling the tab to align costs with revenue.

If gold prices rise, the value of the rings and necklaces in the display case climbs with the debt. If they fall, both shrink together. The trade-off is interest on the loan.

Now, a jeweler, an asset manager and a fintech firm are wrapping this age-old wisdom in a crypto token, offering investors gold that actually pays a yield.

It’s an example of how digital technology is disrupting traditional finance. Gold has always been a “dead” asset, a store of value that, unlike stocks and bonds, pays no dividends or interest to its owner.

“For centuries, jewelers didn’t borrow paper money to buy gold, they borrowed the gold itself,” said Ivan Hoo, executive director at Singapore jeweler Mustafa Gold. “We are giving that ancient logic a sleek, synthetic upgrade.”

Mustafa has teamed up with FundBridge Capital which, in collaboration with tokenization platform Libeara, is offering investors digital tokens that track the price of gold.

The money FundBridge gets for selling its “MG999” tokens is lent to Mustafa, who pays 2.5% interest on the loan. Mustafa uses the money to buy physical gold and make jewelry.

Crucially, the loan is denominated in gold rather than cash. If Mustafa borrows $1 million, the debt is expressed as the amount of gold that sum could buy at prevailing market prices.

This means if gold prices rise, Mustafa’s repayment obligation increases — but so too does the value of its jewelry. If prices fall, the debt shrinks along with inventory value. The matching of costs and revenue helps to stabilize margins.

It’s a synthetic version of borrowing physical gold to avoid price risk.

Giving gold a yield

There’s an upside for investors too. They get exposure to gold but with the added bonus of yield derived from the interest Mustafa pays on the loan. After deducting management fees, FundBridge pays a 1% yield to token holders.

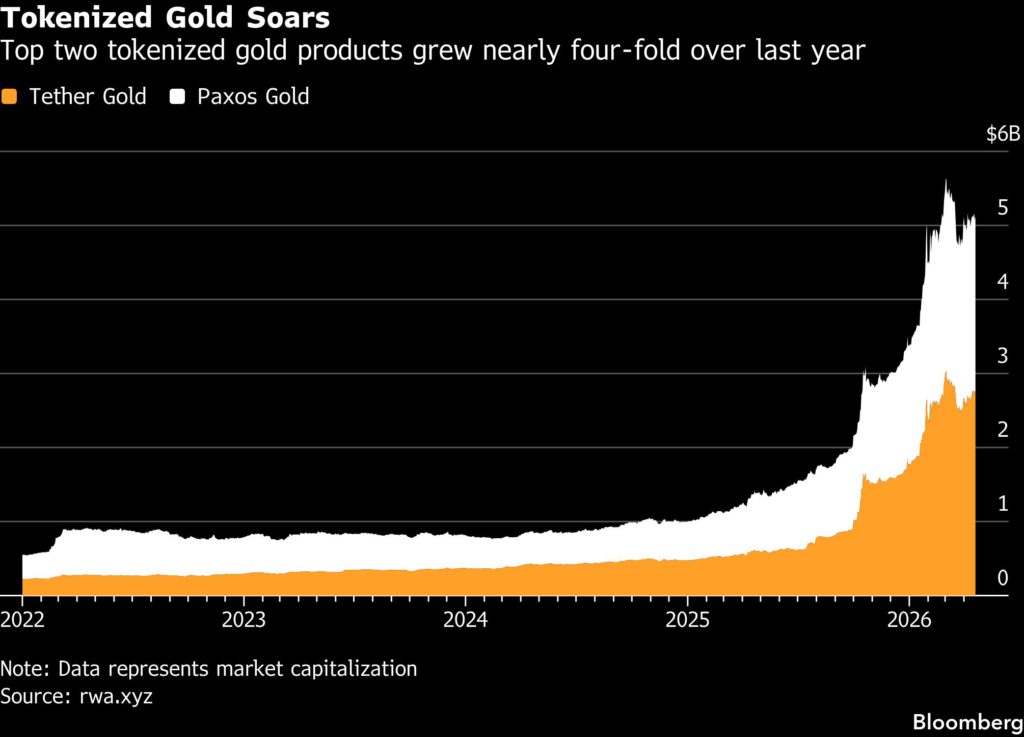

There are numerous ways to gain exposure to gold without holding the metal physically, from exchange-traded funds to futures, options and mutual funds. In the digital world, Tether Holdings SA and Paxos Trust Company offer tokens backed by gold.

But none of these directly offer investors a yield and some, such as ETFs, carry costs in the form of management fees, said John Bao Vu, chief portfolio manager at FundBridge.

“Typically, even though you get gold exposure, you get it in a negative carry sense,” he said. “We thought about doing something one step further to reduce that negative carry. This is how we came up with the idea with Mustafa.”

Gold lending, or leasing, has become more institutional and complex. Jewelers can manage risk with a mix of tools including gold loans, forward contracts and hedging programs, but smaller retailers are more likely to rely on ordinary bank financing.

For Mustafa, FundBridge is offering an alternative source of capital.

“Our biggest source of borrowing is from banks,” said Hoo. “But those loans are in US dollars, not denominated in gold terms. So this diversity of funding is good for us. It unlocks a fresh vault of capital from investors and meaningful diversification to how we fund the business.”

The price of gold has roughly tripled over the last four years as investors have sought safe havens amid heightened geopolitical uncertainty. Crypto firms have responded to that demand with more tokenized gold products.

FundBridge doesn’t need to hold any gold to maintain the value of its token. Instead, it is backed by the contractual claim against Mustafa — the right to receive back cash equal to a specific amount of gold at whatever the market price is at maturity.

To ensure the token is tied to the price of gold, the number on issue must maintain a prescribed ratio with the amount of outstanding loans.

“The price risk gets transferred to the investor in the fund,” said Vu. “They get the return (yield) as an upside while they take the exposure to gold-price risk. And the investors want to get exposure to gold.”

FundBridge has raised $15 million so far and hopes to reach $100 million initially. Working with a retailer like Mustafa, which requires a ton of gold a year, ensures quick deployment of the money.

“We are simply bringing this practice of borrowing on gold terms into the digital age,” said Mustafa’s Hoo. “What’s old is new again.”

(By Suvashree Ghosh and Yihui Xie)

Ghana directs Newmont, AngloGold, Zijin to shift mining ops to local firms by December

Ghana’s mining regulator has given international companies Newmont, AngloGold Ashanti and Chinese-owned Zijin until December 2026 to shift mining operations over to local contractors or face sanctions, according to five sources with direct knowledge of the matter and documents.

The three companies currently operate the mines with their own staff. They are the only ones still doing so after many firms outsourced mining operations ahead of Ghana, Africa’s top gold producer, revising local ownership rules in January 2025 and requiring all miners to switch to contract mining.

Under the rules, surface mining must be undertaken by fully Ghanaian-owned firms, while underground mining must be carried out by companies with at least 50% Ghanaian ownership.

Apart from Newmont, Zijin and AngloGold Ashanti’s smaller Iduapriem gold mine, almost all large miners in Ghana have already transitioned to contract mining, two government officials and three mining executives said.

African governments have been tightening mining rules to extract more revenue against a backdrop of rising prices for minerals and metals produced. Mali ended a near two-year standoff with Barrick in November over enforcement of its new mining code.

Ghana’s Minerals Commission asked Newmont, AngloGold and Zijin to fully comply with the contract mining requirements by December 2026, according to separate letters sent to the companies in October and January that were seen by Reuters on Wednesday. The three companies had separately requested extensions to allow full compliance.

The regulator warned that miners that failed to meet the deadline could face sanctions, the letters showed.

Zijin’s Ghana unit said it has been engaging with the Minerals Commission since November 2025 to comply with the local content rules, including preparing tenders and technical frameworks for a shift to contract mining, while rolling out new technologies that require initial benchmarking before a full tender process.

Newmont and AngloGold did not immediately respond to requests for comment.

Regulator rejects Newmont’s request

Newmont’s compliance was discussed during meetings this month in Accra between its global CEO, Natascha Viljoen, and the Minerals Commission after the company again sought an extension, the government sources said.

Newmont, which operates the Ahafo North and South gold mines, had asked to comply fully by 2027, citing additional regulatory and governance requirements it must satisfy as a listed company, one government official said.

But regulators rejected that request, noting that other listed miners, including Gold Fields, had already complied, the official said.

The Ghana Chamber of Mines did not respond to requests for comment but a source in the group said it was engaging with the commission.

“It is a good option, but we think it should be commercially driven,” he said. “If I can be more efficient, why shouldn’t I mine myself?”

The government sources said the new rules are aimed at building capacity among Ghanaian mining service companies and retaining more value in-country, citing the emergence of Ghanaian firms such as Rocksure and Engineers & Planners.

Local companies have the capacity to take on expanded contract mining roles and the commission will hold their hands to execute, the first government official said.

Miners that fail to comply face “a huge fine for the first step,” the second official said. “If they still don’t comply, we have the right to shut down the mine.”

(By Maxwell Akalaare Adombila; Editing by Veronica Brown and Nia Williams)