It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Colombia is becoming increasingly dependent on costly LNG imports as domestic natural gas production and reserves continue to decline.

A potential Super El Niño could reduce hydroelectric generation, increasing demand for gas-fired power and pushing energy prices even higher.

Rising gas costs, inflation, fiscal pressures, and weakening domestic production are creating significant economic and energy security risks.

Scientists predict 2026 will bring a devastating Super El Niño weather event, with rising temperatures and economically damaging droughts expected. There are fears the climate pattern will hit Colombia especially hard, triggering severe droughts that lower water levels and sharply reduce hydroelectric power generation. This will significantly pressure Colombia’s thermal power plants, already constrained by a natural gas shortage, while straining the electricity grid. As a result, costly natural gas imports will rise, adding pressure to Colombia’s fragile, fiscally strained economy.

Colombia first began importing natural gas in December 2016. Since then, the volume of liquified natural gas (LNG) shipments soared higher, despite rising prices. For 2025, it is estimated that around 18% of all natural gas consumed in Colombia that year was imported. Already for 2026, that number is ballooning out at a worrying rate. While earlier calculations predicted that around a quarter of Colombia’s natural gas would come from overseas, that amount has blown out to over 32% and is expected to climb further.

As a result, natural gas prices across Colombia are soaring, with LNG imports significantly more expensive than domestically produced dry gas. Between 2022 and 2024, prices surged by 36%, and despite attempts to mitigate the risks associated with rising natural gas imports, they continue to rise. Industry analysts estimate that natural gas prices in Colombia will rise by as much as 25% during 2026, further impacting businesses and households, with a spiraling cost-of-living crisis emerging.

This, in turn, will fuel further jumps in the inflation rate, which is already at a multiyear high. These developments are weighing heavily on an already fragile economy, which is fiscally vulnerable with the budget deficit at near historic highs of 6.4% of gross domestic product (GDP) at the end of 2025. It is anticipated it will blow out to 6.6% during 2026, which will make Colombia’s fiscal deficit the world’s third-largest.

Costly liquefied natural gas (LNG) imports are driving inflation higher, pushing up business and household costs because it is an essential commercial and domestic fuel. According to the government statistics agency DANE, Colombia’s monthly inflation rate hit 0.47% for May 2026, which translates to 5.84% on an annual basis. That marks the highest rate since 2024, when inflation was still easing after reaching a record 12.36% in 2023, driven by excess pandemic stimulus and a global price surge linked to COVID-19 lockdowns.

Colombia’s growing dependence on natural gas imports arose because of a marked decline in domestic production along with dwindling reserves of the essential fossil fuel. During April 2026, Colombia pumped 694 million cubic feet of natural gas per day, which was nearly 1% lower month over month and a worrying 15% less than a year earlier. That number is 36% lower than a decade earlier, underscoring the steep production decline of this economically vital fossil fuel from a period when Colombia was self-sufficient.

The decline is largely due to a lack of new discoveries and a substantial drop in output from Colombia’s Chuchupa and Ballena fields in the offshore La Guajira Basin. Production from the Chuchupa peaked in 2010, with over 90% of all recoverable hydrocarbons now extracted. The field will reach its economic limit in 2027, now accounting for a mere 1% of Colombia’s total natural gas output. Ballena’s output peaked in 2014, with production expected to continue until 2039, when analysts forecast that economically recoverable natural gas will be depleted.

These factors are responsible for declining production and a widening supply gap that will worsen if El Niño arrives in Colombia during the second half of 2026. Recent news that Colombia’s proven reserves of the essential fossil fuel have fallen again heightens the risks to its natural gas-dependent economy. According to Colombia’s petroleum regulator, the National Hydrocarbon Agency (ANH), proven natural gas reserves at the end of 2025 fell 17% year over year to 1.717 trillion cubic feet.

Source: National Hydrocarbon Agency (ANH).

This represents an 18-year low, with growing fears that Colombia’s proven natural gas reserves will continue to decline.

President Gustavo Petro’s short-sighted energy policies, which focus on significantly reducing Colombia’s dependence on fossil fuels, are a disaster for the country’s oil patch. Petro is Colombia’s first-ever left-wing president who, upon taking office on August 7, 2026, implemented a series of policies aimed at maximizing the benefits delivered by oil extraction while reducing dependence on fossil fuels. This included banning new exploration and production contracts, weighing heavily on drilling activity and foreign energy investment.

That is a key reason for the lack of new oil discoveries in Colombia, where there has not been a world-class discovery since the 1990s. This continues to weigh on the country’s hydrocarbon reserves. Petro’s decision to frequently hike taxes for energy companies and attempt to ban hydraulic fracturing, known as fracking, further contributed to the growing malaise in Colombia’s oil patch. Those policies, particularly regular tax hikes, saw many drillers operating in Colombia sharply slash spending in the country.

Some energy companies, like Exxon, chose to exit the country, seeing greater opportunity, security, and returns from any investment in other nearby countries, such as Guyana. Those developments are heavily impacting Colombia’s hydrocarbon production and reserves. The sharp impact of Petro’s regulatory and tax reforms on Colombia’s oil industry is magnified by rising lawlessness and violence in remote regions where many energy operations are located.

Since Petro took office, illegal armed groups have expanded their ranks, using his “total peace” policy as an opportunity to extend their territory, number of recruits and operations. Colombia’s security agencies estimate there are 22,000 members of various illegal armed structures across the country have 22,000 members. This is significantly greater than the 15,000 members reported for 2022 when Petro assumed office. This, along with rising coca cultivation and cocaine production, is responsible for a sharp uptick in violence in many rural regions.

Colombia’s growing dependence on ever-larger volumes of costly imported natural gas presents a considerable risk to a fragile economy, already buffeted by structural issues and serious headwinds. This will not only drive inflation higher, forcing Colombia’s central bank to keep interest rates higher for longer, but it will also negatively affect industry and agriculture, where natural gas is an important low-cost source of energy. There is also the very real risk of a sharp drop in electricity supply, further impacting the economy.

By Matthew Smith for Oilprice.com

Wednesday, June 17, 2026

Op-Ed: U.S.-Iran Ceasefire Deal is a Costly Return to Prewar Conditions

The deal does not address the nuclear issue, and further negotiations on Iran's uranium enrichment will be as fraught as ever

Centrifuges used in uranium enrichment at an Iranian nuclear facility (file image courtesy AEOI)

Shehbaz Sharif, the prime minister of Pakistan, which served as the key negotiator between the U.S. and Iran, announced on June 14, 2026, that the two sides had agreed on a deal to end the war. It will be officially signed on June 19 in Switzerland.

President Donald Trump announced it on Truth Social as a triumph, claiming that the Strait of Hormuz is open for everyone, the U.S. blockade has been lifted, and the oil is flowing again. What Trump did not mention was Iran’s nuclear program and what happens to its enriched uranium stockpile, one of the main reasons cited for starting the war. The nuclear issue – along with core issues such as ballistic missiles and Iran’s proxies – has been deferred for 60 days.

This raises two important questions: What was the war actually for? And what did the U.S. achieve? As an international and nuclear security expert, I believe the answer is nothing – and in the process the U.S. lost credibility as a negotiating partner.

Why the nuclear question is the hardest

The “rationalist theory of war,” as developed by political scientist James Fearon in 1995, identifies three problems that drive states to war when they would prefer to reach a deal: incomplete information about each other’s resolve; the inability to credibly promise a deal or commitment; and what international relations scholars call the indivisibility problem – when the thing in dispute cannot be split or shared, because it leaves no middle ground to settle on.

The war clarified the first reason. Each side saw what the other would actually do – how much force the U.S. was willing to use and what Iran could absorb while still staying in the fight. What the war could not solve was the nuclear commitment problem. And this goes far back between the U.S. and Iran.

Iran adhered to the 2015 Joint Comprehensive Plan of Action [JCPOA], the landmark nuclear deal that restricted Tehran’s nuclear program. The International Atomic Energy Agency verified that Tehran kept uranium enrichment to 3.67% and its stockpile under 300 kilograms – a concentration used to fuel a power reactor but far too low for a weapons program.

But the U.S. walked away in 2018, and Trump later called it “the worst deal ever” over its sunset clauses and on its silence on Iran’s ballistic missiles. Iran returned to negotiations in 2025, and the U.S. and Israel bombed Iran while those talks were still taking place. Similarly, in February 2026 the negotiations were ongoing and a deal was within reach when Israel and the U.S. struck Iran – killing Supreme Leader Ali Khamenei and lead negotiator Ali Larijani.

The U.S. has demonstrated a record of reneging on its deals and breaking the negotiating process. Which is why Iran now insists on guarantees and demands sanctions relief before signing a deal, and not just good faith.

A state that previously kept its commitments and was still bombed has little reason to accept promises of relief in the future. For this reason, I believe the 60-day deferral is a window for Tehran to watch whether the U.S. and Israel will hold the ceasefire on all fronts, including Lebanon.

The third problem of indivisibility – when the thing or issue in dispute can’t be split or shared – is why the nuclear question is the hardest. Most disputes can be split. Sanctions, for example, can be lifted by degrees. Even a nuclear program can be split, which the world saw in the Joint Comprehensive Plan of Action deal, with centrifuges counted, enrichment capped and a stockpile metered.

What cannot be split is the U.S. demand for zero uranium enrichment and Tehran calling uranium enrichment a sovereign right.

A deal, a war and a ceasefire

The 2015 nuclear deal also limited Iran’s centrifuges – the machines that do the enriching – and placed Iran’s nuclear program under the most intrusive inspections, all in exchange for sanctions relief. The nuclear question was not part of the 2015 deal – it was the actual deal.

During the June 2025 negotiations with Iran, and again in February 2026, the U.S. position was about the nuclear program, but in the opposite direction from the Joint Comprehensive Plan of Action. It was not about limits but the total elimination of Iran’s nuclear program.

In both rounds of talks in 2025 and 2026, Washington’s envoy, Steve Witkoff, demanded zero enrichment and the dismantling of Natanz, Fordow and Isfahan – Iran’s three most important nuclear sites. Iran called enrichment a sovereign right and refused.

Both rounds of negotiations ended in bombings.

The current deal to be signed on June 19 does not put a cap on Iran’s enrichment, nor does it discuss the elimination of its nuclear program. It ends the fighting, reopens the Strait of Hormuz and consigns enrichment, the stockpile, missiles and Iran’s regional proxies to 60-day negotiations.

In a recent New York Times interview, Trump said he was in no rush to remove the near-bomb-grade fuel still buried under the bombed sites. He claimed Iran would suspend enrichment for 15 or 20 years and enrich only for nonmilitary purposes.

In the Joint Comprehensive Plan of Action deal under President Barack Obama, the nuclear question was addressed where 97% of Iran’s stockpile was shipped out of the country and the cap was a verified fact.

Because it doesn’t address any of these issues, the Trump deal is a ceasefire agreement, not a nuclear agreement.

A costly return to the status quo

Going back to the bargaining theory, we know the war settled the information problem – it revealed what each side would endure.

The commitment problem remains. Neither side can yet make a promise the other believes, least of all an Iran whose negotiators were killed.

And I believe the indivisibility problem is now worse. The question of zero enrichment versus a sovereign right cannot be split. The current 60-day deferral is not a resolution. It is the same unsolved problem with a clock attached.

The one thing that could change is American restraint. If Washington holds Israel from striking Iran and Lebanon, it can slowly rebuild its credibility that was destroyed by the two wars. And that is a real challenge for the Trump administration.

Even as the deal was being finalized, Israel struck Beirut, the kind of action that can derail any talks.

In my view, the 60-day window should be read not as the path to a settlement but as the interval or pause before the next one fails. I argued in April that this conflict would not end in a clean settlement but in a series of contested pauses. The deal to be signed on June 19 is the first of them.

Iran emerges with its enrichment knowledge intact, its stockpile buried and fresh reason to believe that only a nuclear weapon would have deterred the U.S.-Israel attack.

But Iran also knows that it stood its ground and was able to strike U.S. bases and allies in the region. It has discovered leverage it did not previously know it held. The Strait of Hormuz has proved a better deterrent than the nuclear bomb.

The strait is open, the oil is flowing, and the question the war was fought over sits exactly where it began. Thousands of lives were lost to arrive back to square one. Nobody has won, though both sides will say they did.

Farah N. Jan is a political scientist and Senior Lecturer teaching in the International Relations Program at the University of Pennsylvania.

This article appears courtesy of The Conversation and may be found in its original form here.

The opinions expressed herein are the author's and not necessarily those of The Maritime Executive.

It is clear now that even if an agreement is signed between the United States and Iran imminently, it will only establish an agenda to be negotiated over the next few months. Israel is not party to the potential agreement and has the capacity to act independently should negotiations proceed in a way that jeopardizes Israeli national security. There are also a series of contentious issues that could cause any extended ceasefire to break down should the negotiations reach an impasse. During the negotiations, both the United States and Iran, for different reasons, will want to maintain progress — but Iran faces far greater economic, fiscal and, ultimately, political peril if the negotiations were to collapse, because it is in imminent danger of losing the oil revenues that have so far kept its government machine running.

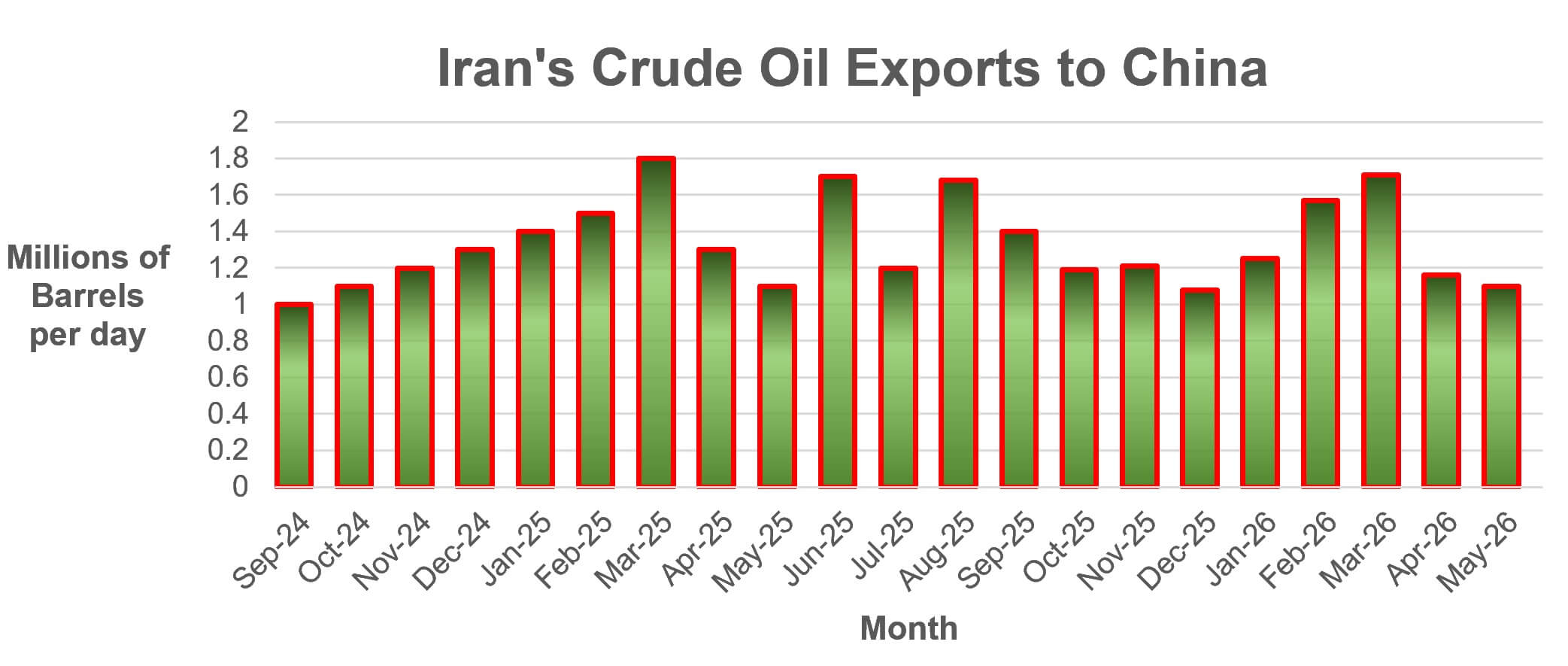

After the US Navy imposed its blockade on Iranian ships and ports on April 13, Iran was able to continue selling oil — not only from the stockpile it had built up for just such a contingency, but also from laden ships that were still on their way to import terminals in China. These ships have mostly discharged, and Chinese importers are now drawing heavily on the Iranian reserves held afloat in Asia.

China has for many years bought about 90% of Iranian oil exports. Chinese purchases over the last month have fallen considerably, and what China has bought has come almost entirely from the stock built up before the war and held afloat off China and Malaysia. (CJRC/Kpler data)

According to Kpler statistics, Iranian oil stocks held afloat appear to have declined from 192 million barrels in mid-April to about 140 million barrels at the end of May, of which about half is trapped inside the US naval blockade. The roughly 50-million-barrel drawdown over the last month appears to have come almost wholly from the stock held afloat off Malaysia and China.

If this trend continues through June, and another 50 million barrels are taken from the stock off Malaysia and China, then that reserve will be nearing empty. The Iranians are in trouble whatever transpires, as even if oil afloat within the US blockade is released, it will still take time to ship it to Asia. Any delay in reopening the Strait and lifting the blockade will merely prolong the damage to Iranian revenues and make matters even worse.

Whether the blockade is lifted or not, Iran is therefore likely to start suffering significant financial pressures by the end of June, unless it can persuade its friends to extend it credit. A shortage of revenue affects the ability of the Iranian government to soften the impact of the war on Iranian consumers by offering increased subsidies and handouts, which are important factors in maintaining social stability. In resolving the situation, the Iranians can no longer depend on the guile of their dark fleet operators and sanctions evaders; the US Operation Economic Fury is making it a much more perilous undertaking to evade US sanctions, and in the offing are further seizures of Iranian oil held afloat in sanctioned tankers or blockade runners.

Reinforcing this picture, there have been no substantial loadings at Kharg Island for several weeks now. At the Kooh Mubarak Single Point Mooring, no tanker has been seen loading since June 1, reflecting only sporadic use of the facility and probable restrictions on the flow of crude reaching the terminal from the collection point at Goreh in Bushehr Province.

Others will be affected, but not to the degree that Iran will. Oil consumers, suffering from the loss of 14 million barrels per day of oil that used to come through the Strait of Hormuz, appear to have adjusted to the shortfall, which has been compensated for by US reserve drawdowns and by the rise in price, which has curbed demand. China does not appear to have used much of its strategic reserve and has enough to keep going without major economic upset for several more months; in any case, China generates about 85% of its energy needs from its own internal resources, including nuclear, coal and wind power. Supply of LNG, where demand is more inelastic, presents more of a problem if the Strait stays closed for longer, but traders in London think current prices have not yet risen high enough to bring about significant demand destruction — in other words, the market can still absorb more difficulties ahead.

Within Iran itself, these difficulties are not being aired publicly. Instead, Paydari and IRGC hardliners have been ramping up their bombast and defiance in a coordinated propaganda campaign, to disguise the danger and to bolster the Iranian negotiating position. This should not be interpreted as confidence, but rather as an awareness of what peril lies ahead unless a settlement can be achieved quickly with the United States, whose negotiating position is much stronger than is generally assumed.

Column: Is the Iran war just an energy shock – or a turning point?

(The views expressed here are those of the author, Clyde Russell, a columnist for Reuters.)

The Iran war’s disruption to global crude oil and LNG markets is already being measured in lost barrels and higher prices. Now, with a US-Iran peace deal expected to reopen the Strait of Hormuz, the reckoning begins: was this a watershed moment, or merely another blip?

Consider two precedents.

The Volkswagen “Dieselgate” scandal over rigged emissions tests in 2015 seemed innocuous at first, but signalled the demise of diesel passenger cars and the rise of electric vehicles (EVs).

By contrast, Russia’s 2022 invasion of Ukraine caused a dramatic surge in energy prices, yet the market’s ability to reroute flows and absorb the shock meant the impact proved short-lived.

Certainly, the market has so far worked its magic in dealing with the effective closure of the Strait of Hormuz since the US-Israeli attacks on Iran began on February 28.

At least 1 billion barrels of crude oil and refined products have been lost from Middle East producers such as Iraq, Kuwait, the United Arab Emirates and Iran itself.

As much as 20% of global liquefied natural gas supply is also trapped in the narrow waterway between Iran and Oman.

A combination of strategic and commercial inventory releases and a dramatic reduction in imports by China, the world’s biggest crude importer, has helped keep benchmark Brent crude futures under $100 a barrel for much of the current crisis.

It could also be argued that optimism about a deal to reopen the Strait has played its part, with traders seemingly willing to believe President Donald Trump’s numerous social media posts that an agreement was imminent.

That long-awaited deal began to materialize on Sunday when the US and Iran announced they had agreed on a framework that could allow vessels to resume transit. By Monday, Trump said oil tankers were starting to move out of the Strait.

While full details of the agreement have yet to be publicly revealed, the prospect of tankers soon entering and exiting the waterway without hindrance raises the question of what happens next.

The first effect would be a short-term sugar hit of relief for energy markets as tankers trapped in the Gulf exit and deliver cargoes.

This would be followed by efforts to restore flows and supply chains to pre-war levels, and by the longer process of rebuilding depleted inventories.

This could mean crude oil and LNG prices stay higher for longer as the lost barrels are replaced, but much will depend on how rapidly Middle East producers are able to ramp up output and exports, and whether the OPEC+ group is actually able to pump the higher volumes it has agreed to produce.

Behaviour changes?

But the bigger question is what the long-term impact will be.

Much will depend on the view taken by both consumers and governments, especially in energy-hungry Asia, the fastest-growing region.

Consumers who have the ability to change are likely to consider switching to electric or hybrid vehicles to insulate themselves from future diesel and gasoline price shocks.

An early snapshot of how this may look is provided by Australia, the world’s biggest importer of diesel and a country reliant on overseas refineries for over 80% of its fuel requirements.

Australian EV sales hit a record high in May, with a market share of 20%, and when combined with hybrid vehicles, the share climbed to 46%.

This is approaching levels in China, the leading EV manufacturer, where EVs and hybrids accounted for more than 50% of sales in 2025, and rose to 60% in May this year.

Government policies are also likely to shift in favour of boosting renewables and electrification over fossil fuels.

Dieselgate saw the motor fuel fall out of favour, especially in Europe, where its share of passenger car sales dropped from around 52% in 2015 to under 10% by 2025.

Asian countries such as Vietnam are already putting in place policies to encourage EVs and electric scooters, and that momentum is likely to grow across the region.

LNG is also at risk in Asia as countries weigh the security risks of an imported fossil fuel against buying solar panels, wind turbines and battery storage from China, or developing domestic industries with Chinese backing.

One fossil fuel that may emerge as a long-term winner from the current crisis is coal.

Countries with vast domestic reserves, such as China, India and Indonesia, will be tempted to keep using the fuel given its cost advantage and supply security, even if it makes reducing carbon emissions more challenging.

Importing countries may also deem coal a safer bet, given that the major exporters – Indonesia, Australia and South Africa – have traditionally been reliable suppliers and that shipments aren’t at risk from chokepoints like the Strait of Hormuz.

However, a long-term shift away from crude oil and LNG isn’t assured, as producers and exporters of these fuels are unlikely to take their demise lying down.

Getting people to forget the last crisis may be as simple as ensuring prices drop rapidly and stay low for an extended period. The early market reaction – with Brent tumbling 4% to $83 on the deal announcement – suggests that process may already be underway.

If diesel and gasoline vehicles are cheap to refuel and LNG can compete with coal and renewables, it’s possible that governments and consumers will forgive and forget the disruption and costs of the Iran war, much as they did after previous conflict-induced price spikes.

Search for Safety

War in the Middle East has offshore companies looking elsewhere.

(Article originally published in Mar/Apr 2026 edition.)

The world needs secure and reliable energy, now more than ever, and offshore E&P is one of the best ways to find it in the near term.

Energy companies have multiple options to shift future investments out of the shallow-water Arabian Gulf and into deepwater frontier regions where security risks are more manageable. Offshore oil and gas reserves are abundant along the continental margins of South America, West Africa and the Gulf of America – areas with the stability and political will to underpin development.

Now, with energy-consuming nations looking for long-term options to diversify oil and gas imports, offshore is well-placed to deliver – and profit.

KNOCKOUT PUNCH?

The ongoing conflict in the Gulf has had a substantial impact on oil production but may have longer-lasting effects on liquified natural gas.

Seaborne gas exports have to be loaded out at LNG liquefaction terminals, and the largest LNG complex in the world – Ras Laffan, the plant for Qatar's vast North Field offshore gas reservoir – was damaged by an Iranian missile strike. In one night, the attack on Ras Laffan reduced worldwide LNG export capacity by 13 million tons per annum, roughly three percent of the global total.

Repairs will take up to five years.

Luckily, the rest of the offshore industry is well-positioned to step up and add more capacity over the same period. Major gas projects make up a large and promising share of the future offshore E&P portfolio overseas, even in areas better known for oil, like the eastern continental margin of South America.

ExxonMobil's Longtail FPSO is a case in point. Located in the prolific Stabroek Block lease area off Guyana, it will be able to process 1.2 billion cubic feet of gas per day, more than any FPSO ever built. Next door, in the thriving Brazilian offshore market, Equinor is investing $9 billion to develop the massive Raia gas find in the Campos Basin. It's the Norwegian oil major's largest overseas project ever and upon completion will supply about 15 percent of Brazil's domestic natural gas needs.

FLNGs TO THE RESCUE

Shipyard-constructed FLNGs (floating liquefied natural gas facility) will go further towards filling demand for transportable, tradeable natural gas. FLNGs are massive offshore vessels designed to extract, liquefy, store and offload natural gas directly over a gas field at sea.

Rystad Energy forecasts that FLNG capacity will quadruple in ten years from 14 mtpa in 2024 to 55 mtpa in 2035. That extra boost alone will zero out the loss of two trains at Ras Laffan.

FLNGs are smaller than onshore plants and have their own technical challenges, but they've matured as a practical solution to onshore challenges. A fully offshore liquefaction-plant footprint requires no export pipeline, no mobilization for onshore construction and less physical exposure to the local security environment on land – ideal for remote projects in the developing world.

FLNGs' security advantage has proven itself in the Rovuma Basin frontier gas region, some 40 nautical miles off Mozambique. Eni was first to market in the region by a wide margin with one FLNG in production and another nearing completion.

By contrast, TotalEnergies chose to build a mega-sized LNG plant on shore in order to export its planned production from the Rovuma Basin. The plant site is exposed to the security situation in northern Mozambique, and development has been set back by five years due to an Islamist insurgency. First LNG at the TotalEnergies plant will not arrive until 2029, ten years after its launch.

Due in part to the same security-related delays, Exxon is still short of a final investment decision for a neighboring Mozambican project after years of planning.

CLOSER TO HOME

Offshore gas has a major role to play in Europe's energy security, and future supplies could come from close to home, thanks to frontier developments in the Mediterranean.

Exxon and Chevron are making big moves to explore for gas off the coast of Greece and on an expedited timeline. New offshore gas supplies can't come too soon, according to Greek Energy Minister Stavros Papastavrou. "Europe thought that dependence meant stability and that Russian gas was cheap. But one can't call something cheap if it's not safe. And Europeans learned this the hard way," Papastavrou told a panel at this year's CERAWeek conference in Houston.

As the operator of Israel's Leviathan gas field and a partner in two others nearby, Chevron is already a leader in the Mediterranean. It's also the chosen E&P partner (with Qatari backing) for offshore gas exploration off Syria – a first for the country's energy industry and a sign of the American oil major's willingness to go first in politically-challenging environments.

The area could hold trillions of cubic meters of undiscovered gas deposits, just like the rest of the Levant Basin where exploration has turned up multiple supergiant fields. Syria is in dire need of revenue for rebuilding the local economy and is motivated to bring its first offshore gas project online by the end of the decade.

"Before the summer, God willing, we will start mobilization and drilling," Syrian Petroleum Company chief Youssef Kabalawi told AP in February.

FUTURE OPPORTUNITIES

Frontier offshore regions like these could become even more attractive to oil majors in the wake of the Gulf conflict.

Brent oil futures rose by nearly 60 percent in March and settled comfortably above $100 by the end of the month. If sustained, "higher-for-longer" prices would help make the business case for offshore projects in calmer parts of the world.

But for now, the offshore drilling industry is taking it slow, says ABS' Senior Vice President of Global Offshore, Miguel Hernandez: "Clients are controlling expenses and generating revenue with existing assets right now. We see forward progress, but companies are moving cautiously. Regionally, South America and West Africa remain the big focus areas. These are important regional hubs and the future of deepwater production."

For shipowners in the business of supporting offshore drilling and production – operators of subsea, offshore supply and offshore construction vessels – the current market sentiment is favorable, says Jake Scott, founder and managing partner at shipping investment firm Easterly Clear Ocean. Large numbers of offshore vessels are bottled up in the Arabian Gulf, with positive commercial effects for owners outside the region.

"The subsea guys and a lot of these offshore folks move equipment around as they need it to meet multiyear commitments," Scott explains. "All of a sudden that equipment is no longer available. When are you going to get it? So you're seeing greater optimism in the space. You're seeing more contracting outside the Gulf as a result."

ROBOTS AT WORK

Offshore projects depend heavily on economics and cost control, and improved technology is one of the fastest ways to get there.

From planning drill paths to maintaining platforms, the offshore energy industry is at the cutting edge of adopting industrial AI and automation. E&P firms recognize the value of digital automation for speed, standardization and labor-saving, including in the "red zone" of the drill floor.

Transocean's two "eighth generation" drillships are at the forefront of the trend.

The drill rigs aboard Deepwater Atlas and Titan are highly automated, and humans rarely need to enter the working area. "We now have robots working offshore on an ultra-deepwater drillship running a riser in 10,000 feet of water without a single person being involved on the rig floor apart from the driller," said Keelan Adamson, Chief Operating Officer at Transocean, in an interview during the first ship's debut.

It's not just about safer, more cost-effective offshore drilling. Automation is also driving efficiencies on production platforms by improving predictive maintenance and speeding up troubleshooting.

VROC, an industrial AI company with experience offshore, says that an AI maintenance management system's value is in providing decision support to engineers. By analyzing data from a panoply of equipment sensors all at once – vibration, pressure, temperature, electrical loads and more – the software can provide a platform's engineering team with a set of probable options for the root cause of a problem along with a detailed explanation of which sensor values are abnormal.

This speeds up the process of identifying the right fix, cutting downtime and potentially saving tens of thousands of dollars per day in lost production. BP is an early adopter of AI-driven maintenance prediction and troubleshooting in the U.S. Gulf and claims strong early results.

CLASS APPROVAL

The top class societies are fully on board with AI offshore and are lending their expertise.

"As the world embraces more digitalization, remote operations and AI," says ABS' Hernandez, "ABS is evolving our tools and services as well. This supports our clients by giving them better predictability and knowledge of their assets, which can add days of up time and greater value."

Getting the implementation right is the key, says DNV, which recently carried out a comprehensive AI safety review for Norway's offshore regulator.

Training an AI model to succeed in offshore asset management requires a high-quality maintenance dataset, carefully managed to ensure completeness and relevance. With buy-in and support from engineers, the model should be kept up to date in order to counteract drift between its original training and the state of current operations, DNV advises.

The opinions expressed herein are the author's and not necessarily those of The Maritime Executive.

Saturday, May 16, 2026

Suriname’s Delayed Oil Boom Is Finally Ready for Takeoff

Suriname’s offshore oil sector rebounded after years of disappointing drilling results and delayed investment decisions.

The $10.5 billion Gran Morgu project is expected to produce 220,000 barrels per day starting in 2028.

Low breakeven costs, favorable contracts, and growing regional gas demand are attracting new investment into Suriname’s energy sector.

The tiny impoverished South American country of Suriname has been battling for six years to launch a petroleum boom, which pundits believe will replicate neighboring Guyana’s oil rush. A combination of poor drilling results, high gas-to-oil ratio, and mismatched seismic data delayed the emergence of what could be South America’s last great offshore oil boom. Suriname’s favorable regulatory environment and low break-even prices, coupled with the recent price shock following U.S. and Israeli strikes on Iran, will drive greater investment in the country’s oil boom.

After a slew of poor drilling results, including dry wells, during the 1960s and 70s Big Oil abandoned the offshore Guyana Suriname Basin, believing it held very little oil potential. Consequently, the United States Geological Survey (USGS) determined the sedimentary basin held very little petroleum. According to a May 2001 agency report, the Guyana Suriname Basin held somewhere between 2.8 and 32.6 million barrels of undiscovered oil resources with a mean estimate of 15.2 billion barrels. This saw Big Oil ignore the sedimentary basin, with drillers focusing on Atlantic coast Africa and Brazil.

Nonetheless, in a surprise development at the time during 2015, global supermajor ExxonMobil made a world-class oil discovery with the Liza-1 exploration well in Guyana’s 6.6-million-acre offshore Stabroek Block. That discovery, in the territorial waters of the contested Essequibo region, surprised Big Oil and the global petroleum industry after decades of poor drilling results. Liza-1 was the first of a swathe of high-quality oil discoveries in offshore Guyana, with over 35 made in the Stabroek Block alone. Exxon estimates the prolific oil acreage contains at least 11 billion barrels.

Suriname’s big moment came in January 2020, when APA Corporation discovered oil with the Maka Central 1 well in offshore Block 58. This was followed by four more commercial discoveries in the 1.4-million-acre oil block.

Source: APA Corporation.

By the end of 2022, however, it appeared that Suriname’s burgeoning oil boom had hit a major roadblock. TotalEnergies, which was now the operator of Block 58, chose to delay the final investment decision (FID).

You see, a combination of a high gas-to-oil ratio at existing discoveries, poor drilling results, and mismatched seismic data deeply concerned the French supermajor. As a result, TotalEnergies and 50% partner in Block 58 APA Corporation delayed the FID in late 2022, alarming Suriname’s government in the capital Paramaribo. A rapidly deteriorating economy, coupled with rising civil unrest as the cost-of-living spiraled, sparked fears of a financial crisis for the deeply impoverished former Dutch colony.

That left Paramaribo hungrily eyeing neighboring Guyana’s massive oil boom, which catapulted the former British colony to South America’s wealthiest country based on gross domestic product (GDP) per capita. Nonetheless, in October 2024, TotalEnergies and partner APA announced the FID for the $10.5 billion Gran Morgu project in Block 58 offshore Suriname. The project is developing the Sapakara and Krabdagu discoveries, targeting a reservoir estimated to hold around 760 million barrels of crude oil.

Gran Morgu will be comprised of 16 production and 16 injection wells with a nameplate capacity of 220,000 barrels per day. As of April 2026, the project is reportedly 50% complete, with first oil expected in 2028. TotalEnergies is developing an all-electric low-emission facility, which is expected to have low greenhouse gas emissions of less than 16 kilograms of carbon dioxide emitted for every barrel of crude oil produced. This is lower than the estimated global average of 18 kilograms per barrel lifted and significantly less than heavy oil producers like Venezuela, where as much as 1,460 kilograms of carbon is produced for every barrel lifted in the Orinoco Belt.

Importantly for Paramaribo, Suriname’s national oil company, and industry regulator Staatsolie will control 20% of the Gran Morgu. The state-controlled oil company acquired a 20% operating interest in Gran Morgu for approximately $2.4 billion in 2025. This will significantly bolster the financial benefits received by Paramaribo once the project comes online and production reaches full capacity. It is estimated Gran Morgu will deliver up to $26 billion in income for the government, reinvigorating one of South America’s most impoverished countries, which, with a 2025 GDP per capita of $21,830, is the fifth poorest.

The Guyana Suriname sedimentary basin is proving to be one of the world's hottest offshore drilling locations, with Suriname shaping up to be potentially the last great oil frontier in South America. The Gran Morgu project and Block 58 are just the start of a larger hydrocarbon boom that will deliver a solid economic windfall for Suriname. There are currently 23 delineated and allocated oil blocks in offshore Suriname, as illustrated by the map below.

Source: Staatsolie.

The low breakeven costs for new oil projects, estimated to be $40 to $45 per barrel, along with favorable production sharing agreements, which at 30 contract years are among the industry’s longest, bolster the attractiveness of investing in Suriname.

Suriname’s next major hydrocarbon project will be in offshore Block 52, where Malaysia’s national oil company Petronas is the operator and holds an 80% working interest, with the remainder held by Staatsolie. A major natural gas project centered on the 2020 Sloanea-1 discovery is currently being planned after the November 2025 declaration of commerciality. Petronas plans to make an FID by late 2026 for the multibillion-dollar project, which couldn’t arrive at a more opportune time. You see, major regional natural gas producer Trinidad and Tobago is experiencing a significant decline in reserves and output, threatening vital regional supply.